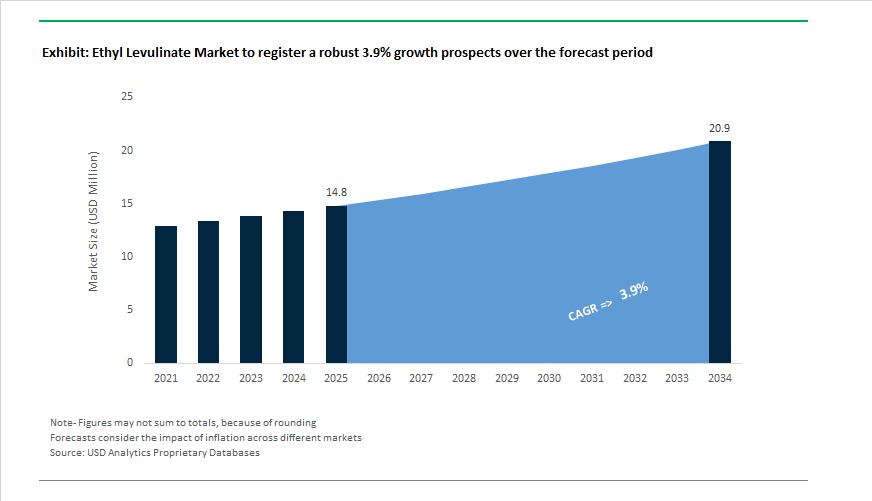

Ethyl Levulinate Market to Reach $20.9 Million by 2034 at 3.9% CAGR Amid Bio-Solvent Adoption and Waste-to-Chemical Scale-Up

The Ethyl Levulinate Market is projected to grow from $14.8 Million in 2025 to $20.9 Million by 2034, registering a CAGR of 3.9%. Market expansion is being shaped by tightening European solvent regulations, increasing diesel blending trials in Southeast Asia, and structural investment in biomass-to-chemical technologies. Ethyl levulinate, produced via esterification of levulinic acid and ethanol, is transitioning from a niche specialty solvent to a platform molecule within the broader bio-based chemicals ecosystem. Its biodegradability, favorable solvency parameters, and compatibility with existing fuel and coating systems position it as a strategic alternative to high-VOC petrochemical solvents and silicone-based emollients.

In October 2025, GFBiochemicals launched RE:CHEMISTRY NEW320 (Ethyl Propanediol Acetal Levulinate), targeting the personal care sector’s migration away from cyclopentasiloxane (D5) ahead of stricter 2026 European environmental enforcement. The product replicates silicone-like volatility and skin feel while maintaining full biodegradability, directly addressing regulatory and consumer pressure for microplastic-free and non-persistent cosmetic formulations. To support scale-up, GFBiochemicals simultaneously strengthened senior leadership appointments focused on procurement and manufacturing expansion, reflecting accelerating demand across its Solve100 and Move200 bio-solvent portfolios.

Industrial decarbonization pathways are reinforcing supply-side innovation. In July 2024, Biofine Technology initiated the pre-commercial rollout of its Maine-based biomass conversion facility using municipal solid waste (MSW) as feedstock. The company targets a 10,000 tons per year capacity by late 2026, marking a notable milestone in waste-to-ethyl levulinate commercialization. Meanwhile, India’s decision in September 2025 to remove quantitative restrictions on ethanol production from sugarcane derivatives ensures abundant bio-ethanol availability for domestic esterification, strengthening Asia’s competitive cost position. Latin America is also emerging as an export-oriented supplier; Brazil and Argentina are leveraging sugarcane bagasse and cassava waste to pilot integrated biomass-to-ester facilities aimed at European markets.

Fuel and CASE (Coatings, Adhesives, Sealants, Elastomers) applications are broadening the market base. In January 2024, Langfang Triple Well Chemicals signed a distribution agreement supporting diesel blending trials in Malaysia and Thailand, positioning ethyl levulinate as a lubricity enhancer and sulfur-emission reducer. BTC Europe and NXTLEVVEL Biochem expanded distribution across Europe for high-purity grades serving industrial cleaning and coatings. In February 2026, Avantium partnered with Will & Co to integrate levulinic derivatives into sustainable resin systems, reinforcing ethyl levulinate’s role as a green modifier within advanced polymer formulations.

