Europe Water Treatment Chemicals Market Outlook

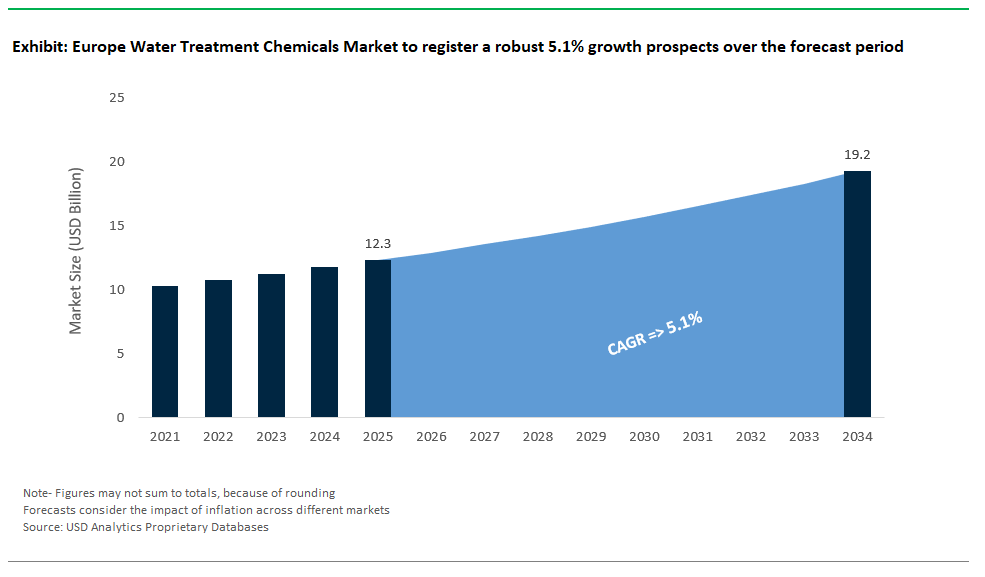

Europe Water Treatment Chemicals Market Size is estimated at $12.3 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 5.1% to reach $19.2 Billion by 2034.

The European water treatment chemicals market is undergoing structural evolution, shaped by comprehensive environmental legislation, climate neutrality targets, and a strong focus on resource efficiency under the EU’s Circular Economy framework. The region’s regulatory leadership through directives such as the EU Drinking Water Directive (Directive (EU) 2020/2184), Urban Waste Water Treatment Directive (UWWTD), and the Water Framework Directive (2000/60/EC) has positioned Europe as a global reference point for advanced, sustainable water treatment practices.

Municipal utilities across Europe continue to rely on established coagulants such as aluminum sulfate and polyaluminum chloride (PACl) to meet the turbidity standard of <0.3 NTU specified in national drinking water quality laws aligned with EN 1302. These coagulants typically generate 1–2 kg/m³ of sludge, with management practices governed by the EU Sewage Sludge Directive (86/278/EEC), which restricts heavy metal concentrations and encourages sludge treatment before reuse in agriculture. Disinfection strategies are progressively incorporating chlorine dioxide (ClO₂) to reduce trihalomethane (THM) formation, particularly in utilities in Germany and the Netherlands, where THM levels must comply with a 100 µg/L limit. Advanced Oxidation Processes (AOPs), such as UV-H₂O₂, are being piloted in drinking water facilities along the Rhine and Meuse rivers for removal of pesticide residues like atrazine and bentazone, achieving >90% degradation efficiency. Orthophosphate dosing is widely adopted to control lead leaching, supporting the EU Drinking Water Directive’s phased reduction of allowable lead concentrations from 10 µg/L to 5 µg/L by 2036. Silicate-based inhibitors are often used in regions with soft water, including parts of Scotland and Scandinavia.

