Ethylene BIS Stearamide (EBS) Market Advancing on Bio-Based Additives and Polymer Processing Optimization

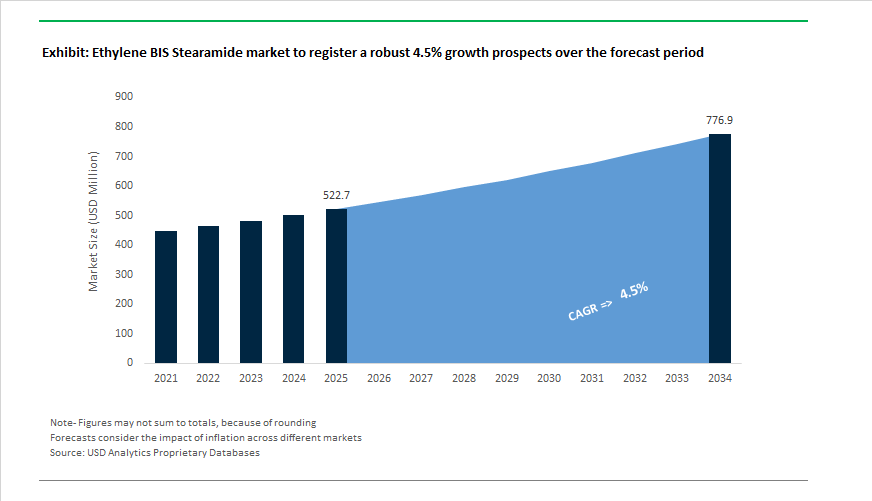

The Ethylene Bis Stearamide (EBS) Market is projected to grow from $522.7 Million in 2025 to $776.8 Million by 2034, reflecting a CAGR of 4.5%. Growth is being driven by increasing demand for high-performance polymer processing aids, slip agents, anti-block additives, and mold release lubricants across engineering plastics, masterbatches, rubber, and powder metallurgy applications. EBS continues to play a critical functional role in improving surface finish, reducing friction, enhancing dispersion of pigments, and optimizing cycle times in injection molding and extrusion processes. Market dynamics through 2024–2026 show a decisive shift toward sustainable feedstocks, PFAS-free formulations, and regionally diversified supply chains.

In June 2024, PMC Biogenix announced a 50% capacity expansion at its Armoslip facility in Gyeongju, South Korea. The investment strengthens supply of high-purity EBS grades used as friction reducers and processing lubricants in polyolefins and engineering resins. With commissioning targeted for mid-2026, the expansion addresses rising demand from Asia’s automotive and electronics manufacturing clusters, where surface quality and dimensional precision are non-negotiable.

Sustainability compliance is becoming a structural competitive differentiator. Clariant confirmed completion of its transition to a 100% PFAS-free additive portfolio as of late 2023, positioning its waxes and EBS-related products as compliant alternatives ahead of stringent 2026 regulatory deadlines. The elimination of per- and polyfluoroalkyl substances from additive systems directly benefits polymer converters seeking low-risk formulations for European and North American markets. In Q3 2025, Clariant also reported margin expansion within its Adsorbents & Additives segment, supported by strong pricing power in sustainable additive lines.

Portfolio focus among specialty producers is sharpening. Valtris Specialty Chemicals finalized the divestiture of its Champlor Renewables business in February 2026, reallocating capital toward its core polymer additives portfolio, including high-performance EBS waxes. Earlier, in April 2024, Valtris expanded its partnership with China’s Transfar Group to accelerate sustainable polymer solutions in Asia, reinforcing EBS’s role in high-growth masterbatch and PVC stabilization systems.

Bio-based chemistry integration is accelerating across the amide value chain. Emery Oleochemicals highlighted its Green Polymer Additives portfolio at Fakuma 2024, emphasizing USDA-certified bio-based derivatives essential for EBS synthesis. The company’s 2024 Sustainability Report, released in December 2025, confirmed ISO 50001 certification and ongoing decarbonization of fatty acid and amide production lines. This transition aligns with OEM and brand-owner mandates for lower Scope 3 emissions in plastics used in consumer electronics, appliances, and automotive interiors.

