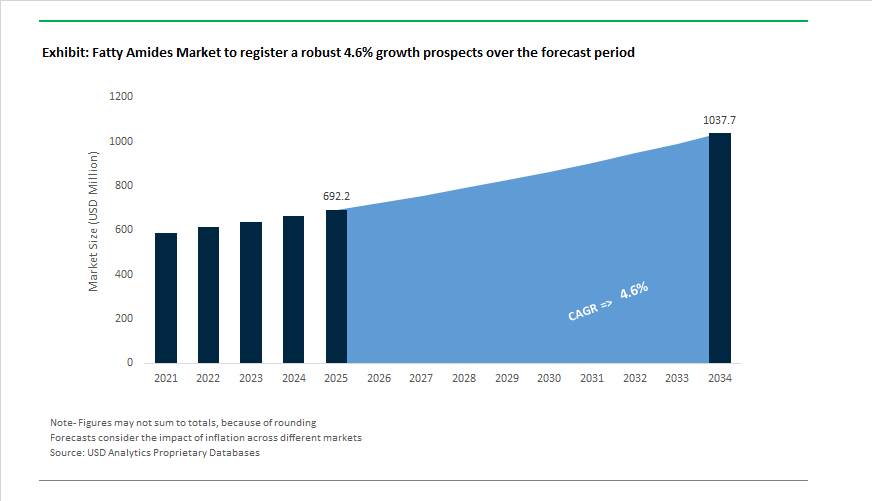

Fatty Amides Market to Reach $1,037.6 Million by 2034 from $692.2 Million in 2025 at 4.6% CAGR Backed by Polymer Additives, Bio-Based Precursors and High-Performance Surface Modifiers

The global Fatty Amides Market is projected to expand from $692.2 Million in 2025 to $1,037.6 Million by 2034, progressing at a CAGR of 4.6%. Market growth is supported by sustained demand for slip agents, anti-block additives, mold release agents, anti-fog agents, and friction modifiers used across polymer processing, food packaging films, automotive components, agricultural films, personal care formulations, and specialty construction materials. Increasing regulatory scrutiny on hazardous additives in plastics, expansion of bio-based feedstock routes, and reshoring of polymer manufacturing capacity in North America and Asia are reshaping supply chains for erucamide, oleamide, stearamide, behenamide, and specialty fatty amide derivatives.

In January 2026, Valtris Specialty Chemicals launched an enterprise-wide transformation initiative aimed at positioning itself as a preferred supplier of sustainable additives. The program includes consolidation of business units and intensified service delivery for specialty fatty amide and ester portfolios targeting renewable energy infrastructure and advanced construction materials through 2026. In November 2025, Croda International entered a strategic partnership with Amino GmbH to expand its high-purity ingredient portfolio for the biopharma sector. The collaboration leverages Croda’s specialty amide technology for stabilizers and shear protectants in cell culture media. In September 2025, Valtris confirmed participation at K 2025 in Düsseldorf, presenting low-TPP and bio-based amide solutions aligned with upcoming 2026 EU regulations restricting hazardous additives in consumer plastics. In January 2025, Kao Corporation’s Sustainability Report highlighted a 24% increase in sales of environmentally advanced products, driven by a pivot toward high-performance surfactants and amides derived from low-solubility natural raw materials, supporting its carbon-zero manufacturing target for 2040.

