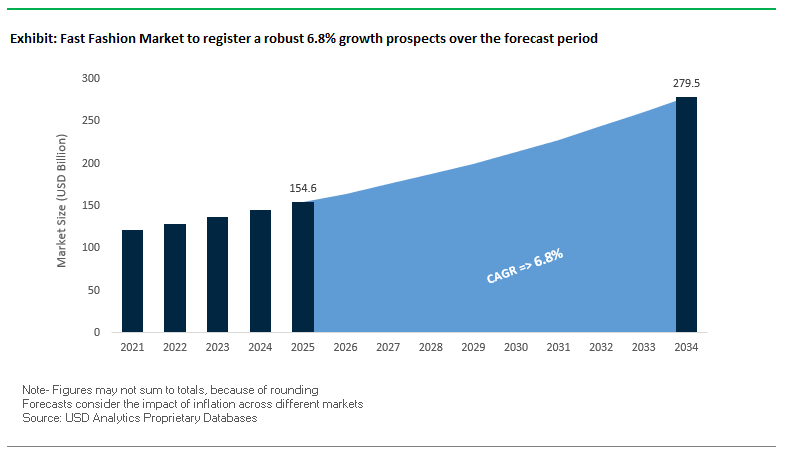

The global fast fashion market is anticipated to reach USD 154.6 billion in 2025 and USD 279.5 billion in 2034, growing at a CAGR of 6.8%. The fast-fashion segment of the apparel market has a quick design-to-retail cycle, low prices, and an ability to capture new fashion trends in real time. Fast-fashion businesses are constantly managing speed-to-market versus sustainability demands, digital retailing innovation, and geographic expansion into high-growth emerging market areas. For experienced industry players, the market offers threats as well as opportunities, namely in supply chain responsiveness, environmental compliance, and competitive brand positioning.

The fast fashion segment remains among the most responsive and nimble apparel markets, and companies are making aggressive strategic moves to build market share and optimize operational effectiveness. In August 2024, Shein partnered with Australian fashion designer Alice McCall to launch the "SHEIN X Alice McCall" collection, a diversification strategy with celebrity-partnered collaborations. The action is in line with Shein's digital-first, on-demand strategy overall, in which small-batch testing and short production runs optimize both trend fit and inventory control.

In November 2024, Primark embarked on a daring U.S. expansion strategy, spending over $90 million on opening new stores in the Southern United States and Midwest, including its Manhattan store launch in Herald Square. It is a long-term gambit to compete in the North American market on its low-cost, high-volume retailing model. Sustainability remained the narrative in 2025's competitive tale, as H&M's March 2025 Sustainability Report reported an 89% adoption rate of sustainable materials and a 41% decline in Scope 1 and 2 emissions compared to 2019 levels.

Regional growth also accelerated in mid-2025, with Shein establishing its first resale store "SHEIN Exchange" in France, Germany, and the UK in June 2025, placing itself in the growing circular fashion economy. Uniqlo, on the other hand, kept its growth focused with a Hue, Vietnam store launch and participation in the "Blue Ocean – Blue Future" sustainability program. Zara's July 2025 digital-led business also showed again how physical store optimization is leading tech-led shopping experiences, with self-checkouts and real-time fitting room booking systems being introduced to enhance consumer interaction.

Artificial intelligence is transforming fast fashion by allowing for the production of micro-collections designed with unprecedented precision to meet the tastes of customers. With AI-powered image recognition and trend detection, fashion brands can browse millions of social media images to forecast demand for particular styles, colors, and fabrics. The technology, Heuritech says, can cut down on inventory waste by as much as 40% by making production very responsive to actual demand. The use of generative AI now allows for the production of tailored styles from scratch, speeding up concept-to-shelf timelines and enabling the release of hyper-relevant fashion. A report by the UNSW Institute for Climate Risk & Response underscores AI's dual effect on market responsiveness and environmental sustainability, as it optimizes supply chains and enables climate-friendly production choices. This renders AI not only a creative tool, but also a strategic tool for profitability and sustainability.