The industrial segment is witnessing a marked shift toward phosphonate-free scale inhibitors such as polyepoxysuccinic acid (PESA) and polyaspartic acid (PASP), both compliant with REACH and EDC (Endocrine Disrupting Chemicals) screening criteria. These alternatives are increasingly preferred for cooling towers and process water systems operating under moderately scaling conditions (LSI <2.0). Corrosion control in closed-loop systems is guided by the Association of German Engineers' standard VDI 2035, which recommends minimizing use of zinc and phosphate. In response, manufacturers now offer zinc-free corrosion inhibitors that deliver corrosion rates below 0.1 mm/year on mild steel, verified through EN ISO 9227 salt spray testing. For microbial control, glutaraldehyde is subject to restrictions under the EU Biocidal Products Regulation (BPR, Regulation (EU) 528/2012), prompting substitution with faster-degrading actives such as DBNPA and THPS. Both are permitted under the BPR with accepted product authorizations for cooling water and paper mill applications due to their lower environmental persistence and breakdown into non-toxic byproducts.

Zero Liquid Discharge & High-TDS Applications: In sectors such as chemical and textile manufacturing, zero liquid discharge (ZLD) systems are increasingly paired with specialty antiscalants such as sulfonated terpolymers to manage high total dissolved solids (TDS) in brine streams exceeding 200,000 ppm. Wet oxidation technologies, including LOPROX® and Zimpro®, are deployed for final polishing, achieving COD reductions to <50 mg/L with specific energy demands ranging between 15 and 25 kWh/m³, depending on influent load.

Nutrient Recovery & Energy Efficiency in Wastewater: Wastewater utilities are integrating resource recovery technologies to align with the EU Green Deal. Struvite precipitation (MgNH₄PO₄·6H₂O) is widely implemented in anaerobic digestate treatment lines for phosphorus recovery, with operational installations in countries like the Netherlands and Denmark. Anammox (anaerobic ammonium oxidation) processes are now part of full-scale deployments in Germany and Austria, reducing nitrogen removal energy consumption by up to 60% compared to conventional nitrification-denitrification processes, as verified in EEA technical reports. Addressing Micropollutants & PFAS: To comply with emerging PFAS thresholds proposed in the revised EU Drinking Water Directive currently under phased national adoption European utilities are trialing hybrid removal solutions combining ion exchange resins with granular activated carbon (GAC), as well as electrocoagulation and plasma-based oxidation methods. Pilot-scale data from utilities in Sweden and Belgium indicate >95% PFAS removal efficiency for legacy compounds such as PFOA and PFOS.

Innovation & Circular Economy Alignment: The European Commission’s Circular Economy Action Plan (2020) promotes sustainable chemistry adoption, driving interest in bio-based water treatment chemicals such as lignosulfonates and tannin-based coagulants. These are under active evaluation in Scandinavian wastewater treatment plants for sludge dewatering and primary clarification. Meanwhile, research centers in the Netherlands and Germany are advancing AI-integrated chemical dosing platforms such as real-time control via Raman spectroscopy and model predictive control algorithms achieving chemical use reductions of 20–30% while maintaining compliance with effluent discharge standards.

Market Trend: PFAS Ban and Circular Economy Drive Next-Gen Chemical Formulations in Europe

Europe’s water treatment chemicals market is being redefined by a confluence of regulatory stringency and circular economy imperatives, notably the EU-wide PFAS ban proposed for 2025 and the revised Industrial Emissions Directive (IED). As power generation, food & beverage, and chemical manufacturing collectively account for 65% of chemical demand, the sector is witnessing a systematic shift toward PFAS-free, biodegradable, and digitally optimized solutions. Industry leaders are rapidly phasing out fluorinated surfactants and foam suppressants, replacing them with siloxane-based alternatives such as Solvay’s Rhodafac® RS-710, while bio-based antiscalants like BASF’s Sokalan® ECO are gaining ground for their ability to reduce Scope 3 emissions by over 50% in thermoelectric facilities. The evolution is not just chemical but digital Veolia’s Hubgrade™ platform, for example, enables real-time phosphate optimization in UK wastewater plants, cutting over 20% of unnecessary dosing. With the Urban Wastewater Treatment Directive (2024) mandating 80% phosphorus removal, and 30% of suppliers soon subject to green chemistry KPI disclosures under EU Taxonomy, water treatment strategies must be fully integrated with decarbonization and transparency goals to remain compliant and competitive.