Capacity expansion and feedstock innovation defined 2024. In November 2024, BASF partnered with Acies Bio to advance fermentation-based production of fatty alcohols from methanol, establishing a sustainable precursor route for downstream fatty amide synthesis used in detergents and conditioners. In October 2024, Fine Organic Industries signed a lease agreement with the Jawaharlal Nehru Port Authority to establish a new SEZ manufacturing unit in Maharashtra, enhancing export capacity for specialty amides serving food packaging and cosmetic markets. In late 2024, Fine Organics restored operations at its Badlapur, Maharashtra facility after disruptions earlier in the year, stabilizing supply of food-grade and polymer-grade fatty amides to South Asia and Europe. Throughout 2024, KLK OLEO integrated Temix Oleo’s European operations, combining upstream palm-based oleochemical strength with specialty amide expertise for automotive and lubricant applications. In June 2024, PMC Biogenix announced expansion of its Armoslip facility in Gyeongju, South Korea, increasing high-purity fatty amide capacity by 50% with new volumes expected by mid-2026, while simultaneously investing in its Memphis, Tennessee facility to expand U.S. production of metal stearates and fatty amides aligned with North American polymer reshoring trends. During 2024–2025, Evonik divested non-core polyester and polyolefin businesses under its Tailor Made program, reallocating capital toward high-performance additives where fatty amide derivatives contribute to surface modification, dispersion control, and friction reduction in specialty polymers.

Trends and Opportunities in the Fatty Amides Market

Transition to Specialized Bis-Amides for High-Output Polymer Extrusion

- As global packaging volumes rise and extrusion lines operate at higher throughputs, traditional mono-amides such as oleamide are increasingly insufficient. Polymer processors are moving toward specialized bis-amides, particularly Ethylene Bis-Stearamide (EBS), to achieve consistent lubrication, reduced die buildup, and thermal stability under demanding processing conditions.

- In 2025, technical disclosures from Kao Corporation highlighted a clear industry shift toward high-purity fatty amides engineered for controlled surface migration. According to Kao’s Integrated Report 2025, processors using optimized bis-amide formulations achieved up to a 12% reduction in extrusion torque on high-speed cast film lines, translating directly into lower energy consumption and improved line stability. This is a critical advantage in multilayer film structures, where inconsistent slip behavior can disrupt downstream printing, lamination, and bag-making operations.

- The focus has moved decisively toward interfacial performance. Modern fatty amides are designed to bloom to the polymer surface at predictable rates, ensuring stable coefficients of friction across the entire conversion chain. This precision is increasingly essential for the global flexible packaging industry, where downtime or surface defects carry significant financial penalties.

- Sustainability is now inseparable from performance. In late 2025, Croda International confirmed its transition to 100% RSPO-certified fatty amides. This move aligns lubricant additives used in food-contact plastics with the EU Deforestation Regulation, which became a decisive procurement criterion in 2025.

Integration of Alkylamidoamines in Precision Agriculture Adjuvants

- Fatty amides are also gaining strategic importance in agrochemical formulations as regulators tighten controls on spray drift, runoff, and environmental exposure. Alkylamidoamines, particularly cocoamidoamines, are being adopted as multifunctional adjuvants that enhance deposition, penetration, and rainfastness while supporting lower application rates.

- In April 2025, the U.S. Environmental Protection Agency finalized its Insecticide Strategy, formally incentivizing the use of drift-reducing adjuvants. Fatty amides have emerged as preferred deposition aids because they increase droplet mass and reduce fine spray particles, allowing growers to earn mitigation credits required for pesticide use near sensitive ecosystems.

- Bio-based innovation is reinforcing this trend. In October 2025, Nouryon reported strong market uptake of its coco-amidoamine-based Adsee® C80W surfactant. The product is positioned as a readily biodegradable alternative to tallow amines, delivering improved humectancy and rainfastness in herbicide and fungicide tank mixes. Independent studies conducted between 2024 and 2025 demonstrated that amidoamine-based adjuvants can increase active ingredient uptake by up to 20%, enabling lower dosage rates and directly supporting the EU Farm to Fork objective of reducing pesticide use by 50% by 2030.

High-Performance Corrosion Inhibitors for Green Hydrogen and CCUS Infrastructure

- A major opportunity for fatty amides is emerging in corrosion protection for carbon capture, utilization, and storage (CCUS) systems and green hydrogen infrastructure. These environments expose steel assets to aggressive conditions, including wet CO₂, acidic streams, and hydrogen-induced degradation.

- In November 2025, peer-reviewed research demonstrated that waste-oil-derived fatty amides can achieve corrosion inhibition efficiencies of up to 88.5% on carbon steel exposed to acidified environments typical of CCUS operations. These amides form persistent molecular films that protect pipelines, storage tanks, and absorber units carrying amine-rich capture fluids, significantly extending asset life.

