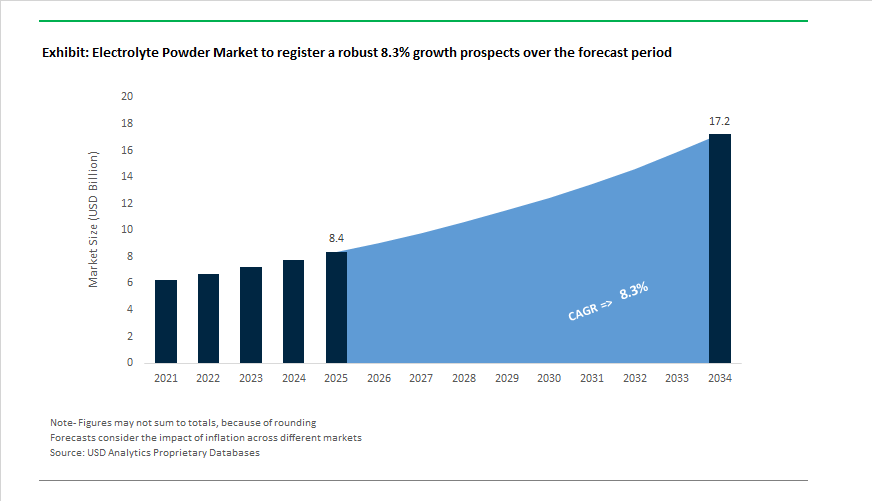

Electrolyte Powder Market to Reach $17.2 Billion by 2034 at 8.3% CAGR as Functional Hydration Becomes a Daily Wellness Staple

The Electrolyte Powder Market is projected to expand from $8.4 billion in 2025 to $17.2 billion by 2034, registering a CAGR of 8.3%. Growth is increasingly driven by the shift from performance-only sports hydration to everyday functional wellness, clean-label formulations, and global retail expansion. In September 2024, PepsiCo’s Gatorade introduced Hydration Booster, its first powdered enhancer positioned for all-day hydration rather than just athletic recovery. The formula contains no artificial colors or sweeteners and delivers 100% of the daily value of vitamins A, B, and C, signaling a repositioning of electrolyte powders as immunity-support and lifestyle beverages.

In April 2025, Hindustan Unilever launched Liquid I.V. in India, bringing the U.S. market leader into one of the fastest-growing functional beverage markets globally. The rollout included localized flavors such as Acai Berry, Brazilian Orange, and Lemon Lime, directly targeting Gen Z and millennial consumers pursuing active lifestyles and heat-related hydration support. The India entry reflects multinational beverage companies leveraging emerging market demand for sachet-format nutraceuticals. Complementing this geographic expansion, Liquid I.V. introduced its Sugar-Free Hydration Multiplier in August 2025, featuring an amino acid–based formulation that avoids synthetic sweeteners while maintaining rapid fluid absorption, appealing to diabetic and low-sugar consumers.

Competitive intensity is escalating through brand diversification and athlete partnerships. In January 2025, Celsius Holdings expanded into zero-sugar, caffeine-free hydration powders with Celsius Hydration, enriched with B-vitamins and essential minerals to extend consumer engagement beyond energy drinks. Meanwhile, in December 2025, IRONMAN announced Precision Fuel & Hydration as its Official Hydration Partner starting in 2026, replacing prior sponsors across global IRONMAN and 70.3 races. This partnership institutionalizes science-based electrolyte ratios in endurance events and elevates premium powder brands into mainstream sports ecosystems. Specialty brand Skratch Labs reinforced this high-performance niche in June 2025 with a limited-edition real-fruit hydration mix engineered to match sweat electrolyte composition, strengthening the segment for endurance athletes demanding precise sodium-to-carbohydrate ratios.

Market dynamics in Europe revealed regulatory and competitive shifts. In late 2025, LMNT discontinued official European operations due to compliance and operational hurdles, creating an immediate supply gap in the high-sodium zero-sugar segment. This vacuum enabled regional players such as NoordCode and BeKeto to capture share among keto-focused consumers. Simultaneously, U.K.-based Phizz expanded its retail footprint in April 2025 with Phizz Daily Energy, combining seven electrolytes with multivitamins and guarana-derived caffeine, targeting hybrid consumers seeking hydration plus cognitive stimulation. In October 2025, Rehydration Nation launched sugar-free high-potassium tablets aimed at low-carb and keto users prioritizing mineral balance without glucose.

