Ethyl Lactate Market to Reach $8.5 Billion by 2034 at 7.3% CAGR Driven by Low-VOC Coatings and Semiconductor-Grade Demand

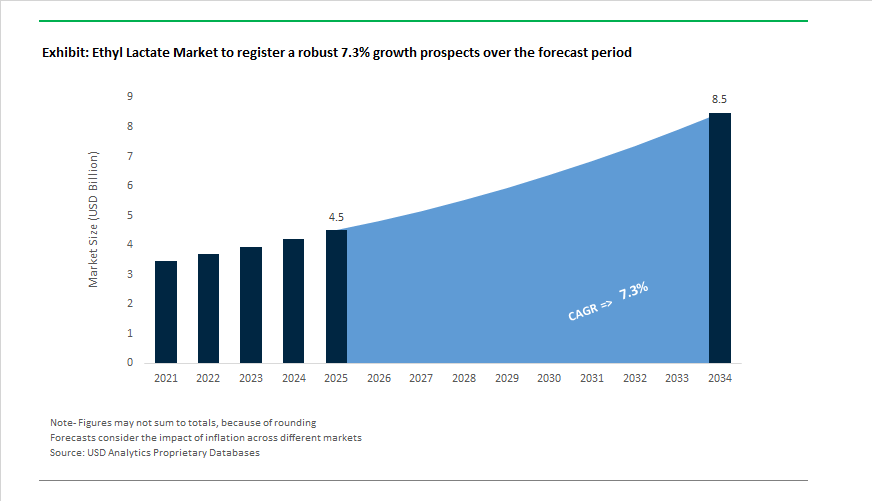

The Ethyl Lactate Market is projected to expand from $4.5 billion in 2025 to $8.5 billion by 2034, registering a CAGR of 7.3%. Growth momentum is anchored in regulatory-driven solvent substitution, semiconductor-grade ultra-purity applications, and the accelerating adoption of bio-based chemicals across coatings, pharmaceuticals, and food processing. Ethyl lactate—derived from lactic acid and ethanol—has transitioned from a niche green solvent to a mainstream industrial alternative to aromatic hydrocarbons such as toluene and xylene. Its biodegradability, low toxicity profile, and favorable solvency parameters make it strategically positioned in the 2026–2034 decarbonization cycle.

In May 2024, the United States Environmental Protection Agency issued updated VOC guidance requiring coatings and adhesives to maintain VOC levels below 0.8 kg per kg of solids. This regulatory tightening directly accelerated ethyl lactate adoption in North American printing inks, packaging laminates, and specialty coatings. Parallel momentum is visible in Europe following the adoption of Regulation (EU) 2024/2895, which enforces stricter microbiological criteria for ready-to-eat foods effective July 2026. Food processors are increasingly shifting to food-grade ethyl lactate as a safe extraction and flavor carrier solvent to meet compliance benchmarks without compromising product safety.

On the production side, Corbion finalized major energy-efficiency upgrades at its esters facilities in December 2025, reinforcing its PURASOLV® EL portfolio with a reduced greenhouse gas footprint. The initiative aligns with EcoVadis Leader status requirements and addresses procurement mandates from semiconductor manufacturers that increasingly demand Scope 3 emission transparency. In its 9M 2025 financial disclosure, Corbion also reported double-digit growth in Health & Nutrition and Pharma segments, supported by rising demand for medical-grade ethyl lactate in biodegradable drug delivery matrices and biocompatible device coatings.

Asia-Pacific has consolidated its position as the global production hub, accounting for over 42% of global output by late 2025. Godavari Biorefineries Limited announced a ₹130 crore grain-based distillery expansion scheduled for commissioning in FY2026, diversifying feedstock risk away from sugarcane and stabilizing ethanol supply for esterification. In February 2026, the company entered a strategic collaboration with Synthomer to develop bio-based solvent alternatives for the European coatings market, leveraging ethyl lactate as a foundational building block.