Upstream integration is also influencing long-term cost structures. In August 2025, Kao Corporation inaugurated a new tertiary amine plant in the United States, strengthening precursor supply for specialty amide and surfactant chains. Stable upstream availability improves reliability for downstream EBS producers reliant on fatty acid and amine feedstocks.

India is emerging as a competitive export hub. MLA Group significantly scaled EBS exports during 2024–2025, leveraging multi-tier quality control systems aligned with EU REACH and U.S. FDA standards. This positions Indian manufacturers as reliable suppliers of high-bloom, high-purity grades used in engineering plastics and specialty masterbatch formulations.

Technological demand drivers remain robust. EBS is increasingly specified in high-temperature thermoplastics, 3D printing filaments, and recyclable polymer blends, where controlled migration behavior and improved pigment dispersion are critical. Simultaneously, recyclate-enhanced plastics require performance additives capable of restoring surface smoothness and reducing melt friction—an area where EBS continues to demonstrate superior compatibility.

Trends and Opportunities in the Ethylene Bis Stearamide (EBS) Market

Reformulation for High-Speed, Energy-Efficient Masterbatches

- Plastics processors are intensifying the use of EBS-based internal and external lubricants to reduce melt viscosity and improve processing efficiency in extrusion and injection molding operations.

- Between 2024 and 2025, technical data from large-scale compounding facilities showed that optimized EBS formulations reduced shear stress by 10 to 15% during polyolefin processing. This reduction enables processors to operate at lower barrel temperatures, delivering measurable reductions in electricity consumption per kilogram of polymer processed. As energy intensity becomes a monitored KPI across global plastics operations, these efficiency gains are directly influencing additive selection.

- Product innovation is reinforcing this trend. In September 2025, HERWE expanded its HERWEMAG AWV-N2 portfolio with vegetable-based EBS supplied in dust-free pellet form. These pellets are engineered for automated masterbatch lines, improving dosing accuracy, enhancing pigment dispersion, and reducing occupational exposure risks associated with fine powders.

- Despite innovation in pelletized forms, powder EBS continues to dominate. Industry observations in late 2025 indicate that powder grades account for roughly 64% of total EBS consumption, driven by superior dispersion in dry-blend PVC and ABS formulations. This form factor remains critical for compounders prioritizing consistent surface finish and color uniformity in high-output lines.

Scaling Bio-Based and Sustainability-Certified EBS Grades

- Sustainability certification is moving from a differentiator to a procurement requirement, particularly in consumer-facing and export-oriented plastic products.

- Oleochemical leaders such as KLK OLEO are expanding RSPO-certified vegetable-based EBS offerings, including the PALMOWAX series. These grades rely on sustainably sourced stearic acid and are increasingly specified in food-contact packaging, cosmetic containers, and household goods where traceability and renewable carbon content are mandatory.

- Feedstock transition is extending beyond fatty acids. Industry developments in January 2025 highlighted growing investment in bio-based ethylenediamine synthesis. By sourcing ethylene from agricultural residues, initiatives involving Dow and New Energy Blue are enabling the production of EBS with materially lower lifecycle emissions compared to conventional petrochemical routes.

- By November 2025, high-purity and non-toxic EBS grades were being prioritized by personal care manufacturers, where EBS functions as a rheology modifier and emulsifier. The global shift toward clean beauty formulations has driven increased demand for plant-derived lubricants that maintain performance while meeting stringent safety and labeling expectations.

Enabling High-Filler-Load Wood Plastic Composites

- The rapid adoption of wood plastic composites in construction and landscaping is creating a structurally strong demand base for EBS.