Beyond solvents and fuels, specialty niches are gaining traction. Lallemand Inc reported progress in flavor-enhancing applications for plant-based meats, leveraging the ester’s mild fruity and caramel notes. Spanish fragrance house Puig adopted >98% purity bio-esters, including ethyl levulinate, in its eco-fragrance lines during 2025, achieving measurable export growth in Europe.

Trends and Opportunities in the Ethyl Levulinate Market

Industrial Scale-Up as a Drop-In Bio-Based Platform Solvent

- Ethyl levulinate is moving rapidly from laboratory validation to industrial-scale deployment as production economics improve and downstream demand solidifies. Proprietary catalytic pathways and integration with existing biomass processing infrastructure have narrowed the cost gap with fossil-derived solvents, enabling broader commercial uptake.

- In October 2025, GFBiochemicals expanded its RE:CHEMISTRY® portfolio with the launch of NEW320, a plant-based solvent and emollient derived from ethyl levulinate ketals. The product is positioned as a direct replacement for cyclopentasiloxane in cosmetic formulations, addressing regulatory pressure on silicones while delivering high renewable carbon content aligned with EU Green Deal environmental footprint criteria.

- To accelerate market penetration, NXTLEVVEL Biochem, a joint venture between Towell Engineering and GFBiochemicals, finalized a pan-European distribution agreement with BTC Europe. Active through 2025, this partnership enables large-scale adoption of levulinate solvents in industrial and institutional cleaning as well as agricultural coatings, reducing the commercialization gap between bio-refineries and end users.

- Cost competitiveness is being further enhanced through side-stream integration. In mid-2025, multiple bio-based startups in Canada and the Netherlands secured Series B funding to attach demonstration units to pulp mills and agro-processing facilities. Industrial trials using corn cobs and bagasse reported ethyl levulinate yields of up to 29.2 %, highlighting the potential to reduce feedstock costs while valorizing agricultural waste.

Strategic Integration into Natural Fragrance and Flavor Supply Chains

- Ethyl levulinate’s mild fruity and caramel-like profile has positioned it as a high-value intermediate in clean-label fragrance and flavor formulations. As sustainability becomes a purchasing driver rather than a marketing differentiator, aroma houses are prioritizing ingredients with verified natural origin and favorable toxicological profiles.

- Consumer research conducted in 2024–2025 indicates that nearly 70% of U.S. consumers actively prioritize sustainable and natural-origin claims in personal care products. This shift has elevated ethyl levulinate as a preferred modifier in perfumes and body sprays, particularly for brands seeking biodegradable alternatives to synthetic fixatives.

- Formulation synergies are also emerging in food innovation. Lallemand Inc. announced initiatives in early 2025 to incorporate bio-based additives such as ethyl levulinate into plant-based meat analogues. Its ability to enhance flavor perception while maintaining non-toxicity and biodegradability supports the health and wellness positioning of next-generation protein products.

- From a safety and compliance perspective, 2025 evaluations by Research Institute for Fragrance Materials confirmed the absence of genotoxicity concerns for levulinic acid derivatives at current usage levels. This clearance has removed a key barrier to adoption in premium skincare and sun care products, categories that recorded average annual unit growth of approximately 5.6% in 2025.

Performance-Enhancing Additive for Next-Generation Biofuels

- Ethyl levulinate is gaining traction as a multifunctional additive for low-carbon fuels, particularly as a diluent and oxygenate that improves biodiesel performance. Its role in cold-flow enhancement and soot reduction positions it as a practical bridge fuel while electrification of heavy transport continues to scale.

- A May 2025 study published in Biomass and Bioenergy confirmed that ethyl levulinate significantly improves lubricity and reduces particulate emissions when blended with conventional diesel. In Colombia, policy discussions around a 20% ethyl levulinate blend have translated into a potential demand of roughly 9,400 tons per month to meet domestic fuel requirements.

- Technological advances are reinforcing supply scalability. Microwave-assisted catalysis developments reported in 2024–2025 achieved complete conversion of 5-HMF to ethyl levulinate, addressing a historical yield bottleneck. These gains are particularly relevant for aviation and maritime stakeholders evaluating oxygenates that support compliance with ICAO CORSIA emissions frameworks.