Contract manufacturers are also innovating in delivery systems. In early 2026, SIRIO Europe introduced its FizzyBits™ and HydraPowder Energy & Recovery platforms, enabling fast-melt and effervescent electrolyte formats for brands responding to rising demand for portable, rapid-absorption hydration. Industry surveys indicate that more than 40% of global consumers now consider hydration a foundational wellness pillar, accelerating the crossover between sports nutrition, preventive healthcare, and functional beverage markets.

Trends and Opportunities in the Electrolyte Powder Market

Premiumization and Functional Blending in Consumer Nutrition

- The traditional sodium-potassium hydration mix is rapidly being replaced by advanced hydration plus formulations that combine electrolytes with vitamins, nootropics, and metabolic support ingredients. This premiumization trend reflects a broader shift toward lifestyle hydration, where products are consumed throughout the day rather than exclusively during athletic activity.

- In September 2024, PepsiCo expanded its hydration strategy through the launch of Gatorade Hydration Booster, a powdered enhancer positioned for all-day consumption. The formulation integrates electrolytes derived from watermelon juice and sea salt with 100% Daily Value of multiple vitamins, signaling a strategic move toward clean-label, functional nutrition rather than performance-only sports drinks.

- A similar trajectory is visible in Unilever’s Liquid I.V. brand, which reported in early 2025 that its growth momentum was driven by functional variants rather than core electrolyte SKUs. Expansion into markets such as the UK and China has been led by sugar-free and lifestyle-focused blends using alternative sweeteners like allulose and stevia. These products address premium dietary preferences while maintaining rapid hydration efficacy, reinforcing electrolyte powders as a daily wellness staple.

- Another layer of premiumization is the integration of cognitive and mood-support ingredients. Late 2024 launches featuring citicoline, L-theanine, and adaptogenic compounds reflect growing demand from professionals, gamers, and knowledge workers who associate hydration with mental performance and sustained focus. This convergence of hydration and nootropic nutrition is creating higher-margin product tiers and increasing brand differentiation.

Integration into Medical and Clinical Nutrition Protocols

- Electrolyte powders are increasingly migrating from retail channels into clinical and quasi-medical use cases, driven by aging demographics and renewed regulatory emphasis on nutrition as a determinant of health outcomes. Hospital systems and care providers are standardizing oral rehydration solutions as part of post-discharge and chronic care protocols.

- In December 2025, the Food and Drug Administration emphasized nutrition’s role in disease management through its Nutrition Center of Excellence, accelerating the adoption of structured oral rehydration therapy in outpatient and home-care settings. This regulatory positioning has increased demand for powdered electrolyte formats that offer precise dosing, longer shelf life, and easier storage compared to ready-to-drink alternatives.

- Clinical guidance reinforced in the MSD Manual Professional Edition continues to recommend oral rehydration therapy as the first-line treatment for mild-to-moderate dehydration, based on sodium-glucose cotransport mechanisms. As a result, commercial electrolyte powders adhering closely to World Health Organization ORS specifications are gaining traction in home medical kits and long-term care facilities. With dehydration affecting an estimated 30% of seniors in assisted living environments, powdered formats are increasingly favored for their dosing flexibility and patient compliance advantages.

Formulation for Extreme Occupational and Environmental Heat Stress

- Rising global temperatures and tightening workplace safety regulations are transforming electrolyte powders into essential occupational health inputs. Governments and employers are increasingly recognizing hydration with electrolytes as a preventive intervention against heat-related illness and productivity loss.

- In August 2024, the Occupational Safety and Health Administration issued a Notice of Proposed Rulemaking on Heat Injury and Illness Prevention, encouraging electrolyte use for prolonged heat exposure. This regulatory direction has been reinforced at the state level, with Maryland’s heat stress standard mandating frequent hydration breaks when heat indices exceed 80°F. Such policies are creating recurring institutional demand for bulk electrolyte powder procurement across construction, agriculture, logistics, and warehousing sectors.

