Emulsifiers Market to Reach $46.4 Billion by 2034 at 7.6% CAGR Amid Clean-Label Reformulation and Microbiome-Certified Innovation

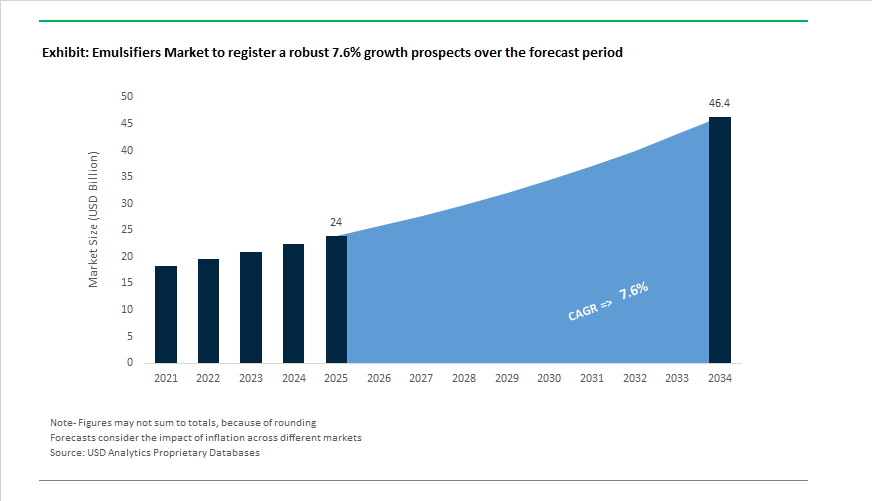

The Emulsifiers Market is projected to expand from $24 billion in 2025 to $46.4 billion by 2034, registering a CAGR of 7.6%. Growth momentum is anchored in clean-label reformulation, plant-based functional systems, regulatory tightening, and advanced personal care chemistry. In November 2025, Corbion completed the divestment of its Emulsifiers business under its Advance 2025 strategy, reallocating capital toward fermentation-derived preservation and lactic acid specialties. This exit signals structural consolidation in conventional emulsifier manufacturing while accelerating the transition toward bio-based and specialty-driven portfolios.

Regulatory evolution is actively reshaping global supply chains. China’s revised GB 2760-2024 standard came into effect in February 2025, updating the list of permitted food emulsifiers and dosage thresholds. Multinationals such as Ingredion and Cargill were required to re-certify product lines for compliance, particularly lecithin and mono- and diglyceride systems. In parallel, ADM announced in February 2025 a $500–$750 million cost optimization program through 2026, restructuring its Nutrition segment to focus on simplified ingredient systems aligned with North American clean-label demand. The tightening of additive approvals and labeling transparency is pushing formulators to seek multifunctional emulsifiers that deliver stabilization, texture enhancement, and shelf-life performance under stricter regulatory oversight.

Product innovation is increasingly centered on biodegradable and microbiome-compatible solutions. In February 2025, BASF’s Emulgade® Verde 10 MS received the Fountain Award at PCHi China for its 100% naturally derived, oil-in-water emulsification system tailored for clean beauty skincare and sun care. Throughout 2025, suppliers including BASF and Cargill Beauty expanded clinically validated Microbiome-Friendly emulsifier lines designed not to disrupt the skin barrier, capturing high-growth dermatological and anti-aging segments. Safic-Alcan strengthened its Asia-Pacific manufacturing footprint by acquiring a majority stake in Avees Biocos in November 2024, securing regional production capacity for cosmetic esters and specialty emulsifiers. BASF further reinforced its industrial segment with a new dispersions production line in Mangalore announced in February 2026, supporting coatings and construction emulsification demand in India’s expanding infrastructure ecosystem.

Food and beverage applications remain the largest revenue driver, with rapid diversification toward alternative proteins and dairy-free formulations. In 2025, Kerry introduced Puremul™, an acacia-derived clean-label emulsification system positioned as a substitute for sunflower lecithin amid supply volatility. In January 2026, Kerry’s Global Taste & Nutrition Charts emphasized functional indulgence, requiring advanced emulsifiers capable of preserving creamy mouthfeel in reduced-sugar and plant-based matrices. Ingredion reinforced its strategic focus in February 2026 with leadership realignment following record 2025 earnings, prioritizing grain- and fruit-derived specialty texturants and emulsifiers to replace synthetic stabilizers. Meanwhile, Shiru launched its AI-powered protein discovery marketplace in May 2024, leveraging machine learning to identify novel plant proteins with emulsification functionality capable of replicating egg yolk or synthetic ester performance. The market trajectory is increasingly defined by biotechnology-enabled discovery, regulatory harmonization, and the integration of sustainability metrics into formulation design.

Trends and Opportunities in the Emulsifiers Market

Clean-Label Reformulation Accelerated by Enforced Natural Claims Standards

- The clean-label movement has moved from marketing-driven positioning to regulator-enforced compliance, directly reshaping emulsifier selection across food and beverage formulations. Authorities are now challenging loosely defined natural claims, forcing manufacturers to eliminate synthetic esters and chemically modified emulsifiers from mainstream products.

- In January 2025, the Food Safety and Standards Authority of India formalized an annual July 1 enforcement cycle for labeling and additive amendments. This included explicit advisories against 100% natural claims on products containing synthetic stabilizers, triggering rapid reformulation across dairy, bakery, and beverage segments. As a result, demand for plant-derived lecithins, citrus fibers, and fermentation-based emulsifiers has risen sharply in India and export-oriented production hubs.

- Strategic responses from ingredient leaders reinforce this shift. In September 2025, Corbion advanced its BRIGHT 2030 strategy, positioning clean-label emulsification as a core growth pillar. Its Verdad Essence systems are designed to replace chemically modified mono- and diglycerides in commercial baking while preserving volume, crumb softness, and shelf life. Similarly, Ingredion introduced Evanesse CB6194, a vegan emulsifier derived from chickpea broth, enabling egg-free and allergen-reduced formulations in sauces and dressings. These innovations highlight how regulatory pressure is directly translating into premiumization and differentiation within the emulsifiers market.

Precision Emulsification for Advanced Plant-Based and Fermentation-Derived Foods

- The rapid rise of precision fermentation and hybrid protein products is redefining functional requirements for emulsifiers. Stabilizing recombinant proteins and novel lipid structures demands emulsification systems capable of withstanding high shear, thermal stress, and extended shelf life without compromising sensory performance.

- A notable milestone occurred in November 2025 when the French startup Verley received an FDA No Questions letter for its precision-fermented dairy proteins. Its UHT-stable whey protein relies on a tailored emulsification profile that prevents denaturation during high-temperature processing, addressing one of the key technical bottlenecks in fermented dairy alternatives.

- At the research level, collaborative initiatives such as the PLANTOMYC consortium, funded under Horizon Europe in late 2025, are advancing minimally processed meat analogues. The consortium is developing functional emulsifiers from pea-protein byproducts to create meltable, animal-fat-like textures without hydrogenated oils. These approaches are delivering measurable performance gains, including roughly 30% reductions in syneresis in plant-based yogurts and cheeses, narrowing the sensory gap with conventional dairy and supporting broader consumer adoption.

Emulsifiers as Enablers of Next-Generation Lipid-Based Drug Delivery

- Pharmaceutical applications represent one of the most attractive value pools for emulsifier manufacturers, driven by the growing challenge of poor bioavailability in lipophilic and water-insoluble active pharmaceutical ingredients. High-purity emulsifiers are increasingly central to lipid-based drug delivery systems, where droplet size control and interfacial stability directly influence therapeutic efficacy.

- In December 2025, academic research demonstrated a self-nanoemulsifying drug delivery system using cashew nut kernel oil that achieved droplet sizes near 105 nm, significantly enhancing intestinal absorption of poorly soluble drugs. Such findings reinforce the commercial momentum behind SNEDDS and SEDDS technologies, which use specialized emulsifier blends to improve drug solubility by up to 40%.

- Beyond oral delivery, the rapid expansion of lipid nanoparticle platforms for mRNA vaccines and advanced biologics has created a premium niche for pharma-grade phospholipids and surfactants. These emulsifiers must meet stringent purity and consistency standards to ensure stability during storage and circulation, positioning certified high-purity suppliers for long-term, contract-based growth.

Sustainable Industrial and Agrochemical Emulsions for Low-VOC Systems

- Industrial and agrochemical applications are emerging as a parallel growth engine as regulators tighten controls on volatile organic compounds and environmentally persistent surfactants. Emulsifiers are increasingly specified as part of broader green chemistry strategies, particularly in coatings, crop protection, and polymer processing.

- Strategic investments underline this opportunity. In November 2024, Safic-Alcan acquired a majority stake in Avees Biocos to strengthen the supply of bio-based emulsifiers across Asia-Pacific industrial and personal care markets. In the agrochemical space, Palsgaard introduced Einar 981 in 2025, a plant-based emulsifier designed to replace ethoxylated amines in polymerization and crop applications facing increasing regulatory scrutiny.

- The architectural coatings sector further amplifies demand. As waterborne systems replace solvent-based formulations, bio-based emulsifiers and coalescents have become critical for maintaining film stability and durability. In May 2025, Dow expanded its Decarbia portfolio with low-carbon silicone and conditioning systems that deliver high performance without petroleum-derived surfactants. Collectively, these developments position sustainable emulsifiers as essential inputs for low-VOC industrial growth, rather than optional green alternatives.

Emulsifiers Market Share and Segmentation Insights

Mono- and Di-Glycerides Lead Global Emulsifier Consumption Across Food Formulations

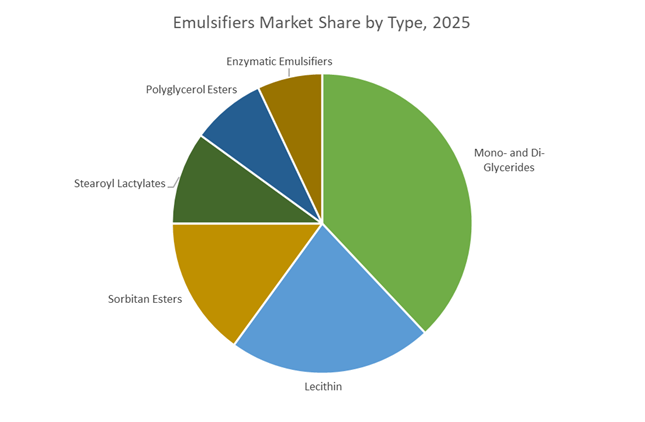

Mono- and di-glycerides command 38% of total emulsifier market share in 2025, reflecting their extensive use in bakery, confectionery, margarine, ice cream, and processed foods. Their cost-effectiveness, multifunctionality, and broad regulatory acceptance position them as foundational ingredients for improving texture, volume, crumb structure, and shelf life. Lecithin maintains a strong market position, particularly soy and sunflower variants, benefiting from clean-label trends and demand for naturally derived emulsifiers in chocolate, bakery, and personal care formulations. Sorbitan esters play a vital role in stabilizing oil-in-water and water-in-oil emulsions across food, cosmetics, and pharmaceutical products. Stearoyl lactylates remain important in bakery applications for gluten strengthening and dough conditioning. Polyglycerol esters are gaining traction in reduced-fat and heat-stable formulations, while enzymatic emulsifiers represent an emerging premium segment aligned with sustainability, precision functionality, and label-friendly positioning.

Food and Beverage Industry Dominates Emulsifier Demand with Broad Application Scope

The food and beverage sector represents 62% of global emulsifier consumption in 2025, reinforcing its leadership across bakery, dairy, beverages, confectionery, and convenience foods. Emulsifiers enable stable fat-water dispersion, improve mouthfeel, extend product shelf life, and support formulation of reduced-fat and plant-based alternatives aligned with evolving consumer preferences. Personal care and cosmetics form a major secondary segment, utilizing emulsifiers in creams, lotions, makeup, and hair care products to achieve stability, texture optimization, and premium sensory performance. Pharmaceutical applications account for a smaller but high-value share, requiring pharmaceutical-grade emulsifiers for oral suspensions, topical treatments, and injectable formulations with strict purity standards. Industrial applications, including agrochemicals, paints and coatings, and polymer processing, represent a growing segment where emulsifiers enhance formulation stability and overall product performance across advanced manufacturing systems.

Competitive Landscape of the Emulsifiers Market

The global emulsifiers market in 2026 is highly consolidated around vertically integrated multinationals and agri-based ingredient giants, with competition centered on clean-label emulsifiers, PCF-zero solutions, lecithin dominance, enzymatic modification, and ESG-compliant supply chains across food, cosmetics, and personal care applications.

BASF SE drives PCF-zero emulsifiers through Verbund integration and circular chemistry

BASF leads the high-performance emulsifiers market by leveraging its Verbund production model and full backward integration into ethylene oxide and fatty alcohols. Its Lamemul® and Lameform® ranges remain industry benchmarks for whipped toppings, margarine, and high-fat dairy stabilization. In March 2024, BASF secured USD 75 million in U.S. government funding to develop low-carbon pathways, enabling the 2026 rollout of Product Carbon Footprint (PCF) Zero emulsifiers. Late 2025 also saw the launch of Ccycled® emulsifiers derived from chemically recycled plastic waste, targeting cosmetics sustainability mandates. BASF’s “2026 Resilience” strategy focuses on logistics optimization to offset 12% raw material cost spikes, ensuring stable pricing in a volatile merchant emulsifiers market.

ADM dominates plant-based lecithin with farm-to-formulation traceability

ADM controls the global lecithin landscape, holding approximately 40% of the product-type segment in 2026 through its Non-GMO soy, sunflower, and canola lecithins. Growth is powered by its Specialty Ingredients division and the PurelyForm™ platform, serving plant-based meat and dairy alternatives. In late 2025, ADM expanded sunflower lecithin capacity in Europe to address soy-free labeling trends and mitigate soybean supply risks. Its vertically integrated model, spanning farm gate to refined emulsifier, delivers 100% traceability aligned with ESG reporting requirements. Strategically, ADM is accelerating enzymatically modified lecithins that deliver superior heat stability for industrial baking, reinforcing its leadership in clean-label emulsifiers for large-scale food manufacturing.

Cargill strengthens turnkey emulsifier systems for global food processors

Cargill positions itself as a “total solution” provider by integrating emulsifiers with texturizers and sweeteners for complete formulation support. Its Lecigran™ and EmulPur™ portfolios anchor applications in chocolate, confectionery, and convenience foods, with a 2026 highlight being liquid sunflower lecithin optimized for high-speed chocolate lines. In February 2026, Cargill prioritized regional sourcing efficiency, shifting production closer to APAC demand hubs to counter tariff volatility. Operating in over 70 countries, the company enables just-in-time delivery, reducing inventory costs for food manufacturers. A 2025 hybrid emulsifier system combining starch stabilizers with monoglycerides now enables up to 20% fat reduction, strengthening Cargill’s role in healthier processed food innovation.

Kerry Group advances clean-label emulsification with AI-driven formulation science

Kerry leads the clean-label emulsifiers segment by focusing on sensory performance, nutrition, and regulatory transparency. Its ULTRALEC® lecithin and MYVEROL™ distilled monoglycerides support brands removing E-numbers in 2026 product reformulations. During 2025 to 2026, Kerry embedded AI-driven predictive modeling into its Sustainably Sourced program, optimizing emulsifier functionality in gluten-free and vegan applications. A new Taste & Nutrition hub in Southeast Asia, opened in late 2025, targets the region’s projected 7.8% CAGR through 2032. Kerry’s “Functional Transparency” strategy delivers digital provenance documentation for palm-derived emulsifiers, ensuring compliance with EU anti-deforestation regulations while strengthening its leadership in clean-label food emulsifiers.

Corbion scales fermentation-based emulsifiers for bakery and confectionery leadership

Corbion differentiates through biotechnology, fermentation-derived ingredients, and high-stability ester emulsifiers. In January 2026, it achieved a CDP ‘A’ climate rating, positioning itself as the most carbon-efficient specialist producer in the emulsifiers market. Its SIMPLY KAKE™ solution, launched with Vantage Food, improves cake volume and shelf life without synthetic additives, supporting clean-label bakery demand. Corbion dominates the bakery and confectionery segment, which holds a 35.4% market share in 2026. Strategic investments in late 2025 upgraded energy systems at ester plants to offset European power costs, while its Natural Mold Inhibition Model integrates emulsification with preservation for extended product freshness.

United States: Clean-Label Scale-Up and Precision Fermentation Convergence

The United States emulsifiers market is undergoing a structural shift toward clean-label, fermentation-enabled, and functionality-driven solutions, supported by large-scale capital deployment. In February 2025, Ingredion Incorporated committed over $100 million to modernize its Indianapolis facility. This investment is specifically aligned with advanced texture solutions and high-efficiency emulsification systems, reflecting rising demand from food manufacturers for clean-label, corn-starch-based texturants that deliver consistent mouthfeel without synthetic additives. Parallelly, Ingredion allocated an additional $50 million to expand its Cedar Rapids, Iowa plant, strengthening capacity for specialty industrial starches used as emulsifying agents in sustainable packaging and paper applications. This dual investment highlights how food and non-food emulsifier demand are increasingly converging around bio-based performance requirements.

Innovation is accelerating beyond physical assets. In May 2025, Ingredion secured exclusive access to precision-fermented Reb M technology following the restructuring of its joint venture with Amyris, enabling the integration of fermentation-derived emulsification aids into sugar-reduced beverage systems planned for 2026 launches. Clean-label sourcing has also expanded upstream. Cargill inaugurated a dedicated sunflower lecithin production facility in late 2024, providing U.S. food processors with non-GMO, allergen-free emulsifiers that bypass soy-related regulatory and consumer constraints. Complementing formulation stability, Balchem invested in a new U.S. microencapsulation facility in December 2025, designed to enhance controlled release and shelf stability of emulsified nutrients in functional and medical nutrition products.

China: Digitalized Chemical Growth and High-End Industrial Emulsifiers

China’s emulsifiers market is being reshaped by national industrial policy emphasizing high-end fine chemicals, digital manufacturing, and downstream value capture. In September 2025, the Ministry of Industry and Information Technology and six other departments released a joint petrochemical and chemical work plan targeting average annual added-value growth exceeding 5% through 2026. Advanced emulsifiers and dispersants for automotive, electronics, and industrial coatings are explicitly prioritized within this framework, signaling a strategic move away from commodity surfactants.

Industrial execution is already visible. In November 2025, BASF commissioned a high-performance production line in Nanjing utilizing Controlled Free Radical Polymerization technology. This facility enables the localized manufacture of advanced emulsifiers and dispersants tailored for low-VOC and high-durability coatings, supporting Asia’s accelerating green construction and electric vehicle manufacturing trends. Additionally, the MIIT’s AI + Petrochemicals initiative launched in late 2025 is incentivizing emulsifier producers to deploy digital twins and real-time process analytics. Plants participating in the program are targeting up to 15% waste reduction in specialty surfactant and emulsifier manufacturing by the end of 2026, strengthening cost competitiveness while improving environmental performance.

India: Infrastructure-Led Demand and Localization of Functional Emulsifiers

India’s emulsifiers market is expanding in tandem with fine chemical infrastructure development, nutraceutical localization, and rising domestic consumption of functional products. In 2025, AMI Organics announced a ₹177 crore expansion of its Jhagadia facility, with commissioning scheduled for the first half of FY 2025-26. While the project includes electrolyte additives, it also targets specialty emulsifiers used in pharmaceuticals, nutrition, and performance formulations, reinforcing India’s role as a regional supplier of value-added ingredients.

On the demand side, localization by global brands is reshaping emulsifier specifications. In July 2025, Otsuka Nutraceutical India expanded its Indian operations, relying on local emulsifier supply chains to produce oral rehydration and functional hydration products. These formulations require enhanced thermal stability to withstand India’s high-temperature logistics environment, driving demand for robust, food-grade emulsification systems. This interplay between infrastructure investment, climate-driven formulation needs, and domestic manufacturing incentives is accelerating the shift toward higher-performance emulsifiers in the Indian market.

Germany (European Union): Regulatory-Driven Purity and Enzymatic Innovation

Germany’s emulsifiers market is being reoriented by tightening EU regulatory frameworks and a strategic pivot toward enzymatic and biotech-derived solutions. Regulation (EU) 2025/351, published in February 2025, introduces stricter purity and documentation requirements for substances used in food-contact materials. Emulsifier manufacturers must now trace and document all Non-Intentionally Added Substances for products sold ahead of the September 2026 compliance deadline, significantly raising the bar for process transparency and analytical control.

Corporate responses underscore this shift. In May 2025, dsm-firmenich completed the acquisition of a European biotechnology startup specializing in enzymatic emulsifiers, strengthening its pipeline of sustainable, high-performance ingredients for dairy and bakery applications ahead of 2026. Meanwhile, Evonik concluded its Tailor Made efficiency program in December 2025, restructuring 90% of its business lines to optimize specialty additives and emulsifiers for its Care and Advanced Technologies segments. This restructuring reflects a strategic narrowing toward higher-margin, regulation-resilient emulsifier applications.

Türkiye: Low-Carbon Manufacturing and Regional Supply Hub Formation

Türkiye is emerging as a strategically located export hub for low-carbon emulsifiers serving adjacent regions. In October 2025, BASF started up a new production line in Dilovası dedicated to low-VOC and low-CO₂ dispersions and emulsifiers. The facility is designed to supply architectural coatings markets across the Middle East and Northwest Africa, regions experiencing rapid urbanization and regulatory tightening on solvent emissions.

A defining feature of the Dilovası expansion is its sustainability profile. The site operates entirely on green electricity and applies the Mass Balance approach, enabling BASF to roll out certified carbon-reduced emulsifier grades by 2026. This positioning allows Turkish production to compete not only on logistics and proximity but also on environmental credentials, increasingly demanded by multinational coatings formulators.

The Netherlands: Portfolio Realignment Toward Fermentation and Plant-Based Systems

The Netherlands is witnessing strategic realignment in the emulsifiers market, marked by capacity expansion in plant-based systems and divestment from legacy portfolios. In early 2025, Cargill announced a 60% expansion of its Deventer coatings and fillings plant. The investment focuses on vegan and dairy-free emulsification systems for confectionery, aligning with Europe’s accelerating demand for plant-based and allergen-free products.

Conversely, Corbion completed the divestment of its traditional emulsifiers business in November 2025 under its Advance 2025 strategy. Capital is being redeployed toward natural preservation and fermentation-derived ingredients as part of the BRIGHT 2030 roadmap, signaling a decisive shift away from conventional emulsifier chemistries toward bio-based, fermentation-led value creation.

Emulsifiers Market: Country-Level Strategic Snapshot

Emulsifiers Market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Key Corporate Actions

|

Structural Implication

|

|

United States

|

Clean-label and fermentation

|

Large-scale plant upgrades, precision fermentation

|

Premium food and nutrition emulsifiers

|

|

China

|

High-end fine chemicals

|

CFRP lines, AI-enabled plants

|

Industrial and coatings emulsifiers

|

|

India

|

Localization and infrastructure

|

Fine chemical expansion, nutraceutical demand

|

Regional specialty supply

|

|

Germany

|

Regulatory compliance and enzymes

|

Enzymatic acquisitions, portfolio restructuring

|

High-purity EU-compliant emulsifiers

|

|

Türkiye

|

Low-carbon export hub

|

Green electricity, mass balance

|

MENA and Africa supply base

|

|

Netherlands

|

Plant-based and fermentation shift

|

Capacity expansion and divestment

|

Next-gen natural emulsifiers

|

Emulsifiers Market Report Scope

Emulsifiers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24 Billion

|

|

Market Size (2034)

|

$46.4 Billion

|

|

Market Growth Rate

|

7.6%

|

|

Segments

|

By Type (Lecithin, Mono- and Di-Glycerides, Sorbitan Esters, Stearoyl Lactylates, Polyglycerol Esters, Enzymatic Emulsifiers), By Source (Plant-Based, Synthetic, Animal-Based), By Form (Liquid, Powder, Pellets), By Function (Emulsification and Stabilization, Texture Improvement, Aeration and Whipping, Shelf-Life Extension), By End-Use Industry (Food and Beverage, Personal Care and Cosmetics, Pharmaceuticals, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ingredion Incorporated, Cargill, Incorporated, Archer Daniels Midland Company, Kerry Group plc, BASF SE, dsm-firmenich AG, Evonik Industries AG, Palsgaard A/S, Corbion N.V., International Flavors & Fragrances Inc., Sakata InX Corporation, Puratos Group, Univar Solutions Inc., Riken Vitamin Co., Ltd., Taiyo Kagaku Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Emulsifiers Market Segmentation

By Type

- Lecithin

- Mono- and Di-Glycerides

- Sorbitan Esters

- Stearoyl Lactylates

- Polyglycerol Esters

- Enzymatic Emulsifiers

By Source

- Plant-Based

- Synthetic

- Animal-Based

By Form

By Function

- Emulsification and Stabilization

- Texture Improvement

- Aeration and Whipping

- Shelf-Life Extension

By End-Use Industry

- Food and Beverage

- Personal Care and Cosmetics

- Pharmaceuticals

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Emulsifiers Industry

- Ingredion Incorporated

- Cargill, Incorporated

- Archer Daniels Midland Company

- Kerry Group plc

- BASF SE

- dsm-firmenich AG

- Evonik Industries AG

- Palsgaard A/S

- Corbion N.V.

- International Flavors & Fragrances Inc.

- Sakata InX Corporation

- Puratos Group

- Univar Solutions Inc.

- Riken Vitamin Co., Ltd.

- Taiyo Kagaku Co., Ltd.

*- List not Exhaustive