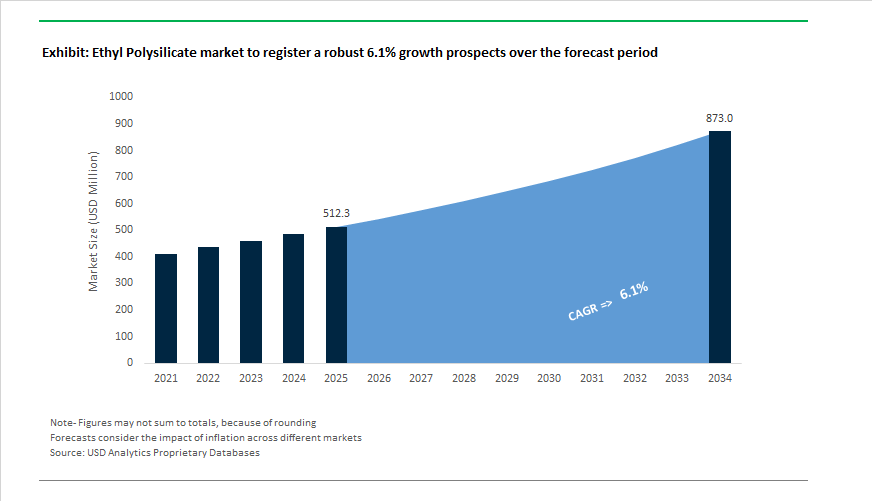

Ethyl Polysilicate Market to Reach $872.9 Million by 2034 at 6.1% CAGR Driven by Inorganic Coatings and Renewable Infrastructure Demand

The Ethyl Polysilicate Market is projected to expand from $512.3 Million in 2025 to $872.9 Million by 2034, reflecting a 6.1% CAGR. Growth is anchored in structural shifts toward inorganic binders, high-temperature casting systems, and renewable-energy material demand. Ethyl polysilicate (commonly Ethyl Silicate 40) functions as a silica precursor and inorganic binder, offering superior corrosion resistance, thermal stability, and low VOC emissions compared to organic resin systems. As environmental regulations tighten across Europe and North America, zinc-rich primers and heavy-duty industrial coatings are increasingly transitioning toward silicate-based chemistries, reinforcing medium-term demand stability through 2034.

In July 2024, Wacker Chemie AG announced an investment exceeding $200 million to expand operations at its Charleston, Tennessee site. Although centered on silicone specialties, the expansion directly strengthens North American capacity for high-purity silicates and ethyl polysilicate derivatives required in anti-corrosion coatings and industrial infrastructure rehabilitation. Earlier, Wacker introduced a high-resistance industrial-grade variant tailored for offshore oil & gas and maritime structures, where lifecycle extension and resistance to saltwater degradation are critical procurement factors. These developments align with the broader U.S. infrastructure modernization cycle and reshoring of specialty material production.

Performance momentum is also evident across Europe. In Q1 2024, Evonik Industries reported a 28% year-on-year increase in adjusted EBITDA within its Performance Materials division, attributing gains partly to robust uptake of Dynasylan® and SILBOND® 40 product lines. SILBOND® 40 (Ethyl Polysilicate 40) continues to gain adoption as a binder in investment casting and high-durability protective coatings. In October 2024, Evonik further introduced eco-friendly formulations that minimize hazardous hydrolysis byproducts, improving occupational safety profiles while maintaining adhesive strength and chemical resistance.

Regulatory pressure is accelerating substitution trends. In January 2026, the European Union implemented stricter VOC limits for industrial coatings, prompting coating manufacturers to convert zinc-rich primers from organic epoxies to ethyl polysilicate-based systems. These inorganic alternatives offer lower emission profiles and improved thermal tolerance, particularly valuable for steel structures, refineries, and renewable energy installations. Simultaneously, China’s Green Factory audits in 2024–2025 triggered consolidation, with top domestic producers—including Nangtong Chengua and Changzhou Wujin Hengye—now controlling more than 65% of regional output, signaling a quality-driven market rationalization.

