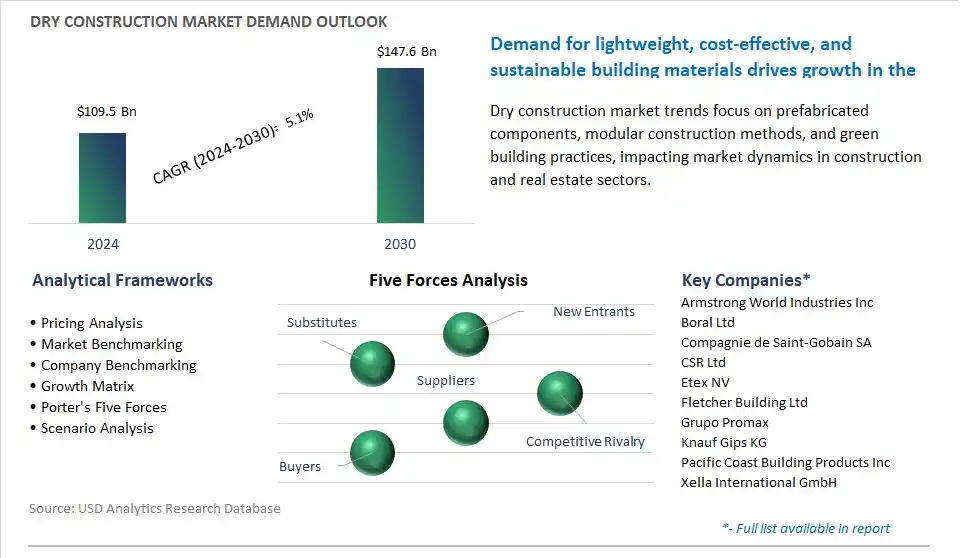

The global Dry Construction Market is poised to register a 5.1% CAGR from $109.5 Billion in 2024 to $147.6 Billion in 2030.

The global Dry Construction Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Material (Wood, Metals, Plasterboard, Plastic, Glass, Others), By System (Wall, Ceiling, Flooring, Others), By Application (Residential, Non-residential).

An Introduction to Global Dry Construction Market in 2024

The dry construction market is experiencing growth driven by the increasing demand for sustainable, cost-effective, and efficient building solutions in the construction industry. Key trends shaping the future of the industry include innovations in drywall systems, prefabricated components, and modular construction techniques to streamline construction processes and reduce project timelines. Advanced dry construction solutions offer benefits such as lightweight materials, ease of installation, and flexibility in design, allowing for rapid construction and customization in various building applications. Moreover, the integration of digital technologies, such as Building Information Modeling (BIM) and prefabrication automation, enhances precision, productivity, and quality control in dry construction projects. Additionally, the growing emphasis on green building certifications, energy efficiency, and waste reduction drives market demand for dry construction methods that minimize environmental impact and resource consumption. As architects, developers, and contractors seek to accelerate construction schedules, improve building performance, and minimize construction waste, the dry construction market is poised for continued growth and innovation as a preferred choice for modern construction projects.

Dry Construction Market Competitive Landscape

The market report analyses the leading companies in the industry including Armstrong World Industries Inc, Boral Ltd, Compagnie de Saint-Gobain SA, CSR Ltd, Etex NV, Fletcher Building Ltd, Grupo Promax, Knauf Gips KG, Pacific Coast Building Products Inc, Xella International GmbH.

Dry Construction Market Dynamics

Dry Construction Market Trend: Growth in Sustainable Construction Practices

The most prominent trend in the dry construction market is the growth in sustainable construction practices, driven by environmental awareness, regulatory mandates, and the need for energy-efficient building solutions. Dry construction methods, which involve the use of prefabricated components and minimal wet trades such as plastering and masonry, are inherently more sustainable than traditional construction methods due to reduced material waste, energy consumption, and construction time. As governments and industries prioritize sustainable development goals and green building certifications, there's a growing demand for dry construction solutions that minimize environmental impact, enhance energy efficiency, and improve indoor air quality. This trend is expected to drive market growth in the dry construction sector as developers, contractors, and building owners seek sustainable building alternatives.