- Brazil provides a representative case study. With its bioeconomy projected to expand at roughly 8% annually through 2025, ethyl levulinate is increasingly viewed as a compatible drop-in component that leverages existing engine infrastructure while supporting national decarbonization objectives.

Non-Phthalate Plasticizers and Biodegradable Polymer Additives

- The global move away from ortho-phthalates is creating a structurally attractive opportunity for ethyl levulinate-derived plasticizers in both legacy and bio-based polymers. Regulatory pressure in Europe and North America has accelerated demand for alternatives that combine mechanical performance with high bio-content.

- In February 2025, research published in ACS Sustainable Chemistry and Engineering introduced bioplasticizers synthesized from ethyl levulinate ketals. When incorporated into polyhydroxyalkanoates, these additives significantly enhanced thermal stability and flexibility, expanding the application envelope of biodegradable plastics.

- Performance data from recent trials underscores the material potential. In polylactic acid formulations, the inclusion of 20 weight% levulinic acid ester achieved elongation at break exceeding 500 %, rivaling conventional citrate plasticizers while substantially increasing renewable content. This positions ethyl levulinate as a viable solution for rigid and flexible packaging seeking regulatory compliance without performance trade-offs.

- Beyond additives, ethyl levulinate is emerging as a monomer platform. Research published in April 2025 by the National Institute for Technology Karnataka demonstrated sustainable pathways to ketal derivatives suitable for poly(levulinate ester) synthesis. These materials are under evaluation for high-end medical packaging and agricultural mulching films, signaling longer-term upside beyond solvent and additive markets.

Ethyl Levulinate Market Share and Segmentation Insights

Industrial Grade Ethyl Levulinate Anchors Volume Demand Across Solvents and Biofuel Blends

Industrial grade ethyl levulinate commands 58% of total market share in 2025, reflecting its role as the standard specification for solvents, biofuel additives, and agrochemical formulations. Its cost efficiency and adequate purity support large-scale industrial adoption, particularly in renewable solvent systems and green fuel blending. Technical grade holds a meaningful share in polymer processing and plasticizer applications where intermediate purity is required for formulation stability. Food grade remains a smaller but premium segment, supplying fragrances, flavors, and pharmaceutical intermediates that demand strict regulatory compliance and human-contact safety. Across grades, ethyl levulinate benefits from rising interest in biomass-derived chemicals, positioning it as a versatile platform molecule within sustainable chemistry value chains.

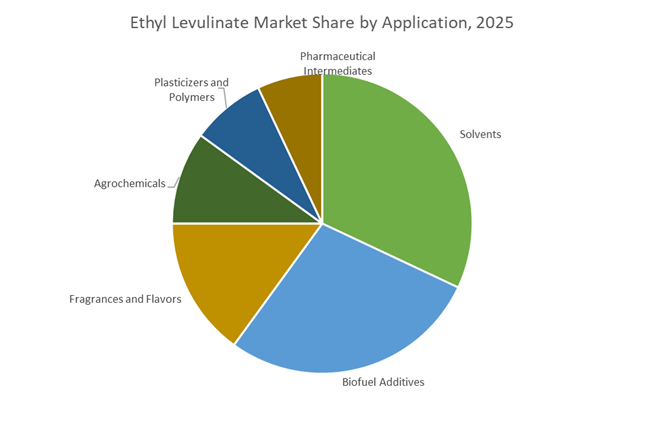

Solvents and Biofuel Additives Lead Application Growth for Renewable Levulinate Esters

Solvents account for nearly 32% of ethyl levulinate demand in 2025, driven by its use as a biodegradable replacement for petroleum-based solvents in coatings, industrial cleaners, and specialty chemical processing. Biofuel additives represent a major growth segment, with ethyl levulinate blended into diesel and biodiesel to improve cold-flow properties, reduce emissions, and increase renewable content. Fragrances and flavors maintain an important share, leveraging ethyl levulinate’s fruity sensory profile and GRAS status in premium formulations. Agrochemicals show steady uptake through solvent and adjuvant applications, while plasticizers and polymers are expanding as manufacturers adopt ethyl levulinate as a renewable plasticizer and bio-based polymer intermediate. Pharmaceutical intermediates remain niche but strategic, supporting sustainable API synthesis and drug development pathways.