Advanced manufacturing is adding new technical dimensions. In 2025–2026, chemical companies began integrating 3D-printed X3D® catalyst support architectures that rely on ethyl polysilicate as a high-purity silica network precursor. These structured supports improve flow distribution and reduce pressure drop in reactors used for hydrogen production and emission-control systems, reinforcing the material’s role in decarbonization infrastructure. Aerospace demand is also expanding: Momentive Performance Materials broadened its specialty silane and silicate portfolio in 2025, targeting ceramic shell systems for precision casting of jet engine components, where dimensional stability under extreme temperatures is mandatory.

Beyond coatings and casting, niche growth is emerging in renewable energy and optics. Asia-Pacific suppliers reported increasing use of ethyl polysilicate in solar-grade coatings and silicon-source applications as annual PV installations exceed 500 GW globally. Meanwhile, COLCOAT expanded optical-grade production in 2024, supplying anti-reflective and hard coatings for consumer electronics and eyewear—segments rebounding in East Asia.

Trends and Opportunities in the Ethyl Polysilicate Market

Accelerated Adoption in Low-VOC Inorganic Zinc-Rich Primers (IZRPs)

- Environmental compliance has become a binding specification rather than a design preference. As of January 17, 2025, finalized U.S. EPA amendments to national VOC emission standards tightened reactivity-based limits for aerosol and industrial coatings. This regulatory shift has directly accelerated the transition toward ethyl polysilicate-based binders in zinc-rich primers used for corrosion protection.

- Unlike organic epoxy binders, ethyl polysilicate grades such as 28 and 40 create an electrically conductive silicate matrix that enables true cathodic protection. In offshore and maritime environments classified as C5-M, these inorganic systems are now delivering service lives exceeding 25 years. Maintenance intervals are being extended by roughly 30% compared with conventional organic primers, materially lowering total lifecycle costs for ports, shipyards, and offshore energy assets.

- Product innovation is reinforcing this trend. In March 2024, Evonik Industries introduced an enhanced ethyl polysilicate grade optimized for controlled hydrolysis. Faster dry-to-handle times are improving coating line throughput in shipyards and fabrication yards, where downtime directly impacts global logistics efficiency. Material efficiency has also improved, with standardized grades such as Wacker Chemie AG WACKER® Silicate TES 28 delivering precisely 28.5 wt% SiO₂ upon hydrolysis. This precision minimizes sagging and settling when combined with high-density zinc dust, reducing waste during large infrastructure coating projects.

Integration into Sol-Gel Coatings for Advanced Surface Functionalization

- Sol-gel chemistry based on ethyl polysilicate precursors is transitioning from pilot-scale R&D into high-volume automotive, electronics, and architectural applications. These hybrid inorganic coatings offer molecular-level protection that conventional polymers cannot replicate.

- In the automotive sector, Dow introduced low-VOC, solvent-free sol-gel coating systems in 2024 that are now being adopted by Tier-1 suppliers. These coatings extend the service life of aluminum and polymer exterior components while providing functional properties such as anti-fingerprint and anti-reflective behavior for cockpit displays. This aligns with OEM sustainability mandates without compromising aesthetics or durability.

- Electronics and semiconductor packaging represent another fast-growing application. Technical bulletins issued between 2023 and 2025 by Saint-Gobain highlight the shift toward ethyl polysilicate-derived SiO₂ nanocoatings that provide superior moisture resistance and electrical insulation in compact, high-heat-density devices. Beyond electronics, architectural glass and facade systems are adopting self-cleaning SiO₂ layers derived from ethyl polysilicate. These coatings reduce reliance on chemical cleaners, supporting EU Paints Directive objectives to lower the environmental footprint of urban infrastructure.

High-Temperature Binders for Ceramic Fiber and Thermal Insulation

- Rising industrial operating temperatures in steel, glass, and advanced ceramics are exposing the limitations of organic and clay-based binders. Ethyl polysilicate offers a high-purity inorganic alternative capable of maintaining structural integrity at extreme temperatures.