- The scale of opportunity is expanding rapidly. As the U.S. Department of Energy and the EU Hydrogen Bank accelerate electrolyzer deployment, fatty amides are being engineered into advanced heterocyclic inhibitors such as imidazolines. These formulations are critical for mitigating hydrogen embrittlement and pitting corrosion in high-pressure electrolyzer components, a challenge that previously lacked standardized chemical solutions.

- Circular economy models are strengthening the value proposition. By 2025, commercial proof-of-concept projects demonstrated the synthesis of corrosion-inhibiting amides from waste cooking oil, reducing the carbon intensity of industrial inhibitors by nearly 60% compared to petroleum-derived alternatives. This positions fatty amides as both performance-critical and sustainability-aligned solutions for next-generation energy infrastructure.

Fatty Amides as Phase Change Materials for Battery Thermal Management

- The electrification of transport and energy storage is opening a high-technology application for fatty amides as organic Phase Change Materials (PCMs). Primary amides such as stearamide and behenamide exhibit sharp melting points between 30°C and 70°C and high latent heat of fusion, making them well suited for managing heat in batteries and power electronics.

- Research published in August 2025 confirmed that fatty amides outperform paraffin waxes in long-term thermal stability while offering non-toxicity and bio-based sourcing advantages. These attributes are increasingly attractive for electric vehicle battery packs, where thermal runaway prevention and cycle life extension are critical design objectives.

- By December 2025, pilot-scale projects demonstrated that encapsulating fatty amides with graphene or boron nitride can significantly enhance thermal conductivity while maintaining electrical insulation. This composite PCM approach is being evaluated by major EV battery designers to stabilize cell temperatures during ultra-fast charging, with early results indicating potential battery lifespan improvements of 15% to 20%.

- Beyond mobility, fatty amide PCMs are also gaining traction in pharmaceutical cold-chain monitoring. In late 2025, chipless temperature sensors incorporating coconut-oil-derived amides demonstrated reliable, irreversible detection of temperature excursions, supporting the safe global transport of temperature-sensitive biologics.

Fatty Amides Market Share and Segmentation Insights

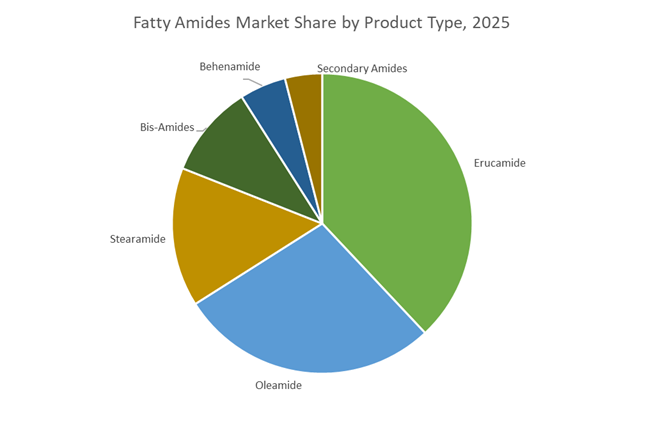

Erucamide Dominates Slip Additive Demand Across Polyolefin Film Applications

Erucamide holds 38% of fatty amides market share in 2025, driven by its superior migration behavior and ability to rapidly reduce coefficient of friction in polyethylene and polypropylene films. This makes it the preferred slip agent for food packaging, shrink wrap, and industrial films where clarity, machinability, and extrusion stability are critical. Oleamide represents a significant secondary segment, favored for faster surface migration and low-temperature performance in flexible films, inks, and mold release systems. Stearamide maintains importance in higher-temperature plastic and rubber processing due to its thermal stability. Bis-amides are gaining share as internal lubricants and dispersants in engineering plastics and masterbatches, offering longer-lasting performance. Behenamide serves high-temperature specialty films, while secondary amides address niche requirements in corrosion inhibition, pigment dispersion, and select personal care formulations.

