Ethylene Butyl Acrylate (EBA) Market Expands on Adhesives, Flexible Packaging, and Automotive Lightweighting

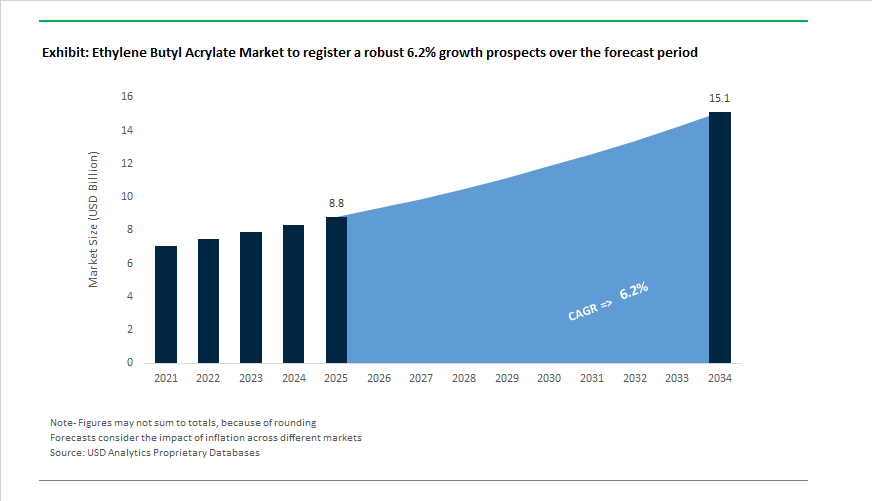

The Ethylene Butyl Acrylate (EBA) Market is projected to grow from $8.8 billion in 2025 to $15.1 billion by 2034, registering a CAGR of 6.2%. Demand is being propelled by the rapid expansion of high-performance adhesives, flexible multilayer packaging, automotive sealants, and impact-modified polymer systems. EBA copolymers—valued for their superior flexibility, low-temperature toughness, adhesion to polar substrates, and stress-crack resistance—are increasingly replacing conventional EVA and polyethylene blends in premium end-use applications.

A key structural development is the strengthening of upstream acrylate integration. In July 2025, Indian Oil Corporation confirmed progress toward commissioning its 150 KTA Butyl Acrylate plant at the Gujarat Refinery Complex. Based on Mitsubishi Chemical technology, the facility provides a critical domestic supply of butyl acrylate monomer, reducing India’s dependence on imports and supporting downstream EBA production for adhesives, coatings, and infrastructure membranes. This move aligns with India’s industrial self-sufficiency strategy and positions the country as a regional hub for acrylate-based polymer systems.

European production dynamics are shifting due to rationalization and restructuring. In April 2025, Dow Inc. announced the shutdown of multiple upstream European assets, including the Böhlen cracker in Germany. The restructuring aims to streamline operations and deliver a $200 million EBITDA uplift. Reduced regional upstream capacity could tighten feedstock availability for ethylene derivatives, potentially influencing EBA pricing dynamics in Europe through 2027. In January 2026, Dow further launched its Transform to Outperform program, targeting $2 billion in EBITDA improvement and modernizing supply alignment for packaging and automotive customers.

Competitive differentiation is increasingly linked to regulatory approvals and sustainable content integration. In late 2024, Repsol secured FDA approval for its Ebantix® EBA grades for food-contact applications. This certification allows penetration into high-margin food packaging markets where EBA’s low water absorption and strong seal integrity under variable temperature conditions are critical. Meanwhile, in April 2025, Arkema converted its European acrylic rheology line to include up to 30% bio-based content, reducing product carbon footprint by approximately 25% compared to conventional petroleum-based grades.

Asia-Pacific continues to see competitive polymer innovation. SK Functional Polymer launched high-polarity acrylate copolymers targeting breathable films and industrial membranes—segments that directly compete with premium EBA applications. Such developments indicate growing emphasis on higher acrylate-content resins designed for durability and chemical resistance in demanding environments.

Upstream feedstock stability remains central to margin performance. In November 2025, Westlake Chemical Partners LP renewed its Ethylene Sales Agreement, securing stable margins on 95% of its ethylene output through 2027. This arrangement insulates downstream polymer operations—including acrylate copolymers—from feedstock volatility, strengthening supply reliability in North America.

Automotive lightweighting, food-grade multilayer packaging, infrastructure sealants, and specialty wire & cable coatings are expected to remain primary growth pillars. EBA’s ability to enhance impact resistance in polypropylene blends and maintain flexibility in sub-zero climates positions it favorably for electric vehicle battery encapsulation films and cold-chain packaging systems.

Trends and Opportunities in the Ethylene Butyl Acrylate (EBA) Copolymer Market

Accelerated Substitution of Flexible PVC in Regulated Medical and Wire & Cable Applications

- Stringent environmental and health regulations are accelerating the displacement of flexible PVC by EBA copolymers in highly regulated sectors. Updates to EU REACH and continued U.S. regulatory scrutiny on phthalates and halogenated materials have made inherently flexible polyolefins commercially preferable to plasticized PVC.

- Unlike PVC, EBA copolymers achieve softness without migratory plasticizers, eliminating risks associated with DEHP leaching and dioxin formation. In medical applications, EBA-modified polyolefins are increasingly specified for IV bags, infusion tubing, and cardiovascular catheters. Recent industry validation shows that EBA-based medical tubing maintains close to 90% optical transparency while retaining flexibility across a wide operating temperature range, supporting both clinical safety and device durability.

- In wire and cable, EBA adoption is being driven by the global shift toward Low-Smoke Zero-Halogen cable systems. EBA does not release corrosive hydrochloric acid gas during processing or combustion, reducing equipment damage and post-fire recovery costs. Large-scale infrastructure projects commissioned during 2024–2025, particularly in data centers and high-speed rail corridors, have standardized EBA-based jacketing to meet combined fire safety, corrosion resistance, and long-term insulation reliability requirements.

Integration into High-Barrier Multilayer Packaging for Food Safety and Lightweighting

- EBA copolymers are playing a central role in the evolution of high-barrier multilayer packaging, where bonding dissimilar polymers is a persistent technical challenge. Their inherent polarity enables strong adhesion between non-polar polyethylene layers and polar barrier materials such as EVOH and polyamide.

- By early 2025, the global tie-layer resin segment, where EBA is a core component, reached an estimated value of USD 1.83 billion. Growth is being driven by five-layer and seven-layer barrier films used in meat, dairy, and ready-meal packaging, where oxygen and moisture resistance directly reduce food spoilage and logistics waste.

- EBA-based sealant layers also offer lower seal initiation temperatures than conventional LDPE. On high-speed packaging lines operating at up to 830 feet per minute, this characteristic has translated into roughly 15% higher line efficiency and about 10% lower sealing energy consumption. These gains are strategically important as packaging converters balance throughput expansion with rising energy costs and sustainability targets.

High-Performance Adhesives for Automotive and Electronics Assembly

- The shift toward lightweight electric vehicles and miniaturized electronics is driving demand for adhesives capable of bonding low-surface-energy plastics without surface pretreatment. EBA copolymers are increasingly incorporated into hot-melt adhesive formulations to deliver high tack, flexibility, and thermal stability.

- In automotive interiors, EBA-modified adhesives are replacing mechanical fasteners in trim, headliners, and NVH components, supporting weight reduction and improved acoustic performance. In electronics assembly, comparative benchmarks from 2024 showed that EBA-enhanced systems outperform traditional EVA adhesives in UV resistance and long-term aging. This performance advantage is critical in applications such as display panel bonding and flexible printed circuits, where thermal cycling and dimensional stability directly impact product lifespan.

- As electronics assembly continues to scale across Asia, North America, and Europe, EBA-based adhesives are emerging as a preferred solution in a global market exceeding USD 20 billion annually.

Advanced Impact Modification for Post-Consumer Recycled Plastics and Renewable Energy Systems

- Global mandates for recycled content are exposing the mechanical weaknesses of post-consumer recycled polyolefins, particularly brittleness and inconsistent impact strength. EBA is emerging as a key compatibilizer to restore performance in these materials.

- Industry collaborations announced in December 2025 by Borealis and Dow demonstrated that incorporating just 5 to 10% EBA into recycled polypropylene can improve notched impact strength by more than 40%. This enables recycled plastics to be used in higher-value applications such as automotive bumpers, durable consumer housings, and industrial containers.

- Upstream sustainability is reinforcing this opportunity. In August 2024, BASF completed the transition of its ethyl acrylate portfolio to a bio-based version with approximately 40% renewable content. As ethyl acrylate is a critical EBA feedstock, this development allows EBA producers to offer copolymers with lifecycle carbon footprint reductions of around 30 %, directly supporting Scope 3 emission reduction targets for global brand owners.

- Beyond circular plastics, renewable energy applications are emerging as a structurally important demand driver. By late 2025, energy majors including ExxonMobil and Repsol reported advances in EBA-based solar encapsulation materials. Compared to traditional EVA, EBA demonstrates superior weatherability and a lower yellowing index over 25-year service lifecycles, making it increasingly attractive for long-duration photovoltaic installations.

Ethylene Butyl Acrylate (EBA) Market Share and Segmentation Insights

Medium Butyl Acrylate Content Grades Lead with Balanced Flexibility and Mechanical Strength

Medium butyl acrylate (BA) content EBA copolymers, typically containing 15–30% BA, account for 48% of total market share in 2025, reflecting their position as the most versatile formulation category. These grades deliver an optimal balance of flexibility, tensile strength, and thermal stability, making them the preferred choice for hot melt adhesives, wire and cable jacketing, and polymer modification. Low BA content grades (around 5–15%) maintain a significant share in packaging films and extrusion coatings, where higher crystallinity and dimensional stability are critical for barrier performance. High BA content EBA (30%+ BA) is the fastest-growing segment, increasingly specified for solar encapsulants, impact modifiers, and specialty adhesives that demand extreme flexibility and low-temperature toughness. This diversified grade structure allows EBA producers to address applications ranging from rigid packaging to highly elastic renewable energy materials.

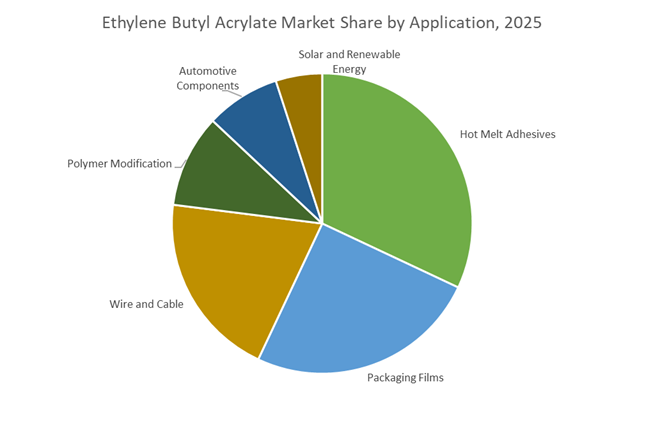

Hot Melt Adhesives Anchor Demand as Packaging and Energy Applications Expand

Hot melt adhesives represent 32% of global EBA consumption in 2025, driven by EBA’s strong adhesion to non-porous substrates, long open time, and thermal stability across packaging, bookbinding, woodworking, and hygiene products. Packaging films form a major secondary segment, using EBA in coextruded structures for food packaging, stretch hoods, and industrial sacks where toughness and heat-seal performance are essential. Wire and cable applications rely on EBA for jacketing and semiconductive layers in medium- and high-voltage systems. Polymer modification continues to grow, with EBA improving impact resistance in polypropylene, polyamide, and polyester compounds for automotive and industrial components. Automotive applications remain steady across interiors and harnesses, while solar and renewable energy is emerging rapidly, adopting high-BA EBA grades as encapsulants for photovoltaic modules requiring transparency, adhesion, and long-term weatherability.