The rental trend is transforming ownership habits, especially among sustainable consumers who are fashion-conscious and environmentally aware. Peer-to-peer rental platforms such as By Rotation are at the forefront, providing access to high-quality, fashion-conscious apparel without purchase permanence. The platform's user base of over 150,000 members proves the scalability of the model, where clothes are worn more often before being disposed of, lengthening product life cycles. Scholarly research proves that the appeal is variety and lower environmental impact, with formal wear headlining rentals and segments such as maternity wear, sportswear, and office wear quickly gaining traction. The confluence of high-speed internet connectivity, frictionless discovery, and reverse logistics optimization has established circular rental platforms as a mainstream trend.

The addition of TikTok Live to fast fashion sales campaigns is building a strong vehicle for real-time conversion driving. By combining entertainment, socializing, and instant purchasing, brands are constructing high-engagement experiences that lead to purchases. Based on a study of Indonesia's Gen Z and Millennial generations, live streaming activities with price reductions and scarcity markers significantly induce impulse purchases. TikTok's ability to build micro-trends means that fashion seen on live streams can go viral within hours, and this directly affects brand inventory planning. With 39% of Gen Z having admitted to purchasing items after seeing them on TikTok, the platform is now a high-impact trend adoption and sales driver.

Growing focus on the environmental and labor performance of fast fashion is driving brands towards verifiable compliance with ethical production standards. Governments are also turning up the heat of regulation, such as the UK's Environment Act of 2021, which has extended producer responsibility and promotes sustainable production. Brands that invest in "green" certified factories that meet environmental, safety, and labor standards are becoming transparency and ethical responsibility leaders. This approach not only minimizes regulatory and reputational risk but builds consumer trust in markets where purchasing decisions are increasingly driven by brand ethics.

Tops dominate the fast fashion market in 2025 with a 30% market share with repeat buying at short intervals and rapid style turnover via trends such as cropped silhouettes and oversized fits. Dresses, particularly casual and mini dresses, are the quickest-growing category, driven by social media fashion hauls and influencer marketing. Bottomwear with a 25% market share has consistent demand, with sustainable denim innovation such as H&M's "Conscious" line appealing to environmentally conscious consumers. Outerwear, such as light jackets and hoodies, is assisted by climate-adaptive designs, while skirts especially minis are seeing a comeback via the Y2K revival. The "Others" category, including activewear and loungewear, continues to expand as hybrid work-from-home lifestyles drive demand for comfort-led versatile pieces.

Polyester is firmly entrenched with a strong 45% of the fast fashion market share because it is cheap, versatile, and has a short production cycle. Nevertheless, the material is increasingly under fire for microplastic pollution, and companies are launching recycled polyester lines like Shein's "Eco Collection," which takes up 20% of the polyester category. Cotton is holding steady at 30%, prized for its breathability, while organic cotton is gaining traction as companies react to the trend towards sustainability. Viscose, being hyped as a semi-synthetic material, is gaining usage because it is softer than polyester and cheaper than cotton. The "Others" segment, comprised of linen, Tencel, and blends, is seeing strong growth Tencel's biodegradability has propelled year-over-year adoption gains, particularly among eco-conscious consumers looking for premium yet sustainable fashion offerings.

.png)

Fast fashion is characterized by a core set of multinational leaders dominating fast design cycling, supply chain expertise, and international brand recognition. The leaders are reshaping the industry with innovation, sustainability, and growth strategy. The major players are Inditex (Zara, Pull&Bear, Bershka), H&M, Shein, Uniqlo, Primark, Forever 21, Urban Outfitters, Topshop, ASOS, C&A, Boohoo Group (Boohoo, PrettyLittleThing), Fashion Nova, Mango, Revolve, Missguided, Others.

Zara shook up the rhythm of retail with its just-in-time manufacturing model, condensing the design-to-store process to weeks. It has shrunk its store network by 22.5% since 2020, channeling investment into large-format flagship stores with RFID-based inventory tracking and AI-driven personalization technology. Its forays into cosmetics, footwear, and sportswear take it into yet more consumers.