Plastics and Polymers Drive Core Demand Supported by Packaging and Automotive Growth

Plastics and polymers account for 42% of global fatty amides consumption in 2025, reinforcing their role as essential slip agents, anti-block additives, and lubricants in extrusion, injection molding, and film production. Packaging forms a substantial secondary segment, where fatty amides enable smooth film handling and high-speed converting in flexible food and industrial packaging. Inks and coatings utilize fatty amides to enhance slip, mar resistance, and flow in printing inks and overprint varnishes. Rubber applications remain steady through mold release and processing aid usage in tires and industrial goods. Automotive demand is expanding as fatty amides improve surface feel and processing of interior plastics, wire coatings, and rubber components. Personal care remains niche but strategic, incorporating selected amides as opacifiers and viscosity modifiers in hair and skin formulations aligned with mild, compatible ingredient systems.

Competitive Landscape of the Fatty Amides Market

The global Fatty Amides Market is shaped by specialty additive leaders competing on slip performance, anti-block efficiency, bio-based traceability, and high-purity formulations for packaging films, engineering plastics, inks, and coatings, with sustainability credentials and regional manufacturing footprint now decisive for long-term contracts.

Croda International Plc drives premium fatty amides with blockchain traceability and European capacity expansion

Croda International Plc leads the specialty fatty amides market with around 14% global share in 2026, supported by manufacturing hubs in Hull (UK), Gouda (Netherlands), and Mianyang (China). Its Crodamide™ and Incroslip™ portfolios, including erucamides and oleamides, deliver superior slip and anti-block performance in LLDPE and LDPE packaging films. In early 2026, Croda finalized a multi-year investment to expand Hull capacity, targeting rising European demand for high-end polymer additives. Strategically, the company is rolling out blockchain-based traceability, enabling customers to verify 100% bio-based origin, reinforcing Croda’s Sustainability-as-a-Service positioning across global FMCG and packaging value chains.

Fine Organic Industries Ltd. scales green fatty amides through export-led growth and specialty blends

Fine Organic Industries Ltd. is India’s largest oleochemical additive producer and a major force in green chemistry, generating roughly 55 to 60% of revenue from exports in 2026. In February 2026, the company unveiled a global expansion strategy, including a new 30-acre JNPA SEZ site in India and a 160-acre acquisition in South Carolina, USA, to localize manufacturing. With over five decades of emulsifier expertise, Fine Organics produces fatty amides that also function as high-efficiency pigment dispersants for inks and coatings. Its strategic pivot toward high-value specialty blends aims to stabilize margins amid volatile feedstock prices.

PMC Biogenix advances custom fatty amides for engineering plastics and closures

PMC Biogenix, part of PMC Group, is a pioneer in fatty amide technology across North America and South Korea. Its Kemamide® and Armoslip® brands are industry benchmarks for primary and secondary amides used for lubricity and mold release. By 2026, PMC fully integrated its Center for Renewable Chemistry in Memphis, focusing on amides with thermal stability above 250°C for engineering plastics. With full in-house control over chain length and acid value, PMC enables rapid custom formulation for niche applications. The company also leads the caps and closures segment, where Kemamide® S reduces opening torque in bottle caps.

Kao Corporation targets low-migration fatty amides for electronics and high-precision packaging

Kao Corporation is strengthening its position in high-purity fatty amides under its Global Sharp Top strategy, prioritizing segments where it holds technological leadership. During 2025 to 2026, Kao introduced a low-migration amide that mitigates blooming issues that disrupt printing and lamination. In 2026, the company deployed AI-enabled supply chain controls to maintain the stringent purity standards demanded by Japanese and South Korean electronics manufacturers. Kao’s ESG credentials further differentiate its portfolio, with its sixth consecutive Carbon Footprint for Organization certification achieved in early 2026, supporting growing demand from European and US sustainability-focused B2B clients.

Valtris Specialty Chemicals accelerates bio-based fatty amides through global manufacturing and soy chemistry

Valtris Specialty Chemicals is reshaping its specialty additives platform in 2026 following a CEO-led transformation to streamline operations and improve order fulfillment. Its Santicizer® portfolio and tailored fatty amide blends are being promoted globally, including at PLASTINDIA 2026, with emphasis on bio-derived lubricants and plasticizers. Valtris also secured Ohio Soy Council funding in 2026 to scale soy-based chemistries feeding directly into green amide R&D. With nine manufacturing sites across North America, Europe, and Asia, Valtris positions itself as a supplier of choice for polymer compounders requiring consistent regional supply and fast innovation cycles.

United States: Onshoring Momentum and Regulatory Pull for Bio-Based Fatty Amides

The United States fatty amides market is undergoing a structural reset driven by onshoring investments, trade realignment, and regulatory preference for low-toxicity additives. In August 2025, Kao Corporation inaugurated a 20,000-ton-per-year tertiary amine and derivatives facility in Pasadena, Texas. This plant deploys proprietary process technology to secure local supply of amine-based additives for plastics and personal care applications, while materially reducing logistics-related CO2 emissions for North American customers. The commissioning underscores a broader trend of multinational suppliers shifting capacity closer to downstream converters to improve supply reliability and regulatory responsiveness.

Parallel to this, Fine Organic Industries announced the acquisition of 159.9 acres in South Carolina in July 2025 to establish its first U.S. manufacturing base. The facility is designed to produce bio-based slip additives such as erucamide and oleamide, directly addressing demand from the rapidly expanding U.S. flexible packaging sector. Trade policy has amplified this localization push. Following executive actions in April 2025, the U.S. implemented a 10% baseline reciprocal tariff on chemical imports, with sharply higher rates on Chinese-origin specialty additives. This has driven domestic masterbatch producers to prioritize U.S.-manufactured fatty amides to offset a 40–50% escalation in intermediate costs. On the demand side, USDA Certified Biobased Product labeling awarded in late 2024 accelerated adoption of fatty amides in agricultural films and compostable packaging during 2025. Looking ahead, updated Environmental Protection Agency SNAP guidelines effective January 2026 are accelerating the replacement of phthalate-based lubricants with fatty amides in medical-grade polymer tubing.

India: Export-Oriented Capacity Build-Up Under Policy Protection

India is positioning itself as a global export hub for high-purity fatty amides, supported by regulatory protection and incentive-led capacity expansion. In April 2025, the Ministry of Environment, Forest and Climate Change granted environmental clearance to Fine Organic Industries for a large greenfield project at the JNPA SEZ in Maharashtra. The facility is engineered to scale production of high-purity erucamide for international markets, strengthening India’s role in global slip additive supply chains.

Policy instruments are reinforcing domestic manufacturing economics. In the Union Budget 2025–26, the government considered raising customs duties on imported plastic additives to 10% to counter low-cost Chinese inflows, directly incentivizing Make in India oleochemical initiatives. In parallel, the Production-Linked Incentive scheme for specialty chemicals was extended in 2025 to firms localizing secondary amide synthesis for advanced automotive engineering plastics. Beyond polymers, application diversification is emerging. Under the BioE3 Policy, Indian manufacturers are innovating with stearamide and behenamide as non-toxic anti-caking agents in granulated fertilizers, signaling a gradual expansion of fatty amides into agri-input formulations aligned with sustainability mandates.

China: Feedstock Supremacy and Environmental Compliance Pressures

China’s fatty amides market continues to benefit from unmatched upstream scale while simultaneously adapting to tighter environmental controls. By 2025, China’s ethylene production capacity exceeded 62 million metric tons, providing a structurally low-cost feedstock base for nitrogenous intermediates required in fatty amide synthesis. This feedstock advantage underpins China’s competitiveness in large-volume products such as ethylene bis-stearamide.

In April 2025, Wanhua Chemical achieved full commercial operation of its Phase II ethylene complex. The project secures localized supply of ethylene and ammonia precursors, enabling world-scale EBS production integrated within domestic petrochemical clusters. However, regulatory pressure is reshaping product specifications. Stricter VOC emission caps enforced in the Pearl River Delta from January 2026 are pushing downstream industries, particularly printing inks, toward high-purity, low-odor fatty amides. This shift is favoring producers capable of advanced purification and odor-control technologies over legacy batch operators.