Competitive Landscape of the Ethylene Butyl Acrylate (EBA) Market

The global Ethylene Butyl Acrylate market in 2026 is defined by specialty polymer leaders competing on high-pressure polymerization expertise, bio-attributed EBA grades, and application-driven innovation across hot-melt adhesives, HFFR cables, extrusion coating, automotive plastics, and advanced packaging.

Arkema S.A. leads bio-attributed EBA innovation for adhesives and packaging

Arkema S.A. is a pioneer in high-pressure polymerization and a global benchmark in EBA technology through its LOTRYL® BA series, offering acrylate content up to 35% for hot-melt adhesives and polymer modification. During 2025 to 2026, Arkema introduced bio-attributed EBA grades using a mass-balance approach, helping packaging customers reduce Scope 3 emissions. Its Taixing Sunke Chemicals facility in China anchors Arkema’s dominance in the Asian merchant market, supporting electronics and footwear manufacturing clusters. A core differentiator is Arkema’s formulation depth, providing detailed reactivity ratio data that enables precise copolymer customization for impact modification, flexibility enhancement, and adhesion performance in demanding industrial applications.

LyondellBasell Industries scales circular EBA solutions for cables and multilayer film recycling

LyondellBasell Industries supplies Lucalen EBA resins known for high melt strength and broad molecular weight distribution, making them ideal for high-speed extrusion coating. In 2026, the company showcased its Circular Solutions strategy at PLASTINDIA, positioning EBA as a universal compatibilizer that enables recycling of previously non-recyclable multilayer films. LyondellBasell dominates the HFFR cable segment, where EBA supports high aluminum trihydroxide loading while preserving mechanical flexibility for power grid infrastructure. Strategically, the company is pivoting from commodity polyethylene toward value-driven specialty resins like EBA to stabilize margins amid petrochemical cyclicality.

Dow Inc. advances medical-grade and automotive EBA with AI-enabled production

Dow Inc. positions EBA as a premium material for packaging, automotive, and medical plastics through its ELVALOY® AC copolymers, valued for toughness without brittleness in PET and PA impact modification. In 2026, Dow embedded AI-driven digital twins across EBA production lines to achieve ultra-low impurity levels required for medical-grade extractables. Its Transform to Outperform program is modernizing EBA assets, targeting a 10 to 12% carbon footprint reduction versus 2020. Dow’s global integrated supply chain ensures consistent availability, making it a preferred EBA partner for multinational automotive OEMs and advanced packaging converters.

Westlake Corporation delivers high-temperature EBA resins for industrial sealing and solar encapsulation

Westlake Corporation specializes in functionalized acrylate resins through its EBAC® and EBAC+® product lines, with patented blocked copolymer technology that enhances adhesion to non-polar substrates. In February 2026, Westlake reported gains from its PEM profitability improvement plan, driven partly by optimizing its specialty acrylate mix. Its plus grades offer thermal stability up to ~330°C, providing a competitive edge in high-temperature industrial sealing. EBA is also emerging in solar panel encapsulation, where Westlake materials deliver long-term UV resistance and moisture barrier performance for outdoor renewable energy installations.

Repsol S.A. targets semiconductor-grade EBA for Europe’s power cable infrastructure

Repsol S.A. has built a specialized European niche with its Ebantix® EBA range, engineered for high-performance compounds and semi-conductive layers in medium-to-high voltage cables. Under its European Resilience strategy, Repsol is positioning itself as a regional alternative to Asian imports, emphasizing short lead times and strict REACH and EU Green Deal compliance. In late 2025, the company launched a semicon-grade EBA with ultra-low metallic impurities to prevent electrical breakdown in undersea power cables. Deep integration into Spain’s refining and aromatics chains enables effective hedging of ethylene and butyl acrylate feedstock costs.