- Industrial furnace manufacturers are increasingly specifying ethyl polysilicate-based composite binders that remain stable beyond 1,000°C, with certain formulations sustaining bonding strength up to 1,700°C. Systems such as Aremco Ceramabind™ series prevent the shrinkage and degradation commonly observed in traditional binders, extending refractory service life in continuous-duty kilns.

- From an energy perspective, the denser and more uniform binder matrix formed by ethyl polysilicate reduces thermal conductivity in refractory boards and shapes. Industrial operators report fuel consumption reductions in the range of 5 to 8% due to improved heat retention, translating directly into lower operating costs and emissions.

Formulation of Next-Generation Concrete Densifiers and Sealers

- The global shift toward polished concrete in commercial and industrial architecture is opening a substantial opportunity for ethyl polysilicate-based densifiers. Unlike topical acrylic sealers, these materials react chemically within the concrete matrix to form permanent insoluble silicate bonds.

- Industry reports from 2025 indicate that densifier-treated floors in modular and prefabricated construction achieve up to 30% higher surface hardness consistency than untreated floors. This allows faster commissioning of logistics hubs, warehouses, and data centers where construction timelines are tightly linked to revenue generation.

- From a sustainability standpoint, ethyl polysilicate sealers significantly reduce lifecycle maintenance requirements. Because the silicate bond does not peel or degrade, material usage over the asset life is reduced by approximately 32% compared with re-applied organic coatings. Dust-related particulate emissions are also lowered, supporting compliance with LEED and BREEAM green building standards.

- Adoption is being further accelerated by smart application methods. By late 2025, around 45% of large flooring contractors had deployed semi-automated or robotic systems for silicate densifier application. These systems improve coating uniformity by roughly 20% across industrial floor plates exceeding 50,000 square meters, reinforcing ethyl polysilicate’s position as a scalable, high-performance construction chemical.

Ethyl Polysilicate Market Share and Segmentation Insights

Ethyl Polysilicate 40 Leads Coatings Performance with High-Silica Binder Efficiency

Ethyl Polysilicate 40 accounts for 48% of total market share in 2025, driven by its dominant role in zinc-rich primers and heavy-duty protective coatings. With ~40% silica content, this grade delivers superior film formation, corrosion resistance, and long-term durability, making it the preferred binder for marine structures, bridges, pipelines, and industrial maintenance coatings. Ethyl Polysilicate 32 holds a substantial secondary share, particularly in precision casting, where its controlled hydrolysis rate supports consistent ceramic shell formation in investment casting. Ethyl Polysilicate 28 serves more reactive, lower-viscosity applications in specialty coatings and chemical intermediates. High-purity ethyl polysilicate represents a fast-growing premium segment, specified for electronics, optical coatings, and sol-gel processing, where ultra-low metal ion content and tight particle control are essential for semiconductor manufacturing and precision optical components.

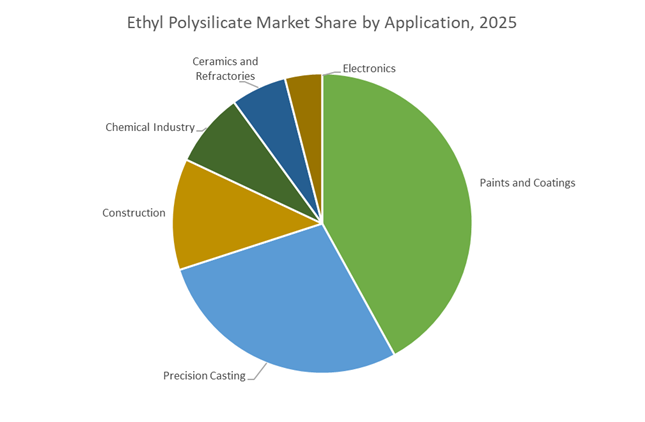

Paints and Coatings Drive Core Demand Supported by Precision Casting and Electronics Growth

Paints and coatings represent 42% of global ethyl polysilicate consumption in 2025, positioning this segment as the primary revenue driver. The material is extensively used as a silicate binder in zinc-rich primers, providing cathodic protection and barrier performance for steel infrastructure. Precision casting follows as a major application, leveraging ethyl polysilicate in ceramic shell slurries to produce high-accuracy molds for aerospace, automotive, and medical components. Construction applications utilize ethyl polysilicate as a consolidant and masonry sealer, enhancing durability of concrete and stone surfaces. Chemical industry demand remains steady through organosilicon synthesis and crosslinking applications. Ceramics and refractories occupy a niche position, while electronics is emerging rapidly as high-purity grades gain adoption in dielectric layers, planarization coatings, and advanced semiconductor fabrication.