- The global WPC market reached an estimated value of USD 8.89 billion in 2025, with building and construction applications accounting for more than 70% of total demand. High filler loadings of wood fiber and minerals introduce abrasive processing conditions, making EBS a critical lubricant to protect extrusion equipment and ensure smooth polymer encapsulation.

- Regulatory support is accelerating adoption. In July 2024, the U.S. Environmental Protection Agency issued guidelines encouraging the use of WPC in federal landscaping and infrastructure projects due to durability and reduced maintenance. These applications require specialized lubricant systems, positioning EBS as an enabling additive for compliance-driven growth.

- Commercial product launches underscore this role. The June 2024 introduction of Proshield WPC Cladding by Oakio highlighted high-density polyethylene blends designed for architectural performance. EBS remains essential in achieving the surface quality, dimensional stability, and long-term weather resistance demanded by such profiles.

Improving 3D Printing Filament Quality and Flow

- The industrialization of additive manufacturing is opening a high-margin niche for EBS as a processing aid in thermoplastic filaments.

- According to the Wohlers Report 2025, the global additive manufacturing industry expanded by 9.1% to reach USD 21.9 billion, with materials accounting for a growing share of value creation. Maintaining filament diameter tolerances within ±0.03 mm is critical for industrial printers, and EBS is increasingly specified to stabilize melt flow and reduce extrusion variability.

- In fused filament fabrication, EBS minimizes nozzle friction, reduces stringing, and improves interlayer adhesion in PLA, ABS, and PETG filaments. These benefits enable higher print speeds without sacrificing part integrity, supporting adoption in automotive tooling, aerospace fixtures, and functional end-use components.

- Strategic investments reinforce this opportunity. In April 2025, 3D Systems announced new application-specific solutions for motorsports and healthcare. These use cases demand repeatable, thermally stable materials, where EBS-enhanced filaments play a central role in ensuring consistent quality and production reliability.

Ethylene Bis Stearamide (EBS) Market Share and Segmentation Insights

Powder Form Dominates Processing Applications Across Polymer Compounding

Powder EBS accounts for 38% of total market share in 2025, reflecting its widespread adoption in plastic compounding, masterbatch production, and rubber processing. The powder form offers balanced particle size, consistent dispersion, and compatibility with polyolefins, ABS, and engineering plastics, making it the preferred choice for slip, anti-block, and lubricant functionality. Beads represent a significant secondary segment, favored for dust-free handling and improved flow in automated feeding systems, particularly in large-scale extrusion and injection molding operations. Fine powder remains important in specialty coatings, inks, and high-performance polymer formulations where rapid melting and uniform dispersion at low loadings are essential. Granules occupy a niche position, serving applications that require controlled melting or delayed release characteristics in select rubber and masterbatch processes.

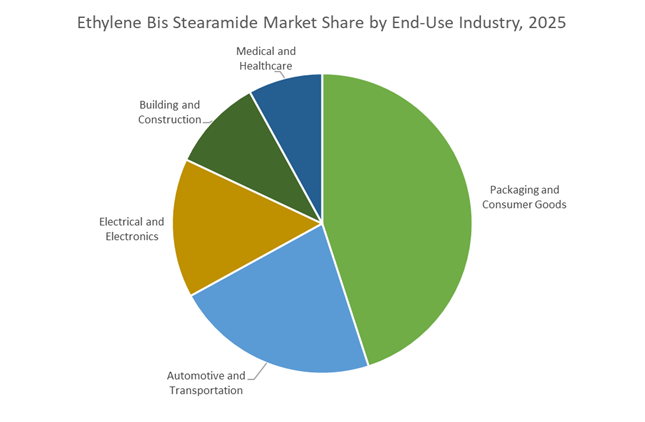

Packaging and Consumer Goods Lead EBS Consumption with Automotive and Electronics Support

