Ethylbenzene Market to Reach $28 Billion by 2034 at 3.4% CAGR Amid Styrene Chain Optimization and Regional Capacity Shifts

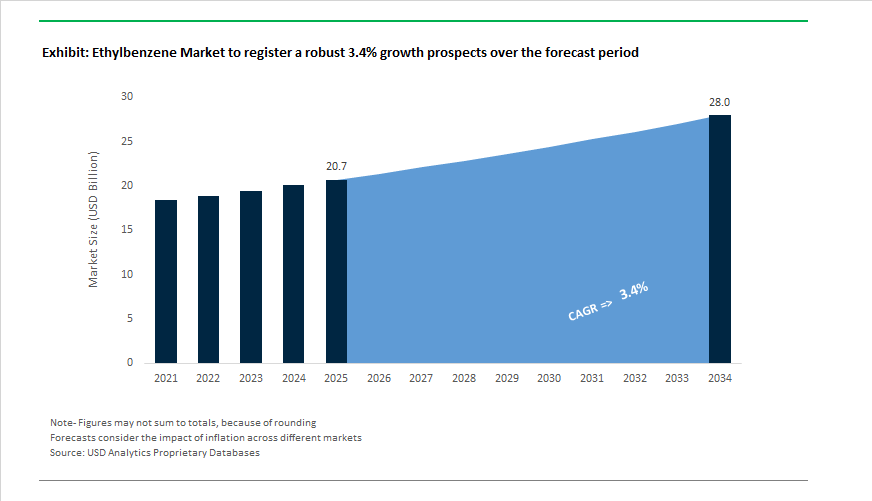

The Ethylbenzene Market is projected to expand from $20.7 billion in 2025 to $28 billion by 2034, reflecting a moderate 3.4% CAGR. Growth remains structurally tied to downstream styrene monomer (SM) demand, particularly in polystyrene, ABS resins, and styrene-butadiene rubber (SBR) applications across packaging, automotive, appliances, and construction. While global consumption growth is steady rather than aggressive, strategic capacity realignments, technological upgrades, and circular feedstock integration are reshaping competitive positioning across regions.

In May 2024, SIBUR announced a major expansion at its Nizhnekamskneftekhim complex, adding 350,000 tons/year of ethylbenzene capacity alongside new styrene and polystyrene units, with commissioning targeted for 2028. This vertically integrated investment is expected to reinforce Russia’s self-sufficiency in the ethylbenzene–styrene value chain and increase export competitiveness in Eurasian markets. Concurrently, Middle Eastern producers added approximately 2.1 million metric tons of combined ethylbenzene and styrene capacity between 2022 and late 2024, leveraging advantaged feedstock economics and proximity to Asia to enhance global supply share.

By contrast, North America experienced structural contraction. In October 2024, INEOS Styrolution confirmed the permanent closure of its Sarnia, Ontario styrene monomer facility following regulatory scrutiny over benzene emissions. Decommissioning is expected to conclude by late 2025, marking a significant reduction in regional ethylbenzene-styrene integration. This reflects a broader rationalization trend in higher-cost jurisdictions facing environmental compliance pressures and aging infrastructure.

Technological evolution is also redefining production economics. Industrial data from 2024 indicates that 43% of global ethylbenzene production now utilizes zeolite gas-phase catalytic systems, overtaking traditional aluminum chloride (AlCl₃) processes. Zeolite technology delivers up to 97% conversion efficiency and reduces waste generation by approximately 16%, improving operational sustainability metrics and lowering downstream purification costs. As emission standards tighten globally, this catalytic shift is expected to accelerate, particularly in Asia-Pacific.

Circularity initiatives are gaining traction within the styrene ecosystem. In September 2025, INEOS Styrolution received its first commercial-scale delivery of recycled styrene monomer at its Antwerp site, supplied via chemical depolymerization. This development introduces a partially decoupled pathway from fossil-derived ethylbenzene feedstock, particularly for food-grade and medical packaging applications. Although still limited in scale, such initiatives indicate emerging competitive pressure from advanced recycling technologies.