H&M's approach is 100% recycled or sustainable materials via circular business models by 2030. It has opened resale stores in 26 markets worldwide and made significant investments in Sellpy, a second-hand online platform. It also improves the in-store shopping experience with additional services like beauty studios and in-store Click & Collect points.

Shein's data-driven manufacturing system allows it to test thousands of new styles in small batches, keeping waste to a minimum and responsiveness to trends to a maximum. Under its SHEIN X scheme, it has collaborated with over 5,300 designers, paying out $12 million in designer commissions since 2021. Sustainability initiatives involve 76% renewable energy usage and R&D collaborations to encourage textile-to-textile recycling.

Uniqlo establishes itself on its "LifeWear" concept, providing quality, functional basics instead of pursuing fleeting fashions. Its proprietary materials, HEATTECH and AIRism, make it a textile innovation leader. It expands strategically, with flagship stores like GU NY SOHO and targeted market entrances in Southeast Asia.

The United States fast fashion market is being reshaped by the integration of AI-driven forecasting and advanced analytics to better predict consumer demand, streamline inventory management, and reduce overproduction risks. This technology-first approach is enabling brands to respond more precisely to rapidly changing trends while lowering operational waste. Supply chain agility is another competitive edge, with companies investing in real-time tracking systems and just-in-time manufacturing to ensure swift adaptation to emerging styles. Social media platforms like TikTok and Instagram are playing an outsized role in accelerating trends, with influencer-led campaigns creating instant demand.

Consumer sentiment is shifting toward sustainability and ethics, fueling a surge in second-hand, vintage, and upcycled clothing platforms such as ThredUp and Depop. Brands are responding with transparency initiatives, including the use of recycled materials and energy-efficient manufacturing processes. This balance of trend responsiveness and sustainability positioning is defining the competitive landscape, pushing U.S. fast fashion brands to embrace technology without losing sight of environmental responsibility.

China remains the epicenter of global fast fashion manufacturing, supported by highly connected supply chain clusters in regions like the Pearl River Delta. These hubs enable quick turnaround through close proximity to factories, ports, and airports. E-commerce leaders such as Shein are setting new speed standards by relying heavily on international air freight, even at premium costs, to fulfill overseas orders in record time. Chinese fast fashion companies are increasingly adopting AI-based demand forecasting and advanced production optimization, integrating “Consumer Orientation” principles into every stage of the process.

Government investment in infrastructure and high-tech industries continues to enhance manufacturing efficiency, although the sector faces mounting criticism for its environmental and labor practices. The rapid pace of ultra-fast fashion often outstrips regulatory oversight, highlighting the growing need for stronger environmental laws and labor protections. China’s ability to innovate while addressing these challenges will determine its long-term market leadership.

Italy’s fast fashion sector operates within a unique environment where traditional high fashion meets rapid production cycles. The "Made in Italy" designation is central to maintaining craftsmanship standards, with government and industry stakeholders ensuring that substantial product transformation occurs domestically. The market is increasingly polarized, catering to both luxury buyers and fast fashion consumers, forcing brands to strategically navigate dual market demands.

In alignment with EU directives, Italy is enforcing eco-design standards and banning the destruction of unsold goods. Regulatory scrutiny is intensifying, particularly against greenwashing, with recent fines issued to foreign brands for misleading sustainability claims. This regulatory framework is pushing domestic and international players operating in Italy to prioritize genuine environmental compliance and transparent supply chain practices.

France is pioneering regulatory measures to curb the environmental impact of fast fashion through its new “Anti-Fast Fashion” law. This legislation introduces an eco-score labeling system that rates garment sustainability, enabling consumers to make informed purchases and compelling brands to improve production standards. Durability-based fees starting at €5 per low-scoring item and potentially increasing to €10 by 2030 are designed to discourage low-quality, short-lifespan products.

A landmark aspect of the law is its advertising ban for non-durable textiles, extending to influencer promotions on social media. This directly challenges one of fast fashion’s most potent marketing channels. The move positions France as a model for environmental governance in the apparel industry and is likely to influence similar legislative actions across Europe.