Packaging and consumer goods account for 45% of global EBS demand in 2025, driven by its role as a slip agent, anti-block additive, and processing lubricant in polyolefin films, food packaging, and molded consumer products. EBS reduces coefficient of friction, prevents film sticking, and enhances surface finish in blown film and injection molding operations. Automotive and transportation represent a major secondary segment, incorporating EBS in polypropylene and ABS components to improve mold flow and surface properties. Electrical and electronics applications utilize EBS in wire and cable insulation and connector housings, benefiting from its lubricity and insulation characteristics. Building and construction rely on EBS in PVC pipe and profile manufacturing for improved processing efficiency, while medical and healthcare applications are growing steadily, using high-purity EBS in medical device components and pharmaceutical packaging where compliance and biocompatibility are essential.

Competitive Landscape of the Ethylene Bis Stearamide (EBS) Market

The global Ethylene Bis Stearamide (EBS) market in 2026 is shaped by vertically integrated oleochemical leaders and specialty additive innovators competing on RSPO-certified feedstocks, high-purity grades, and performance-driven solutions for plastics compounding, inks, wire & cable, and engineering polymers.

KLK OLEO dominates global EBS supply through palm-based vertical integration

KLK OLEO leads the ethylene bis stearamide market with an estimated 15 to 18% global share in 2026, supported by integrated manufacturing hubs across Malaysia, China, and Düsseldorf. Its PALMOWAX range is widely specified as the industry-standard EBS lubricant and dispersing agent for ABS, PS, and PP compounding. KLK’s core advantage lies in full vertical integration, controlling the value chain from palm plantations to stearic acid and finished EBS. In 2026, the company is prioritizing traceable, RSPO-certified grades to comply with the EU Deforestation Regulation (EUDR), reinforcing its leadership in sustainable polymer additives and bio-based processing aids.

Fine Organic Industries Ltd. scales renewable EBS for inks, masterbatches, and 3D printing

Fine Organic Industries Ltd. is a dominant player in green polymer additives, supplying oleochemical-based EBS to global plastics and coatings markets. During 2025 to 2026, the company expanded its Finawax C series with a micro-fine powder grade optimized for 3D printing filaments and powder metallurgy. A new Indian production block commissioned in late 2025 lifted overall capacity to serve Southeast Asian masterbatch demand. Its EBS grades are specified for pigment dispersion in high-speed inks due to thermal stability above 240°C. Notably, Fine Organics transitioned its entire EBS production to 100% renewable energy, advancing its Zero-Carbon 2030 roadmap.

Kao Corporation targets premium electronics EBS with AI-driven customization

Kao Corporation positions itself as a quality leader in high-purity ethylene bis stearamide for electronics, automotive, and precision molding applications. Under its K27 mid-term plan accelerated in February 2026, Kao is expanding its Global Chemical business beyond Japan, focusing on specialty margins. Its KAO WAX EB delivers ultra-low volatility and superior metal release in injection molding. In 2025 to 2026, Kao introduced AI-powered “Individual Optimal Selection” to tailor EBS particle sizes to polymer melt-flow indexes. The company is also advancing biomanufacturing via a NEDO-backed initiative to de-fossilize its chemical intermediate chain.

PMC Biogenix strengthens North American EBS supply for engineering plastics

PMC Biogenix is the leading North American EBS supplier, serving engineering plastics, rubber, and powder metallurgy markets. Its Kemamide® W-40 brand is widely used as a processing aid in wire and cable compounds. PMC’s technical customization spans beads, prills, and micronized powders to match specialized feeding systems. In 2025 to 2026, the company invested in advanced flaking technology at its Memphis facility to introduce dust-free EBS beads, improving workplace safety. High-purity PMC grades are also critical internal lubricants in automotive powder metallurgy, ensuring consistent density and part integrity.

Croda International Plc advances bio-based EBS blends for food-contact and ECO additives

Croda International Plc is repositioning its EBS portfolio around sustainability and high-value applications. Following an €18 million investment in France in late 2025, Croda expanded European capacity for specialty additives, supporting regional manufacturing resilience. Its Incroslip™ and EBS blends are marketed as premium slip agents for food-contact packaging, meeting updated 2026 FDA and EFSA standards. Under its Green Transformation strategy, Croda targets mid-to-high single-digit organic growth via ECO-range additives using 100% bio-based carbon. To accelerate specification wins post inventory correction, the company deployed regional application labs in China and India.

India: Regulatory Relief Enabling Export-Oriented Scale-Up

India’s ethylene bis stearamide market entered a structurally favorable phase in late 2025 following decisive regulatory de-escalation. The Ministry of Chemicals and Fertilizers’ November 28, 2025 notification rescinding mandatory BIS Quality Control Orders for several industrial chemicals materially reduced compliance friction for specialty additives such as ethylene bis stearamide. For domestic producers, this change has eased access to imported fatty acids and amine intermediates while shortening approval timelines for downstream customers in plastics compounding and masterbatch manufacturing. The policy shift is particularly relevant for high-purity EBS grades used as slip agents, mold-release additives, and internal lubricants where formulation consistency is critical.

Capacity and distribution strategies are evolving in parallel. Fine Organic Industries secured final environmental clearance in August 2025 for a ₹7.5 billion greenfield project on SEZ land, engineered for high-purity oleochemical additives with commissioning targeted for early 2027. This domestic scale-up is complemented by an outward-facing distribution pivot. The incorporation of a wholly owned subsidiary in Dubai’s Jebel Ali Free Zone in December 2025 positions India as an export hub to GCC and European markets during the 2026 fiscal cycle. On the demand side, the BioE3 Policy is accelerating adoption of non-toxic lubricants like EBS in bioplastic mulching films, while the removal of ABS quality controls has intensified competition. As a result, Indian suppliers are prioritizing performance-differentiated dispersing grades to retain relevance in local ABS compounding and injection molding applications.

China: Feedstock Supremacy and Polymer-Aligned Formulation Shifts

China’s ethylene bis stearamide ecosystem is being reshaped by unmatched upstream feedstock dominance. By end-2025, national ethylene capacity surpassed 62 million metric tons, delivering structurally lower costs for ethylene-derived intermediates used in amide wax synthesis. This advantage is reinforced by the commissioning of large integrated petrochemical complexes, including ExxonMobil’s Daya Bay project and BASF’s Zhanjiang site, both of which embed downstream specialty chemical units that directly support regional EBS production.

The market’s strategic pivot is increasingly formulation-driven rather than purely volume-led. China’s rapid expansion in metallocene polyethylene has forced EBS producers to recalibrate products as high-efficiency anti-blocking and slip agents for thinner, high-performance films expected in the 2026 packaging cycle. Breakthroughs in ethylene oxide availability, highlighted by Jilin Petrochemical’s successful startup of a 300,000 tpa unit in October 2025, are strengthening local supply chains for complex amide wax synthesis.

United States: Reshoring, EV Integration, and Regulatory Tailwinds

The U.S. ethylene bis stearamide market is undergoing strategic reshoring combined with demand-side upgrading. In July 2025, Fine Organics announced the acquisition of 159.9 acres in South Carolina to establish a domestic manufacturing base, targeting improved supply reliability for automotive and packaging customers seeking localized sourcing. This move reflects a broader U.S. trend toward shortening additive supply chains amid logistics volatility.

Demand growth is increasingly linked to electrification and sustainability mandates. Industrial audits in late 2025 indicate a 16% increase in EBS usage within molded automotive components as OEMs pursue lightweighting for EV platforms. Regulatory alignment is reinforcing this trajectory. Under the 2026 EPA SNAP framework, ethylene bis stearamide is being fast-tracked as a preferred green lubricant, accelerating substitution away from metal-based stearates in powder metallurgy and wire drawing. At the premium end, U.S. demand for ultra-fine EBS powders used in specialty coatings and aerospace finishes expanded by 12% in 2025, signaling a shift toward higher-margin, purity-sensitive applications.

