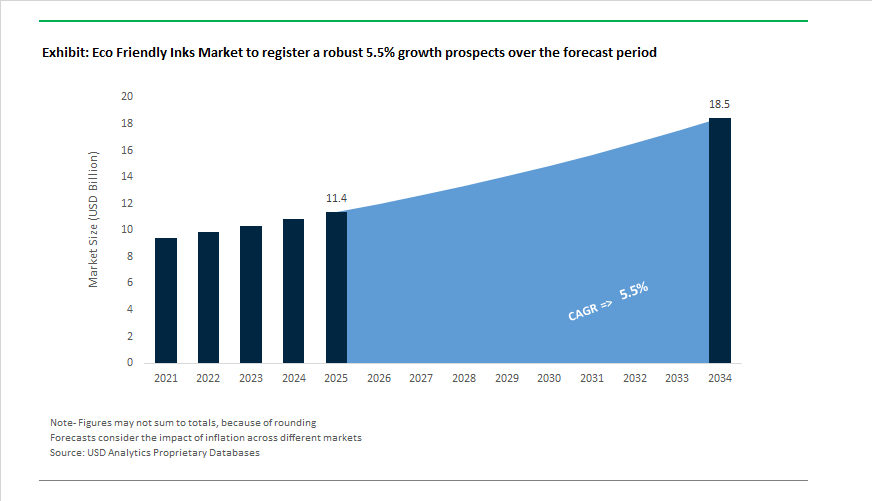

Eco Friendly Inks Market to Reach $18.5 Billion by 2034 at 5.5% CAGR as Circular Packaging and Food-Safe Compliance Accelerate

The Eco Friendly Inks Market is projected to grow from $11.4 billion in 2025 to $18.5 billion by 2034, registering a CAGR of 5.5%. Growth is increasingly anchored in regulatory compliance for food-contact packaging, compatibility with mechanical recycling streams, and corporate decarbonization mandates across the global printing ecosystem. A milestone event occurred in February 2026, when Siegwerk became the first ink manufacturer to receive RecyClass technology approval for its SICURA Nutriflex UV/LED-curable inks on polyethylene films. This certification confirms full compatibility with colored PE recycling streams in Europe, removing a longstanding barrier to adopting UV-curable systems in flexible packaging circularity models.

Regulatory preparedness has become a competitive differentiator. In January 2026, Sun Chemical launched a complete portfolio compliant with the German Ink Ordinance (GIO), which enforces strict safety standards for substances used in food-contact materials. This pre-deadline compliance ensures packaging converters can transition away from migratory components without production disruption. Earlier, in October 2025, Siegwerk introduced mineral oil-free (MOF) ink systems for India’s pharmaceutical packaging sector, addressing risks of mineral oil hydrocarbon migration into medicinal products. These initiatives reflect the market’s pivot toward low-migration, non-toxic ink chemistries tailored to regulated applications.

Sustainability metrics are increasingly influencing procurement across FMCG and packaging value chains. Flint Group’s 2024 Sustainability Report, released in November 2025, confirmed a 34% reduction in greenhouse gas emissions since 2019. The company attributed progress to its PRISM framework and the expansion of water-based AQUACode and vegetable oil-based Novasens® PRIME ink series. Flint further strengthened its footprint in Asia by inaugurating a 9,000-square-meter water-based inks and coatings facility in India in August 2024, supporting the transition from plastic to recyclable paperboard packaging that requires repulpable, low-residue ink systems.

Corporate restructuring has also aligned with ESG-driven product innovation. Hubergroup was acquired by MAVNU Ltd. in April 2025, followed by the appointment of its first Head of Sustainability and the release of its inaugural sustainability report. In January 2025, Hubergroup launched the Dynamica eco-friendly series, formulated to be cobalt-free and mineral oil-free while maintaining high-speed commercial printing performance. INX International introduced Innova Plus NCF in May 2025, eliminating nitrocellulose to enhance mono-material recyclability and thermal stability in flexible packaging applications.

Digitalization and AI integration are emerging as complementary levers for reducing environmental impact. In November 2025, HP announced its fiscal 2026 AI-powered sustainability initiative, targeting optimized ink consumption, predictive maintenance, and waste minimization across managed print services. Parallel transparency efforts were reinforced when Sun Chemical earned a Silver EcoVadis rating in August 2025, ranking within the top 15% of chemical sector performers for sustainable formulation practices.