Germany and the European Union: Low-Carbon Compliance and Cosmetic-Grade Purity

In Europe, the fatty amides market is being reshaped by regulatory tightening and carbon-footprint disclosure requirements. Manufacturers are actively upgrading purification units to comply with the 2026 REACH recast, which imposes stricter limits on trace impurities in amides used for cosmetic emollients and food-contact plastics. These requirements are raising technical barriers to entry and increasing the value of high-purity production capabilities.

At the same time, sustainability-driven differentiation is accelerating. In October 2025, BASF launched a new line of bio-attributed fatty amides in Germany using its Mass Balance approach. This allows automotive OEMs and plastics converters to source additives with a demonstrably lower carbon footprint, directly supporting net-zero roadmaps targeting 2030. As a result, the European fatty amides landscape is shifting toward fewer, more technologically advanced suppliers aligned with regulatory and sustainability benchmarks.

Strategic Snapshot: Fatty Amides Market by Country (2025–2026)

Fatty Amides Market County Level Snapshot

|

Country / Region

|

Core Strategic Driver

|

Key Applications

|

Market Implication

|

|

United States

|

Onshoring, tariffs, SNAP regulations

|

Packaging, medical tubing, agri-films

|

Strong pull for domestic bio-based fatty amides

|

|

India

|

PLI incentives and duty protection

|

Slip additives, fertilizers, auto plastics

|

Export-oriented capacity and application diversification

|

|

China

|

Feedstock scale and VOC compliance

|

EBS, inks, polymer processing aids

|

Shift toward higher-purity, low-odor grades

|

|

Germany / EU

|

REACH recast and decarbonization

|

Cosmetics, food-contact plastics, automotive

|

Premiumization and consolidation around compliant suppliers

|

Fatty Amides Market Report Scope

Fatty Amides Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$692.2 Million

|

|

Market Size (2034)

|

$1037.6 Million

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Product Type (Erucamide, Oleamide, Stearamide, Behenamide, Secondary Amides, Bis-Amides), By Form (Beads or Prills, Powder, Fine Powder, Pellets), By Function (Slip Agents, Anti-Blocking Agents, Release Agents, Dispersants, Lubricants, Anti-Static Agents), By End-Use Industry (Plastics and Polymers, Packaging, Inks and Coatings, Rubber, Personal Care, Automotive)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Croda International Plc, Kao Corporation, Fine Organic Industries Limited, PMC Biogenix, Inc., BASF SE, Evonik Industries AG, Italmatch Chemicals S.p.A., Nippon Fine Chemical Co., Ltd., KLK Oleo, China Petroleum & Chemical Corporation, Valtris Specialty Chemicals, Lonza Group, Mitsubishi Chemical Group, Palsgaard A/S, Wanhua Chemical Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fatty Amides Market Segmentation

By Product Type

- Erucamide

- Oleamide

- Stearamide

- Behenamide

- Secondary Amides

- Bis-Amides

By Form

- Beads or Prills

- Powder

- Fine Powder

- Pellets

By Function

- Slip Agents

- Anti-Blocking Agents

- Release Agents

- Dispersants

- Lubricants

- Anti-Static Agents

By End-Use Industry

- Plastics and Polymers

- Packaging

- Inks and Coatings

- Rubber

- Personal Care

- Automotive

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Fatty Amides Industry

- Croda International Plc

- Kao Corporation

- Fine Organic Industries Limited

- PMC Biogenix, Inc.

- BASF SE

- Evonik Industries AG

- Italmatch Chemicals S.p.A.

- Nippon Fine Chemical Co., Ltd.

- KLK Oleo

- China Petroleum & Chemical Corporation

- Valtris Specialty Chemicals

- Lonza Group

- Mitsubishi Chemical Group

- Palsgaard A/S

- Wanhua Chemical Group

*- List not Exhaustive