Japan’s electronics sector is also emerging as a high-margin growth vector. Musashino Chemical Laboratory Ltd expanded high-purity ethyl lactate capacity in 2024–2025 to serve semiconductor fabs and LCD panel manufacturers. Ethyl lactate functions as a resist diluent and cleaning solvent in wafer fabrication, where purity thresholds are stringent and contamination tolerance minimal.

Transformative Trends and High-Growth Opportunities Shaping the Ethyl Lactate Market

REACH Solvent Restrictions and Net Zero Targets Accelerating Green Ethyl Lactate Substitution Trends

The global regulatory phase-out of hazardous solvents is structurally repositioning Ethyl Lactate as a primary bio-based alternative across electronics, pharmaceuticals, and industrial coatings. In June 2025, the European Commission adopted Regulation EU 2025/1090, adding N,N-dimethylacetamide and 1-ethylpyrrolidin-2-one to the REACH Annex XVII Restriction List, with enforcement effective December 23, 2026 prohibiting concentrations above 0.3%. This restriction creates immediate substitution demand in high-solvency applications where reprotoxic and high-VOC solvents were previously dominant. Ethyl Lactate, with a Kauri-Butanol value of approximately 88 compared to Acetone at 84, delivers comparable solvency power while offering significantly lower acute toxicity and reduced dermal exposure risk, strengthening its position as a drop-in replacement solvent in precision cleaning and pharmaceutical synthesis.

Sustainability metrics further reinforce this transition. Life Cycle Assessment data published in October 2025 demonstrate that switching to lactate esters can reduce greenhouse gas emissions by up to 70% relative to petroleum-derived solvents, directly aligning with Net Zero and Scope 3 reduction targets across paints, coatings, and specialty chemicals industries. As regulatory compliance, occupational safety, and decarbonization converge, bio-based Ethyl Lactate is gaining structural preference in solvent reformulation strategies across the global chemical value chain.

Circular Bioeconomy and Food Waste Valorization Strengthening Sustainable Feedstock Trends

The Ethyl Lactate market is increasingly embedded within the circular bioeconomy, with feedstock strategies shifting from food-competing starch to agricultural residues and urban food waste. In February 2026, researchers at the Pune Institute in India demonstrated a scalable process converting restaurant food waste into process-ready lactic acid with a sugar extraction efficiency of 90.17% and a lactic acid titer of 91 g/L, outperforming traditional lignocellulosic fermentation routes. This breakthrough enhances supply resilience while lowering raw material volatility in bio-based solvent production.

Further innovation in pretreatment technologies is accelerating cost competitiveness. A December 2025 global biorefinery review highlighted that low-frequency acoustic cavitation at 24 kHz can increase L-lactic acid production by 92% from food waste substrates, reducing net treatment costs by approximately €153 per ton. Major producers such as Corbion are expanding lactic acid capacity in North America and Europe to integrate second-generation feedstocks, reinforcing Ethyl Lactate’s sustainability credentials and stabilizing long-term supply chains within the green solvent market.

Electronic-Grade Ethyl Lactate Unlocking Semiconductor and Advanced PCB Cleaning Opportunities

As semiconductor nodes advance toward 2 nm and 3 nm geometries, demand for electronic-grade Ethyl Lactate exceeding 99.8% purity is rising sharply due to its effectiveness in photoresist stripping and delicate wafer cleaning. By January 2026, Asia-Pacific accounts for 45% of global consumption of electronic-grade lactate esters, supported by fabrication capacity expansion in Taiwan, South Korea, and Japan. The solvent’s low toxicity and high solvency performance make it particularly suitable for Edge Bead Removal formulations and plasma etch residue cleaning in high-density semiconductor and PCB manufacturing.