Corporate restructuring is influencing capital allocation. In January 2026, LyondellBasell reported $153 million in site closure costs under its cash optimization strategy, reflecting portfolio rationalization within its aromatic and derivative chain. Similarly, BASF SE disclosed elevated restructuring charges as it modernizes legacy chemical assets to align with decarbonization objectives. These moves signal a gradual shift toward cost-advantaged, energy-efficient complexes.

Asia remains the production anchor. By 2024, China, the U.S., and South Korea collectively accounted for more than 19 million metric tons of ethylbenzene output, with Chinese producers increasingly operating integrated ethylbenzene–styrene units that reduce operating costs by roughly 9%. Integration allows tighter feedstock management, improved energy utilization, and margin resilience in volatile benzene markets.

Trends and Opportunities in the Ethylbenzene Market

Aggressive Capacity Expansion in Asia Driven by Engineering Thermoplastics

- Ethylbenzene capacity growth is increasingly tied to engineering thermoplastics rather than commodity plastics. Asia, particularly China, is leading this expansion to support durable applications such as electronics housings, automotive interiors, and appliance components.

- By late 2025, China had confirmed plans to add approximately 3.05 million tonnes per annum of new Acrylonitrile Butadiene Styrene capacity by 2030. Projects nearing completion include the Jilin Petrochemical Company ABS Plant 5 and the Sinochem Quanzhou Petrochemical ABS complex, each contributing roughly 0.60 mtpa of incremental ABS output. These projects directly translate into higher captive demand for ethylbenzene through styrene monomer integration.

- This expansion is aligned with a national push for self-sufficiency. According to late-2025 industry tracking, China’s growing domestic styrenics base is reducing import dependence, forcing global ethylbenzene producers to pivot toward higher-margin grades of High Impact Polystyrene for high-temperature electronics and automotive interiors. These applications remain resilient even as broader commodity polymer demand softens.

- In India, downstream pull is also strengthening. The Supreme Petrochem expansion in Maharashtra, scheduled for commissioning by 2026, is targeting appliance shells and consumer electronics enclosures. These segments rely on styrene-based resins with tight dimensional stability requirements, reinforcing ethylbenzene’s role in durable goods manufacturing across South Asia.

Benzene Feedstock Volatility and the Shift Toward Circular Sourcing

- Feedstock economics are emerging as a critical strategic variable for ethylbenzene producers. Volatility in upstream benzene pricing is compressing margins and accelerating the adoption of alternative sourcing models.

- During Q3 2025, ethylbenzene prices corrected downward in key hubs, with declines of approximately 11.96% in Houston and 16.40% in Belgium. These movements closely tracked benzene price fluctuations, highlighting the sensitivity of ethylbenzene economics to aromatics markets. As a result, producers are increasingly shifting toward flexible pricing formulas and long-term supply agreements.

- A notable structural response is the move toward circular benzene. In a long-term agreement initiated in mid-2024 and scaled through 2025, BASF partnered with Encina to source chemically recycled benzene derived from post-consumer plastics. This circular feedstock enables mass-balanced ethylbenzene and styrene production, allowing suppliers to serve premium automotive and electronics brands seeking lower Scope 3 emissions exposure.

- Regulatory signals are reinforcing this shift. In March 2025, India’s Directorate General of Trade Remedies recommended anti-dumping duties on Linear Alkyl Benzene, indicating a broader policy trend toward safeguarding domestic aromatics value chains. These measures are indirectly shaping ethylbenzene competitiveness by influencing regional benzene availability and cost structures.

High-Value Demand from Medical and Automotive TPEs Based on SEBS

- Ethylbenzene-derived styrene is increasingly finding high-margin applications in Styrene-Ethylene/Butylene-Styrene block copolymers, which are replacing PVC and natural rubber in sensitive and performance-critical uses.

- By December 2025, Styrenic Block Copolymers held the largest share of the medical-grade thermoplastic elastomers market. SEBS materials are particularly valued in medical tubing, catheters, and fluid handling systems due to their biocompatibility, sterilization resistance, and absence of plasticizers. Industry benchmarks indicate that SEBS compounds achieve 90 to 95% compliance with stringent biocompatibility standards, making them a preferred choice for single-use medical devices.

