The global Ethylene Market study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments including By Feedstock (Naphtha, Ethane, LPG, Others), By Application (LDPE, HDPE, Ethylene oxide, Vinyl, Others).

The Ethylene Market remains a cornerstone of the global petrochemical industry, serving as a fundamental building block for the production of a wide range of plastics, chemicals, and synthetic materials. Ethylene, a key hydrocarbon compound derived primarily from ethane or naphtha feedstocks, finds extensive application in polymerization processes to manufacture polyethylene, the most widely used plastic globally. The market experiences steady growth driven by the increasing demand for plastics in various end-use sectors such as packaging, construction, automotive, and consumer goods. Additionally, ethylene serves as a precursor for numerous chemical derivatives used in industries including textiles, pharmaceuticals, and detergents. Technological advancements in ethylene production methods, such as steam cracking and ethane extraction from natural gas, enhance process efficiency, yield, and environmental sustainability. Moreover, the market benefits from regional economic development, infrastructure projects, and urbanization trends that drive demand for ethylene-derived products. As industries strive for innovation and sustainability in materials production, the ethylene market remains poised for continued growth, offering opportunities for market participants to capitalize on evolving consumer preferences and industry trends.

The global Ethylene Market Industry is highly competitive with a large number of companies focusing on niche market segments. Amidst intense competitive conditions, Ethylene Market Companies are investing in new product launches and strengthening distribution channels. Key companies operating in the Ethylene Market Industry include- BASF SE, Braskem SA, Chevron Corp, China National Petroleum Corp, Dow Chemical Co., Eastman Chemical Co., Exxon Mobil Corp, Formosa Plastics Group, Huntsman International LLC, Koch Industries Inc, LyondellBasell Industries N.V., Merck KGaA, Mitsubishi Chemical Group Corp, Mitsui Chemicals Inc, NOVA Chemicals Corp, Reliance Industries Ltd, Saudi Basic Industries Corp, Shell plc, Sumitomo Chemical Co. Ltd, TotalEnergies SE

A significant trend in the Ethylene market is the growing demand for biodegradable plastics and sustainable packaging solutions, driven by increasing environmental awareness, regulatory initiatives, and consumer preferences for eco-friendly products. Ethylene is a key building block for the production of various plastics, including polyethylene (PE), which is widely used in packaging applications. As concerns over plastic pollution and waste management intensify, there's a rising interest in developing biodegradable plastics derived from ethylene-based feedstocks, such as bio-based ethylene or ethylene produced from renewable sources. The trend reflects a shift towards sustainable materials and circular economy principles in the packaging industry, driving innovation and investments in ethylene production technologies that support environmental sustainability.

A significant driver propelling the Ethylene market is the growth in construction and infrastructure development projects worldwide, fueled by urbanization, population growth, and economic development. Ethylene is a vital component in the production of polyethylene (PE), which is used in various applications in the construction sector, including pipes, fittings, insulation, and waterproofing membranes. With increasing investments in infrastructure projects, residential and commercial construction, and renovation activities, there's a corresponding demand for ethylene-based materials to meet the needs of the construction industry. The driver underscores the importance of ethylene as a fundamental building block in construction materials and highlights its role in supporting economic growth and urban development globally.

An untapped opportunity in the Ethylene market lies in the expansion into petrochemical value chains and downstream derivatives that offer higher value-added products and applications. Ethylene serves as a feedstock for the production of a wide range of chemical derivatives, including ethylene oxide, ethylene glycol, vinyl acetate monomer (VAM), and polyvinyl chloride (PVC), among others. By diversifying into downstream petrochemicals and specialty chemicals, ethylene producers can capture additional value along the supply chain, mitigate market volatility, and differentiate their product portfolios. Furthermore, downstream derivatives such as ethylene glycol are used in various industries, including automotive, textiles, and personal care, presenting opportunities for market expansion and revenue growth beyond traditional polyethylene applications. By exploring new markets and applications for ethylene derivatives, producers can unlock untapped growth potential and create value-added products tailored to specific customer needs and market demands.