Competitive Landscape of the Ethyl Polysilicate Market

The ethyl polysilicate market in 2026 is shaped by integrated silicone producers, sol-gel innovation, and rising demand from coatings, precision casting, electronics, and semiconductor manufacturing, with competition centered on purity control, APAC capacity expansion, and Product Carbon Footprint transparency.

Wacker Chemie AG leads low-VOC ethyl polysilicates with globally integrated silane production

Wacker Chemie AG remains a cornerstone supplier, leveraging fully integrated Verbund sites across Germany, the US, and China to ensure stable silane precursor availability for its ethyl polysilicate portfolio. The company reported preliminary 2025 group sales of €5.48 billion and is executing its 2026 PACE program to cut over €300 million annually in administrative and production costs. In early 2026, Wacker implemented price adjustments of up to 25% in response to sharply higher platinum and raw material costs. Its latest low-VOC ethyl polysilicate grades reduce emissions by ~15%, aligning with stringent EU architectural and industrial coatings regulations and reinforcing Wacker’s leadership in sustainable binder chemistry.

Evonik Industries AG scales high-purity ethyl polysilicates for APAC coatings and semiconductor sol-gel processes

Evonik Industries AG continues to expand aggressively in specialty silicates, commissioning a 20% capacity increase and a new Shanghai production facility during 2025 to 2026 to capture APAC growth. With reported 2024 sales of €15.2 billion, Evonik is prioritizing “Green Growth” through its TEGOSURF® and DYNASYLAN® platforms, targeting high-purity silica synthesis via sol-gel routes for semiconductor applications. A key differentiator is Evonik’s Product Carbon Footprint (PCF) disclosure for ethyl polysilicate batches, enabling customer ESG reporting. Its strategy focuses on reinforcing global production infrastructure while supplying advanced additives for electronics, industrial coatings, and next-generation functional surfaces.

Momentive Performance Materials Inc. dominates investment casting binders with high-silica ethyl polysilicate innovation

Momentive Performance Materials commands strong share in precision investment casting, supplying high-silica ethyl polysilicates such as Ethyl Silicate 40 for aerospace and defense components. In 2025/2026, the company allocated over 18% of its R&D budget to advanced sol-gel and high-purity polysilicate technologies. A late-2025 R&D collaboration accelerated development of hybrid organic-inorganic coatings delivering up to 2x corrosion resistance versus conventional zinc-rich primers. Momentive’s technical specialization in fast-curing, high-durability binders supports industrial sealing and metal protection markets, positioning it as a premium innovation partner for foundries and high-performance coating formulators.

Zhejiang Xinan Chemical anchors APAC supply with cost-advantaged bulk ethyl polysilicates and TEOS upgrades

Zhejiang Xinan Chemical, part of Wynca Group, is a major APAC producer holding a mid-teens share of global ethyl polysilicate capacity, serving a region that accounts for nearly 40% of worldwide consumption in 2026. Its full phosphorus-silicon backward integration into silicon metal and intermediates provides structural cost leadership in the merchant market. The company specializes in Ethyl Silicate 28 and 32 for construction and marine coatings, while upgrading refining assets to enter electronic-grade TEOS for semiconductors and optical fiber. This dual strategy of volume leadership and electronics-grade expansion underpins Wynca’s rapid regional market penetration.

COLCOAT CO., LTD. advances anti-static and optical coatings with precision ethyl polysilicate systems

COLCOAT is the high-precision specialist supplying functional ethyl polysilicate solutions for electronics, optical coatings, and precision casting across Japan and South Korea. Its portfolio includes anti-static coating agents and hydrolyzed silicates critical for IC tubes, trays, and glass substrates. In early 2026, COLCOAT launched a hydrophilic anti-glare hybrid coating using ethyl polysilicate to deliver self-cleaning solar panels and architectural glass. With multi-purpose plants in Japan and Malaysia, the company supports Southeast Asia’s electronics supply chain while maintaining leadership in optical and casting applications where surface performance, purity, and consistency are non-negotiable.