- Automotive lightweighting is reinforcing this demand. In 2025, more than 40% of automotive manufacturers reported replacing conventional rubber components with TPEs to reduce vehicle mass and improve energy efficiency. This transition is especially critical for electric vehicles, where weight reduction directly translates into extended driving range. Ethylbenzene demand is therefore increasingly linked to durable elastomer consumption rather than cyclical packaging markets.

- In parallel, demand for soft-touch, non-latex materials in premium automotive interiors and consumer electronics has driven a reported 25% increase in the use of styrene-based elastomers. This niche provides a margin-accretive outlet that helps offset declines in traditional polystyrene packaging.

Ethylbenzene as a Strategic Intermediate in Sustainable Aviation Fuel Pathways

- A transformative opportunity is emerging for ethylbenzene beyond polymers, positioning it as a strategic hydrocarbon intermediate in Alcohol-to-Jet pathways for Sustainable Aviation Fuel.

- In November 2025, LanzaJet achieved full commercial operation at its Freedom Pines Fuels facility, the world’s first plant converting ethanol into jet fuel at scale. In these pathways, ethylbenzene plays a role in supplying the aromatic content required to meet ASTM D7566 specifications, which mandate controlled aromatic levels for aircraft seal compatibility.

- Policy mandates are accelerating adoption. The United Kingdom’s SAF mandate took effect on January 1, 2025, while India announced a 1% SAF blending target by 2027 in September 2025. These regulations are forcing refiners to explore co-processing of ethylbenzene-rich streams, effectively repositioning ethylbenzene as a fuel-grade intermediate rather than solely a chemical monomer.

- Decarbonization metrics reinforce the opportunity. Research published in 2025 in the SAE International Journal of Sustainable Transportation indicates that ethanol-to-jet pathways can reduce aviation carbon intensity by up to 84 to 90% compared with conventional kerosene. This positions ethylbenzene-linked SAF routes as one of the fastest scalable options for aviation decarbonization, creating a structurally new demand vector for the ethylbenzene market.

Ethylbenzene Market Share and Segmentation Insights

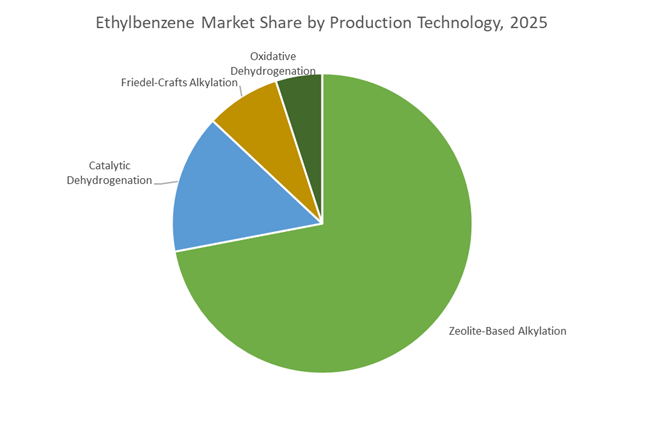

Zeolite-Based Alkylation Dominates Production with Lower Emissions and Higher Selectivity

Zeolite-based alkylation commands 72% of ethylbenzene production capacity in 2025, reflecting its status as the industry-standard technology for reacting benzene with ethylene. Solid zeolite catalysts deliver high selectivity, reduced corrosion, elimination of liquid acid waste, and improved energy efficiency, driving widespread adoption across modern petrochemical complexes. Legacy Friedel–Crafts alkylation continues to decline due to aluminum chloride waste handling and operational challenges, persisting mainly in older facilities. Catalytic dehydrogenation appears in integrated sites where ethylbenzene production is directly linked to styrene units, while oxidative dehydrogenation remains an emerging pathway aimed at improving energy efficiency in styrene conversion. Overall, sustainability mandates and operating cost optimization continue to accelerate migration toward zeolite-based ethylbenzene production technologies.

Styrene Monomer Manufacturing Absorbs the Vast Majority of Ethylbenzene Output

Styrene monomer production accounts for 92% of global ethylbenzene consumption in 2025, underscoring ethylbenzene’s strategic role as the primary feedstock for styrene value chains. Ethylbenzene is dehydrogenated to styrene, which is subsequently polymerized into polystyrene, ABS, styrene-butadiene rubber, and unsaturated polyester resins used across packaging, construction, consumer goods, and automotive components. Chemical intermediates form a small but important segment, supplying acetophenone, ethylanthraquinone, and specialty derivatives. Solvent usage has declined under environmental regulations, while gasoline blending continues to shrink as aromatics limits tighten and ethylbenzene’s value in styrene production outweighs fuel applications. This concentration of demand tightly links ethylbenzene market dynamics to global styrenics capacity expansions and downstream plastics consumption trends.