China: Verbund Economics and Import Replacement in High-End Acrylates

China’s ethylene butyl acrylate landscape is being reshaped by large-scale feedstock integration and policy-backed self-sufficiency. In August 2025, BASF successfully commenced operations at its 400,000 metric ton per year butyl acrylate plant at the Zhanjiang Verbund site. This asset is structurally advantaged by full backward integration, including a one million ton ethylene steam cracker scheduled for complete start-up by December 2025. For domestic EBA producers, this sharply reduces ethylene and acrylate ester input volatility, allowing more predictable pricing for downstream copolymer producers serving automotive interiors, wire and cable, and solar encapsulation films.

Policy alignment is accelerating this shift. Under the MIIT 2025–2026 work plan focused on High-End New Materials, Chinese majors such as Sinopec and Wanhua Chemical are scaling EBA output to displace imports previously sourced from Northeast Asia and Europe. Supply chain resilience is further reinforced by infrastructure-linked intermediates. The ramp-up of Jilin Petrochemical’s 300,000 tpa ethylene oxide unit in October 2025 secures key inputs for advanced EBA copolymers used in high-durability coatings. As a result, China is transitioning from volume-driven EBA consumption to application-specific, performance-led formulations aligned with infrastructure coatings and next-generation mobility.

India: Structural Import Substitution and Refinery-to-Polymer Linkages

India entered a decisive inflection point in 2025 with the commissioning trajectory of its first domestic butyl acrylate facility. Indian Oil Corporation is on track to bring a 150 KTA BA plant online at the Gujarat Refinery Complex in July 2025, utilizing Mitsubishi Chemical technology. This single project fundamentally alters India’s ethylene butyl acrylate value chain by eliminating complete import dependence for acrylate-based polymer modifiers used in adhesives, packaging films, and automotive sealants. For downstream processors, localized BA availability reduces lead times and currency exposure while enabling tighter formulation control.

Policy frameworks are reinforcing long-term demand. The 2025 BioE3 Policy is incentivizing pilot-scale development of bio-based acrylates, with Indian research institutions testing EBA grades containing up to 30% renewable content for sustainable flexible packaging. At the same time, infrastructure readiness is improving. The HPCL Rajasthan Refinery, expected to reach final commissioning in early 2026, is engineered to supply high-purity ethylene and aromatics. This creates the backbone for secondary EBA units in Western India, supporting domestic growth in hot-melt adhesives, pressure-sensitive labels, and impact-modified plastics.

United States: Reshoring, EV Demand, and Regulatory Pull-Through

The U.S. ethylene butyl acrylate market is increasingly shaped by capacity optimization and application diversification rather than greenfield builds. In mid-2025, major producers including Dow and ExxonMobil reported record utilization rates across Texas-based ethylene copolymer lines. These trends reflect a 30% capacity boost executed during 2023–2024 to meet accelerating demand for EBA in EV battery housings, lightweight interior components, and high-performance hot-melt adhesives.

Regulation is acting as a demand catalyst rather than a constraint. Updated EPA SNAP guidelines effective January 2026 are accelerating substitution of phthalate-based plasticizers with EBA, particularly in industrial sealants and medical-grade tubing where low toxicity and flexibility retention are critical. At the same time, legal precedents around recycling and circularity reporting, influenced by ExxonMobil’s early 2025 regulatory challenges in California, are reshaping how EBA producers document recycled content and lifecycle performance. This is pushing suppliers to provide more robust technical data aligned with 2026 sustainability disclosures.

Germany: Low-Carbon Feedstocks and Electronics-Driven Adhesive Demand

Germany’s EBA market is increasingly defined by decarbonization and electronics-led consumption. BASF and Evonik have initiated a transition toward bio-attributed ethylene feedstocks for European EBA lines. By 2026, these producers aim to commercialize low-carbon footprint EBA grades that directly support automotive OEM compliance with the EU Corporate Sustainability Reporting Directive. This shift is less about volume expansion and more about embedding carbon metrics into material selection for Tier 1 suppliers.

Demand-side momentum is strongest in advanced adhesives. In September 2025, German distributors reported a 14% increase in procurement of high-butyl-content EBA for UV-curable adhesive systems. This trend is driven by the electronics sector’s push toward faster curing cycles, reduced VOC emissions, and improved adhesion on mixed substrates. Consequently, Germany is emerging as a premium market for performance-optimized EBA rather than a price-driven outlet.

