Electrochromic Glass Market Overview with Dynamic Light Control & Energy Efficiency Insights

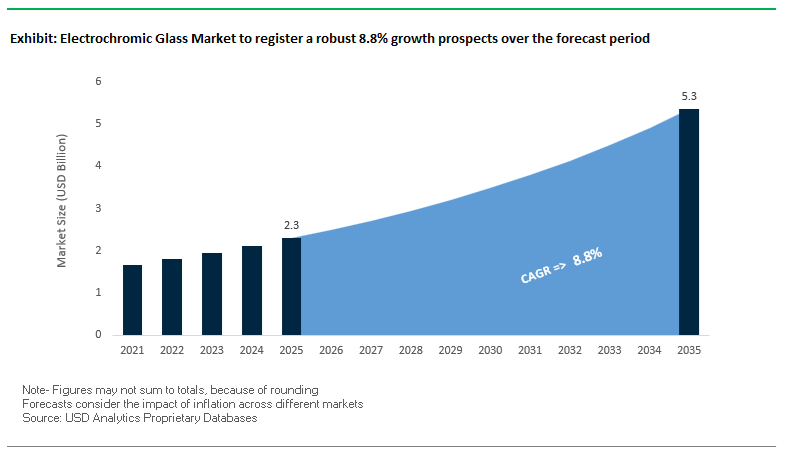

The global electrochromic glass market is projected to rise from USD 2.3 billion in 2025 to USD 5.3 billion by 2035, reflecting a strong CAGR of 8.8%. Market expansion is underpinned by the rapid adoption of smart windows, dynamic architectural glazing, and intelligent light-regulating solutions across commercial buildings, premium residential projects, and next-generation electric vehicles. As governments enforce aggressive energy-efficiency mandates and HVAC optimization becomes central to sustainable design, electrochromic glazing is emerging as a critical high-performance building technology.

For manufacturers, vendors, and façade-system integrators, growth is driven by the shift toward automated daylight management, ultra-low power electrochromic materials, and improved tinting uniformity targeting premium architectural projects. Advanced electrochromic windows can reduce HVAC loads by 19.8%–40.28%, while offering precise dynamic control of visible light transmittance—ranging from 45.4% in clear state to 0.3% in fully tinted mode. This performance advantage aligns directly with LEED certification, net-zero building design, and occupant wellness metrics.

Key Electrochromic Glass Insights for Manufacturers & Façade Vendors

- HVAC energy reduction of up to 40.28% through automated electrochromic window integration.

- Dynamic visible light modulation from 45.4% (clear) to 0.3% (deep tint) supports glare-free daylighting.

- Ultra-low power tint maintenance at approximately 50 mW/m², enabling long-term smart façade operation.

- Thermal comfort improvement with up to 4.5% extension in comfort time for building occupants.

- Near-infrared rejection reduces NIR transmission from 31.9% to as low as 2.6%, lowering SHGC and cooling loads.

Market Analysis: Strategic Moves Reshaping the Global Electrochromic Glass Industry

The electrochromic glass market is undergoing an accelerated transformation driven by innovation in dynamic glazing materials, new integration partnerships, and structural shifts within leading manufacturers. A defining trend is the industry’s shift from architectural glass alone to a broadening ecosystem that includes smart-home integration, automotive glazing, IoT-enabled dynamic facades, and scalable roll-to-roll manufacturing technologies.

Momentum is strong across architectural and mobility sectors. In February 2025, SageGlass launched RealTone™, the first electrochromic glazing engineered for a neutral color tint—addressing long-standing market critiques regarding bluish or greenish hues in earlier EC systems. In January 2025, Glaston partnered with Miru Smart Technologies to expand production capacity for next-generation eWindows, signaling a manufacturing scale-up necessary to support global demand growth. Meanwhile, AGC Inc. and Panasonic’s collaboration (January 2025) underscores rising adoption of EC technologies within smart homes and consumer electronics, broadening electrochromic applications far beyond façade glass.

