Fire Protection Coatings Market Growth Driven by Intumescent Innovation, Infrastructure Safety Mandates, and Low-VOC PFP Systems

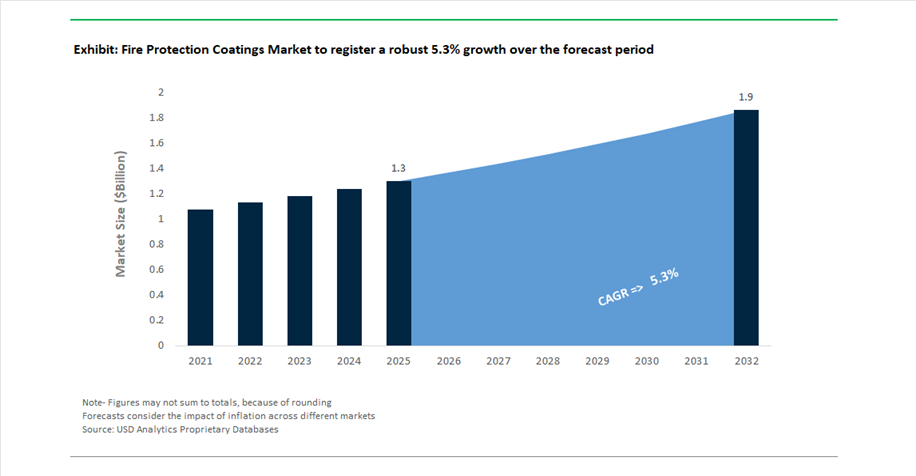

The global Fire Protection Coatings Market was valued at USD 1.3 billion in 2025 and is projected to grow at a CAGR of 5.3% between 2025 and 2032, reaching USD 1.9 billion by 2032. This steady expansion is driven by increasing regulatory emphasis on fire safety compliance, structural protection, and building resilience across commercial construction, infrastructure, energy, and industrial sectors.

Fire protection coatings—particularly intumescent and epoxy passive fire protection (PFP) systems—are critical in safeguarding structural steel by forming an insulating char layer when exposed to high temperatures. This delays structural failure, providing crucial evacuation time and protecting assets. A key growth driver is the surge in infrastructure development, including airports, metro systems, commercial buildings, and energy installations, where stringent fire safety codes are mandatory.

The market is also benefiting from the shift toward advanced waterborne and solvent-free PFP technologies, driven by environmental regulations and sustainability goals. Manufacturers are focusing on low-VOC, heavy-metal-free, and high-efficiency coatings that reduce application thickness, minimize emissions, and improve installation efficiency. Additionally, the integration of aesthetic compatibility with fire protection systems is gaining traction, particularly in modern architectural designs where exposed steel structures require both performance and visual appeal.

Low-VOC Intumescent Systems, Hybrid Epoxy PFP Innovation, and Infrastructure-Led Expansion Reshape Market Dynamics

The fire protection coatings market is undergoing a transformation driven by product innovation, sustainability initiatives, and strategic capacity expansion. In February 2026, PPG Industries launched STEELGUARD 652, a water-based intumescent coating designed for interior structural steel. This product offers up to two hours of fire resistance and supports low-VOC construction practices, enabling “trade stacking” and aligning with green building certifications such as LEED.

High-performance epoxy-based PFP systems are also advancing rapidly. In March 2025, Hempel introduced Hempafire Extreme 550, a solvent-free epoxy coating providing up to four hours of fire resistance while reducing application thickness by up to 40%. This innovation significantly lowers carbon footprint and accelerates project timelines, particularly in large-scale infrastructure projects. Complementing this, in November 2025, Jotun launched hybrid epoxy PFP coatings with enhanced resistance to saline and chemical environments, addressing durability requirements in offshore platforms and coastal industrial facilities.

Collaborative innovation is improving formulation efficiency. In August 2024, Hexion partnered with Clariant to develop advanced water-based intumescent systems, reducing application complexity while maintaining high fire resistance performance. Sustainability is also becoming a key differentiator, with PPG Industries achieving an AAA ESG rating in October 2024, highlighting its leadership in low-VOC and heavy-metal-free fire protection coatings.

Strategic regional expansion is strengthening market penetration. In January 2026, Sherwin-Williams expanded its footprint in Latin America through the integration of Suvinil, enabling localized production of its Firetex® intumescent coatings. Meanwhile, in February 2026, Kansai Paint restructured its Indian operations to focus on performance coatings, including fire-retardant systems, to support the country’s infrastructure growth.