The HDPE (High-Density Polyethylene) segment is the largest in the Ethylene Market by application. HDPE's dominance stems from its versatile use across numerous industries, including packaging, construction, and automotive. Its high strength-to-density ratio makes it ideal for producing durable goods like containers, pipes, and geomembranes. The global demand for sustainable and recyclable materials further boosts HDPE usage, as it is widely recyclable and complies with environmental regulations. Additionally, the growing trend toward lightweight yet robust materials in industrial applications solidifies HDPE's position as the leading segment in the ethylene market.

The Ethane segment is expected to be the fastest-growing in the Ethylene Market by feedstock over the forecast period to 2034. This growth is driven by the increasing availability of ethane due to the expansion of natural gas production, particularly in regions like North America. Ethane is a highly efficient and cost-effective feedstock for ethylene production, offering higher yields compared to alternatives like naphtha. Additionally, the surge in investments in ethane crackers and the preference for cleaner feedstock with lower carbon emissions further accelerate its adoption. The global push toward sustainability and energy efficiency solidifies ethane's position as the fastest-growing segment.

|

Parameter |

Details |

|

Market Size (2024) |

$212.8 Billion |

|

Market Size (2034) |

$374.1 Billion |

|

Market Growth Rate |

5.8% |

|

Segments |

By Feedstock (Naphtha, Ethane, Butane, Propane, Coal), By Application (HDPE, LDPE, Ethylene Oxide, Ethyl Benzene, Others) |

|

Study Period |

2019- 2024 and 2025-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

BOREALIS AG, Braskem SA , Chevron Phillips Chemical Company LLC, China Petroleum & Chemical, Exxon Mobil Corp, INEOS, LyondellBasell Industries Holdings B.V., Reliance Industries Ltd, Royal Dutch Shell plc, SABIC, and Others. |

|

Countries |

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa |

By Feedstock

By Application

Geographical Analysis

*- List not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Ethylene Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Analyzed

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Ethylene Market Size Outlook, $ Million, 2021 to 2030

3.2 Ethylene Market Outlook by Type, $ Million, 2021 to 2030

3.3 Ethylene Market Outlook by Product, $ Million, 2021 to 2030

3.4 Ethylene Market Outlook by Application, $ Million, 2021 to 2030

3.5 Ethylene Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Ethylene Industry

4.2 Key Market Trends in Ethylene Industry

4.3 Potential Opportunities in Ethylene Industry

4.4 Key Challenges in Ethylene Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Ethylene Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Ethylene Market Outlook by Segments

7.1 Ethylene Market Outlook by Segments, $ Million, 2021- 2030

By Feedstock

Naphtha

Ethane

LPG

Others

By Application

LDPE

HDPE

Ethylene oxide

Vinyl

Others

8 North America Ethylene Market Analysis and Outlook To 2030

8.1 Introduction to North America Ethylene Markets in 2024

8.2 North America Ethylene Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Ethylene Market size Outlook by Segments, 2021-2030

By Feedstock

Naphtha

Ethane

LPG

Others

By Application

LDPE

HDPE

Ethylene oxide

Vinyl

Others

9 Europe Ethylene Market Analysis and Outlook To 2030

9.1 Introduction to Europe Ethylene Markets in 2024

9.2 Europe Ethylene Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Ethylene Market Size Outlook by Segments, 2021-2030

By Feedstock

Naphtha

Ethane

LPG

Others

By Application

LDPE

HDPE

Ethylene oxide

Vinyl

Others

10 Asia Pacific Ethylene Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Ethylene Markets in 2024

10.2 Asia Pacific Ethylene Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Ethylene Market size Outlook by Segments, 2021-2030

By Feedstock

Naphtha

Ethane

LPG

Others

By Application

LDPE

HDPE

Ethylene oxide

Vinyl

Others

11 South America Ethylene Market Analysis and Outlook To 2030

11.1 Introduction to South America Ethylene Markets in 2024

11.2 South America Ethylene Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Ethylene Market size Outlook by Segments, 2021-2030

By Feedstock

Naphtha

Ethane

LPG

Others

By Application

LDPE

HDPE

Ethylene oxide

Vinyl

Others

12 Middle East and Africa Ethylene Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Ethylene Markets in 2024

12.2 Middle East and Africa Ethylene Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Ethylene Market size Outlook by Segments, 2021-2030

By Feedstock

Naphtha

Ethane

LPG

Others

By Application

LDPE

HDPE

Ethylene oxide

Vinyl

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

BASF SE

Braskem SA

Chevron Corp

China National Petroleum Corp

Dow Chemical Co.

Eastman Chemical Co.

Exxon Mobil Corp

Formosa Plastics Group

Huntsman International LLC

Koch Industries Inc

LyondellBasell Industries N.V.

Merck KGaA

Mitsubishi Chemical Group Corp

Mitsui Chemicals Inc

NOVA Chemicals Corp

Reliance Industries Ltd

Saudi Basic Industries Corp

Shell plc

Sumitomo Chemical Co. Ltd

TotalEnergies SE

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Feedstock

By Application

Geographical Analysis

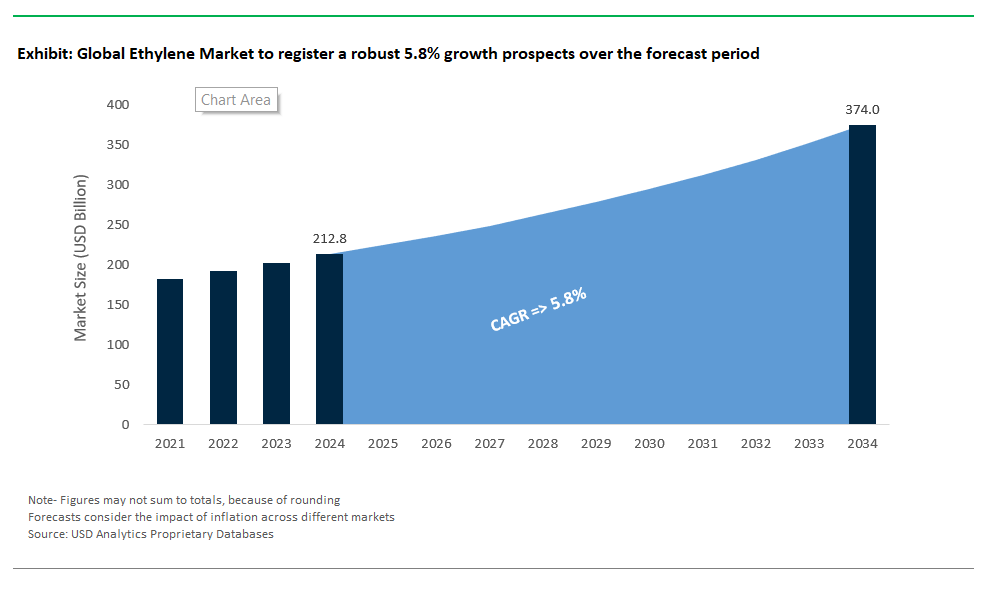

Ethylene Market Size is valued at $212.8 Billion in 2024 and is forecast to register a growth rate (CAGR) of 5.8% to reach $374.1 Billion by 2034.

Emerging Markets across Asia Pacific, Europe, and Americas present robust growth prospects.

BASF SE, Braskem SA, Chevron Corp, China National Petroleum Corp, Dow Chemical Co., Eastman Chemical Co., Exxon Mobil Corp, Formosa Plastics Group, Huntsman International LLC, Koch Industries Inc, LyondellBasell Industries N.V., Merck KGaA, Mitsubishi Chemical Group Corp, Mitsui Chemicals Inc, NOVA Chemicals Corp, Reliance Industries Ltd, Saudi Basic Industries Corp, Shell plc, Sumitomo Chemical Co. Ltd, TotalEnergies SE

Base Year- 2024; Estimated Year- 2025; Historic Period- 2019-2024; Forecast period- 2025 to 2034; Currency: Revenue (USD); Volume