Automotive adoption is rising sharply. In August 2025, NIO integrated electrochromic side windows into its ES8 SUV using Ambilight technology, spotlighting dynamic glazing in electric vehicles as a functional and comfort-enhancing feature. This follows Gentex Corporation’s strategic move in April 2025 to acquire Voxx International, expanding its automotive smart-glass and electronics footprint. These developments collectively reinforce the cross-industry relevance of electrochromic glass as OEMs seek glare reduction, adaptive privacy, and energy-efficient cabin temperature control.

The market also experienced notable restructuring. View Inc. filed for Chapter 11 bankruptcy in April 2024 and executed workforce reductions in October 2024, transitioning into a privately controlled company under lender oversight. This event altered manufacturing capacity and competitive dynamics, prompting new entrants and partners to accelerate R&D. Academic and industrial research highlighted in October 2025 demonstrated breakthroughs in chiral ferroelectric nematic liquid-crystal windows, achieving ultra-low-power tinting (~50 mW/m²), indicating future-generation EC technologies capable of outperforming current tungsten-oxide-based systems.

Next-Generation Trends Driving Grid-Interactive Smart Buildings and High-Durability Fast-Switching Electrochromic Systems

Market Trend 1: Deep Integration of Electrochromic Glass with BMS and IoT to Enable Grid-Interactive Efficient Buildings (GEBs)

A major trend reshaping the Electrochromic Glass Market is the rapid integration of electrochromic (EC) glazing into Building Management Systems (BMS) and IoT platforms to create grid-interactive efficient buildings (GEBs) capable of actively managing cooling loads, solar heat gain, and peak electricity demand. Energy simulation studies across North America demonstrate that EC windows controlled by BMS algorithms can reduce peak cooling electricity demand by 0.46–0.65 W/ft², significantly easing the load on HVAC systems during the most energy-intensive hours.

Dynamically modulated EC windows reduce solar heat gains by up to 88.9% compared to code-minimum static glazing. This substantial reduction in thermal loading allows building mechanical engineers to downsize HVAC system capacity by 25–58%, delivering meaningful savings in upfront CAPEX and long-term operational energy expenses.

Across cooling-dominant climates, EC-enabled façades deliver annual energy savings of 6–30 kWh/ft², cutting building energy consumption by up to 40% relative to static glass. Such performance positions EC glazing as a core technology in achieving net-zero building codes, peak demand management, and smart grid integration strategies.

Market Trend 2: Material & Fabrication Innovation Delivering Faster Switching and Automotive-Scale Durability

The second major trend involves breakthroughs in electrochromic material science and deposition processes that dramatically improve switching speeds, durability, and large-area uniformity. Traditional tungsten oxide (WO₃) films required >10 seconds to reach 90% of optical modulation, but next-generation nanostructured WO₃, including nanowire bundles and composite architectures, achieve <3.5-second coloration times and <1.1-second bleaching times, enabling real-time adaptive tinting in both buildings and vehicles.

High coloration efficiency (CE) is another critical metric for material utilization and low-power operation. Advanced WO₃ nanocomposites now reach 154.16 cm²/C, delivering significant optical modulation with minimal charge input.

Durability validation has also advanced: modern EC glass systems are qualified for 20–30+ years of operational lifespan, enduring tens of thousands of switching cycles with minimal optical drift. Improvements in layered sputter deposition, interface engineering, and ion-transport materials now allow production of large-format curved EC glass panels (up to 1.5 m × 1.6 m) with uniform tinting—key for automotive sunroofs, skylights, and complex architectural façades.

Commercial Opportunities in Automotive Smart Glass Integration and Low-Cost Printable EC Films for Mass Retrofit Markets

Market Opportunity 1: Acceleration of EC Sunroofs and Dynamic Privacy Glass Adoption in Automotive & EV Applications

The automotive industry presents a major commercial opportunity for EC glass, driven by cabin comfort requirements and EV efficiency targets. Modeling studies show that EC smart glass installed in an electric vehicle exposed to strong sunlight (33°C ambient temperature) reduces air conditioning cooling demand by 762 W, significantly lowering HVAC energy consumption.

For EVs, reduced HVAC load directly enhances driving range, and simulations estimate that EC windows can increase range by up to 33.1 miles under hot-weather conditions compared to vehicles using standard glazing. Thermal comfort also improves drastically: EC glass reduces the Standard Effective Temperature (SET) by ~7°C*, lowering perceived cabin temperature without relying on mechanical cooling.

In addition to comfort and energy efficiency, automotive EC glass provides ≥99% UV protection in all tint states, extending interior material lifespan and protecting occupants. As OEMs prioritize energy-efficient cabin conditioning, EC sunroofs and privacy glass are emerging as high-value differentiators for next-generation EVs, premium vehicles, and autonomous cabin designs.

Market Opportunity 2: Low-Cost Printable Electrochromic Films for Scalable Building Retrofit and Consumer Applications

A transformative opportunity is emerging through printable, solution-processed electrochromic films, which reduce cost and enable mass deployment in retrofit markets. Techniques such as screen printing and roll-to-roll (R2R) fabrication eliminate reliance on high-vacuum sputtering, slashing per-square-meter costs and making electrochromics viable for widespread building retrofit, consumer devices, and flexible substrates.

Organic EC materials such as PEDOT:PSS have demonstrated extremely high coloration efficiencies up to 352 cm²/C, surpassing many inorganic systems and offering exceptional optical modulation with minimal charge. 3D-printed flexible EC devices now achieve 1.6-second coloration and 0.6-second bleaching times—competitive with high-end inorganic EC materials but at a fraction of the manufacturing cost.

Breakthroughs in device architecture, such as self-powered EC systems integrating WO₃ and vanadium-doped nickel oxide, eliminate traditional ITO counter electrodes, enabling lower-cost, more flexible, and more durable designs. Printable EC technologies unlock new applications across smart home windows, consumer electronics, privacy panels, and low-cost window retrofits—positioning the segment as one of the fastest-growing opportunities in the electrochromic ecosystem.

Country Analysis: Global Drivers in the Electrochromic Glass Ecosystem

United States: Commercial-Scale Electrochromic Manufacturing and AI-Integrated Smart Building Deployment

The United States is the world’s most advanced commercialization hub for Electrochromic Glass, supported by large-scale real estate adoption, strong federal energy-efficiency incentives, and rapid integration with smart building platforms. View, Inc.’s $400+ million investment into its 800,000 sq. ft. Mississippi factory in April 2024 demonstrates a decisive commitment to industrial-scale Electrochromic Glass production, ensuring high-yield manufacturing capable of supporting airports, hospitals, universities, and corporate campuses. This capacity is critical as the company surpasses 90 million sq. ft. of installed smart windows, proving real-world scalability across complex, high-occupancy environments.

A defining advantage of the U.S. market is the convergence of dynamic glazing with AI-based building automation. View Smart Windows employ machine learning algorithms to adapt tint levels in real time, optimizing daylight availability while simultaneously minimizing HVAC loads—an essential feature for net-zero and LEED-certified building design. The U.S. Department of Energy (DOE) reinforces market momentum, estimating that dynamic glazing could save 1.9 quadrillion BTUs annually, driving federal, state, and commercial adoption. Participation in government-backed programs such as the GSA Green Proving Ground underscores the role of the U.S. as a proving field for advanced Electrochromic technologies, accelerating mainstream acceptance of AI-driven façade intelligence.

European Union (Germany/France): EPBD-Driven Net-Zero Renovation and Aesthetic-Optimized Dynamic Glazing Technology

The European Union—particularly Germany and France—remains a global leader in low-carbon building transformation, where Electrochromic Glass plays a pivotal role in meeting EPBD and European Green Deal requirements. Europe’s aggressive renovation agenda, aimed at upgrading nearly 75% of inefficient building stock, is propelling dynamic glazing into both new construction and deep retrofit markets. Electrochromic solutions offer a high-value pathway to comply with near-zero-energy building (nZEB) standards by reducing cooling loads, improving daylighting, and enabling automated solar control without mechanical shading.