Competitive Landscape of the Ethylbenzene Market

The global ethylbenzene market in 2026 is shaped by vertically integrated styrenics giants, low-cost feedstock leaders, and technology licensors driving efficiency, with competition centered on EB/SM integration, APAC capacity expansion, circular polymers, and energy-optimized production.

LyondellBasell Industries strengthens EB/SM integration to power circular styrenics growth

LyondellBasell Industries remains a dominant force in high-purity ethylbenzene through its fully integrated EB/SM production platform, supplying downstream polystyrene and specialty copolymers. In late 2024, the company deepened its Asia strategy via a major joint venture with Sinopec under Ningbo ZRCC LyondellBasell New Material, establishing a large-scale EB/SM complex for the APAC market. Its strategic focus on circular and low-carbon solutions targets at least 2 million metric tons of recycled and renewable polymers annually by 2030, directly reshaping ethylbenzene sourcing. With unmatched vertical integration from monomers to advanced plastics, LyondellBasell mitigates raw material volatility while serving automotive, electronics, and packaging demand.

Chevron Phillips Chemical Company leverages shale feedstocks for low-cost aromatics production

Chevron Phillips Chemical Company is a key aromatics producer, manufacturing ethylbenzene via benzene alkylation with ethylene for internal styrene use and gasoline blending. During 2025 to 2026, the company accelerated operational excellence by deploying digital twin technology across its US Gulf Coast assets, optimizing energy-intensive aromatic distillation. Its deep integration with refining operations enables flexible production using reformate streams, allowing rapid margin-driven volume shifts. A core competitive advantage is feedstock economics: by maximizing North American shale gas derivatives, Chevron Phillips consistently ranks among the lowest-cost ethylbenzene producers globally, reinforcing its position in the merchant styrenics and fuels value chain.

INEOS Group advances circular styrenics while optimizing European ethylbenzene assets

INEOS, through its styrenics platform, operates one of the world’s most flexible ethylbenzene and styrene asset bases, with a strong European footprint in 2026. The company continues to pioneer depolymerization technologies, converting polystyrene waste back into styrene, a circular innovation that gradually moderates long-term virgin ethylbenzene demand. In early 2026, INEOS prioritized asset resilience, optimizing heat integration across alkylation units to offset elevated European energy costs. Nearly all of its ethylbenzene feeds ABS and polystyrene production, supporting surging automotive and electronics applications where lightweight plastics and high-impact materials remain critical growth drivers.

Sinopec anchors APAC ethylbenzene supply with mega-complex integration

Sinopec stands as Asia’s aromatics powerhouse and the largest ethylbenzene producer across the APAC region, which commands roughly 35.9% of global market share in 2026. Continuous investment in integrated petrochemical complexes, including the Ningbo project, links ethylbenzene with advanced styrene and propylene oxide units to serve China’s manufacturing engine. In 2025, Sinopec achieved process intensification breakthroughs, cutting steam consumption in EB-to-styrene dehydrogenation by over 10%. Backed by government alignment and massive scale, Sinopec benefits from policy-driven innovation and supply chain self-sufficiency, reinforcing its leadership in regional styrenics.

Honeywell International Inc. powers over half of global ethylbenzene capacity through EBMax technology

Honeywell, via Honeywell UOP, acts as the market’s critical technology enabler, licensing EBMax™ zeolite catalyst systems that deliver high-purity ethylbenzene with minimal byproducts. As of 2026, more than half of worldwide ethylbenzene output relies on Honeywell UOP technology, giving the company unmatched visibility into global capacity trends. In late 2025, Honeywell introduced a next-generation EBMax catalyst operating at lower temperatures, significantly reducing synthesis carbon intensity. Its “Technology-as-a-Service” strategy now integrates digital performance monitoring, providing real-time optimization to maximize yield and catalyst life for producers across North America, Europe, and Asia.