Dry Construction Market Driver: Urbanization and Population Growth

A key driver in the dry construction market is urbanization and population growth, fueled by rapid urban migration, demographic shifts, and economic development in urban centers worldwide. As populations continue to urbanize and concentrate in cities, there's a corresponding demand for residential, commercial, and infrastructure construction to accommodate housing needs, commercial activities, and public services. Dry construction methods offer several advantages in urban environments, including faster construction timelines, reduced disruption to surrounding areas, and improved construction site safety. The need for efficient and cost-effective building solutions in densely populated urban areas drives demand for dry construction technologies and systems, sustaining market growth and driving innovation in the dry construction industry.

Dry Construction Market Opportunity: Adoption of Modular and Prefabricated Construction

The dry construction market presents a potential opportunity for the adoption of modular and prefabricated construction techniques, offering opportunities for efficiency, scalability, and customization in building projects. Manufacturers and contractors can capitalize on this opportunity by embracing modular construction principles, which involve assembling building components in controlled factory environments before transporting them to the construction site for assembly. Modular construction offers benefits such as reduced construction time, lower labor costs, and improved quality control compared to traditional onsite construction methods. Additionally, prefabricated building systems allow for greater design flexibility and customization, enabling developers to create unique and sustainable buildings tailored to specific project requirements. By promoting the adoption of modular and prefabricated construction, stakeholders in the dry construction market can unlock new opportunities for market expansion, accelerate construction timelines, and address the challenges of urbanization and population growth.

Dry Construction Market Share Analysis: Plasterboard segment generated the highest revenue in the industry

The plasterboard segment is the largest segment in the Dry Construction Market for diverse reasons. The plasterboard, also known as drywall or gypsum board, is one of the most commonly used materials in dry construction due to its versatility, affordability, and ease of installation. Plasterboard consists of a gypsum core sandwiched between layers of paper or fiberglass, providing excellent fire resistance, sound insulation, and thermal properties. Additionally, plasterboard is lightweight yet durable, making it suitable for a wide range of interior partitioning, wall lining, ceiling, and cladding applications in residential, commercial, and industrial buildings. In addition, plasterboard offers advantages such as smooth surface finish, dimensional stability, and compatibility with various finishing materials such as paint, wallpaper, and tiles, allowing for customized and aesthetically pleasing interior spaces. Further, the widespread availability of plasterboard products, standardized sizes, and construction techniques contribute to its popularity among architects, builders, contractors, and homeowners. As a result of these factors, the plasterboard segment dominates the Dry Construction Market, solidifying its position as the largest segment.

Dry Construction Market Share Analysis: Flooring Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The flooring segment is the fastest-growing segment in the Dry Construction Market for diverse reasons. The there is a growing demand for innovative and sustainable flooring solutions in both residential and commercial construction projects. Dry construction methods offer advantages such as faster installation, reduced construction time, minimal disruption, and ease of maintenance compared to traditional wet construction methods. Additionally, dry construction systems for flooring, such as raised access floors, laminate flooring, engineered wood flooring, and modular floor systems, provide flexibility, durability, and aesthetic appeal. These flooring solutions offer benefits such as sound insulation, thermal insulation, moisture resistance, and compatibility with underfloor heating systems, making them suitable for various indoor environments. In addition, advancements in flooring materials, technologies, and installation techniques contribute to the growth of the flooring segment in the Dry Construction Market. Further, the increasing focus on sustainability, energy efficiency, and occupant comfort drives the adoption of dry construction flooring systems that incorporate eco-friendly materials, recycled content, and energy-efficient features. As a result of these factors, the flooring segment is expected to experience rapid growth in the Dry Construction Market, solidifying its position as the fastest-growing segment.

Dry Construction Market Share Analysis: Non-residential Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The non-residential segment is the fastest-growing segment in the Dry Construction Market for diverse reasons. The there is a growing trend towards sustainable and efficient building practices in the non-residential construction sector, driven by factors such as environmental regulations, energy efficiency goals, and corporate sustainability initiatives. Dry construction methods offer advantages such as reduced construction time, minimal waste generation, and improved energy performance compared to traditional wet construction methods, making them attractive for non-residential projects. Additionally, non-residential buildings such as offices, commercial spaces, healthcare facilities, educational institutions, and industrial facilities have diverse and specialized requirements for interior partitions, ceilings, floors, and other dry construction systems. In addition, the increasing adoption of modular construction techniques and prefabricated building components in the non-residential sector drives the demand for dry construction systems that offer flexibility, speed, and cost-effectiveness in construction projects. Further, the growing focus on indoor environmental quality, occupant comfort, and wellness in non-residential buildings drives the adoption of dry construction systems that offer superior acoustic performance, thermal insulation, fire resistance, and air quality management features. As a result of these factors, the non-residential segment is expected to experience rapid growth in the Dry Construction Market, solidifying its position as the fastest-growing segment.