Upstream pigment consolidation also shapes eco-friendly ink performance capabilities. In October 2024, Sudarshan Chemical acquired the Heubach Group, combining global manufacturing scale with advanced sustainable pigment technologies. This consolidation strengthens the availability of high-purity, heavy-metal-free colorants required for next-generation water-based, UV-curable, and bio-based ink systems. The eco friendly inks market is increasingly defined by regulatory compliance readiness, recyclable substrate compatibility, low-migration chemistry, and ESG-aligned manufacturing investments across global printing supply chains.

Trends and Opportunities in the Eco-Friendly Inks Market

Mandate-Driven Shift to Carbon-Negative and NIR-Detectable Bio-Pigments

- One of the most disruptive trends in the eco-friendly inks market is the rapid commercialization of bio-based, Near-Infrared detectable pigments that directly address long-standing recycling bottlenecks. Traditional carbon black pigments absorb NIR light, rendering black packaging invisible to automated sorting systems and effectively excluding it from recycling streams. This technical limitation is now being eliminated.

- In December 2025, UPM launched Circular Renewable Black, the world’s first bio-based, carbon-negative, and NIR-detectable black pigment, produced at its EUR 1.3 billion biorefinery in Leuna, Germany. Derived from renewable lignin, the pigment enables black plastic and inked packaging to be correctly identified by sorting infrastructure, directly unlocking recyclability for one of the most problematic color segments in packaging. For converters, this translates into immediate Scope 3 emission reductions and compliance with circular packaging mandates.

- Regulatory alignment is accelerating adoption. The German Printing Ink Regulation, coming fully into force on January 1, 2026, imposes strict compositional controls on food-contact inks. In response, Flint Group reaffirmed in November 2025 that its AQUACode water-based ink series fully complies with the regulation, proactively removing substances targeted by the ordinance. This pre-emptive compliance strategy is becoming essential for uninterrupted access to European food retail supply chains.

- From a carbon accounting perspective, bio-based ink formulations are now delivering measurable negative footprints. Bio-polymer ink systems showcased by Braskem at K 2025 demonstrated a cradle-to-gate carbon footprint of minus 2.27 kg CO2e per kilogram, allowing brand owners to materially offset emissions at the packaging level rather than relying solely on downstream offsets.

Commercialization of Dual-Curing and High-Efficiency UV-LED Systems

- The shift away from mercury-vapor lamps toward UV-LED curing represents a structural transformation in the eco-friendly inks market. UV-LED systems reduce energy consumption, eliminate hazardous mercury, and enable printing on thin, heat-sensitive sustainable substrates such as recyclable polyethylene films and mono-material laminates.

- In July 2025, Sun Chemical launched SunCure Advance ECO, a range of UV sheetfed inks containing 25% to 30% bio-renewable content. These inks are engineered for press speeds exceeding 20,000 impressions per hour, demonstrating that eco-friendly LED-curable inks can match the productivity of conventional petroleum-based UV systems while lowering energy intensity.

- At Labelexpo Asia 2025, Flint Group showcased its EkoCure dual-curing technology, which allows converters to operate on both conventional UV and UV-LED platforms. This flexibility supports gradual capital transitions while delivering energy savings of 50% to 80% versus mercury lamps. Importantly, these systems enable high-quality printing on ultra-thin recyclable PE films, a critical requirement for downgauging strategies in flexible packaging.

- Investment momentum is increasingly tied to migration compliance. In 2025, INX International expanded its INXJet MDLM platform for metal packaging and beverage cans, addressing stringent food safety and durability requirements while reducing curing-related energy consumption. This underscores how UV-LED inks are becoming essential for food-safe, high-throughput packaging lines rather than optional sustainability upgrades.

Functional Inks Enabling the Paperization of High-Volume Packaging

- The global move to replace plastic packaging with fiber-based alternatives is creating a significant growth opportunity for functional, water-compatible inks and coatings. This paperization trend requires inks that deliver moisture, grease, and oxygen resistance while remaining fully repulpable and compatible with recycling systems.

- At Fachpack 2025, Heidelberg and Solenis unveiled an inline barrier-coating process integrated directly into the Boardmaster flexographic press. This innovation allows industrial-scale production of barrier-coated paper packaging, enabling plastic pouches to be replaced with recyclable paper formats without sacrificing performance.

- The paperization segment is forecast to grow at approximately 4.5% annually through 2030, driven by regulatory frameworks such as the EU Packaging and Packaging Waste Regulation and India’s 2024 Eco-mark Rules. These policies are standardizing circularity-by-design requirements and accelerating adoption of inks certified for clean de-inking, home compostability, and food-contact safety. Eco-friendly inks that do not contaminate paper recycling streams are becoming mandatory inputs rather than premium options.

Digital Textile Inks as a Near-Shoring and Zero-Waste Enabler

- In the textile sector, eco-friendly digital inks are emerging as a core enabler of near-shoring, on-demand manufacturing, and water conservation. Digital inkjet printing eliminates the water-intensive pre- and post-treatment steps associated with conventional dyeing, directly addressing one of the industry’s most severe environmental challenges.

- In May 2025, Kornit Digital introduced its Apollo high-throughput system at FESPA, bridging the productivity gap between analog screen printing and digital workflows. This capability enables apparel brands to near-shore production to Europe and North America, reducing lead times and cutting shipping-related carbon emissions while maintaining industrial-scale output.

- Pigment-based digital inks, such as Sun Chemical’s Xennia Sapphire platform showcased at ITMA Asia 2025, allow textile mills to eliminate water-intensive processing entirely. These systems significantly reduce chemical discharge and energy consumption, aligning directly with the EU’s 2025 Ecodesign for Sustainable Products Regulation.

- Industry bulletins released in November 2025 highlight an additional structural advantage: digital printing supports zero-waste design by applying color only where needed. This improves recyclability of textile offcuts and supports the 25% textile waste recycling mandates being implemented in major manufacturing hubs such as China, reinforcing digital eco-friendly inks as a foundational technology for circular fashion supply chains.

Eco-Friendly Inks Market Share and Segmentation Insights

Water-Based Inks Lead Sustainable Printing Technologies with Strong Market Penetration

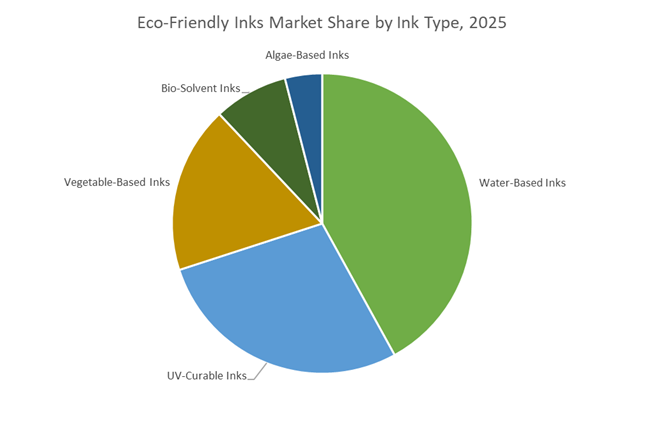

Water-based inks capture 42% of the global eco-friendly inks market share in 2025, driven by increasing regulatory pressure on VOC emissions and strong brand commitments toward sustainable packaging solutions. Their low environmental impact, food contact compliance, and adaptability across flexible packaging and corrugated substrates position them as the preferred solution for paper and board printing applications. UV-curable inks represent a rapidly expanding segment, offering zero VOC emissions, instant curing, and superior adhesion on non-porous materials such as films and labels. Vegetable-based inks, including soy and linseed formulations, maintain relevance in publication and commercial printing due to renewable content and efficient de-inking during recycling. Bio-solvent inks serve niche outdoor and signage markets requiring aggressive adhesion with reduced petroleum content, while algae-based inks remain an emerging innovation area aligned with circular economy initiatives and sustainable brand differentiation strategies.

Flexible Packaging Drives Demand for Low-VOC and Food-Safe Ink Solutions

Flexible packaging accounts for 35% of eco-friendly ink applications in 2025, reflecting accelerating sustainability commitments from global consumer goods brands. Water-based and UV-curable inks are widely adopted in snack food, pet food, and household product packaging due to low migration properties and regulatory compliance for food safety. Corrugated boxes and folding cartons represent a major segment supported by e-commerce expansion and demand for recyclable packaging materials. Labels and tags rely heavily on UV-curable and water-based inks for high-definition graphics and durability in food and beverage applications. Publication and commercial printing maintain a steady share with vegetable-based inks standard for newspapers and marketing materials where recyclability is prioritized. Textile and apparel printing is a growing application area, leveraging water-based pigment inks in digital textile printing to reduce water usage and support sustainable fashion production models.

Competitive Landscape of the Eco Friendly Inks Market

The Eco Friendly Inks Market in 2026 is defined by rapid innovation in low-migration packaging inks, water-based printing inks, UV-curable systems, and recyclable mono-material solutions, with leading players competing on circular economy integration, regulatory compliance, and sustainable pigment chemistry to serve food packaging, labels, and flexible packaging applications.

Circular economy driven UV and packaging ink leadership by Sun Chemical

Sun Chemical, part of the DIC Group, leads the global eco friendly inks market through its circular “5Rs” framework (Reuse, Reduce, Renew, Recycle, Redesign). The company’s SunCure Advance ECO UV inks for folding cartons and SunLam ultra-low monomer adhesives are rapidly replacing solvent-based systems in flexible packaging. In January 2026, Sun Chemical achieved full GIO compliance across its food packaging portfolio, strengthening exports to Europe. Its integrated model combines bio-pigments, water-based inks, and RecyClass-approved adhesives into a single sustainable packaging stream. Backed by DIC Group’s $7+ billion annual sales, sustainability-led products now contribute a growing double-digit revenue share, reinforcing Sun’s dominance in low-VOC and food-safe printing inks.

NC-free packaging inks and mono-material recycling focus at Siegwerk Druckfarben AG & Co. KGaA

Siegwerk positions itself as the industry’s circularity specialist, concentrating on recyclable packaging and labels. In February 2025, it launched its first nitrocellulose-free ink series for PE/PP surface printing, significantly improving mechanical recycling yields. The company scaled its SustainUP sustainable procurement program in India in early 2026, strengthening responsible sourcing across Asia. Siegwerk’s CIRKIT portfolio enables fiber-based cups, trays, and pouches to become water-resistant while remaining recyclable. Under its RethINK Packaging strategy, Siegwerk actively replaces multi-material laminates with mono-material structures compatible with existing recycling streams, making it a preferred partner for brands targeting food packaging sustainability and circular printing ink solutions.

Digital transformation and compostable ink innovation by Flint Group

Flint Group blends conventional and digital printing expertise with forward-looking chemistry aligned to the EU PPWR framework. Its TerraCode Bio Bag SX02 water-based inks are seeing strong 2026 demand in compostable and biodegradable retail paper bags. The Evolution Series de-inking primer allows labels to recycle alongside PET bottles, improving reclaimed material yield by 10%. Flint’s FlintLink B2B portal and VIVO Colour Solutions enable right-first-time color accuracy, reducing ink and substrate waste by up to 15%. With leadership in NC-free VertixCode and MatrixCode technologies, Flint delivers chemical stability at plastic recycling temperatures, strengthening its position in sustainable labels and eco friendly packaging inks.

LED-UV curing and food-safe ink expansion by Artience Co., Ltd.

Artience, formerly Toyo Ink SC Holdings, has pivoted toward value-added chemistry for electronics and sustainable packaging. In late 2025, Toyo Ink India announced a 1.5x capacity expansion in Gujarat, building a future export hub for eco friendly liquid inks. February 2026 saw Toyo Ink Europe introduce Steraflex UV inks meeting strict German GIO elution standards. Artience leads in LED-UV curing inks, reducing printing energy consumption by up to 50% versus mercury systems. Its EkoPro LED series supports low-migration, food-safe printing on paper and non-absorbent substrates, positioning Artience strongly in energy-efficient, regulatory-compliant packaging ink markets.

Cradle-to-cradle certified water-based inks from Hubergroup

Hubergroup has evolved into a chemicals and inks partner with deep backward integration into sustainable raw materials. Its DYNAMICA commercial inks and newly launched ELARA additives (February 2026) address performance demands across coatings and printing. Following its April 2025 acquisition by MAVNU Ltd., Hubergroup accelerated ESG initiatives, appointing its first Global Head of Sustainability. The company manufactures much of its own resins and additives in India, supported by a water treatment unit that reuses 60% of wastewater. With multiple Cradle to Cradle Gold certifications, Hubergroup delivers low-VOC, water-based inks optimized for material recirculation and sustainable packaging supply chains.