China: Smart Verbund Enforcement and Styrenics-Led Self-Sufficiency

China’s ethylbenzene market is being reshaped through state-directed capacity rationalization combined with aggressive downstream styrenics expansion. In October 2025, a multi-ministerial petrochemical restructuring mandate led by the Ministry of Industry and Information Technology set a clear objective to lift petrochemical value-added growth above 5% while eliminating structurally inefficient assets. Under this framework, legacy ethylbenzene units are being phased out in favor of high-efficiency Smart Verbund complexes that integrate refining, aromatics, and polymer intermediates. This policy-driven consolidation is intended to mitigate regional oversupply while improving energy efficiency and emission control across coastal chemical clusters.

Downstream demand strength is anchored in styrenics. By late 2025, China commissioned more than 2 million tons of new ethylbenzene-to-styrene capacity, including major units at Jingbo Sida Rui and Jilin Petrochemical. This expansion directly supports a sharp rise in ABS output, which grew over 27% year on year during the first ten months of 2025, reinforcing ethylbenzene’s role as a critical feedstock. Full-chain integration is further exemplified by the Yantai Yulong Petrochemical complex, where a 500,000 tpa ethylbenzene unit operates within a refinery-to-polymer configuration. As a result of these coordinated investments, China transitioned into a net exporter of styrene monomer by Q4 2025, materially reducing its historical dependence on imported ethylbenzene derivatives.

India: Refinery Integration and Import Substitution Momentum

India’s ethylbenzene landscape is defined less by volume expansion and more by strategic import substitution supported by new refinery assets. The integrated completion of the HPCL Rajasthan Refinery in early 2025 marks a structural inflection point. Designed to generate large volumes of benzene and ethylbenzene, the complex is expected to cut India’s reliance on imported aromatics by up to one-fifth by 2026. This shift enhances domestic feedstock security for downstream styrene, coatings, and pharmaceutical intermediates, particularly as consumption scales with automotive and packaging growth.

Complementing this upstream push, targeted investments across the aromatics chain are tightening regional supply-demand balances. Tamilnadu Petroproducts’ announced expansion of linear alkyl benzene and caustic soda capacity is stabilizing benzene availability, indirectly supporting ethylbenzene economics. At the same time, India is finalizing a new styrene facility with capacity approaching 387,000 tonnes, scheduled to ramp through the 2026–2027 cycle. Policy support under the BioE3 framework is also catalyzing early-stage research into bio-based ethylbenzene pathways, positioning India as a future innovation hub rather than a purely derivative consumer.

United States: Operating Rate Compression and Gasoline Pool Resilience

The U.S. ethylbenzene market is navigating structural pressure from volatile trade dynamics and subdued downstream construction activity. In mid-2025, sharp fluctuations in benzene export pricing out of the Gulf Coast disrupted feedstock economics, prompting producers to reassess export-oriented strategies. As a result, North American ethylbenzene-to-styrene monomer operating rates are projected to remain constrained into 2026, reflecting high input costs and weaker housing-driven demand for styrenic resins.

Despite these headwinds, ethylbenzene continues to demonstrate resilience through its role as a high-octane aromatic blendstock. In late 2025, steady gasoline blending demand helped offset softness in derivative exports, particularly for export-grade fuel pools. However, structural rationalization is underway. The closure of Ineos Styrolution’s ABS plant in Ohio underscores the broader recalibration of U.S. styrenics capacity, driven by capital intensity, regulatory compliance costs, and competitive pressure from Asia and the Middle East.

Saudi Arabia: Vision 2030 Scale and Carbon-Integrated Expansion

Saudi Arabia is reinforcing its position as a low-cost, globally competitive ethylbenzene producer through mega-scale petrochemical integration. Vision 2030 approvals granted in 2025 for the Sipchem–LyondellBasell joint project in Jubail provide upstream support via a mixed-feed cracker capable of generating substantial ethylene volumes, strengthening the aromatics and ethylbenzene value chain. Parallel to this, the Amiral complex developed by Saudi Aramco and TotalEnergies reached key construction milestones, laying the groundwork for one of the region’s most integrated petrochemical platforms post-2027.