Competitive Landscape of the Ethyl Levulinate Market

The ethyl levulinate market in 2026 is defined by bio-based solvent innovation, green chemistry adoption, and rising demand from personal care, coatings, flavors & fragrances, and specialty intermediates, with competition centered on IP depth, purity standards, and sustainable distribution networks.

GFBiochemicals pioneers green solvent scale-up with patented levulinic acid technology

GFBiochemicals is the primary architect of the global levulinic acid value chain, leveraging more than 200 proprietary patents to maintain a commanding position in bio-based ethyl levulinate. Its flagship Solve100™ is positioned as a high-performance sustainable solvent for personal care formulations and industrial coatings, directly replacing petrochemical alternatives. In 2025/2026, the company earned an EcoVadis Silver rating and the ICIS Innovation Award for its RE:CHEMISTRY® circular production platform, reinforcing its ESG leadership. Commercial momentum accelerated through a strategic distribution partnership with BTC Europe, enabling EU-wide penetration. GFB’s core strength remains intellectual property dominance, creating a substantial competitive moat in the fast-growing green solvent and renewable ester markets.

Merck KGaA sets purity benchmarks for pharma, fragrance, and analytical ethyl levulinate

Merck, through its Sigma-Aldrich life science portfolio, anchors the purity-critical segment of the ethyl levulinate market, supplying both Natural (98%) and Synthetic (99%) grades compliant with FCC and JECFA standards. The company dominates analytical, pharmaceutical, and fragrance applications, where ethyl levulinate serves as a reference compound for wine aroma profiling and advanced organic synthesis. In 2025, Merck expanded its “Greener Alternative Products” program, formally classifying bio-derived ethyl levulinate under the 12 Principles of Green Chemistry. Rather than competing on volume, Merck focuses on high-margin specialty grades, reinforcing its role as the quality benchmarking leader for R&D labs and regulated end markets.

Vigon International accelerates clean beauty adoption through agile F&F distribution

Vigon International, backed by Azelis’ global network, acts as a critical bridge between bulk producers and premium flavor and fragrance brands in North America. By 2026, Vigon emerged as a key supplier to the Clean Beauty movement, positioning ethyl levulinate as a sustainable scent fixative and functional solvent. Its FEMA 2442-certified grade delivers distinctive green, fruity, and apple-like notes for food and beverage formulations. In 2025, Vigon implemented digital batch tracking, enabling real-time verification of biomass origin and carbon footprint. The company’s core advantage lies in agile distribution, customized blending, and just-in-time delivery, making it a preferred partner for mid-sized fragrance houses.

Advanced Biotech strengthens natural ethyl levulinate supply for food-grade applications

Advanced Biotech specializes in fermentation-derived natural ethyl levulinate, targeting highly regulated food and beverage markets. Its product portfolio is engineered for flavor enhancement in dairy, confectionery, and savory systems, where ethyl levulinate stabilizes aroma compounds and improves sensory longevity. In 2026, the company secured Non-GMO and EU Natural certifications, aligning with stricter transparency and clean-label mandates from global food manufacturers. Advanced Biotech’s strategic focus on “Natural Identity” ensures regulatory compliance across multiple jurisdictions, positioning it strongly within premium natural ingredients. The company’s fermentation-first approach differentiates it from synthetic suppliers, supporting sustained growth in bio-based flavor carriers and clean-label formulations.

Tokyo Chemical Industry Co., Ltd. expands APAC ethyl levulinate use in electronics and green resins

Tokyo Chemical Industry (TCI) leads the Asia-Pacific specialty reagent segment, supplying ethyl levulinate as a versatile chemical intermediate for electronics, biodiesel, and advanced polymer applications. In late 2025, TCI expanded logistics hubs in Shanghai and Hyderabad to support surging APAC demand for bio-based intermediates. Its 2026 industrial-grade blends are now used as high-efficiency biodiesel diluents, improving cold-flow performance, while also serving as building blocks for green resins and 3D-printing plasticizers. TCI’s massive catalog breadth, spanning methyl, ethyl, and butyl levulinates, enables one-stop procurement for research labs and specialty manufacturers, reinforcing its role as the region’s reagent market leader.