In 2025, Ethyl Lactate was recognized as a superior alternative to Methyl Ethyl Ketone and toxic glycol ethers, delivering residue-free cleaning without compromising silicon wafer integrity. Producers including Godavari Biorefineries reported increased demand for high-purity variants with minimum assay levels of 99.00% for use as carrier solvents in advanced lithography and electronics applications. This shift toward high-value, electronic-grade solvent grades is positioning semiconductor manufacturing as a premium growth segment within the global Ethyl Lactate market.

Platform Chemical Role in PLA Recycling and Biopolymer Integration Driving Circular Polymer Opportunities

Beyond its solvent applications, Ethyl Lactate is emerging as a strategic intermediate in the chemical recycling and production of Polylactic Acid, one of the fastest-growing biodegradable biopolymers. In October 2025, researchers at the University of Bath demonstrated catalytic depolymerization of post-consumer PLA waste to produce Ethyl Lactate at a 71% yield under mild conditions of 50°C, creating a circular pathway for end-of-life bioplastics. This innovation supports closed-loop recycling strategies in sustainable packaging and reduces dependency on virgin lactic acid feedstock.

Advancements in solvent-assisted transesterification reported in 2025 achieved an 80% yield of Ethyl Lactate from commingled plastic streams while retaining full stereochemical purity, a critical requirement for high-performance PLA resin synthesis. Major agri-industrial players such as Cargill and ADM introduced integrated bio-based product lines in 2025 linking Ethyl Lactate production with downstream biopolymer manufacturing. This vertical integration strategy is designed to capture rising demand for compostable food-contact packaging and reinforces Ethyl Lactate’s expanding role as a platform chemical within the global bio-based materials economy.

Ethyl Lactate Market Share and Segmentation Insights

Solvent Applications Drive Adoption of Bio-Based Ethyl Lactate Across Industrial Formulations

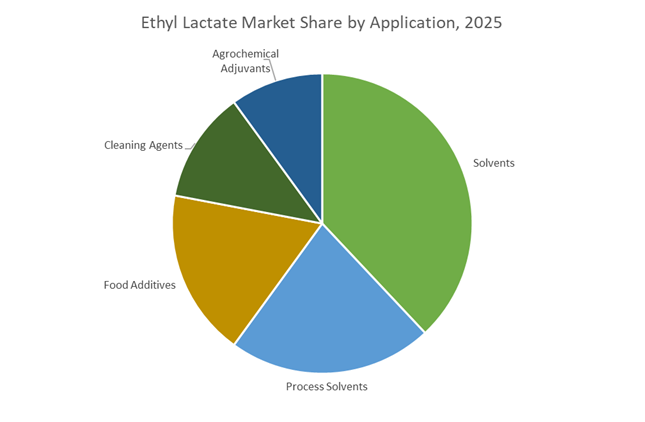

Solvents account for 38% of ethyl lactate demand in 2025, positioning this segment as the primary growth engine for the market. Ethyl lactate is increasingly adopted as a high-performance, biodegradable alternative to NMP, toluene, and chlorinated solvents in coatings, printing inks, and industrial cleaning due to its strong solvency for cellulose derivatives, resins, and polymers. Process solvents represent a significant secondary segment, particularly in pharmaceutical and fine chemical manufacturing, where ethyl lactate functions as a reaction medium and extraction solvent aligned with green chemistry initiatives. Food additives maintain an important share, supported by ethyl lactate’s GRAS status and use as a flavoring agent and food-grade extraction solvent. Cleaning agents are expanding rapidly, leveraging ethyl lactate in degreasers and precision cleaners for its oil-dissolving capability and user safety profile, while agrochemical adjuvants remain a niche but strategic application.