China: Semiconductor Self-Sufficiency and AI-Led Process Intensification

China remains the most structurally aggressive market for ethyl polysilicate, with growth shaped by coordinated industrial policy, semiconductor localization, and digitalized manufacturing mandates. The September 2025 Work Plan released by the Ministry of Industry and Information Technology sets a clear direction for upgrading the chemical sector toward high-end fine chemicals. Advanced silicate binders, including ethyl polysilicate grades used in electronics and emerging low-altitude economy applications, are explicitly prioritized. This policy alignment is accelerating R&D spending and fast-tracking capacity approvals in Jiangsu and Zhejiang, where specialty silicate clusters already benefit from proximity to electronics manufacturing ecosystems.

Operational efficiency is being reshaped through the national AI + Petrochemical initiative. Producers are deploying AI-based process control systems to optimize hydrolysis and condensation stages, delivering estimated reductions of 12% in VOC emissions and energy consumption by 2026. On the demand side, China’s push for 7nm and 5nm semiconductor self-sufficiency has materially lifted requirements for high-purity ethyl polysilicate used in insulating layers and lithography-related applications. Regional suppliers such as Yajie Chemical expanded semiconductor-grade lines in late 2025 to meet these specifications. Supply stability is further reinforced by the integrated ethylene-to-silicate value chain at the SINOPEC-BASF Zhanjiang Verbund site, which is entering full downstream throughput in early 2026, reducing exposure to raw material price volatility.

India: Infrastructure-Led Demand and Export Normalization

India’s ethyl polysilicate market is evolving around infrastructure expansion, domestic substitution, and export readiness rather than pure volume growth. The July 2025 launch of eight high-potential chemical clusters under NITI Aayog marks a structural shift toward higher-value derivatives. These hubs offer shared utilities and viability gap funding, lowering entry barriers for ethyl polysilicate 40 and related cross-linking agents. This policy framework is closely aligned with Aatmanirbhar Bharat objectives, under which domestic procurement of silica-based binders rose sharply in Q3 2025, particularly for weather-resistant coatings used in airports, highways, and urban infrastructure.

Application-side innovation is most visible in marine and heavy-duty coatings. Indian paint majors, including Asian Paints, have increased the incorporation of ethyl polysilicate in marine-grade anti-corrosive systems to meet durability standards associated with naval expansion and port modernization. Parallel to domestic uptake, Indian suppliers have standardized REACH-compliant technical dossiers, including impurity profiles and lifecycle data. This compliance-driven professionalism enabled a measurable increase in exports of silicate cross-linkers to European automotive and industrial coating customers in late 2025, repositioning India as a credible secondary supply base rather than a purely domestic market.

United States: Protective Coatings and Electrification Pull

In the United States, ethyl polysilicate demand is increasingly anchored in asset rehabilitation and electrification rather than traditional foundry uses. In March 2024, Evonik Industries launched an enhanced ethyl polysilicate grade tailored for high-performance protective coatings. By late 2025, this material achieved broad commercial penetration across energy infrastructure and bridge rehabilitation projects, where long-term corrosion resistance and inorganic binder stability are critical performance criteria.

A second growth vector is emerging from electric mobility. U.S. chemical formulators are adapting ethyl polysilicate for dielectric and thermal barrier coatings used in EV battery housings, a transition supported by U.S. Department of Energy grants for sustainable materials innovation awarded in early 2025. Regulatory continuity also supports diversification into life sciences. The U.S. Food and Drug Administration reaffirmed the safety status of specific silicate-based excipients in 2025, sustaining demand for pharmaceutical-grade ethyl polysilicate in oral and topical drug delivery systems through the 2026 fiscal cycle.