A defining differentiator is sustainability integration. SABIC’s operation of a large-scale carbon capture facility is being embedded into ethylbenzene-linked production chains. This alignment with low-carbon petrochemical standards enhances the export competitiveness of Saudi-derived ethylbenzene and styrenics as global buyers increasingly factor emissions intensity into procurement decisions.

South Korea: Capacity Discipline and Regional Expansion

South Korea’s ethylbenzene strategy reflects a dual-track approach of overseas expansion and domestic capacity discipline. The inauguration of the Lotte Chemical Indonesia complex in November 2025 provides Korean-led access to Southeast Asia’s growing aromatics market, with significant benzene and toluene output feeding regional ethylbenzene demand. This outward investment offsets domestic market saturation while strengthening South Korea’s influence across ASEAN petrochemical supply chains.

Domestically, government-led restructuring agreements finalized in late 2025 mandate substantial reductions in naphtha cracking capacity to address chronic oversupply. This contraction is forcing producers to pivot away from commodity volumes toward higher-value ethylbenzene derivatives and specialty applications. The resulting shift prioritizes margin stability and technological differentiation over scale, aligning South Korea’s ethylbenzene sector with a more sustainable long-term operating model.

Strategic Snapshot: Ethylbenzene Market Dynamics by Country (2025–2026)

Ethylbenzene Market County Level Snapshot

|

Country

|

Structural Driver

|

Value Chain Focus

|

Strategic Position

|

|

China

|

Capacity rationalization and styrenics expansion

|

Integrated ethylbenzene to ABS

|

Global production and export hub

|

|

India

|

Refinery integration and import substitution

|

Benzene and styrene feedstocks

|

Emerging self-reliant market

|

|

United States

|

Trade volatility and demand softness

|

Gasoline blending and derivatives

|

Mature market under rationalization

|

|

Saudi Arabia

|

Mega-scale integration and carbon capture

|

Cracker-linked aromatics

|

Low-cost global supplier

|

|

South Korea

|

Capacity discipline and ASEAN expansion

|

High-value derivatives

|

Margin-focused regional player

|

Ethylbenzene Market Report Scope

Ethylbenzene Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$20.7 Billion

|

|

Market Size (2034)

|

$28 Billion

|

|

Market Growth Rate

|

3.4%

|

|

Segments

|

By Production Technology (Catalytic Dehydrogenation, Zeolite-Based Alkylation, Friedel-Crafts Alkylation, Oxidative Dehydrogenation), By Purity Grade (High Purity Grade, Industrial Grade, Reagent Grade), By Application (Styrene Monomer Production, Gasoline Blending, Solvents and Intermediates, Chemical Intermediates), By End-Use Industry (Packaging and Consumer Goods, Automotive and Transportation, Building and Construction, Agriculture, Electronics and Electrical Appliances)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

China Petroleum & Chemical Corporation, LyondellBasell Industries N.V., ExxonMobil Corporation, SABIC, BASF SE, INEOS Group, Reliance Industries Limited, TotalEnergies SE, Chevron Phillips Chemical Company, Lotte Chemical Corporation, Wanhua Chemical Group, Shell plc, Hengli Petrochemical, LG Chem, Formosa Plastics Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ethylbenzene Market Segmentation

By Production Technology

- Catalytic Dehydrogenation

- Zeolite-Based Alkylation

- Friedel-Crafts Alkylation

- Oxidative Dehydrogenation

By Purity Grade

- High Purity Grade

- Industrial Grade

- Reagent Grade

By Application

- Styrene Monomer Production

- Gasoline Blending

- Solvents and Intermediates

- Chemical Intermediates

By End-Use Industry

- Packaging and Consumer Goods

- Automotive and Transportation

- Building and Construction

- Agriculture

- Electronics and Electrical Appliances

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ethylbenzene Industry

- China Petroleum & Chemical Corporation

- LyondellBasell Industries N.V.

- ExxonMobil Corporation

- SABIC

- BASF SE

- INEOS Group

- Reliance Industries Limited

- TotalEnergies SE

- Chevron Phillips Chemical Company

- Lotte Chemical Corporation

- Wanhua Chemical Group

- Shell plc

- Hengli Petrochemical

- LG Chem

- Formosa Plastics Corporation

*- List not Exhaustive