South Korea: Specialty Pivot and Acrylate Copolymer Differentiation

South Korea’s ethylene butyl acrylate trajectory is closely linked to its broader petrochemical rationalization agenda. In late 2024 and early 2025, SK Functional Polymer introduced the LOTRYL 40MA05T grade, signaling a strategic pivot toward high-polarity acrylate copolymers as alternatives to EVA in flexible cable jacketing and impact modification. While not a pure EBA grade, the launch reflects a wider 2025–2026 roadmap to reposition acrylate chemistry as a specialty growth lever.

This strategy is reinforced by government direction. Under the 2026 Petrochemical Vision emphasizing Specialty over Commodity, companies such as LG Chem are converting standard polyethylene assets into EBA and EEA copolymer units. The objective is to serve global semiconductor, solar, and electronics markets where performance margins are structurally higher and less exposed to cyclical oversupply.

Strategic Snapshot: Ethylene Butyl Acrylate Market by Country (2025–2026)

Ethylene Butyl Acrylate (EBA) Market County Level Snapshot

|

Country

|

Structural Driver

|

Key Applications

|

Strategic Implication

|

|

China

|

Verbund integration and self-sufficiency

|

Infrastructure coatings, automotive, solar

|

Cost leadership with performance scaling

|

|

India

|

First-time domestic BA production

|

Adhesives, packaging, automotive modifiers

|

Import substitution and rapid demand unlock

|

|

United States

|

Reshoring and EV-led demand

|

EV components, medical tubing, hot-melt adhesives

|

High utilization and regulatory pull-through

|

|

Germany

|

Decarbonized feedstocks

|

UV-curable adhesives, electronics

|

Premium low-carbon EBA positioning

|

|

South Korea

|

Specialty petrochemical pivot

|

Cable jacketing, semiconductors, solar

|

Margin expansion via copolymer differentiation

|

Ethylene Butyl Acrylate (EBA) Market Report Scope

Ethylene Butyl Acrylate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.8 Billion

|

|

Market Size (2034)

|

$15.1 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Butyl Acrylate Content (Low Content, Medium Content, High Content), By Grade (Industrial Grade, Polymer Grade, Specialty Grade), By Application (Hot Melt Adhesives, Wire and Cable, Packaging Films, Polymer Modification, Solar and Renewable Energy, Automotive Components), By End-Use Industry (Packaging, Automotive and Transportation, Electrical and Electronics, Building and Construction, Renewable Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., ExxonMobil Corporation, BASF SE, Arkema S.A., SK Functional Polymer, LyondellBasell Industries N.V., Westlake Corporation, Borealis AG, China Petroleum & Chemical Corporation, LG Chem, Mitsui & Dow Polychemicals, Repayl S.A., Wanhua Chemical Group, Mitsubishi Chemical Group, Indian Oil Corporation Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ethylene Butyl Acrylate Market Segmentation

By Butyl Acrylate Content

- Low Content

- Medium Content

- High Content

By Grade

- Industrial Grade

- Polymer Grade

- Specialty Grade

By Application

- Hot Melt Adhesives

- Wire and Cable

- Packaging Films

- Polymer Modification

- Solar and Renewable Energy

- Automotive Components

By End-Use Industry

- Packaging

- Automotive and Transportation

- Electrical and Electronics

- Building and Construction

- Renewable Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ethylene Butyl Acrylate Industry

- Dow Inc.

- ExxonMobil Corporation

- BASF SE

- Arkema S.A.

- SK Functional Polymer

- LyondellBasell Industries N.V.

- Westlake Corporation

- Borealis AG

- China Petroleum & Chemical Corporation

- LG Chem

- Mitsui & Dow Polychemicals

- Repayl S.A.

- Wanhua Chemical Group

- Mitsubishi Chemical Group

- Indian Oil Corporation Limited

*- List not Exhaustive