- Internationally, heat action plans are scaling electrolyte distribution at a population level. India’s 2025 regional heat action programs highlight annual losses of hundreds of billions of labor hours due to extreme heat, prompting government-backed distribution of ORS packets to outdoor workers. These initiatives position electrolyte powders not just as consumer products but as public health and workforce resilience tools, significantly expanding volume potential in emerging markets.

Development of Clean-Label, Low-Sugar, and Ketogenic-Friendly Products

- Clean-label reformulation has shifted from a marketing advantage to a baseline requirement in the electrolyte powder market. Regulatory clarification around healthy labeling and growing metabolic health concerns are accelerating the removal of high-glycemic fillers and artificial additives.

- By 2025, compliance with updated FDA guidance has driven widespread elimination of maltodextrin in favor of non-nutritive sweeteners such as monk fruit and stevia. This transition supports both diabetic-friendly positioning and broader consumer skepticism toward hidden sugars. Concurrently, the rise of ketogenic and low-carbohydrate lifestyles has created a distinct product niche for electrolyte powders with elevated magnesium and potassium content and zero carbohydrates, addressing mineral imbalances commonly associated with carbohydrate restriction.

- Consumer research published in late 2025 indicates that clean-label attributes now influence more than 60% of purchasing decisions in the hydration category. This is particularly pronounced among parents and active older consumers who actively avoid synthetic dyes and artificial colors. For manufacturers, this creates an opportunity to command pricing premiums through transparent labeling, simplified ingredient decks, and alignment with metabolic and preventive health narratives.

Electrolyte Powder Market Share and Segmentation Insights

Multi-Electrolyte Blends Dominate Consumer Hydration with Comprehensive Mineral Formulations

Multi-electrolyte blends account for 72% of total electrolyte powder market share in 2025, reflecting strong consumer preference for all-in-one hydration solutions delivering sodium, potassium, magnesium, and calcium in balanced ratios. These formulations address the combined physiological roles of multiple electrolytes in fluid balance, muscle contraction, nerve signaling, and post-exercise recovery, making them the leading choice across sports nutrition, wellness supplements, and clinical hydration products. Brands increasingly position multi-electrolyte powders as premium recovery aids, integrating clean-label ingredients, low sugar content, and functional additives to enhance market appeal. Single-electrolyte powders maintain a meaningful presence in targeted therapeutic and performance niches, including potassium supplementation for cardiovascular support and magnesium for muscle cramp prevention. While smaller in volume, this segment benefits from medically guided usage and precision dosing requirements, particularly in healthcare and specialized fitness communities where individualized electrolyte management is prioritized.

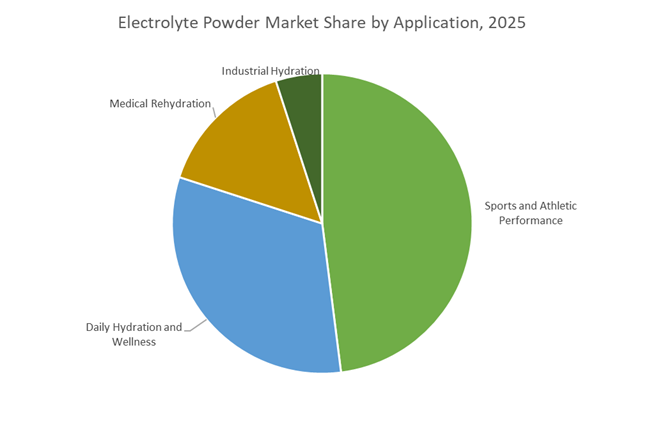

Sports Performance Applications Drive Nearly Half of Global Electrolyte Powder Consumption

Sports and athletic performance represent 48% of total electrolyte powder demand in 2025, driven by rising participation in fitness activities and growing awareness of hydration’s impact on endurance and recovery. Athletes and active consumers rely on electrolyte powders for rapid rehydration during training and competition, supported by strong visibility in gyms, endurance events, and digital fitness platforms. Daily hydration and wellness follows as a fast-expanding segment, fueled by lifestyle trends emphasizing energy optimization, mental clarity, and alcohol-free social habits, positioning electrolyte powders as everyday functional beverages. Medical rehydration remains a critical application, supplying hospitals and clinics with formulations meeting strict osmolality and electrolyte balance standards for dehydration management and post-operative care. Industrial hydration occupies a smaller but stable niche, supporting workers in high-heat environments such as construction, mining, and agriculture, where employer-led heat stress prevention programs sustain consistent demand.