Innovation is also extending into design integration. In March 2026, AkzoNobel introduced color-coordinated intumescent coatings, allowing architects to achieve both fire protection and aesthetic requirements without additional finishing layers, reducing material usage by up to 15%.

Epoxy Intumescent Coatings Replacing Cementitious Fireproofing in Steel Structures

The fire protection coatings market is undergoing a structural transition as epoxy intumescent coatings increasingly displace traditional cementitious spray-applied fire-resistive materials in high-rise and industrial steel construction. This shift is driven by the superior performance characteristics of epoxy-based passive fire protection systems, particularly in hydrocarbon fire scenarios. Epoxy intumescent coatings are uniquely capable of achieving UL 1709 rapid-rise fire ratings, making them essential for infrastructure located near fuel-intensive environments such as transport hubs and petrochemical facilities. Unlike cementitious materials, which are prone to moisture absorption, modern epoxy systems provide inherent resistance to water ingress, effectively mitigating corrosion under insulation and enhancing long-term structural durability. Adhesion performance is also significantly improved, with epoxy coatings achieving pull-off strengths exceeding 3,000 psi, ensuring coating integrity under mechanical stress and vibration. In contrast, cementitious systems often rely on weaker mechanical bonding, increasing the risk of cracking and delamination over time. Additionally, the adoption of shop-applied intumescent coatings is improving project efficiency, with pre-coated steel reducing on-site application time by up to 40% and eliminating weather-related curing delays. These advantages are driving widespread adoption of thin-film and thick-film epoxy intumescent coatings as a high-performance, durable, and application-efficient solution in modern fire protection systems.

Aerospace Fire Safety Regulations Driving Adoption of Advanced Fire-Resistant Coatings for Composite Structures

The evolution of aerospace engineering toward lightweight composite airframes is prompting stricter regulatory oversight on fire safety, leading to increased adoption of advanced fire-resistant coatings. New airworthiness directives introduced by aviation authorities in 2026 are mandating enhanced fire propagation resistance for interior cabin linings and fuselage components. These regulations are driving the use of fluoropolymer-modified fire-retardant coatings that offer improved thermal stability while minimizing toxic emissions during combustion. Modern aerospace intumescent coatings are engineered to provide up to 15 minutes of burn-through protection while maintaining significantly lower weight compared to traditional insulation materials, contributing to reduced aircraft operating empty weight and improved fuel efficiency. Additionally, these coatings address structural durability challenges by offering flexibility that accommodates repeated pressurization cycles, reducing the risk of cracking in composite fuselage components. Enhanced inspection requirements for fuselage structures are also encouraging the use of coatings that combine fire resistance with mechanical resilience, ensuring long-term compliance with evolving safety standards. These developments are positioning advanced fire-resistant coatings as a critical material solution in next-generation aircraft design and maintenance strategies.

California Wildfire Regulations Driving Demand for Exterior Fire-Resistant Coatings

The tightening of wildfire resilience regulations in California is creating a substantial growth opportunity for exterior fire protection coatings designed for combustible substrates. Updates to Title 24, Chapter 7A in 2026 have established stringent requirements for ignition-resistant construction in high-risk wildfire zones, mandating that exposed wood surfaces be treated with certified fire-resistant coatings or replaced with non-combustible materials. This regulatory framework is driving increased adoption of Class A fire-rated exterior coatings across residential and multifamily construction. Retrofit activity is also accelerating, as existing buildings undergoing major renovations are now required to comply with updated fire safety standards, significantly expanding the addressable market beyond new construction. In addition to regulatory compliance, insurance incentives are playing a key role in market growth, with property owners able to secure premium reductions of 10% to 15% by implementing approved fire-resistant coating systems. For manufacturers, achieving certification such as CAL FIRE Building Materials Listing has become essential for market entry, particularly as wood-frame construction continues to expand under density bonus programs. These dynamics are reinforcing the role of fire-resistant coatings as a critical component of wildfire mitigation strategies in high-risk regions.