European architectural preferences further influence product innovation. SageGlass’s COOL-LITE® ST BRIGHT SILVER launched in June 2024, introduced advanced reflective aesthetics combined with dynamic solar control, addressing the dual demand for energy performance and modern façade design. Regulatory emphasis on transparency and lifecycle impact is also accelerating material adoption. In September 2024, SageGlass released Environmental Product Declarations (EPDs) to support BREEAM, LEED, and national compliance frameworks. The February 2025 launch of RealTone™, marketed as the most neutral Electrochromic Glass available, solves a long-standing aesthetic challenge by preserving the appearance of traditional clear glazing while offering dynamic tint capability. These innovations highlight Europe’s leadership in combining sustainability, aesthetics, and performance.

China: High-Volume Electrochromic Manufacturing Expansion and EV-Driven Smart Glazing Adoption

China is rapidly scaling into a major production and application center for Electrochromic Glass due to its manufacturing capacity, fast-growing EV sector, and heightened investment in smart building materials. The surge in China’s EV industry is directly boosting demand for Electrochromic glazing in smart sunroofs, privacy windows, and adaptive rearview mirrors, all designed to reduce heat absorption, lower air-conditioning loads, and improve energy efficiency—critical factors for maximizing electric vehicle range. The technology aligns perfectly with China’s aggressive EV adoption curve and its strategy to integrate comfort-enhancing smart components across vehicle models.

On the architectural side, China is narrowing the technology gap with global leaders by achieving manufacturing scale efficiencies that position domestic companies as competitive suppliers of Electrochromic systems for new commercial towers, high-end residential projects, and public infrastructure. Government-backed research programs promoting tungsten oxide (WO₃)-based Electrochromic materials are improving switching speeds, coloration efficiency, and durability. These advancements, combined with the strategic push to upgrade commercial glazing across China’s rapidly urbanizing cities, make the country a rising heavyweight in global Electrochromic Glass innovation and deployment.

Japan: High-Speed Electrochromic Switching and Global Expansion Through Strategic Partnerships

Japan maintains a strong innovation footprint in Electrochromic materials, emphasizing switching performance, device durability, and cross-border commercialization partnerships. AGC Inc.’s joint venture with Kinestral Technologies—Halio International—positions Japan as a key supplier and global distributor of Halio Smart-Tinting Glass across more than 30 countries. This strategic alliance underscores Japan’s commitment to exporting high-performance dynamic glazing solutions that integrate seamlessly into modern architectural and commercial environments.

Material science excellence remains at the core of Japan’s competitive edge. University and corporate R&D teams continue to refine next-generation Electrochromic materials designed to deliver faster response times, broader tinting ranges, and longer operational life compared to conventional tungsten-oxide-based systems. Such improvements support the deployment of Electrochromic Glass in applications requiring rapid solar load adjustments, such as trains, high-rise façades, and advanced interior partitions. Japan’s balanced focus on material innovations and global market expansion reinforces its strategic influence in the Electrochromic ecosystem.

South Korea: Conglomerate-Backed Innovation and Automotive Leadership in Electrochromic Components

South Korea is emerging as a high-impact contributor to the Electrochromic Glass Market thanks to strong backing from major conglomerates and its advanced electronics and automotive sectors. The strategic $100+ million investment by SK Holdings in Kinestral Technologies (Halio) demonstrates Korea’s intent to secure leadership in smart-tinting technologies and integrate Electrochromic solutions into next-generation construction, mobility, and electronics ecosystems. This investment strengthens manufacturing capacity and accelerates commercialization across Asia-Pacific.

South Korea also holds a dominant position in Electrochromic rearview mirrors, a high-value automotive segment where Korean suppliers leverage their global electronics expertise to deliver reliable, fast-switching mirror systems to top automotive OEMs. As Korean EV manufacturers increasingly prioritize occupant comfort and thermal efficiency, Electrochromic components are expected to expand beyond mirrors into panoramic glazing, side windows, and cockpit privacy systems. The synergy between semiconductor engineering, automotive manufacturing, and advanced material R&D underpins Korea’s rising influence in the global Electrochromic Glass market.