Food and Beverage Processing Leads End-Use Supported by Coatings and Semiconductor Growth

Food and beverage processing represents 32% of global ethyl lactate consumption in 2025, driven by its dual role as a natural flavoring agent and food-grade cleaning solvent for processing equipment. Paints, coatings, and inks form a major secondary segment, utilizing ethyl lactate in low-VOC formulations as a coalescing agent and solvent to meet tightening environmental regulations without sacrificing performance. Electronics and semiconductors are emerging as a high-growth end-use industry, adopting high-purity ethyl lactate in photoresist formulations and precision cleaning where ultra-low residue is essential. Pharmaceuticals and healthcare maintain strong uptake for extraction and processing applications, supported by ethyl lactate’s favorable toxicological profile. Agrochemicals show steady demand through adjuvant and solvent use, while personal care and cosmetics remain niche, incorporating ethyl lactate in nail care, makeup removers, and skincare products targeting sustainability-conscious consumers.

Competitive Landscape of the Ethyl Lactate Market

The global ethyl lactate market in 2026 is shaped by bio-based solvent adoption, semiconductor-grade purity requirements, and aggressive sustainability mandates, with leaders competing on vertical integration, electronic-grade performance, and low-carbon production technologies.

Corbion N.V. drives electronic-grade ethyl lactate with ultra-low metal purity

Corbion is the undisputed global leader in lactic acid derivatives, leveraging vertically integrated fermentation to supply the highest-purity ethyl lactate for microelectronics and advanced manufacturing. Its PURASOLV® ELECT and ELECT Ultra grades feature ultra-low metal content below 500 ppt, making them critical for semiconductor cleaning and photoresist processing. In 2025–2026, Corbion introduced a novel solid-state catalyst process that cut energy consumption by ~15% while improving batch consistency. Strategically, the company is pursuing “sustainability-driven high performance,” targeting full defossilization of semiconductor solvents by 2030. Its core advantage remains in-house L-lactic acid production from renewable carbohydrates, delivering full traceability and supply security for global chipmakers.

Galactic expands bio-based ethyl lactate across personal care and coatings

Galactic is a premier innovator in fermentation chemistry, positioning its Galaster® ethyl lactate range as a non-toxic solvent for cosmetics, pharmaceuticals, and industrial cleaning. In late 2025, the company expanded APAC distribution hubs in China and India to capture rising 2026 demand for clean-label personal care ingredients. Galactic holds a strong foothold in food and beverage applications, where ethyl lactate functions as a natural flavor carrier and essential oil extraction solvent. In early 2026, it signed multi-year agreements with European paint manufacturers to replace phthalate-based solvents in industrial coatings, reinforcing its role in bio-based solvent substitution and low-VOC formulation strategies.

Musashino Chemical Laboratory, Ltd. supplies ultra-pure ethyl lactate to 2nm and 3nm semiconductor fabs

Musashino is the quality benchmark in East Asia, specializing in electronic-grade ethyl lactate with purity exceeding 99.9% for edge-bead removal and photoresist thinning. By 2026, it accounted for a significant share of ethyl lactate used in the world’s most advanced 2nm and 3nm semiconductor fabrication plants across Japan and South Korea. Its precision purification capabilities are globally recognized. In February 2026, Musashino expanded its Japan R&D center to develop hybrid lactate esters that combine ethyl lactate solvency with higher boiling profiles. Deep integration into amino acid and pyruvate value chains further enables co-production of synergistic specialty chemicals.

Godavari Biorefineries Ltd. scales grain-based ethyl lactate for import substitution and exports

Godavari Biorefineries is a leading Indian biorefinery pioneer, converting sugarcane and grain feedstocks into bio-based solvents for global markets. In Q4 FY26, the company is commissioning a new 200 KLPD grain distillery backed by a $15 million investment, materially increasing ethanol and downstream ethyl lactate capacity. In February 2026, Godavari partnered with Synthomer to develop bio-based monomer alternatives using ethyl lactate as a core intermediate. The company focuses on bio-ethyl acetate and ethyl lactate for India’s import substitution drive while expanding exports to Europe. Its circular economy model uses sugar-industry waste streams to power plants, delivering a best-in-class carbon footprint.