Competitive Landscape of the Electrolyte Powder Market

The Electrolyte Powder Market in 2026 is highly competitive and innovation-led, driven by clean-label hydration powders, sugar-free electrolyte blends, DTC wellness brands, and clinical-grade rehydration solutions, with global players competing on functional nutrition, influencer reach, and omnichannel distribution.

Influencer-powered hydration dominance and sugar-free innovation by Liquid I.V.

Liquid I.V., backed by Unilever, leads the U.S. powdered hydration segment in 2026, powered by its proprietary Cellular Transport Technology (CTT) for rapid electrolyte absorption. Following Unilever’s acquisition, the brand executed major international expansion across the UK, China, and the Netherlands during 2024–2025. Its Hydration Multiplier Sugar-Free line, launched in 2025/2026 after two years of R&D, targets keto and metabolic-health consumers. Liquid I.V. commands 44% supermarket share while scaling a robust DTC subscription model. With partnerships involving over 10,000 college athletes, its influencer-driven strategy has made it a Gen Z hydration leader.

Clean-ingredient stick packs and sustainable packaging leadership from Nuun Hydration

Owned by Nestlé Health Science, Nuun has evolved beyond effervescent tablets into high-growth electrolyte powder stick packs emphasizing low sugar, Non-GMO formulations. Its Nuun Sport and Nuun Immunity ranges remain staples for endurance athletes and daily wellness users, while the Nuun Energy powder adds plant-based caffeine and B-vitamins for cognitive hydration. Nestlé reports Nuun’s footprint across 30+ countries, tripling international revenue since 2021. Nuun’s 2026 strategy prioritizes paper-based recyclable sachets, reinforcing its sustainability credentials while expanding share in the clean hydration powder category.

Functional wellness expansion and everyday hydration strategy by Gatorade

Backed by PepsiCo, Gatorade is aggressively scaling its Hydration Booster electrolyte powders to compete with specialty wellness brands. Launched in late 2024/2025, Hydration Booster features watermelon juice, sea salt, and zero artificial sweeteners, targeting clean-label consumers. PepsiCo’s 2025 acquisition of Poppi accelerated its shift toward functional nutrition, directly influencing Gatorade’s powder innovation pipeline. The brand now markets electrolyte powders for travel, heat relief, and daily wellness, not just sports recovery. Supported by the Gatorade Sports Science Institute (GSSI), Gatorade maintains unmatched clinical credibility in performance hydration.

High-sodium performance hydration disruption from LMNT

LMNT has carved out a premium niche by serving keto, CrossFit, and heavy-sweat athletes with a bold 1,000 mg sodium formulation, far above category averages. Its “radical transparency” model publishes the base recipe online, building trust while monetizing flavored stick packs through a loyal digital community. In early 2026, LMNT introduced Hot Hydration flavors like Chocolate Salt and Spicy Habanero for cold-weather recovery. Built as an internet-first electrolyte brand, LMNT leads online retail growth (9.11% CAGR) by leveraging fitness podcasts and performance communities, positioning itself as the go-to high-sodium electrolyte powder for elite users.

Clinical-grade recovery positioning by Abbott Nutrition

Produced by Abbott Laboratories, Pedialyte has successfully transitioned from pediatric rehydration to professional-grade adult electrolyte powders. Its Pedialyte Sport and Immune Support formulations optimize glucose-electrolyte balance for rapid fluid absorption. In 2026, Abbott pivoted messaging toward modern recovery, addressing hangovers, illness-related dehydration, and next-day fatigue. Abbott retains dominance in the medical rehydration segment, representing roughly 12.3% of the global powder market, supported by strong pharmacy penetration and healthcare endorsements. Clinical trust remains Pedialyte’s core differentiator versus lifestyle hydration competitors.