UK Building Safety Act Driving Retrofitting Demand for Intumescent Fire Protection Coatings

The enforcement of the United Kingdom’s Building Safety Act 2022, along with the upcoming Building Safety Levy, is generating significant demand for retrofitting fire protection coatings in residential buildings. The legislation targets the remediation of unsafe cladding and inadequate structural fire protection in mid- and high-rise buildings, creating a large-scale market for passive fire protection solutions. The government aims to raise approximately £3.4 billion over the next decade to fund remediation activities, with intumescent coatings emerging as a preferred solution due to their thin-film application and compatibility with existing structures. Regulatory enforcement is intensifying, with building safety regulators requiring rapid submission of safety case reports, often within 28 days, prompting urgent retrofitting of exposed steel frameworks. Additionally, updated safety standards for buildings exceeding 18 meters in height, including requirements for multiple escape staircases, are increasing the need for high-performance fireproofing solutions in confined spaces where traditional cementitious coatings are impractical. The integration of fire protection upgrades with broader energy retrofit programs, supported by funding mechanisms such as the Social Housing Decarbonisation Fund, is further expanding market opportunities. These regulatory and financial drivers are positioning intumescent fire protection coatings as a critical solution in ensuring compliance, safety, and long-term resilience in the built environment.

Fire Protection Coatings Market Share 2025: Structural Steel and Retrofit Demand Fuel Growth

Substrate Insights: Structural Steel Dominates with Intumescent Fire Protection Demand

The structural steel segment leads the fire protection coatings market with a dominant 52% market share in 2025, driven by stringent fire safety regulations in modern infrastructure. Steel structures begin to lose their load-bearing strength at approximately 500°C, making intumescent fire protection coatings essential for high-rise buildings, stadiums, airports, and industrial facilities. These advanced coatings expand under extreme heat, forming an insulating char layer that delays structural failure and enhances evacuation safety. Additionally, the increasing adoption of off-site prefabrication and modular construction is boosting demand, as steel components are coated in controlled environments to ensure uniform dry film thickness and consistent quality. This process not only reduces on-site labor but also accelerates construction timelines. With rising investments in commercial infrastructure and stricter compliance with passive fire protection standards, structural steel applications will continue to anchor market growth.

Sales Channel Insights: Maintenance and Retrofitting Drive Long-Term Market Expansion

The maintenance and retrofitting segment accounts for the largest 58% share in the fire protection coatings market in 2025, reflecting growing demand for upgrading existing infrastructure to meet evolving fire safety codes. Many older buildings constructed before the 2010s lack adequate passive fire protection systems, creating significant opportunities for intumescent coating retrofits as a cost-effective alternative to structural modifications. Additionally, post-construction inspections and compliance requirements are driving recurring demand for recoating and repairs, especially in commercial buildings, industrial plants, and energy facilities. Fireproof coatings often degrade due to water exposure, mechanical damage, or system modifications such as cable tray installations, necessitating regular maintenance cycles. This consistent need for inspection-driven upgrades ensures a steady revenue stream for coating manufacturers and service providers. As global safety regulations tighten and infrastructure ages, maintenance and retrofitting will remain a key growth engine in the fire protection coatings market.

Fire Protection Coatings Market Competitive Landscape Driven by Intumescent Technologies, Infrastructure Safety, and Sustainable Fireproofing

The fire protection coatings market is highly competitive, driven by intumescent coatings innovation, stringent fire safety regulations, and demand from infrastructure, energy, and industrial sectors. Key players are focusing on low-VOC formulations, extended fire resistance ratings, and digital monitoring solutions to enhance structural fireproofing performance.

PPG Industries leads fire protection coatings innovation with Steelguard® intumescent systems

PPG Industries is advancing the fire protection coatings market through the launch of PPG STEELGUARD® 652, a waterborne intumescent coating delivering up to two hours of UL 263-certified fire resistance for structural steel. The product’s low-VOC formulation enables “trade-stacking,” allowing simultaneous construction activities and reducing project timelines by 15%. PPG’s cellulosic passive fire protection coatings offer 20-year durability with strong adhesion and impact resistance, ensuring long-term structural safety. Following its portfolio optimization, the company is focusing on high-margin industrial and aerospace fireproofing applications. With 44% of revenue derived from sustainably advantaged products, PPG continues to lead in green building compliance. Its innovation strategy strengthens its position in high-performance fire-resistant coatings.

AkzoNobel strengthens fire protection coatings leadership through Interchar® innovation and Axalta merger

AkzoNobel is reinforcing its position in the fire protection coatings market through its Interchar® range, supported by the ongoing merger with Axalta, expected to generate $600 million in cost synergies and enhance global scale. The company achieved a 14.2% EBITDA margin, driven by operational efficiency and pricing discipline. Its integration of aesthetic color technologies into fire protection coatings addresses the growing demand for exposed steel structures in modern architecture. AkzoNobel has also reduced its carbon footprint by 47% compared to 2018 levels, aligning with sustainability goals. Its expertise in powder coatings is expanding into next-generation applications such as EV battery enclosures and data centers. These capabilities position the company at the forefront of sustainable fire protection technologies.

Hempel sets new fire protection standards with Hempafire Extreme epoxy PFP coatings

Hempel A/S is driving innovation in the fire protection coatings market with Hempafire Extreme 550, offering up to four hours of fire resistance for cellulosic fire scenarios in high-rise buildings. The system reduces paint consumption by up to 40%, improving application efficiency and enabling faster project completion. The company reported strong financial performance with €259 million free cash flow and an 18.2% EBITDA margin, supported by growth in protective and marine coatings. Its “Accelerate to Win” strategy focuses on maintaining high margins through technical differentiation. Hempel is also targeting a 90% reduction in Scope 1 and 2 emissions by 2026, positioning itself as a low-carbon leader. These advancements reinforce its leadership in high-performance passive fire protection coatings.

Jotun expands fire protection coatings portfolio with Jotachar systems for extreme environments

Jotun A/S continues to strengthen its presence in the fire protection coatings market through its Jotachar range, including the newly introduced Jotachar 1709 XT designed for hydrocarbon fire scenarios and extreme offshore conditions. The company reported record sales in its Protective Coatings segment, driven by demand in offshore wind and oil and gas industries. Its coatings are widely used in C5-M marine environments, offering long-term durability and minimal maintenance requirements. Jotun is enhancing its digital capabilities through the AssetKeeper platform, enabling real-time monitoring of coating performance across global assets. Third-party certifications from DNV and Lloyd’s Register ensure compliance with stringent safety standards. This combination of durability, certification, and digital integration strengthens its competitive position.

Sherwin-Williams drives fire protection coatings growth with FIRETEX® systems and infrastructure focus

The Sherwin-Williams Company is expanding its fire protection coatings portfolio through its FIRETEX® brand, widely adopted in commercial and institutional construction. Its FIRETEX® FX7002 remains a leading solvent-based acrylic coating, while Heat-Flex® AEB addresses corrosion under insulation in refinery and industrial applications. The company has gained industry recognition through major awards for water infrastructure and tank storage projects. Its extensive distribution network enables rapid delivery of fire protection coatings to large-scale construction sites. Sherwin-Williams is also expanding standardized solutions for pharmaceutical cleanrooms and semiconductor facilities. With projected earnings of $11.50 to $11.90 per share in 2026, the company maintains strong financial and operational positioning.

Sika strengthens fire protection coatings market with Unitherm® systems and integrated building solutions

Sika AG is positioning itself as a system specialist in the fire protection coatings market through its Unitherm® product line, including the high-performance Platinum-120 epoxy intumescent coating. The company leverages its acquisitions to strengthen its presence in cementitious fireproofing solutions for tunnels and infrastructure projects. Sika is expanding rapidly in the Asia-Pacific region, where stricter building codes are driving demand for fire safety coatings. Its integrated approach combines fire protection with sealing and bonding technologies to provide comprehensive building safety systems. The company’s coatings offer high-build capability and fast curing, improving application efficiency. These capabilities enhance Sika’s competitiveness in both structural steel and infrastructure fire protection applications.

China Fire Protection Coatings Market: Regulatory Codification and BIM Integration Driving Scale Leadership

China is the largest and most structured market for fire protection coatings, driven by strict building codes aligned with the Dual-Carbon strategy. A major transformation is the integration of BIM (Building Information Modeling) workflows, which automatically calculate required intumescent coating thickness (DFT) based on structural fire engineering parameters.

Regulatory enforcement is intensifying. New rules mandate that steel-framed buildings above 250 meters must use Class-A intumescent coatings with ≥3-hour fire resistance, while VOC regulations are driving a ~60% shift toward water-based fireproof coatings. Innovation is also advancing through hybrid coatings combining corrosion resistance (C5-M) with fire protection, particularly for offshore wind infrastructure. Additionally, QR-code-based digital compliance systems are improving traceability and regulatory audits, reinforcing China’s leadership in both scale and digital integration.

United States Fire Protection Coatings Market: Infrastructure Refurbishment and Advanced Epoxy Systems Driving Growth

The United States market is evolving through infrastructure modernization and regulatory enforcement, supported by the Infrastructure Investment and Jobs Act (IIJA). A key trend is the adoption of epoxy-based passive fire protection (PFP) coatings for aging industrial and transportation assets.

Innovation is focused on performance and safety. The introduction of edge-retentive intumescent coatings prevents thinning on structural edges, improving fire resistance reliability. Semiconductor expansion under the CHIPS Act is driving demand for low-outgassing fireproof coatings in cleanroom environments, while aerospace applications are adopting lightweight epoxy PFP systems for launch infrastructure. Additionally, rising fire safety concerns are pushing new HUD mandates for fire-retardant coatings in residential construction, reinforcing the market’s shift toward high-performance, compliant systems.