Germany (European Union): Compliance-Led Innovation and Circular Printing Systems

Germany is setting the regulatory and technological benchmark for the eco friendly inks market in Europe, with policy acting as a direct catalyst for formulation innovation. Effective January 1, 2026, the German Ink Ordinance mandates strict compositional compliance for all inks used in food contact materials. This requirement has accelerated a market-wide transition toward low-migration, mineral-oil-free, and toxicologically assessed ink systems, not only within Germany but across the wider European Union due to cross-border packaging supply chains. Ink producers are restructuring portfolios to ensure compliance with both GIO and global brand-owner standards, particularly in flexible and folding carton packaging.

Technology leadership is reinforcing this regulatory shift. In September 2025, Siegwerk showcased its SICURA Nutriflex LED/UV dual-cure systems, enabling up to 50% energy savings while maintaining compliance with food packaging standards from multinational brand owners. In parallel, updated REACH microplastics restrictions in late 2025 have forced the elimination of intentionally added microplastics from specialty inks. hubergroup responded with the Dynamica Ink Series, which is cobalt-free and mineral-oil-free, optimized for high-speed commercial presses. Sustainability performance has become a competitive differentiator, evidenced by Siegwerk’s placement in the 94th percentile of EcoVadis ratings in September 2025. Looking ahead, the EU Circular Economy Act expected in 2026 is driving adoption of wash-off ink technologies that improve recyclate purity, particularly in paper and plastic packaging streams.

United States: Circular Packaging, Bio-Based Inputs, and Operational Efficiency

The United States eco friendly inks market is being shaped by circularity requirements and voluntary sustainability frameworks rather than prescriptive federal mandates. In July 2025, Sun Chemical launched the SunCure Advance ECO UV series for folding cartons, incorporating 25 to 30% bio-renewable content and certified by the American Soybean Association. This reflects growing brand-owner demand for renewable raw materials in packaging inks, particularly in food, beverage, and personal care segments.

Recycling compatibility is emerging as a core purchasing criterion. Sun Chemical’s introduction of SunCure EcoPlast in mid-2025 addressed a critical bottleneck in plastic recycling by enabling UV offset inks to be washed off polypropylene and PET cups during post-consumer processing, in line with Association of Plastic Recyclers guidelines. Regulatory support is reinforcing this shift. The U.S. EPA expanded its Safer Chemical Ingredients List in 2025 to include 12 new bio-derived ink intermediates, encouraging substitution away from petroleum-based solvents. At the operational level, U.S. printers are investing in automated on-site blending systems such as MX12 dispensing units to reduce ink waste, lower VOC emissions, and improve color consistency, a trend expected to gain momentum through 2026.

India: Capacity Expansion Anchored in Policy and Textile Modernization

India’s eco friendly inks market is undergoing structural expansion driven by policy enforcement and infrastructure-led demand. In November 2025, Toyo Ink India, part of the artience group, announced a major capacity expansion at its Gujarat facility. The upgrade is designed to scale liquid ink output to 1.5 times current levels by 2028, primarily to serve the rapidly growing flexible packaging and label segments that are transitioning to sustainable ink systems.

Regulation is acting as an adoption accelerator. Active enforcement of the Ecomark Rules 2024 began in early 2025, redefining eco-label eligibility to favor inks with low VOC emissions and recyclable, plant-based inputs. In parallel, the government’s ₹4,445 crore investment in seven PM MITRA textile parks includes dedicated infrastructure for eco-friendly textile printing, structurally favoring water-based and bio-pigment inks. Industry engagement is reinforcing these trends. At Printpack India 2025, hubergroup introduced its Dynamica process series, highlighting fast-setting behavior and high dampening tolerance suited to India’s competitive commercial printing environment, where efficiency and sustainability are increasingly interlinked.

China: Scale-Driven Transition to Water-Based and Bio-Derived Inks

China remains the largest volume market for eco friendly inks, with growth increasingly shaped by environmental mandates and digital printing expansion. The Ministry of Industry and Information Technology has prioritized National Champion status for companies developing water-based pigment inks for digital textile printing. By Q4 2025, digital ink consumption in the Zhejiang cluster alone grew by an estimated 14 %, supported by zero-liquid-discharge mandates that make conventional dyeing and solvent-heavy inks economically unviable.

Publishing and packaging segments are also transforming. Under the 2025 Green Manufacturing Roadmap, major Chinese publishing houses have transitioned approximately 80% of offset printing operations to soy-based or vegetable-oil-based inks. This shift aligns with national carbon-neutrality targets and reduces reliance on imported petroleum-derived solvents. The result is a structurally higher baseline demand for bio-based ink formulations, positioning China as both a scale market and a manufacturing hub for sustainable ink technologies.

Japan: Recycling-Centric Innovation and Global Standard Alignment

Japan’s eco friendly inks market is characterized by precision innovation and regulatory harmonization. In 2025, Toyo Ink received the Japan Star Award for its peel recycling technology, developed with Lion Corporation. This system enables efficient removal of inks and adhesives from laminated films, significantly improving polyethylene film recovery rates and addressing a critical challenge in flexible packaging recycling.

Beyond technology, Japan is playing a strategic role in aligning eco-label standards globally. Japanese regulators and industry bodies have led efforts to harmonize domestic eco-labeling frameworks so that inks certified under Japan’s Green Star program are recognized within upcoming EU PPWR requirements and U.S. EPA frameworks for the 2026 trade cycle. This alignment reduces technical trade barriers and strengthens the export competitiveness of Japanese eco friendly ink formulations.

Eco Friendly Inks Market: Country-Level Strategic Snapshot

Eco-Friendly Inks Market County Level Snapshot

|

Country

|

Primary Driver

|

Key Application Focus

|

Strategic Direction

|

|

Germany

|

Food-contact regulation and circular economy

|

Packaging, commercial print

|

Low-migration, wash-off, energy-efficient inks

|

|

United States

|

Circular packaging and bio-based inputs

|

Folding cartons, plastics

|

Recycling-compatible UV and soy-based systems

|

|

India

|

Policy enforcement and textile parks

|

Flexible packaging, textiles

|

Capacity expansion in water-based inks

|

|

China

|

Environmental mandates and digital printing

|

Textiles, publishing

|

Scale-driven shift to water-based and bio inks

|

|

Japan

|

Recycling efficiency and standard harmonization

|

Flexible packaging

|

Peel-off inks and global eco-label alignment

|

Eco-Friendly Inks Market Report Scope

Eco Friendly Inks Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.4 Billion

|

|

Market Size (2034)

|

$18.5 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Ink Type (Water-Based Inks, UV-Curable Inks, Vegetable-Based Inks, Bio-Solvent Inks, Algae-Based Inks), By Printing Process (Flexography, Rotogravure, Digital Inkjet, Offset Lithography, Screen Printing), By Application (Flexible Packaging, Labels and Tags, Corrugated Boxes and Folding Cartons, Publication and Commercial Printing, Textiles and Apparel), By End-Use Industry (Food and Beverage, Pharmaceuticals and Healthcare, Cosmetics and Personal Care, E-Commerce and Logistics, Fashion and Decor)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sun Chemical Corporation, Siegwerk Druckfarben AG & Co. KGaA, Flint Group, Toyo Ink LLC, hubergroup, INX International Ink Co., Sakata InX Corporation, T&K TOKA Co., Ltd., Altana AG, Wikoff Color Corporation, Epple Druckfarben AG, Zeller+Gmelin GmbH & Co. KG, Kao Collins Corporation, Doneck Network, Solar Inks Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Eco Friendly Inks Market Segmentation

By Ink Type

- Water-Based Inks

- UV-Curable Inks

- Vegetable-Based Inks

- Bio-Solvent Inks

- Algae-Based Inks

By Printing Process

- Flexography

- Rotogravure

- Digital Inkjet

- Offset Lithography

- Screen Printing

By Application

- Flexible Packaging

- Labels and Tags

- Corrugated Boxes and Folding Cartons

- Publication and Commercial Printing

- Textiles and Apparel

By End-Use Industry

- Food and Beverage

- Pharmaceuticals and Healthcare

- Cosmetics and Personal Care

- E-Commerce and Logistics

- Fashion and Decor

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Eco Friendly Inks Industry

- Sun Chemical Corporation

- Siegwerk Druckfarben AG & Co. KGaA

- Flint Group

- Toyo Ink LLC

- hubergroup

- INX International Ink Co.

- Sakata InX Corporation

- T&K TOKA Co., Ltd.

- Altana AG

- Wikoff Color Corporation

- Epple Druckfarben AG

- Zeller+Gmelin GmbH & Co. KG

- Kao Collins Corporation

- Doneck Network

- Solar Inks Ltd.

*- List not Exhaustive