United States: Industrial-Scale Capacity, Clean-Label Reformulation, and Lifestyle Positioning

The United States electrolyte powder market is undergoing a structural upgrade driven by large-scale manufacturing investments and stricter nutritional governance. In November 2024, Electrolit announced a $400 million investment to build a 600,000-square-foot production facility in Texas, marking its first manufacturing base outside Mexico. Scheduled to ramp up through 2025–2026, the plant is designed to support both ready-to-mix electrolyte powders and liquid hydration formats, significantly strengthening domestic supply resilience while reducing cross-border logistics exposure. This capacity expansion reflects growing institutional confidence in sustained U.S. demand for functional hydration products beyond seasonal consumption patterns.

On the innovation and compliance front, January 2025 saw Celsius Holdings launch Celsius Hydration, a zero-sugar, caffeine-free electrolyte powder positioned for recovery-focused consumers. This pivot aligns with the U.S. FDA’s 2025 revision of Healthy claim criteria, which requires electrolyte supplements to meet updated nutrient thresholds by 2026 to retain premium on-pack health messaging. Parallel clean-label momentum is evident in Gatorade, a subsidiary of PepsiCo, which expanded its Gatorade Hydration Booster line with formulations free from artificial colors and sweeteners. Backed by a high-profile 2025 marketing campaign featuring major athletes, U.S. brands are increasingly blending regulatory alignment with lifestyle branding to capture Gen Z and Millennial consumers who are accelerating adoption of functional fitness supplements.

India: Heat-Resilience Demand, Localized Additives, and Export-Oriented Formats

India’s electrolyte powder market is shaped by climate-driven consumption, industrial workforce welfare, and expanding domestic manufacturing of electrolyte ingredients. In July 2025, Otsuka Pharmaceutical entered the Indian market with the launch of POCARI SWEAT through Otsuka Nutraceutical India Private Limited. The brand is targeting urban heat-illness prevention with 350 ml and 500 ml hydration formats tailored for India’s high-temperature zones, signaling growing multinational interest in India as a long-term hydration market rather than a niche seasonal opportunity.

Upstream capacity is also scaling. AMI Organics committed ₹177 crore to expand its Jhagadia facility, enabling automated production of 4,000 MT per year of electrolyte additives by the first half of FY 2025–26. This expansion coincides with government-backed PM MITRA industrial parks, where worker wellness provisions have triggered bulk procurement of electrolyte powders for dehydration prevention in heat-intensive manufacturing clusters. At the consumer end, Fast&Up has advanced effervescent electrolyte tablet technology, focusing on rapid absorption and portability. Its export-oriented strategy, targeting a 76% revenue contribution from overseas markets by late 2026, highlights India’s growing role as both a consumption and innovation base for electrolyte formats.

Canada: Regulatory Reclassification and Claim Rationalization

Canada’s electrolyte powder market is entering a regulatory transition phase that will reshape product positioning and compliance strategies. In December 2025, Health Canada announced that Sports Electrolyte Supplements will be reclassified as Supplemented Foods rather than Natural Health Products. Formal notification is expected in early 2026, with full compliance mandated by January 1, 2028. This shift introduces standardized food-style labeling, compositional oversight, and marketing restrictions, particularly around therapeutic and medical-style claims.

A key implication of the new framework is the expected removal or tightening of Oral Rehydration Solution claims for many electrolyte powders. Regulators aim to reduce consumer confusion between medical hydration therapies and lifestyle hydration products. For manufacturers, this change favors brands with strong nutrition science documentation and transparent ingredient disclosures, while reducing the appeal of aggressive medical-style positioning in retail hydration categories.

Russia: Digital Traceability and Market Formalization

Russia is advancing formal oversight of the electrolyte powder and sports nutrition segment through digital traceability. The Ministry of Industry and Trade proposed mandatory labeling for sports nutrition and electrolyte products beginning September 1, 2025, supported by Rospotrebnadzor. The initiative seeks to integrate electrolyte powders into existing digital tracking systems used for biologically active additives, strengthening supply chain transparency and counterfeit prevention.