Market Opportunity: Europe’s €3.1B Green Hydrogen Expansion Spurs Ultra-Pure Water (UPW) Chemical Innovation

The explosive growth of Europe’s green hydrogen sector backed by over €540 billion in planned investments is catalyzing a high-value, specialized demand for ultra-pure water (UPW) treatment chemicals, forecast to exceed €3.1 billion by 2030. As proton exchange membrane (PEM) electrolyzers and ammonia synthesis units scale up across Sweden, the Netherlands, and Germany, the water purity thresholds far exceed conventional standards requiring <0.1 µS/cm conductivity, <10 ppb silica, and non-detect levels of PFAS to prevent catalyst degradation. Nordic projects are already deploying ion exchange + EDI systems using resins and heavy metal polishing to meet sub-ppb discharge targets. Meanwhile, major industrial clusters such as the Antwerp-Rotterdam-Rhine corridor are integrating oxygen scavengers for blue hydrogen pipelines, revealing new niches for specialty chemical suppliers. Companies that align with REACH-compliant, PFAS-free formulations, such as Kemira’s Frankfurt plant offerings, and participate in electrolyzer OEM partnerships (e.g., Dow’s AMBERLITE™ HPR-5000 with Siemens Energy) stand to gain not only premium pricing power but also preferential access to EU Green Deal-linked tax credits and public procurement schemes.

Competitive Dynamics in the European Water Treatment Chemicals Market

The European water treatment chemicals market has a clear structure. Multinational giants, regional specialty firms, and fast-growing disruptors each have their own roles based on product range, technology, and regional strength. The top five multinational companies control more than half of the market. However, competition is rising due to the need for sustainability, regulatory requirements, and digital advancements changing the market.

Tiered Market Structure and Strategic Differentiation

- Tier 1 multinationals, such as BASF, Ecolab (Nalco), Solenis, Kemira, and Suez, hold between 50 and 55% of the market. Their edge comes from proprietary products, established contracts with major industrial clients like Unilever and TotalEnergies, and integrated digital control systems like Ecolab’s 3D TRASAR and Suez’s Aquadvanced. These companies are shifting their focus beyond chemical supply, spending significantly on IoT-driven water quality analytics, biodegradable treatment chemicals, and lifecycle water management to support industrial decarbonization. For example, Kemira leads in municipal coagulants, while BASF is launching the EU’s first fully compliant biodegradable scale inhibitor, Steridrop.

- Tier 2 players, including Brenntag, LANXESS, Veolia Water Technologies, Italmatch Chemicals, and Grupa Azoty, have an estimated market share of 30 to 35%. Their strategy focuses on competitive pricing, regional expertise, and technical skills in specific applications. For instance, LANXESS is a top vendor in ion-exchange and membrane RO chemicals for the chemical and pharmaceutical industries, while Italmatch leads in the phosphonates segment in the Mediterranean’s food and beverage sector. These firms are also early adopters of circular water solutions, emphasizing phosphate recovery and zero-liquid discharge (ZLD), especially in line with EU climate funding and supportive investments.

- Tier 3 emerging disruptors, like Aqualysis (UK), BioWater Tech (Sweden), and Desinfix (Spain), hold a small but rapidly growing market share of 5 to 10%. Their limited scale doesn’t hold them back; their impact is rising due to alignment with European Commission funding programs like Horizon 2020 and Green Deal support. These firms use technologies such as AI-driven chemical dosing (Aqualysis), enzymatic biofilm removers (BioWater), and electrochemical disinfection systems (Desinfix), which are becoming popular in pilot projects for municipal utilities and decentralized industrial sites. Their ability to respond to regulatory pressure to remove persistent chemicals like PFAS and non-biodegradable surfactants makes them significant innovation threats to larger players.

Regional Battlegrounds and Regulatory Impacts

- Geography impacts strategic positioning. In Western Europe, regulatory enforcement under the EU Industrial Emissions Directive benefits incumbents with established compliance systems, such as BASF, Ecolab, and Suez. The Nordic region, led by Kemira and BioWater Tech, is focused on the pulp and paper sector, increasing the demand for sustainable coagulants and biofilm control. Eastern Europe is a price-sensitive area currently undergoing infrastructure upgrades, allowing companies like Brenntag and Grupa Azoty to offer cost-effective coagulants. In Southern Europe, water scarcity influences chemical use, with Italmatch and Veolia succeeding with membrane pretreatment and ZLD technologies designed for the agri-food sector.