Spain’s fast fashion industry is anchored by Inditex’s pioneering agile supply chain model, which blends in-house control over capital-intensive operations with outsourcing for labor-heavy production tasks. This structure enables rapid design-to-shelf turnaround, maintaining Spain’s reputation as a fast fashion innovator. The government is also funding circular economy projects like the ECOFAP initiative, which transforms tanned leather waste into materials for 3D printing in footwear and apparel, addressing industrial waste challenges.

The sector is undergoing a digital and green transformation, with the national Observatory coordinating efforts between industry players and public institutions. Funding from the EU’s Next Generation Funds is accelerating this transition, ensuring that Spanish brands remain globally competitive while advancing sustainability goals.

Brazil is the fifth-largest clothing producer in the world, with growth primarily driven by its domestic consumer base. The expanding middle class, backed by rising incomes, is fueling demand for affordable, trend-focused apparel. Major retail chains like Renner and Riachuelo are investing in rapid design adaptation and localized production to capitalize on emerging styles quickly.

Labor transparency is gaining prominence through initiatives like Moda Livre, a platform that tracks working conditions in brand supply chains. This is a direct response to past labor exploitation concerns, signaling an industry shift toward more ethical practices. Brazil’s combination of domestic demand strength, growing ethical oversight, and fast production cycles positions it as an increasingly influential player in the global fast fashion landscape.

|

Parameter |

Details |

|

Market Size (2025) |

$154.6 Billion |

|

Market Size (2034) |

$279.5 Billion |

|

Market Growth Rate |

6.8% |

|

Segments |

By Product (Outerwear, Bottomwear, Tops, Dresses, Skirts, Others), By Gender (Men, Women, Children), By Distribution Channel (Online Stores, Hypermarkets/Supermarkets, Specialty Stores, Others), By Material (Polyester, Cotton, Viscose, Others), By End-User (Adults, Teens, Kids) |

|

Study Period |

2019- 2024 and 2025-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

Inditex (Zara, Pull&Bear, Bershka), H&M, Shein, Uniqlo, Primark, Forever 21, Urban Outfitters, Topshop, ASOS, C&A, Boohoo Group (Boohoo, PrettyLittleThing), Fashion Nova, Mango, Revolve, Missguided, Others. |

|

Countries |

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa |

* List Not Exhaustive

This report investigates the global fast fashion market in comprehensive detail, delivering strategic breakthroughs, analysis reviews, and highlights that equip apparel industry stakeholders with actionable intelligence. Prepared by USDAnalytics, it examines the interplay of rapid design-to-retail cycles, sustainability imperatives, digital-first retail strategies, and evolving consumer behaviors across mature and emerging economies. This report is an essential resource for executives, investors, supply chain managers, and sustainability officers seeking a clear view of market growth dynamics from 2025 to 2034. By integrating competitive intelligence, regional expansion trends, and innovation-driven opportunities, it provides decision-makers with the insight needed to strengthen market positioning and respond to both regulatory and consumer demands. Scope includes-

The research methodology for this fast fashion market report employs a dual-track approach combining primary and secondary research to ensure precision and relevance. Primary research involved structured interviews with brand executives, supply chain specialists, technology providers, sustainability advocates, and retail analysts to capture first-hand perspectives on market shifts. Secondary research included an in-depth review of industry databases, fashion retail reports, government trade data, sustainability disclosures, and financial filings. Quantitative data modeling applied forecasting techniques and scenario analysis to predict market performance across segments and geographies. To maintain data integrity, findings underwent triangulation across independent sources, ensuring that the final insights are credible, actionable, and aligned with the needs of industry professionals navigating the competitive and fast-evolving apparel sector.

Table of Contents: Fast Fashion Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Fast Fashion Market Landscape & Outlook (2025–2034)

2.1. Introduction to the Fast Fashion Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $154.6 Billion

2.2.2. Forecasted Market Size and CAGR (2034): $279.5 Billion at 6.8% CAGR

2.3. Strategic Acquisitions and Brand Collaborations

2.3.1. Shein’s Collaboration with Australian Designer Alice McCall (August 2024)

2.4. Global Expansion and Retail Transformation

2.4.1. Primark’s Ambitious U.S. Expansion with over $90M Investment (November 2024)

2.4.2. Uniqlo’s Strategic Expansion into Vietnam (Mid-2025)

2.4.3. Shein’s Resale Platform “SHEIN Exchange” Expands to Europe (June 2025)

2.5. Sustainability and Digital Advancements

2.5.1. H&M’s March 2025 Sustainability Report (89% Sustainable Materials)

2.5.2. Zara’s July 2025 Digital-First Strategy with Tech-Enabled Stores

3. Breakthrough Innovations and Strategic Opportunities in the Fast Fashion Market

3.1. Trend: AI-Generated Hyper-Targeted Collections

3.1.1. AI for Demand Prediction and Inventory Optimization

3.1.2. Generative AI for Accelerated Design-to-Shelf Timelines

3.1.3. AI's Dual Impact on Market Agility and Sustainability

3.2. Trend: Circular Rental Platforms Driving Sustainable Consumption

3.2.1. Peer-to-Peer Rental Platforms (e.g., By Rotation)

3.2.2. Extending Product Life Cycles and Reducing Environmental Footprint

3.3. Opportunity: TikTok Live Instant Shopping for Accelerated Impulse Purchases

3.3.1. Blending Entertainment and Instant Purchasing

3.3.2. Driving Real-Time Conversions and Micro-Trend Virality

3.4. Opportunity: Regulatory-Compliant Factories as a Competitive Differentiator

3.4.1. Heightened Scrutiny and New Regulations (e.g., UK's Environment Act)

3.4.2. Building Consumer Trust through Transparency and Ethical Manufacturing

4. Competitive Landscape: Fast Fashion Market

4.1. Overview of Market Dynamics and Drivers

4.2. Inditex (Zara, Pull&Bear, Bershka)

4.2.1. Pioneer of Agile Supply Chains and Just-in-Time Production

4.2.2. Store Network Rationalization and Tech-Enabled Flagships

4.3. H&M Group

4.3.1. Sustainability-Centric Circular Business Model and 2030 Goals

4.3.2. Expansion of Resale Operations and Enhanced In-Store Services

4.4. Shein Group

4.4.1. Digital-First, On-Demand Retail Disruptor

4.4.2. Data-Driven Manufacturing and SHEIN X Designer Program

4.5. Fast Retailing Co., Ltd. (Uniqlo)

4.5.1. Function-Driven “LifeWear” Philosophy and Proprietary Materials

4.5.2. Targeted Market Expansion and Sustainability Campaigns

4.6. Other Key Players

5. Market Share and Segmentation Insights: Fast Fashion Market

5.1. By Product

5.1.1. Tops: Largest Market Share (30% in 2025)

5.1.2. Dresses: Fastest-Growing Segment

5.1.3. Bottomwear

5.1.4. Skirts

5.1.5. Outerwear

5.1.6. Others

5.2. By Material

5.2.1. Polyester: Largest Market Share (45% in 2025)

5.2.2. Cotton

5.2.3. Viscose

5.2.4. Others (Linen, Tencel, Blended Fabrics)

5.3. By Gender

5.3.1. Men

5.3.2. Women

5.3.3. Children

5.4. By Distribution Channel

5.4.1. Online Stores

5.4.2. Hypermarkets/Supermarkets

5.4.3. Specialty Stores

5.4.4. Others

5.5. By End-User

5.5.1. Adults

5.5.2. Teens

5.5.3. Kids

6. Country Analysis and Outlook of Fast Fashion Market

6.1. United States: AI-Powered Forecasting and Sustainability-Driven Consumer Shift

6.2. China: Global Supply Chain Dominance and Ultra-Fast Fashion Innovation

6.3. Italy: Balancing ‘Made in Italy’ Heritage with Fast Fashion Regulation

6.4. France: Legislative Action Against Ultra-Fast Fashion

6.5. Spain: Agile Supply Chains and Government-Backed Sustainability Programs

6.6. Brazil: Domestic Market Growth and Labor Transparency

6.7. Canada: Technological Integration and Consumer-Centric Strategies

6.8. Mexico: Rising Consumer Demand and E-commerce Expansion

6.9. Germany: Demand for Sustainable and High-Quality Products

6.10. UK: Shifting Consumer Preferences and Evolving Retail

6.11. Russia: E-commerce Growth and Increasing Disposable Incomes

6.12. Japan: Focus on Comfort, Craftsmanship, and Evolving Trends

6.13. South Korea: Sustainability and Technology Adoption

6.14. Australia: Growth in Luxury and Sustainable Footwear

6.15. India: Aspirational Buyers and Cultural Influences

6.16. South East Asia

6.17. Rest of Asia

6.18. Argentina

6.19. Rest of South America

6.20. Saudi Arabia: Luxury Spending and Fashion-Conscious Consumers

6.21. UAE: Tourism-Driven Retail and Luxury Fashion Hub

6.22. Rest of Middle East

6.23. South Africa: Expanding Affluent Class and Urbanization

6.24. Egypt: Rising Urbanization and Western Fashion Influence

6.25. Rest of Africa

7. Fast Fashion Market Size Outlook by Region (2025–2034)

7.1. North America Fast Fashion Market Size Outlook to 2034

7.1.1. By Product

7.1.2. By Gender

7.1.3. By Distribution Channel

7.1.4. By Material

7.1.5. By End-User

7.2. Europe Fast Fashion Market Size Outlook to 2034

7.2.1. By Product

7.2.2. By Gender

7.2.3. By Distribution Channel

7.2.4. By Material

7.2.5. By End-User

7.3. Asia Pacific Fast Fashion Market Size Outlook to 2034

7.3.1. By Product

7.3.2. By Gender

7.3.3. By Distribution Channel

7.3.4. By Material

7.3.5. By End-User

7.4. South America Fast Fashion Market Size Outlook to 2034

7.4.1. By Product

7.4.2. By Gender

7.4.3. By Distribution Channel

7.4.4. By Material

7.4.5. By End-User

7.5. Middle East and Africa Fast Fashion Market Size Outlook to 2034

7.5.1. By Product

7.5.2. By Gender

7.5.3. By Distribution Channel

7.5.4. By Material

7.5.5. By End-User

8. Company Profiles: Leading Players in Fast Fashion Market

8.1. Inditex (Zara, Pull&Bear, Bershka)

8.2. H&M

8.3. Shein

8.4. Uniqlo

8.5. Primark

8.6. Forever 21

8.7. Urban Outfitters

8.8. Topshop

8.9. ASOS

8.10. C&A

8.11. Boohoo Group (Boohoo, PrettyLittleThing)

8.12. Fashion Nova

8.13. Mango

8.14. Revolve

8.15. Missguided

8.16. (List Not Exhaustive)

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Growth is fueled by rapid design-to-retail cycles, global expansion into emerging markets, and the integration of AI-driven forecasting to align production with real-time consumer demand. Digital-first retail strategies, social media-driven trend adoption, and aggressive price positioning are also critical growth enablers.

Sustainability is becoming a competitive differentiator, with brands increasing the use of recycled fabrics, organic cotton, and biodegradable materials. Regulatory pressures in Europe and consumer demand for eco-friendly apparel are accelerating investment in green-certified factories and circular economy models such as resale and rental platforms.

Asia Pacific, the Middle East, and Latin America offer the strongest growth potential due to rising disposable incomes, expanding retail infrastructure, and a young, trend-conscious population. Markets like China, India, Brazil, and the Gulf states are especially attractive for international brands.

AI enables hyper-targeted micro-collections, reducing design-to-shelf timelines by predicting consumer preferences with high accuracy. By leveraging trend analysis from social media, brands can minimize inventory waste and align production with actual demand, significantly boosting efficiency and responsiveness.

Key players include Inditex (Zara, Pull&Bear, Bershka), H&M, Shein, Uniqlo, Primark, Forever 21, Boohoo Group, ASOS, Mango, and Fashion Nova. These companies excel in supply chain agility, digital-first marketing, and balancing fast trend turnover with evolving sustainability mandates.