Dry Construction Market Report Segmentation

By Material

Wood

Metals

Plasterboard

Plastic

Glass

Others

By System

Wall

Ceiling

Flooring

Others

By Application

Residential

Non-residential

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Dry Construction Companies Profiled in the Market Study

Armstrong World Industries Inc

Boral Ltd

Compagnie de Saint-Gobain SA

CSR Ltd

Etex NV

Fletcher Building Ltd

Grupo Promax

Knauf Gips KG

Pacific Coast Building Products Inc

Xella International GmbH

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Dry Construction Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Dry Construction Market Size Outlook, $ Million, 2021 to 2030

3.2 Dry Construction Market Outlook by Type, $ Million, 2021 to 2030

3.3 Dry Construction Market Outlook by Product, $ Million, 2021 to 2030

3.4 Dry Construction Market Outlook by Application, $ Million, 2021 to 2030

3.5 Dry Construction Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Dry Construction Industry

4.2 Key Market Trends in Dry Construction Industry

4.3 Potential Opportunities in Dry Construction Industry

4.4 Key Challenges in Dry Construction Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Dry Construction Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Dry Construction Market Outlook by Segments

7.1 Dry Construction Market Outlook by Segments, $ Million, 2021- 2030

By Material

Wood

Metals

Plasterboard

Plastic

Glass

Others

By System

Wall

Ceiling

Flooring

Others

By Application

Residential

Non-residential

8 North America Dry Construction Market Analysis and Outlook To 2030

8.1 Introduction to North America Dry Construction Markets in 2024

8.2 North America Dry Construction Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Dry Construction Market size Outlook by Segments, 2021-2030

By Material

Wood

Metals

Plasterboard

Plastic

Glass

Others

By System

Wall

Ceiling

Flooring

Others

By Application

Residential

Non-residential

9 Europe Dry Construction Market Analysis and Outlook To 2030

9.1 Introduction to Europe Dry Construction Markets in 2024

9.2 Europe Dry Construction Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Dry Construction Market Size Outlook by Segments, 2021-2030

By Material

Wood

Metals

Plasterboard

Plastic

Glass

Others

By System

Wall

Ceiling

Flooring

Others

By Application

Residential

Non-residential

10 Asia Pacific Dry Construction Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Dry Construction Markets in 2024

10.2 Asia Pacific Dry Construction Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Dry Construction Market size Outlook by Segments, 2021-2030

By Material

Wood

Metals

Plasterboard

Plastic

Glass

Others

By System

Wall

Ceiling

Flooring

Others

By Application

Residential

Non-residential

11 South America Dry Construction Market Analysis and Outlook To 2030

11.1 Introduction to South America Dry Construction Markets in 2024

11.2 South America Dry Construction Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Dry Construction Market size Outlook by Segments, 2021-2030

By Material

Wood

Metals

Plasterboard

Plastic

Glass

Others

By System

Wall

Ceiling

Flooring

Others

By Application

Residential

Non-residential

12 Middle East and Africa Dry Construction Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Dry Construction Markets in 2024

12.2 Middle East and Africa Dry Construction Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Dry Construction Market size Outlook by Segments, 2021-2030

By Material

Wood

Metals

Plasterboard

Plastic

Glass

Others

By System

Wall

Ceiling

Flooring

Others

By Application

Residential

Non-residential

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Armstrong World Industries Inc

Boral Ltd

Compagnie de Saint-Gobain SA

CSR Ltd

Etex NV

Fletcher Building Ltd

Grupo Promax

Knauf Gips KG

Pacific Coast Building Products Inc

Xella International GmbH

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Material

Wood

Metals

Plasterboard

Plastic

Glass

Others

By System

Wall

Ceiling

Flooring

Others

By Application

Residential

Non-residential

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)