Germany: Decarbonization and Regulatory Precision

Germany’s ethyl polysilicate landscape is being reshaped by decarbonization mandates and regulatory stringency rather than capacity expansion. Leading producers such as Wacker Chemie AG and Evonik Industries are executing asset transformation strategies centered on green chemistry milestones. By 2026, production lines are transitioning toward bio-attributed ethanol feedstocks, targeting a 20% reduction in product-level carbon footprint relative to 2023 baselines.

Compliance requirements under the 2026 REACH Recast are equally influential. German manufacturers are implementing real-time impurity tracking and digital batch certification systems to meet ultra-strict safety thresholds for silicate binders used in consumer-facing adhesives and coatings. This emphasis on traceability and purity positions Germany as a benchmark market for regulatory-grade ethyl polysilicate, even as overall European volumes remain structurally constrained by energy costs.

Brazil: Downstream Optionality from Ethylene Investments

Brazil represents an emerging, optional-growth geography for ethyl polysilicate, driven by upstream petrochemical investments rather than immediate end-use pull. In late 2025, Braskem announced a R$4.2 billion expansion at its Rio de Janeiro complex. While primarily focused on ethylene, the project includes specialized downstream ester units scheduled to reach operational readiness by mid-2026. This infrastructure creates optionality for localized ethyl polysilicate and related ester production, particularly for coatings and construction chemicals serving Latin American markets.

Strategic Snapshot: Ethyl Polysilicate Market by Country (2025–2026)

Ethyl Polysilicate Market County Level Snapshot

|

Country

|

Primary Growth Driver

|

Key Application Focus

|

Strategic Role

|

|

China

|

Semiconductor localization and AI manufacturing

|

Electronics, insulating layers

|

Integrated scale and cost leadership

|

|

India

|

Infrastructure build-out and export compliance

|

Coatings, marine, automotive

|

Domestic substitution and export base

|

|

United States

|

Asset rehabilitation and EV materials

|

Protective and dielectric coatings

|

Application-driven diversification

|

|

Germany

|

Decarbonization and REACH compliance

|

Adhesives, specialty coatings

|

Regulatory and quality benchmark

|

|

Brazil

|

Ethylene-led downstream optionality

|

Construction and industrial coatings

|

Emerging regional supply option

|

Ethyl Polysilicate Market Report Scope

Ethyl Polysilicate market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$512.3 Million

|

|

Market Size (2034)

|

$872.9 Million

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Product Grade (Ethyl Polysilicate 28, Ethyl Polysilicate 32, Ethyl Polysilicate 40, High-Purity Grade), By Application (Paints and Coatings, Precision Casting, Chemical Industry, Electronics, Construction, Ceramics and Refractories), By Function (Binding Agent, Cross-Linking Agent, Intermediate, Surface Modifier)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Wacker Chemie AG, Evonik Industries AG, Momentive Performance Materials Inc., Huntsman Corporation, Shin-Etsu Chemical Co., Ltd., Dow Inc., BASF SE, Hebei Chengxin Co., Ltd., YAJIE Chemical, Zhangjiagang LongTai Chemical, COLCOAT Co., Ltd., Nantong Chenguang Chemical, INEOS Oligomers, Adeka Corporation, Gelest, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ethyl Polysilicate Market Segmentation

By Product Grade

- Ethyl Polysilicate 28

- Ethyl Polysilicate 32

- Ethyl Polysilicate 40

- High-Purity Grade

By Application

- Paints and Coatings

- Precision Casting

- Chemical Industry

- Electronics

- Construction

- Ceramics and Refractories

By Function

- Binding Agent

- Cross-Linking Agent

- Intermediate

- Surface Modifier

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ethyl Polysilicate Industry

- Wacker Chemie AG

- Evonik Industries AG

- Momentive Performance Materials Inc.

- Huntsman Corporation

- Shin-Etsu Chemical Co., Ltd.

- Dow Inc.

- BASF SE

- Hebei Chengxin Co., Ltd.

- YAJIE Chemical

- Zhangjiagang LongTai Chemical

- COLCOAT Co., Ltd.

- Nantong Chenguang Chemical

- INEOS Oligomers

- Adeka Corporation

- Gelest, Inc.

*- List not Exhaustive