Strategic Levers: Innovation, M&A, and Regulation

- Innovation serves as both a key differentiator and a survival tool. Large companies invest in biodegradability and digital control, while smaller firms stand out with next-generation biology or AI. Recent mergers, like Solenis’ acquisition of Sigura (pool chemicals) and the Veolia–Suez merger, have broadened treatment capabilities across industrial and municipal uses, enhancing their technological strengths and market reach. At the same time, regulations are reshaping the market REACH compliance costs and upcoming PFAS bans in 2025 are driving reformulation of chemicals and shifting market power from SMEs to those larger firms that are ready for compliance.

Europe Water Treatment Chemicals Market– Segmentation Insights (2025–2034)

By Type of Chemical: Corrosion Inhibitors Lead, Membrane Cleaners See Fastest Growth

In the European water treatment chemicals market, corrosion and scale inhibitors are projected to hold the largest market share at 28.9% in 2025, driven by widespread aging infrastructure and persistent hard water issues across the region. These inhibitors are particularly vital in industrial sectors such as energy, manufacturing, and district heating, where limescale buildup and corrosion compromise operational efficiency. Utilities and industries alike are increasingly relying on phosphonates and polycarboxylates to enhance asset longevity and meet EU discharge norms.

The membrane cleaning chemicals segment is growing at the fastest pace, with an expected CAGR of 6.7% through 2034, largely attributed to the expansion of reverse osmosis (RO) and nanofiltration (NF) systems in Southern Europe. Regions like Spain and Italy, facing recurring droughts, are scaling up seawater desalination and wastewater reuse projects, intensifying the demand for low-fouling, high-performance membrane cleaners.

Biocides and disinfectants, comprising about 20.8% of the market, are witnessing steady growth due to stringent microbial standards in drinking and industrial water applications. The implementation of the EU Drinking Water Directive (EU) 2020/2184 is catalyzing adoption of advanced oxidizing agents and legionella control chemicals, especially in healthcare, hospitality, and public buildings.

.png)

By Application: Industrial Sector Leads, Desalination Accelerates with Drought Resilience Investments

Industrial water treatment dominates the European market with an estimated 42.9% share in 2025, fueled by strong chemical, food and beverage, and power generation industries. These sectors face complex water chemistry challenges and are embracing chemical-intensive treatment regimens to ensure process stability, reduce downtime, and comply with Zero Liquid Discharge (ZLD) frameworks in regions like Germany and the Netherlands.

Municipal water treatment follows closely, as EU member states invest heavily in advanced disinfection, nutrient removal, and PFAS control. PFAS regulation is becoming a central policy issue in Europe, prompting municipalities to adopt adsorbents, oxidizers, and coagulation agents tailored for persistent chemical contaminants and microplastics.

Meanwhile, desalination applications are growing at the fastest CAGR of 7.3%, propelled by water-stressed Southern European nations such as Spain, Italy, and Greece. These countries are increasing investment in both seawater and brackish water desalination systems to safeguard against prolonged droughts. The rising share of desalination is reinforcing demand for pre-treatment chemicals, membrane antiscalants, and cleaning solutions optimized for high-recovery RO systems.

Europe Water Treatment Chemicals Market Report Scope

Europe Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.3 Billion

|

|

Market Size (2034)

|

$19.2 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Corrosion and Scale Inhibitors, Biocides and Disinfectants, pH Adjusters and Softeners, Oxygen Scavengers, Defoamers and Antifoaming Agents, Membrane Cleaning Chemicals, Other Specialty Chemicals), By Application (Industrial Water Treatment, Municipal Water Treatment, Commercial Water Treatment, Water Desalination), By End-User Industry (Power Generation, Chemical and Petrochemical, Manufacturing, Municipal), By Form of Chemical (Liquid, Powder/Solid