India: BioE3 Policy Execution and Feedstock-Led Export Scalability

India has emerged as one of the most structurally advantaged markets for ethyl levulinate, driven by synchronized bioeconomy policy execution and ethanol feedstock abundance. The operationalization of the BioE3 Policy in late 2025 marks a decisive shift from pilot-scale bio-based chemistry toward high-performance biomanufacturing. Levulinic acid esters, including ethyl levulinate, are explicitly identified as strategic molecules within this framework, unlocking fiscal incentives, accelerated approvals, and infrastructure support for domestic producers. Parallel to this, the redirection of surplus ethanol during the 2025–2026 Ethanol Supply Year has materially altered cost economics. With Oil Marketing Companies allocating over 1,048 crore liters of ethanol and restrictions lifted on sugarcane juice and molasses usage, ethyl levulinate producers now benefit from a structurally low-cost and reliable alcohol feedstock base.

Institutionally, the Department of Biotechnology has reinforced this trajectory through the establishment of bio-foundries designed to compress lab-to-pilot timelines for platform chemicals. Demand-side pull is equally visible. Growth in India’s processed food sector is accelerating the use of ethyl levulinate as a FEMA-compliant natural flavoring, particularly in ready-to-eat desserts and beverages. Agrochemical formulators are also transitioning toward levulinate-based solvents in response to Green Growth standards introduced under the Union Budget. Investments in rice-to-ethanol distilleries commissioned in 2025 further insulate ethyl levulinate synthesis from food-versus-fuel risks, positioning India as a scalable export hub rather than a purely domestic consumption market.

Italy: Commercialization Leadership and Fragrance-Led Pull

Italy represents the global commercialization nerve center for ethyl levulinate, anchored by GFBiochemicals, which continues to define industrial benchmarks for levulinate chemistry. In October 2025, the company expanded its leadership and capital footprint to scale its RE:CHEMISTRY® portfolio, where ethyl levulinate is positioned as a direct replacement for fossil-derived solvents across multiple end uses. Crucially, late-2025 marked the transition of levulinate production from pilot-scale validation to world-scale commercialization, enabled by a proprietary one-step synthesis route that materially lowers production costs and energy intensity.

Downstream integration is strongest in the fragrance and personal care ecosystem. Luxury perfume houses across the Milan–Turin corridor have incorporated ethyl levulinate into 2026 launches, leveraging both its sensory profile and its regulatory alignment with EU Green Deal objectives. This industrial uptake is being reinforced by applied research. Collaborative work involving Italian industry partners and European universities has produced new patent filings focused on defossilizing detergents and home care formulations using ethyl levulinate. Collectively, Italy’s role is less about volume leadership and more about setting commercialization, formulation, and regulatory narratives that influence global adoption curves.

United States: Federal Endorsement and Application-Led Diversification

In the United States, ethyl levulinate adoption is being shaped by federal validation and cross-sector application expansion rather than feedstock scale alone. The U.S. Department of Energy has reaffirmed levulinate technologies as critical bio-based building blocks, a designation that has unlocked targeted grants for biodiesel additive and solvent commercialization pathways throughout 2025. Regulatory pressure from the U.S. Environmental Protection Agency has further accelerated substitution dynamics, as tighter scrutiny of petrochemical solvents is pushing industrial users toward biodegradable, low-toxicity alternatives such as ethyl levulinate.

Structurally, the integration of U.S. levulinate technology into European portfolios following the acquisition of Segetis has created a transatlantic supply chain capable of serving coatings, cleaning, and polymer additive markets by 2026. The food and beverage sector provides an additional layer of stability. The 2025 FEMA safety reassessment reaffirmed ethyl levulinate’s GRAS status, directly triggering higher inclusion rates in fruit-flavored beverage systems. As a result, the U.S. market is evolving into a diversified demand center where energy, industrial cleaning, and flavor applications collectively de-risk long-term adoption.

China: Biomass Utilization and Compliance-Driven Substitution

China’s ethyl levulinate trajectory is being driven by large-scale biomass valorization and tightening environmental compliance. In December 2025, leading chemical groups announced multi-billion-dollar investments in biomanufacturing platforms designed to convert cellulose-rich agricultural waste into levulinic acid derivatives. This strategic pivot aligns with national objectives to reduce petrochemical intensity while monetizing underutilized biomass streams. On the manufacturing front, producers such as Beijing LYS Chemicals have upgraded automation and purification systems to consistently achieve 99.9% food-grade ethyl levulinate, explicitly targeting premium fragrance and flavor markets in Europe and Japan.

Regulatory enforcement is reinforcing this shift. Stricter VOC emission caps in Jiangsu and other chemical zones are compelling coatings and industrial formulation players to substitute aromatic solvents like toluene with bio-esters. Ethyl levulinate’s solvency performance and biodegradability profile make it a natural compliance solution. As a result, China’s role is bifurcating into high-volume biomass conversion and high-purity export supply, strengthening its position across both cost-sensitive and premium segments.

Netherlands and Germany: Distribution Scale and Policy-Backed Adoption

Across the Netherlands and Germany, ethyl levulinate adoption is being accelerated through coordinated distribution and EU-level policy support. In 2025, BTC Europe expanded its distribution agreement with NXTLEVVEL Biochem, ensuring reliable access to levulinate solvents for downstream manufacturers ahead of the 2026 production cycle. This logistical maturity is critical as mid-sized formulators shift portfolios away from fossil solvents without building direct sourcing capabilities.

At the policy level, the European Commission’s updated Bioeconomy Strategy finalized in December 2025 provides explicit competitiveness incentives for industries adopting bio-solvents to meet the 55% emissions reduction target by 2030. Demand pull is further reinforced by fragrance and consumer goods majors. Givaudan has formally integrated ethyl levulinate into its sustainable sourcing framework, signaling long-term procurement intent.

Strategic Snapshot: Ethyl Levulinate Market by Country (2025–2026)

Ethyl Levulinate Market County Level Snapshot

|

Country / Region

|

Primary Growth Lever

|

Key End-Use Pull

|

Strategic Positioning

|

|

India

|

BioE3 policy and ethanol surplus

|

Food, agrochemicals, exports

|

Cost-competitive scale hub

|

|

Italy

|

Proprietary commercialization

|

Fragrance, home care

|

Technology and formulation leader

|

|

United States

|

DOE and EPA endorsement

|

Energy additives, solvents, flavors

|

Application-diversified demand center

|

|

China

|

Biomass valorization and VOC caps

|

Coatings, fragrance exports

|

Volume plus high-purity supplier

|

|

Netherlands & Germany

|

EU bioeconomy incentives

|

Consumer goods, fragrances

|

Distribution and policy accelerator

|

Ethyl Levulinate Market Report Scope

Ethyl Levulinate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.8 Million

|

|

Market Size (2034)

|

$20.9 Million

|

|

Market Growth Rate

|

3.9%

|

|

Segments

|

By Type (Food Grade, Industrial Grade, Technical Grade), By Application (Fragrances and Flavors, Solvents, Biofuel Additives, Pharmaceutical Intermediates, Agrochemicals, Plasticizers and Polymers), By Production Process (Esterification Process, Direct Chemical Synthesis, Biochemical Conversion)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

GFBiochemicals Ltd., BASF SE, Axxence Aromatic GmbH, Advanced Biotech Inc., Beijing LYS Chemicals Co., Ltd., Bedoukian Research, Inc., Berjé Inc., Fleurchem, Inc., Lluch Essence S.L., Indukern Ingredients, Elan Chemical Company, Inc., Synerzine, Inc., Alfa Aesar, M&U International LLC, Sino-High Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ethyl Levulinate Market Segmentation

By Type

- Food Grade

- Industrial Grade

- Technical Grade

By Application

- Fragrances and Flavors

- Solvents

- Biofuel Additives

- Pharmaceutical Intermediates

- Agrochemicals

- Plasticizers and Polymers

By Production Process

- Esterification Process

- Direct Chemical Synthesis

- Biochemical Conversion

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ethyl Levulinate Industry

- GFBiochemicals Ltd.

- BASF SE

- Axxence Aromatic GmbH

- Advanced Biotech Inc.

- Beijing LYS Chemicals Co., Ltd.

- Bedoukian Research, Inc.

- Berjé Inc.

- Fleurchem, Inc.

- Lluch Essence S.L.

- Indukern Ingredients

- Elan Chemical Company, Inc.

- Synerzine, Inc.

- Alfa Aesar

- M&U International LLC

- Sino-High Co., Ltd.

*- List not Exhaustive