Japan: Sustainability-Led Innovation and Electronic-Grade Focus

Japan’s EBS market is characterized by material science-led differentiation rather than capacity expansion. Kao Corporation’s Integrated Report 2025 outlined its Global Sharp Top strategy, emphasizing EBS waxes derived from low-solubility natural raw materials to support a circular bio-economy. This approach aligns with domestic sustainability priorities while preserving performance in demanding polymer systems.

Looking ahead to 2026, Japanese manufacturers are pivoting toward electronic-grade ethylene bis stearamide used as high-purity insulating lubricants in advanced semiconductor packaging and electronics assembly. Kao’s proprietary interfacial science breakthroughs, disclosed in mid-2025, are being applied to develop hybrid EBS lubricants capable of functioning effectively in both water- and oil-based polymer matrices. This dual compatibility is increasingly valuable for next-generation electronics and specialty engineering plastics, reinforcing Japan’s position as a technology benchmark supplier rather than a volume competitor.

Strategic Snapshot: Ethylene Bis Stearamide Market by Country (2025–2026)

Ethylene BIS Stearamide Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Application Focus

|

Competitive Implication

|

|

India

|

Regulatory easing and export orientation

|

Plastics, bioplastics, ABS compounding

|

Scale-up with performance differentiation

|

|

China

|

Feedstock integration and polymer alignment

|

Packaging films, automotive plastics

|

Cost leadership with formulation agility

|

|

United States

|

Reshoring and EV-driven demand

|

Automotive, aerospace, powder metallurgy

|

Premium-grade and localized supply

|

|

Japan

|

Sustainability and electronic-grade innovation

|

Semiconductors, engineering plastics

|

Technology-led margin resilience

|

Ethylene BIS Stearamide Market Report Scope

Ethylene BIS Stearamide market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$522.7 Million

|

|

Market Size (2034)

|

$776.8 Million

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Product Form (Beads, Powder, Fine Powder, Granules), By Grade (Technical Grade, Food Grade, Pharmaceutical Grade), By Application (Plastic Processing, Rubber Manufacturing, Inks and Coatings, Powder Metallurgy, Adhesives and Tapes, Asphalt and Potting Compounds, Textiles), By End-Use Industry (Packaging and Consumer Goods, Automotive and Transportation, Electrical and Electronics, Building and Construction, Medical and Healthcare)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kao Corporation, Fine Organic Industries Limited, Croda International Plc, BASF SE, Evonik Industries AG, PMC Biogenix, Inc., KLK Oleo, Emery Oleochemicals, Lonza Group, Mitsubishi Chemical Group, MÜNZING Chemie GmbH, DEUREX AG, Sinwon Chemical Co., Ltd., Nippon Fine Chemical Co., Ltd., Shandong Huayang Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ethylene Bis Stearamide Market Segmentation

By Product Form

- Beads

- Powder

- Fine Powder

- Granules

By Grade

- Technical Grade

- Food Grade

- Pharmaceutical Grade

By Application

- Plastic Processing

- Rubber Manufacturing

- Inks and Coatings

- Powder Metallurgy

- Adhesives and Tapes

- Asphalt and Potting Compounds

- Textiles

By End-Use Industry

- Packaging and Consumer Goods

- Automotive and Transportation

- Electrical and Electronics

- Building and Construction

- Medical and Healthcare

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ethylene Bis Stearamide Industry

- Kao Corporation

- Fine Organic Industries Limited

- Croda International Plc

- BASF SE

- Evonik Industries AG

- PMC Biogenix, Inc.

- KLK Oleo

- Emery Oleochemicals

- Lonza Group

- Mitsubishi Chemical Group

- MÜNZING Chemie GmbH

- DEUREX AG

- Sinwon Chemical Co., Ltd.

- Nippon Fine Chemical Co., Ltd.

- Shandong Huayang Chemical

*- List not Exhaustive