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), BASF SE (Germany), Kemira Oyj (Finland), Solenis LLC (U.S.), Kurita Water Industries Ltd. (Japan), SNF Floerger (France), Veolia Water Technologies (France), Nouryon (The Netherlands), Lonza Group (Switzerland), Solvay S.A. (Belgium), SUEZ S.A. (France), Buckman (U.S.), Italmatch Chemicals S.p.A. (Italy),

|

Europe Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Corrosion and Scale Inhibitors

- Biocides and Disinfectants

- pH Adjusters and Softeners

- Oxygen Scavengers

- Defoamers and Antifoaming Agents

- Membrane Cleaning Chemicals

- Other Specialty Chemicals

By Application

- Industrial Water Treatment

- Cooling Water Treatment

- Boiler Water Treatment

- Process Water Treatment

- Industrial Wastewater Treatment

- Water Reuse and Recycling

- Sludge Treatment

- Municipal Water Treatment

- Drinking Water Treatment

- Municipal Wastewater Treatment

- Commercial Water Treatment

- Water Desalination

By End-User Industry

- Power Generation

- Chemical and Petrochemical

- Manufacturing

- Automotive

- Food and Beverage

- Pharmaceutical

- Pulp and Paper

- Textile

- Mining and Metallurgy

- Electronics and Semiconductors

- Other Industrial Manufacturing

- Municipal

By Form of Chemical

By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Nordic Countries

- Eastern Europe

- Rest of Europe

Top Companies in Europe Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- BASF SE (Germany)

- Kemira Oyj (Finland)

- Solenis LLC (U.S.)

- Kurita Water Industries Ltd. (Japan)

- SNF Floerger (France)

- Veolia Water Technologies (France)

- Nouryon (The Netherlands)

- Lonza Group (Switzerland)

- Solvay S.A. (Belgium)

- SUEZ S.A. (France)

- Buckman (U.S.)

- Italmatch Chemicals S.p.A. (Italy)

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the Europe Water Treatment Chemicals Market, offering comprehensive analysis reviews, breakthrough insights, and a detailed evaluation of competitive dynamics across municipal, industrial, and commercial sectors. It highlights the impact of EU regulations, PFAS bans, and green hydrogen projects on chemical innovation, while examining growth drivers like advanced oxidation, membrane cleaning solutions, and digital water optimization. This report is an essential resource for industry professionals seeking to understand Europe’s evolving water treatment landscape under stringent environmental and circular economy frameworks.

Scope Includes:

- By Type of Chemical: Coagulants & Flocculants, Corrosion & Scale Inhibitors, Biocides & Disinfectants, pH Adjusters & Softeners, Oxygen Scavengers, Defoamers & Antifoaming Agents, Membrane Cleaning Chemicals, Other Specialty Chemicals

- By Application: Industrial Water Treatment (Cooling, Boiler, Process, Wastewater), Water Reuse & Recycling, Sludge Treatment, Municipal Water Treatment (Drinking Water, Wastewater), Commercial Water Treatment, Water Desalination

- By End-User: Power Generation, Chemical & Petrochemical, Manufacturing (Automotive, Food & Beverage, Pharmaceutical, Pulp & Paper, Textile, Electronics), Municipal

- By Form: Liquid, Powder/Solid

- Geographic Scope: Germany, UK, France, Italy, Spain, Netherlands, Nordic Countries, Eastern Europe, Rest of Europe

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

- Companies: Ecolab Inc., BASF SE, Kemira Oyj, Solenis LLC, Kurita Water Industries Ltd., SNF Floerger, Veolia Water Technologies, Nouryon, Lonza Group, Solvay S.A., SUEZ S.A., Buckman, Italmatch Chemicals S.p.A.

Methodology

The research methodology combines top-down and bottom-up modeling, supported by primary interviews with utility operators, chemical manufacturers, and regulators, and secondary data sources such as the European Commission, Eurostat, ECHA, and trade journals. Forecasting applies advanced statistical models, integrating macroeconomic indicators, regulatory impacts, and industry-specific growth levers. Data validation involves triangulation through multiple datasets, while benchmarking against leading market players ensures accuracy. The analysis emphasizes ESG-driven procurement, PFAS-free chemistry trends, and adoption of circular water strategies.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements