Extrusion Coating Market Growth Driven by Recyclable Packaging Innovation, Polyolefin Advancements, and Circular Economy Mandates

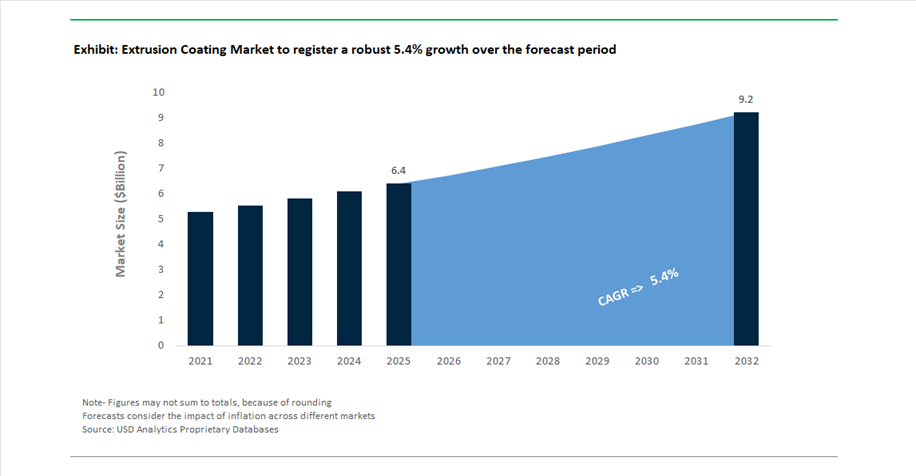

The global Extrusion Coating Market was valued at USD 6.4 billion in 2025 and is projected to grow at a CAGR of 5.4% between 2025 and 2032, reaching USD 9.2 billion by 2032. This growth is being propelled by the increasing demand for high-performance barrier coatings used in flexible packaging, foodservice applications, medical packaging, and industrial laminates. Extrusion coating technology plays a critical role in imparting moisture resistance, oxygen barrier properties, heat sealability, and mechanical strength to substrates such as paper, board, aluminum foil, and polymer films.

A key structural driver is the global shift toward sustainable and recyclable packaging solutions, particularly in response to stringent regulations such as the EU’s Packaging and Packaging Waste Regulation (PPWR). Extrusion coatings are increasingly being engineered to support mono-material packaging structures, enabling recyclability without compromising barrier performance. This has led to the rapid adoption of polyethylene (PE), polypropylene (PP), and specialty copolymers tailored for high-barrier, lightweight, and environmentally compliant packaging applications.

Material innovation is also reshaping the market landscape. The development of mechanically recycled polymers, high-purity resins, and hybrid materials with significant recycled content is enabling manufacturers to meet sustainability targets while maintaining processing efficiency and product performance. Additionally, advancements in multilayer extrusion coating technologies are supporting the production of complex packaging structures with enhanced functional properties for food safety, shelf-life extension, and industrial durability.

Mega Packaging Consolidation, Recycled Polymer Innovation, and Mono-Material Barrier Technologies Transform Market Dynamics

The extrusion coating market is undergoing a structural transformation driven by industry consolidation, circular material innovation, and advanced barrier technology development. A major milestone occurred in February 2026, when Amcor completed its $20 billion merger with Berry Global, forming the world’s largest consumer packaging entity. This consolidation combines Amcor’s expertise in flexible packaging with Berry’s large-scale polyethylene extrusion capabilities, positioning the new entity to lead the transition toward recycle-ready and mono-material packaging solutions.

Sustainability-driven material innovation is accelerating across the value chain. In December 2025, Borealis and Borouge launched the Recleo recycled polymer portfolio, designed specifically for extrusion coating and film applications. These materials enable converters to meet recycled content mandates without compromising barrier performance. Further strengthening this trend, in January 2026, INEOS introduced a hybrid polymer containing 70% recycled content, targeting high-volume industrial packaging applications.

Technological innovation is also advancing mono-material packaging solutions. In March 2025, BOBST, in collaboration with Dow and Michelman, industrialized the oneBARRIER PrimeCycle and FibreCycle platforms. These solutions utilize high-barrier extrusion coatings to maintain recyclability while delivering performance equivalent to traditional multi-layer laminates. Complementing this, in March 2026, H.B. Fuller expanded its Coativ™ barrier coatings portfolio, emphasizing re-pulpability for extrusion-coated paper products.

Capacity expansion and strategic investments are reinforcing supply chain resilience. In March 2026, Mondi completed major capacity expansions under its MAP2030 strategy, with a focus on circular packaging solutions where a majority of revenue now comes from recyclable, reusable, or compostable products. Similarly, in January 2026, Borealis invested €49 million to scale high-performance polypropylene production, targeting specialized extrusion coating applications in medical and technical packaging.

Corporate restructuring is also shaping the competitive landscape. In April 2026, Borouge International was formed through the integration of Borealis, Borouge, and NOVA Chemicals, creating a unified global supplier with a strong focus on circular polyolefin solutions and design-for-recycling initiatives. Additionally, Dow launched its “Transform to Outperform” strategy in January 2026, emphasizing AI-driven production optimization for high-performance ethylene copolymers used in extrusion coating.

Material substitution trends are further expanding application scope. In November 2024, Huhtamaki expanded its fiber-based foodservice products, which utilize thin-layer extrusion coatings to provide barrier functionality, enabling the transition from plastic-heavy packaging to fiber-based alternatives with enhanced performance.

EU PPWR 2024 Enforcement Driving Design-for-Recycling Extrusion Coating Architectures

The enforcement of the European Union’s Packaging and Packaging Waste Regulation (EU) 2024/3901, effective August 2026, is fundamentally restructuring extrusion coating material design, particularly across paperboard packaging and flexible films. The introduction of Design for Recycling performance grades is compelling manufacturers to re-engineer polymer compositions to meet minimum recyclability thresholds. Under the new framework, extrusion-coated packaging must achieve at least 70% recyclability by weight to qualify for Grade C, while premium Grade A compliance requires 95% recyclability, accelerating the transition toward mono-material polyolefin extrusion coatings. This shift is reducing reliance on complex multilayer laminates that hinder recycling streams. The regulation also enforces a strict PFAS ban in food-contact extrusion coatings above 25 ppb, forcing the elimination of fluorinated grease-resistant barriers and driving innovation in alternative coating chemistries such as dispersion coatings and bio-based barriers. Simultaneously, the PPWR’s packaging waste reduction target of 5% by 2030 is encouraging downgauging strategies, where high-performance thin-film extrusion coatings are used to minimize material consumption without compromising barrier performance. The requirement for member states to achieve a 90% separate collection rate for plastic and composite packaging is increasing demand for wash-off primers that enable efficient fiber-polymer separation during recycling. This regulatory ecosystem is accelerating the adoption of recyclable, PFAS-free extrusion coating technologies aligned with circular economy principles and sustainable packaging mandates.

FDA Oversight on PCR Content Elevating Traceability and Food-Safe Extrusion Coating Standards

The U.S. Food and Drug Administration’s intensified scrutiny of post-consumer recycled plastics in extrusion coatings is redefining compliance standards for food-contact packaging applications. In 2026, the FDA’s No Objection Letter process has become the critical validation mechanism for recycling technologies, ensuring that recycled polyethylene and related resins meet stringent safety thresholds. PCR extrusion coatings must undergo surrogate contaminant testing to confirm migration levels below 0.5 ppb, aligning with negligible dietary risk criteria. This requirement is pushing converters to invest in advanced decontamination technologies and closed-loop recycling systems. Additionally, feedstock purity standards mandate that at least 99% of recycled polyethylene used in extrusion coatings originates from food-grade sources, significantly tightening supply chain controls and limiting the use of mixed-waste streams. Digital Product Passports and blockchain-enabled mass balance tracking are becoming standard across the industry, providing verifiable traceability of PCR content in multilayer extrusion-coated structures and supporting compliance audits from major consumer packaged goods companies. The FDA also continues to permit functional barrier strategies, where a virgin polymer layer of 25 to 50 micrometers isolates recycled content, enabling PCR incorporation rates of up to 50% without compromising food safety. These regulatory dynamics are accelerating the development of traceable, high-purity recycled extrusion coatings, enhancing confidence in sustainable packaging solutions across global markets.

Bio-Based Extrusion Coatings Driving Low-Carbon and Compostable Packaging Solutions

The growing emphasis on decarbonization and sustainable packaging is creating strong momentum for bio-based extrusion coatings with high renewable content. Driven by frameworks such as LEED v5 and EN 13432 compostability standards, manufacturers are increasingly adopting plant-derived polymers such as bio-polyethylene, polylactic acid, and polyhydroxyalkanoates for extrusion coating applications. These materials enable a 60% to 80% reduction in cradle-to-gate carbon emissions compared to conventional fossil-based polyethylene coatings, making them highly attractive for environmentally regulated markets. In 2026, bio-based extrusion coatings are targeting a minimum of 50% renewable carbon content, verified through ASTM D6866, to qualify for green building certifications and sustainable procurement criteria. Compostable bio-polyester and PHA coatings are also demonstrating complete biodegradation within 12 weeks under industrial composting conditions, addressing the microplastic concerns associated with traditional plastic-coated paper products. Performance parity with conventional materials is being achieved through advancements in resin engineering, with bio-based coatings delivering heat-seal strengths exceeding 3.0 N per 15 mm at industrial line speeds above 400 meters per minute. These innovations are enabling scalable adoption across food packaging, beverage cups, and flexible packaging formats, positioning bio-based extrusion coatings as a critical growth vector in the transition toward circular and low-carbon packaging systems.

High-Barrier EVOH and Polyamide Extrusion Coatings Enhancing Shelf-Life and Packaging Efficiency

The increasing demand for extended shelf-life in packaged foods, particularly in proteins, dairy, and ready-to-eat segments, is driving the adoption of high-barrier extrusion coating technologies based on ethylene vinyl alcohol and polyamide. EVOH-based coatings provide exceptional oxygen barrier performance, achieving oxygen transmission rates below 0.1 cc per square meter per day, effectively preventing oxidation and preserving product freshness. Polyamide layers complement this functionality by offering strong moisture resistance, puncture durability, and aroma barrier properties, reducing external odor ingress by up to 85%. These materials are typically integrated into co-extrusion structures, where advanced tie-layer resins ensure strong interlayer adhesion between incompatible polymers such as polyethylene and EVOH. The tie-layer resin market has reached a valuation of approximately 1.86 billion in 2026, reflecting its critical role in enabling high-performance multilayer extrusion coatings. In addition to performance enhancements, these high-barrier systems are supporting downgauging initiatives, allowing converters to reduce total coating thickness by up to 30% while maintaining or improving mechanical and barrier properties. This directly aligns with global packaging minimization targets and cost-efficiency objectives. The combination of superior barrier performance, material efficiency, and compatibility with modern extrusion technologies positions EVOH and polyamide coatings as a key opportunity area in the evolving extrusion coating industry.

Extrusion Coating Market Share by Material in 2025: Polyethylene (PE) Dominates Flexible Packaging Applications

Polyethylene (PE) Leadership Driven by Sealability, Cost Efficiency, and High-Volume Packaging Demand

The extrusion coating market by material in 2025 is overwhelmingly dominated by polyethylene (PE), capturing 68.00% market share, owing to its unmatched combination of low cost, superior melt processability, heat sealability, and moisture barrier properties. Specifically, LDPE and LLDPE extrusion coatings are the backbone of the global flexible packaging industry, widely used in liquid packaging board (LPB) and aseptic cartons such as milk cartons and juice boxes. PE coatings (typically 10–30 microns thick) enable hermetic sealing on high-speed form-fill-seal (FFS) machines, protect paperboard from moisture degradation, and ensure FDA-compliant food safety performance. Beyond cartons, PE plays a critical role in flexible packaging laminates, bonding substrates like PET, BOPP, and aluminum foil to create retortable and high-barrier packaging solutions. As the essential sealant layer in multi-layer packaging structures, PE ensures leak-proof integrity and supports innovations like easy-open peelable seals, reinforcing its dominance in food packaging, medical packaging, and industrial wrapping applications.

Extrusion Coating Market Share by Sustainability Category in 2025: Conventional Polyolefins Retain Dominance Amid Recycling Transition

Petroleum-Based Extrusion Coatings Lead with Scale, Cost Efficiency, and Process Reliability

The extrusion coating market by sustainability category in 2025 is dominated by conventional petroleum-based coatings, accounting for 71.00% market share, primarily driven by the entrenched use of LDPE, LLDPE, and polypropylene (PP) derived from large-scale petrochemical infrastructure. These materials offer unmatched cost competitiveness, consistent quality, and high-speed processability, making them indispensable in flexible packaging, industrial wraps, and liquid packaging board applications. With optimized extrusion coating lines operating at speeds exceeding 500 m/min, manufacturers rely on these resins for uniform coating thickness, strong substrate adhesion, and minimal production downtime. The low cost per kilogram of fossil-derived polyolefins remains a decisive factor for high-volume packaging sectors, particularly in commodity food packaging and industrial applications. Their long-standing performance reliability and well-established supply chains ensure that petroleum-based extrusion coatings continue to anchor the market, despite growing regulatory and environmental pressures.

Recyclable Mono-Material Structures Gain Momentum as Sustainable Packaging Innovation Accelerates

While conventional materials dominate volume, recyclable mono-material extrusion coating structures are rapidly emerging as the fastest-growing segment, driven by sustainability mandates, Extended Producer Responsibility (EPR) regulations, and brand-owner commitments to circular packaging solutions. This shift addresses the recyclability limitations of traditional multi-layer laminates (e.g., PET/Aluminum/PE structures), which are difficult to separate and recycle. The industry is transitioning toward all-PE and all-PP mono-material packaging formats, such as MDO-PE/PE laminate structures, which are over 95% polyethylene and fully compatible with mechanical recycling streams. Extrusion coating technology plays a pivotal role by enabling lamination of polyethylene layers and applying heat-sealable coatings to paper substrates, creating repulpable, recyclable packaging solutions. This innovation supports the development of sustainable flexible packaging, recyclable paperboard coatings, and eco-friendly barrier systems, positioning mono-material extrusion coatings as the key growth engine in the evolving global packaging market.

Extrusion Coating Market Competitive Landscape Driven by Circular Polymers, High-Speed Processing, and Sustainable Packaging

The extrusion coating market is highly competitive, led by polymer innovators and integrated packaging leaders focusing on circular economy solutions, high-barrier materials, and advanced extrusion technologies. Competition is shaped by sustainable feedstocks, AI-enabled manufacturing, and growing demand from liquid packaging, healthcare, and e-commerce sectors.

LyondellBasell accelerates extrusion coating innovation through Hyperzone PE and circular feedstock strategy

LyondellBasell is strengthening its position in the extrusion coating industry through its “Vision to Value” strategy, leveraging Hyperzone PE technology to develop HDPE grades with superior stress crack resistance for industrial applications. At Plastindia 2026, the company showcased a comprehensive portfolio targeting infrastructure and healthcare sectors with bio-based and circular polymer solutions. Its leadership in Catalloy technology enables production of high-impact polyolefins widely used in premium packaging and automotive interiors. LYB is advancing its sustainability roadmap by targeting 500,000 tonnes per year of chemically recycled feedstock capacity by late 2026, ensuring a stable supply of green extrusion materials. The company dominates heavy-duty logistics applications with semi-chemical fluting and high-strength extrusion polymers. This integrated approach reinforces its leadership in high-performance extrusion coating resins and circular packaging materials.

Dow Inc. drives high-speed extrusion coating performance with advanced polyethylene and ionomer technologies

Dow Inc. continues to lead innovation in extrusion coating materials with its ELITE™ 5811 polyethylene resin, designed for low neck-in and superior moisture barrier performance in high-speed liquid packaging lines. The company introduced AGILITY™ EC 7000 LDPE, enabling multilayer laminates to maintain seal integrity at ultra-high extrusion speeds, aligning with strong growth in polymer films. Its expansion of the SURLYN™ ionomer portfolio supports mono-material laminates compatible with mechanical recycling, particularly in the fast-growing medical packaging segment. Dow’s BYNEL™ adhesive resins provide critical tie-layer functionality for complex coextrusion structures, especially in retortable food packaging. Leveraging DOWLEX™ solution process technology, the company enables downgauging that reduces material consumption by 15% without compromising performance. This positions Dow at the forefront of sustainable, high-efficiency extrusion coating solutions.

Mondi Group advances recyclable extrusion-coated paper solutions for e-commerce and food packaging

Mondi Group reported a strong EBITDA of €1,001 million in 2025/26, supported by operational integration and restructuring initiatives. The company is optimizing its manufacturing footprint by closing legacy plants and focusing on cost-efficient assets in Central and Eastern Europe. A key innovation includes semi-chemical fluting solutions introduced in April 2026, offering fully recyclable alternatives to plastic-heavy crates in food supply chains. Mondi is a leader in functional barrier papers, utilizing extrusion coating to replace conventional plastic films in e-commerce and dry food packaging. Its strategic focus on flexible packaging expansion and cost optimization supports resilience amid geopolitical challenges. These developments strengthen its role in sustainable extrusion-coated paper packaging and circular material solutions.

Chevron Phillips Chemical enhances extrusion coating performance with metallocene resin technology

Chevron Phillips Chemical (CPChem) is advancing extrusion coating capabilities through its expertise in metallocene-catalyzed resins, which improve toughness, clarity, and performance in BOPP and PET substrates. The company’s leadership in sustainability and innovation was recognized with its executives’ induction into the 2026 CSO Hall of Fame. CPChem’s materials are widely used in agricultural and hygiene films requiring long-term durability and resistance to environmental exposure. In 2026, it optimized its blown and cast film resin portfolio to support near-net-shape extrusion, significantly reducing material waste for industrial packaging customers. The company is also implementing simplified logistics strategies to mitigate rising feedstock and raw material costs. This positions CPChem as a key supplier of high-performance extrusion coating resins for demanding industrial applications.

Borealis pioneers AI-driven extrusion coating and circular polyolefins for sustainable packaging

Borealis is strengthening its market position by integrating advanced AI-based visual inspection systems into extrusion coating production lines, enabling real-time quality control in sterile medical packaging environments. The company is scaling its Borcycle™ circular polyolefins to meet growing demand for sustainable packaging, addressing a key market driver where over 60% of customers prioritize recyclability. Borealis dominates the paperboard lamination segment, which holds dominant market share, providing high-barrier coatings for liquid cartons without reliance on aluminum foil. The company also mitigates polymer price volatility through vertical integration and feedstock hedging strategies. These capabilities position Borealis as a leader in circular extrusion coating materials and advanced lamination technologies.

Smurfit Westrock strengthens vertical integration with plastic-free extrusion-coated board innovation

Smurfit Westrock, formed through a major industry merger, has emerged as a dominant force in extrusion coating with strong share in liquid packaging applications across North America and Europe. The company introduced a 100% plastic-free extrusion-coated board in 2026, utilizing bio-based polymers that deliver moisture barrier performance comparable to LDPE while remaining fully recyclable. Its extensive network of over 500 facilities enables a closed-loop system that collects and reprocesses extrusion-coated waste into new substrates. Smurfit Westrock’s expertise in folding cartons and solid bleached board supports the rapid shift away from single-use plastics in retail packaging. Additionally, the implementation of digital watermarking enhances automated recycling and compliance with EU PPWR regulations. This integrated and sustainable approach solidifies its leadership in next-generation extrusion-coated packaging solutions.

India Extrusion Coatings Market: Regulatory Formalization and FMCG Expansion Driving Rapid Growth

India has emerged as the fastest-growing extrusion coatings market, driven by regulatory enforcement and strong demand from FMCG, packaging, and infrastructure sectors. A key catalyst is the extension of the BIS Quality Control Order (QCO) for polypropylene (PP) materials (effective April 2026), mandating standardized raw materials for all extrusion processes.

Industrial expansion is accelerating capacity. Over 15 new high-speed extrusion coating lines have been commissioned since 2024 to support liquid packaging, dairy laminates, and flexible packaging growth. Government initiatives are also shaping demand—under Biopharma SHAKTI (₹10,000 crore), the need for medical-grade extrusion coatings is rising, while ISM 2.0 is driving production of ESD-safe coated films for semiconductor logistics. Additionally, agriculture is a major driver, with UV-stabilized extrusion-coated woven sacks widely used for fertilizer and grain storage. Textile modernization programs are further expanding applications into technical textiles and geomembranes.

China Extrusion Coatings Market: Graphene Integration and Low-Carbon Transition Driving Scale Leadership

China dominates the global market, accounting for ~60% of Asia-Pacific demand, with a strong pivot toward sustainable and high-performance solutions. Innovation is centered on graphene-enhanced extrusion coatings, which improve oxygen barrier properties by ~30%, extending shelf life for packaged goods.

Regulatory frameworks are driving transformation. Under the 15th Five-Year Plan, policies mandate a 20% reduction in plastic intensity in e-commerce packaging, accelerating adoption of extrusion-coated paper solutions. China also leads in renewable energy applications, producing ~90% of global ETFE-coated PV backsheets. Additionally, semiconductor expansion is driving demand for PTFE-extrusion coated piping, while new standards require ≥15% recycled content in non-food applications by 2026. These factors reinforce China’s global scale advantage.

United States Extrusion Coatings Market: Smart Packaging and Defense Applications Driving High-Value Innovation

The U.S. market is focused on advanced applications and smart packaging technologies, supported by federal programs like the CHIPS Act Phase II. Innovation is accelerating with the launch of sensor-integrated extrusion coatings that monitor temperature and humidity in pharmaceutical logistics.

Defense and high-tech sectors are key drivers. The Department of Defense is funding high-temperature extrusion-coated films (>180°C) for aerospace propulsion systems, while EV growth is boosting demand for metallized polypropylene films used in traction capacitors. Trade policies (Section 232 tariffs) are also encouraging metallized film alternatives to replace aluminum foil in laminates. Additionally, partnerships are promoting low-VOC extrusion coatings for automotive underbody protection, aligning with sustainability goals.

Germany Extrusion Coatings Market: Circular Economy and Mono-Material Innovation Driving Sustainability Leadership

Germany is leading the global transition toward recyclable extrusion-coated materials, driven by strict EU regulations. By 2026, nearly 40% of flexible packaging has shifted to PE-based mono-material laminates, improving recyclability and meeting Cradle-to-Cradle standards.

Regulatory frameworks such as the EU Packaging & Packaging Waste Regulation (PPWR) are mandating repulpable extrusion-coated packaging, especially for food containers. Innovation is also strong in industrial applications, including fluoropolymer extrusion coatings for hydrogen storage tanks to prevent gas permeation. Advanced manufacturing systems using AI-driven optical emission spectroscopy are achieving ±0.5 μm coating precision, while bio-based polymers (e.g., LDPE from renewable sources) are expanding sustainable product offerings. Digital Product Passports (DPP) are also being integrated into coated films for lifecycle tracking.

Japan Extrusion Coatings Market: Ultra-Precision Films and Electronics Integration Driving Advanced Applications

Japan is a global leader in high-precision extrusion coatings, particularly for electronics and advanced materials. The commercialization of sub-500 nm extrusion-coated release films is enabling production of high-capacitance MLCCs used in AI and 5G devices.

Innovation is driven by advanced applications. Japan is pioneering FlexIC-based RFID tags on extrusion-coated films and developing high-refractive-index optical layers for AR/VR systems. The country also dominates supply of high-purity feedstocks (~70% global share) used in advanced coating processes. Additionally, healthcare demand is driving antimicrobial, easy-tear packaging, while architectural applications include ETFE-extrusion coated window films that reduce cooling loads by up to 20%.

Brazil Extrusion Coatings Market: Agribusiness Strength and Sustainable Materials Driving Regional Growth

Brazil is leveraging its agricultural dominance to expand the extrusion coatings market, particularly in packaging and export logistics. Investments are focused on multi-layer extrusion-coated liners for grain storage and shipping, preventing moisture and fungal contamination during transit.

Sustainability is a key differentiator. Companies like Braskem are scaling production of bio-based polyethylene (“I’m green” PE), widely used as a renewable extrusion coating resin. Growth in agrochemicals is also driving demand for chemical-resistant ETFE-coated containers, while infrastructure projects are increasing use of extrusion-coated waterproofing membranes for dams and ports. Additionally, rising demand for ready-to-cook foods (+12% YoY) is boosting production of ovenable and microwaveable coated packaging, reinforcing Brazil’s position as a regional growth leader.

Extrusion Coating Market Report Scope

Extrusion Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.4 Billion

|

|

Market Size (2032)

|

$9.2 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material (Polyethylene, Ethylene Vinyl Acetate, Polypropylene, Polyethylene Terephthalate, Ethylene Butyl Acrylate, Ionomers, Others), By Substrate (Paperboard and Cardboard, Polymer Films, Metal Foils, Woven and Non-woven Fabrics, Others), By End-Use Industry (Food and Beverage, Healthcare and Pharmaceuticals, Personal Care and Cosmetics, Industrial and Chemical, Building and Construction, Automotive, Publishing and Media), By Functional Property (Moisture and Oxygen Barriers, Heat Sealability, Chemical Resistance, Aesthetic, Puncture and Tear Resistance), By Sustainability Category (Conventional Petroleum-based Coatings, Recyclable Mono-material Structures, Bio-based and Compostable Extrusion Coatings)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., LyondellBasell Industries Holdings B.V., ExxonMobil Corporation, SABIC, Borealis AG, Chevron Phillips Chemical Company LLC, DuPont de Nemours, Inc., Westlake Corporation, Eastman Chemical Company, BASF SE, INEOS Group, Celanese Corporation, Arkema S.A., Braskem S.A., The Sherwin-Williams Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Extrusion Coating Market Segmentation

By Material

- Polyethylene

- Ethylene Vinyl Acetate

- Polypropylene

- Polyethylene Terephthalate

- Ethylene Butyl Acrylate

- Ionomers

- Others

By Substrate

- Paperboard and Cardboard

- Polymer Films

- Metal Foils

- Woven and Non-woven Fabrics

- Others

By End-Use Industry

- Food and Beverage

- Healthcare and Pharmaceuticals

- Personal Care and Cosmetics

- Industrial and Chemical

- Building and Construction

- Automotive

- Publishing and Media

By Functional Property

- Moisture and Oxygen Barriers

- Heat Sealability

- Chemical Resistance

- Aesthetic

- Puncture and Tear Resistance

By Sustainability Category

- Conventional Petroleum-based Coatings

- Recyclable Mono-material Structures

- Bio-based and Compostable Extrusion Coatings

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Extrusion Coating Market

- Dow Inc.

- LyondellBasell Industries Holdings B.V.

- ExxonMobil Corporation

- SABIC

- Borealis AG

- Chevron Phillips Chemical Company LLC

- DuPont de Nemours, Inc.

- Westlake Corporation

- Eastman Chemical Company

- BASF SE

- INEOS Group

- Celanese Corporation

- Arkema S.A.

- Braskem S.A.

- The Sherwin-Williams Company

*- List not Exhaustive