Competitive Landscape: Leading Companies Defining the Electrochromic Glass Market

The competitive environment is shaped by companies that combine expertise in dynamic glazing, IoT integration, thin-film deposition, and large-scale fabrication. Architectural EC adoption relies on performance consistency, tint uniformity, sustainable manufacturing, and seamless integration with BMS and HVAC systems. Automotive EC markets depend on mass-manufacturing reliability, ultra-fast switching, and long lifecycle durability. The leaders below represent the core pillars of innovation across both domains.

Saint-Gobain SageGlass: Neutral-Tint Electrochromic Glass Leadership

Saint-Gobain, through its SageGlass division, holds a dominant position in architectural electrochromic glazing with solutions engineered for dynamic control of solar heat, daylight, and glare. Its SageGlass® portfolio allows buildings to eliminate blinds, reduce cooling loads, and achieve advanced daylight harvesting. The launch of RealTone™ in February 2025 introduced a neutral-color EC tinting solution—removing the blue/green shift characteristic of early EC glass and improving aesthetic acceptance in premium architectural projects. With over 1,500 installations worldwide, SageGlass remains the most widely deployed EC technology for airports, healthcare facilities, corporate campuses, and educational buildings. Its system integrates fully with Building Management Systems, enabling automated tinting based on sun angle, HVAC demand, occupancy, and energy optimization algorithms.

Gentex Corporation: Automotive Electrochromic Manufacturing Powerhouse

Gentex is the global leader in automotive electrochromic applications, especially dimming rear-view mirrors, where it dominates OEM supply chains. The company extended its automotive electronics presence by acquiring Voxx International in April 2025, enabling broader integration of smart-glass technologies across sunroofs, skylights, and side windows. Gentex leverages unmatched high-volume manufacturing expertise, supplying millions of EC components annually with exceptional reliability. As EV makers prioritize cabin comfort and thermal efficiency, Gentex’s EC mirrors and glazing are expanding into next-gen EV platforms, complementing advanced driver-assistance systems and interior electro-optic features.

Kinestral Technologies (Halio): Fast-Switching Smart Glass Enabled by AGC JV

Kinestral Technologies, through its Halio™ brand, offers one of the fastest-tinting electrochromic systems, achieving uniform neutral-gray tinting within under 3 minutes. Its strategic joint venture with AGC Inc., the world’s largest glass producer, provides global reach, mass-production capabilities, and integration support for Halio™ in commercial projects. Halio has secured over $100 million in Series D funding (January 2019, led by SK Holdings) to expand manufacturing and commercial deployment. Designed for deep integration with BMS and home automation platforms, Halio supports real-time algorithms for solar control, glare management, and energy savings—positioning it as one of the most advanced solutions for smart buildings.

ChromoGenics AB: Roll-to-Roll Electrochromic Foil Innovation

ChromoGenics differentiates itself via its proprietary roll-to-roll sputtering process for applying electrochromic nano-layers onto plastic film, enabling scalable and cost-efficient production. Its flagship ConverLight® Dynamic glazing, along with static and energy-generating variants (ConverLight® Energy), offers tunable heat and light control while supporting geographically distributed lamination partners. This business model accelerates global availability and reduces logistics complexity. ChromoGenics’ integrated façade concepts, combining dynamic EC glazing with solar cell technology, target high-performance building envelopes and net-zero energy design.

View, Inc.: IoT-Enabled Dynamic Glass with Advanced Automation

View, Inc. is a major innovator in IoT-integrated electrochromic systems, offering View Dynamic Glass, which features multilayer ceramic metal oxide coatings adjustable from clear to 99% light blockage. Each EC pane is digitally addressable via the company’s IoT platform, enabling intelligent façade operation that responds to weather, occupancy, and HVAC signals. Despite financial restructuring—including Chapter 11 filing in April 2024 and workforce reductions in October 2024—View remains a key technology provider within the architectural smart glass market. Historically backed by over $1.1 billion from the SoftBank Vision Fund, the company’s manufacturing scale and software ecosystem continue to shape dynamic façade innovation in commercial buildings.

Electrochromic Glass Market Report Scope

Electrochromic Glass Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.3 Billion

|

|

Market Size (2035)

|

$5.3 Billion

|

|

Market Growth Rate

|

8.8%

|

|

Segments

|

By Technology Type (Electrochromic Glass, SPD Glass, PDLC Glass, Thermochromic & Photochromic Glass), By Device Configuration (Laminated Electrochromic Glass, IGU with Electrochromic Pane), By Material Used (Inorganic Electrochromic Materials, Organic Electrochromic Materials), By Application (Architectural & Building Facades, Automotive Glazing, Aerospace Windows, Consumer Electronics), By Control System (Building Management System Control, Manual Switch Control, Mobile App/IoT Control, AI/Sensor-Based Automatic Control)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

View Inc., SageGlass (Saint-Gobain), AGC Inc., Gentex Corporation, Halio (Kinestral), Gauzy Ltd., Research Frontiers, Chromogenics AB, Polytronix, RavenWindow, SAGE Electrochromics, Hitachi Chemical, Innovative Glass Corp., Yoroe Co., E-Control SmartGlass

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Electrochromic Glass Market Segmentation

By Technology Type

- Electrochromic (EC) Glass

- Suspended Particle Device (SPD) Glass

- Polymer-Dispersed Liquid Crystal (PDLC) Glass

- Thermochromic & Photochromic Glass

By Device Configuration

- Laminated Electrochromic Glass

- IGU with Electrochromic Pane

By Material Used

- Inorganic Electrochromic Materials

- Organic Electrochromic Materials

By Application

- Architectural & Building Facades

- Automotive Glazing

- Aerospace Windows

- Consumer Electronics

By Control System

- Building Management System Control

- Manual Switch Control

- Mobile App / IoT Control

- AI / Sensor-Based Automatic Control

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Electrochromic Glass Market

- View Inc.

- SageGlass (Saint-Gobain)

- AGC Inc.

- Gentex Corporation

- Halio (Kinestral)

- Gauzy Ltd.

- Research Frontiers

- Chromogenics AB

- Polytronix

- RavenWindow

- SAGE Electrochromics

- Hitachi Chemical

- Innovative Glass Corp.

- Yoroe Co.

- E-Control SmartGlass.

*- List not Exhaustive

Research Coverage

The latest Electrochromic Glass Market study from USDAnalytics delivers an in-depth, data-driven assessment of how dynamic glazing is reshaping smart buildings and automotive glazing worldwide. Spanning architectural façades, electric vehicles, aerospace windows, and connected consumer devices, this report investigates the full ecosystem of electrochromic, SPD, PDLC, thermochromic, and photochromic solutions, mapping their impact on HVAC energy use, daylight control, and occupant comfort. It highlights emerging material breakthroughs in inorganic and organic electrochromic layers, fast-switching device architectures, and ultra-low-power smart façade concepts, while analysis reviews regulatory drivers, green-building programs, and grid-interactive building strategies that are accelerating adoption. Detailed technology roadmaps, pricing and adoption curves, and competitive benchmarking of leading dynamic glass vendors are combined with installer feedback and project case studies to give decision-makers a practical implementation lens. From automotive smart sunroofs to BMS-integrated façade systems, this report is an essential resource for glass manufacturers, coating companies, façade consultants, OEMs, and investors seeking to understand where value will concentrate as intelligent light-control solutions scale globally.

Scope Highlights

- Segmentation: Technology Type (Electrochromic Glass, Suspended Particle Device Glass, Polymer-Dispersed Liquid Crystal Glass, Thermochromic & Photochromic Glass); Device Configuration (Laminated EC Glass, IGU with EC Pane); Material Used (Inorganic EC, Organic EC); Application (Architectural & Building Facades, Automotive Glazing, Aerospace Windows, Consumer Electronics); Control System (BMS Control, Manual Switch, Mobile App / IoT, AI / Sensor-Based Automatic Control).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Horizon: Historic data from 2021 to 2025 and detailed forecast trends from 2026 to 2034.

- Companies: In-depth analysis and profiles of 15+ key players across architectural, automotive, and specialty electrochromic glass value chains.