For market participants, mandatory labeling increases compliance costs but also raises entry barriers, favoring established producers with robust documentation and distribution controls. Over time, this is expected to formalize the market and improve consumer trust in branded electrolyte products.

China: Plant-Based Inputs and Domestic Content Targets

China’s electrolyte powder market is increasingly aligned with sustainability and domestic sourcing objectives. Under the MIIT 2025 Green Manufacturing Roadmap, functional beverage and electrolyte producers are transitioning toward plant-based electrolyte sources such as coconut water concentrates and fruit-derived mineral extracts. This shift supports national targets to achieve 70% domestic content for natural health ingredients by 2027.

The emphasis on sustainable inputs is also influencing procurement strategies for electrolyte powders used in fitness, outdoor labor, and mass-market hydration products. By reducing reliance on imported mineral blends and synthetic additives, Chinese manufacturers are positioning electrolyte powders as part of the broader green consumption narrative, while improving supply chain security for the domestic functional nutrition industry.

Electrolyte Powder Market: Country-Level Strategic Snapshot

Electrolyte Powder Market County Level Snapshot

|

Country

|

Core Strategic Driver

|

Key Market Shift

|

Structural Implication

|

|

United States

|

Manufacturing scale and clean-label rules

|

Zero-sugar, FDA-aligned formulations

|

Premiumization and brand-led growth

|

|

India

|

Heat resilience and localization

|

Additive capacity and effervescent tech

|

Dual role as consumption and export hub

|

|

Canada

|

Regulatory reclassification

|

Supplemented food compliance

|

Claim rationalization and transparency

|

|

Russia

|

Mandatory digital labeling

|

Traceability and formal oversight

|

Higher entry barriers, market consolidation

|

|

China

|

Green manufacturing targets

|

Plant-based electrolyte sourcing

|

Domestic content and sustainability focus

|

Electrolyte Powder Market Report Scope

Electrolyte Powder Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.4 Billion

|

|

Market Size (2034)

|

$17.2 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Type (Single-Electrolyte Powders, Multi-Electrolyte Blends), By Form (Sachets and Sticks, Bulk Containers, Effervescent Tablets), By Formulation (Sugar-Free, Low-Sugar, High-Carbohydrate, Clean-Label), By Application (Sports and Athletic Performance, Daily Hydration and Wellness, Medical Rehydration, Industrial Hydration), By End-User (Professional Athletes and Fitness Enthusiasts, Geriatric Population, Pediatric Population, Outdoor and Industrial Workers)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PepsiCo, Inc., Unilever PLC, Abbott Laboratories, Celsius Holdings, Inc., Otsuka Pharmaceutical Co., Ltd., The Coca-Cola Company, Nutricost, LMNT, Inc., Nuun, DripDrop Hydration, Inc., Skratch Labs, Ultima Replenisher, Fast&Up, BioSteel Sports Nutrition Inc., Haleon

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Electrolyte Powder Market Segmentation

By Type

- Single-Electrolyte Powders

- Multi-Electrolyte Blends

By Form

- Sachets and Sticks

- Bulk Containers

- Effervescent Tablets

By Formulation

- Sugar-Free

- Low-Sugar

- High-Carbohydrate

- Clean-Label

By Application

- Sports and Athletic Performance

- Daily Hydration and Wellness

- Medical Rehydration

- Industrial Hydration

By End-User

- Professional Athletes and Fitness Enthusiasts

- Geriatric Population

- Pediatric Population

- Outdoor and Industrial Workers

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Electrolyte Powder Industry

- PepsiCo, Inc.

- Unilever PLC

- Abbott Laboratories

- Celsius Holdings, Inc.

- Otsuka Pharmaceutical Co., Ltd.

- The Coca-Cola Company

- Nutricost

- LMNT, Inc.

- Nuun

- DripDrop Hydration, Inc.

- Skratch Labs

- Ultima Replenisher

- Fast&Up

- BioSteel Sports Nutrition Inc.

- Haleon

*- List not Exhaustive