Vertec BioSolvents, Inc. dominates agrochemical ethyl lactate with EPA-approved formulations

Vertec BioSolvents is a high-agility North American specialist targeting bio-solvent replacement in industrial and agrochemical markets. Its VertecBio™ EL is approved as a US EPA List 4A inert ingredient, enabling low-toxicity pesticide and herbicide formulations without tolerance requirements. Vertec leads the agrochemical ethyl lactate segment, supplying stable emulsions for modern crop protection systems. In 2025–2026, the company launched precision-cleaning blends for aerospace and military electronics, delivering zero-residue performance without chlorinated solvents. Strategically, Vertec focuses on regulatory arbitrage, positioning ethyl lactate as the primary alternative to solvents restricted under EPA Safer Choice programs and California VOC mandates.

United States: Regulatory Fast-Tracking and Semiconductor-Grade Demand

The U.S. ethyl lactate market is being structurally reshaped by regulatory endorsement and strategic reshoring of advanced manufacturing. Under the U.S. Environmental Protection Agency Significant New Alternatives Policy program, updated in 2025, ethyl lactate has been formally fast-tracked as a preferred green substitute for ozone-depleting and high-GWP solvents. This regulatory signal translated directly into market uptake, with eco-solvent adoption within the South Coast Air Quality Management District rising by 19% through late 2025 as industrial users accelerated solvent substitution programs to remain compliant with tightening VOC thresholds.

At the same time, semiconductor supply chain localization is driving demand for ultra-high-purity grades. Following CHIPS and Science Act disbursements, seven out of ten new semiconductor fabrication units commissioned during 2024–2025 integrated ethyl lactate with purity levels exceeding 99.8% for photoresist stripping and wafer cleaning. Trade tariff escalations in early 2025 further amplified this shift, as price volatility in petroleum-derived solvents improved the relative cost stability of bio-based ethyl lactate. Downstream diversification is also visible in the pet nutrition sector, where updated FDA clean-label guidance finalized in December 2025 prompted major brands to adopt ethyl lactate as a carrier solvent for natural flavor extracts, reinforcing its role beyond industrial cleaning applications.

India: Feedstock Integration and Pharmaceutical Excipient Localization

India’s ethyl lactate market is anchored in upstream ethanol security and policy-driven pharmaceutical localization. In January 2025, Aarti Industries Ltd. commissioned a major ethylation capacity expansion at the Dahej Special Economic Zone, tripling output from 10 KTPA to 30 KTPA. This multipurpose ethylation infrastructure allows producers to flex capacity toward high-growth lactate esters, improving responsiveness to pharmaceutical and electronics solvent demand cycles.

Feedstock resilience has been reinforced by distillery investments. Godavari Biorefineries Ltd. completed a Rs 130 crore corn and grain-based distillery project in 2025, securing dedicated bio-ethanol supply for esterification routes. On the demand side, India’s Production Linked Incentive scheme approved funding in mid-2025 for three new high-purity solvent lines, explicitly targeting import substitution of pharmaceutical-grade ethyl lactate used in topical drug delivery and transdermal systems. Regulatory digitalization is adding another layer of momentum, with the January 2026 Catalysts for Change initiative mandating real-time VOC tracking, effectively favoring bio-based solvents with predictable emission profiles.

China: VOC Enforcement and Cost-Leadership at Scale

China’s ethyl lactate market expansion is primarily regulation-driven but reinforced by scale economics. Under the country’s Dual Carbon and Ecological Civilization mandates, stricter VOC enforcement in the Yangtze River Delta chemical cluster has compelled manufacturers to accelerate adoption of biodegradable solvents. By early 2026, procurement of eco-friendly solvents recorded a leading growth rate of 9.6 %, positioning ethyl lactate as a compliance-ready alternative for coatings, electronics, and food extraction applications.

Product diversification is expanding alongside volume. In July 2025, Chinese regulators approved new algae-derived and bio-fermented omega-3 formulations that rely on food-grade ethyl lactate as a primary extraction solvent to meet natural certification requirements. Structurally, China benefits from agricultural feedstock abundance. Leveraging corn starch surpluses, Chinese producers are maintaining cost leadership, and by 2026 more than half of global ethyl lactate capacity is concentrated within the China–India corridor. This scale advantage is reinforcing China’s role as both a domestic compliance supplier and an export anchor for price-sensitive markets.

Germany: REACH-Driven Substitution and Medical-Grade Precision

Germany represents the regulatory and quality frontier for ethyl lactate adoption in Europe. The implementation of new REACH restrictions on CMR substances effective September 1, 2025 has forced industrial formulators to proactively replace traditional solvents with biodegradable alternatives to avoid concentration limit penalties. Ethyl lactate has emerged as a primary beneficiary due to its favorable toxicological profile and established biodegradability credentials.

By 2025, industrial audits indicated that more than 62% of European chemical manufacturers had integrated ethyl lactate into at least one formulation line, reflecting accelerated substitution momentum. German producers are also pushing purity boundaries. Companies such as CABB GmbH and Merck KGaA upgraded analytical and purification systems ahead of 2026 to meet zero-impurity expectations for medical-grade solvents used in advanced drug delivery platforms. This positions Germany as a premium compliance and quality reference point within the global ethyl lactate value chain.

Strategic Snapshot: Ethyl Lactate Market by Country (2025–2026)

Ethyl Lactate Market County Level Snapshot

|

Country

|

Primary Catalyst

|

Industrial Focus

|

Strategic Implication

|

|

United States

|

EPA SNAP fast-tracking, CHIPS Act

|

Semiconductor-grade, clean-label solvents

|

Regulatory-led demand acceleration

|

|

India

|

Ethanol integration, PLI incentives

|

Pharma excipients, import substitution

|

Feedstock-secure growth platform

|

|

China

|

VOC enforcement, scale economics

|

Eco-solvents, food extraction

|

Cost leadership with compliance

|

|

Germany

|

REACH CMR restrictions

|

Medical-grade, zero-impurity solvents

|

Premium quality benchmark

|

Ethyl Lactate Market Report Scope

Ethyl Lactate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.5 Billion

|

|

Market Size (2034)

|

$8.5 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Grade (Industrial Grade, Food Grade, Pharmaceutical Grade, Electronic Grade), By Application (Solvents, Process Solvents, Food Additives, Cleaning Agents, Agrochemical Adjuvants), By End-Use Industry (Food and Beverage Processing, Electronics and Semiconductors, Pharmaceuticals and Healthcare, Paints, Coatings and Inks, Personal Care and Cosmetics, Agrochemicals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Corbion N.V., Galactic, Archer Daniels Midland Company, BASF SE, Eastman Chemical Company, Dow Inc., Musashino Chemical Laboratory, Ltd., Vertec BioSolvents, Inc., Godavari Biorefineries Limited, Aarti Industries Limited, Henan Kangyuan, CABB GmbH, Stepan Company, Perstorp Holding AB, DIC Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ethyl Lactate Market Segmentation

By Grade

- Industrial Grade

- Food Grade

- Pharmaceutical Grade

- Electronic Grade

By Application

- Solvents

- Process Solvents

- Food Additives

- Cleaning Agents

- Agrochemical Adjuvants

By End-Use Industry

- Food and Beverage Processing

- Electronics and Semiconductors

- Pharmaceuticals and Healthcare

- Paints, Coatings and Inks

- Personal Care and Cosmetics

- Agrochemicals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ethyl Lactate Industry

- Corbion N.V.

- Galactic

- Archer Daniels Midland Company

- BASF SE

- Eastman Chemical Company

- Dow Inc.

- Musashino Chemical Laboratory, Ltd.

- Vertec BioSolvents, Inc.

- Godavari Biorefineries Limited

- Aarti Industries Limited

- Henan Kangyuan

- CABB GmbH

- Stepan Company

- Perstorp Holding AB

- DIC Corporation

*- List not Exhaustive