Saudi Arabia Fire Protection Coatings Market: Vision 2030 Megaprojects Driving High-Performance Demand

Saudi Arabia is one of the fastest-growing markets for fire protection coatings, driven by large-scale developments under Vision 2030. Projects like NEOM and the Red Sea Project are specifying desert-grade intumescent coatings capable of maintaining performance in temperatures exceeding 50°C.

Oil & gas infrastructure is a major driver. Offshore projects are deploying dual-layer epoxy PFP coatings with glass-flake reinforcement for hydrocarbon fire protection. Regulatory enforcement under SABER standards is ensuring only certified systems (UL 1709, EN 13381-8) are used. Additionally, the construction boom is driving demand for cementitious fireproofing sprays in metro tunnels and prefabricated fire protection panels for rapid infrastructure development. Localization efforts—such as new resin plants—are further strengthening domestic supply chains.

India Fire Protection Coatings Market: Infrastructure Expansion and Regulatory Formalization Driving Rapid Growth

India is experiencing rapid growth in fire protection coatings, supported by infrastructure expansion and stricter safety regulations. Under the Gati Shakti master plan, fire-rated intumescent coatings are now specified for airports, railways, and major infrastructure projects.

Transportation and real estate are key drivers. The expansion of Vande Bharat trains is increasing demand for fire-retardant interior coatings compliant with global standards (EN 45545-2), while commercial real estate is standardizing 120-minute waterborne intumescent coatings for Grade-A buildings. Data center growth is also a major factor, with increasing demand for intumescent cable coatings to prevent fire spread. Industry consolidation—such as JSW–AkzoNobel integration—is improving local production of high-performance coatings. Additionally, new regulations mandating digital Fire Risk Assessment (FRA) documentation are formalizing compliance across sectors.

Germany Fire Protection Coatings Market: Clean Chemistry and Hydrogen Infrastructure Driving Sustainability

Germany is a leader in sustainable fire protection coatings, driven by strict EU regulations and energy transition initiatives. Innovation is focused on biocide-free mineral coatings, which provide mold resistance without regulated chemical additives, aligning with updated EU environmental standards.

Hydrogen infrastructure is a key growth area. Advanced epoxy-polyurethane hybrid fire coatings are being developed to protect electrolyzers and pipelines from jet-fire scenarios. Additionally, regulatory reforms—such as the Building Safety Regulator (BSR) updates (2026)—are increasing scrutiny on fireproof coatings in high-risk buildings. Technological advancements include UV-curable intumescent coatings, reducing energy consumption by ~40%, and recycled-monomer fire retardants, supporting circular economy goals.

UAE Fire Protection Coatings Market: Smart Monitoring and Desert-Grade Performance Driving Innovation

The UAE is a global testbed for smart fire protection coatings, combining advanced materials with digital monitoring systems. A major innovation is the integration of IoT-enabled sensors within intumescent coatings, enabling real-time detection of temperature anomalies in high-rise buildings.

Regulatory enforcement is a key driver. The UAE Unified Building Codes (2026) mandate non-combustible cladding systems with high-performance fire coatings, while strict TVOC limits (≤250 g/L) are accelerating adoption of low-emission formulations. Infrastructure expansion—particularly in ports and hospitality—is increasing demand for C5-M-rated fire protection coatings and aesthetic metallic finishes. Additionally, the use of AI-powered drone inspections is improving quality control by verifying coating thickness and integrity in large-scale projects.

Fire Protection Coatings Market Report Scope

Fire Protection Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.3 Billion

|

|

Market Size (2032)

|

$1.9 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Coating Type (Intumescent Coatings, Cementitious Coatings, Ablative Coatings, Specialty), By Technology (Water-borne, Solvent-borne, 100% Solids, Powder-based Fire Protection), By Substrate (Structural Steel, Concrete and Masonry, Wood, Cables and Electrical Penetrations, Composites and Plastics), By Fire Scenario (Cellulosic Fire Protection, Hydrocarbon Fire Protection, Cryogenic Spill Protection, Jet Fire Protection), By Application Method (Spray Applied, Brush and Roller Applied, Trowel Applied), By End-Use Industry (Building and Construction, Oil and Gas, Industrial Manufacturing, Transportation, Energy and Power), By Sales Channel (New Construction, Maintenance and Retrofitting)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Jotun A/S, Hempel A/S, Sika AG, RPM International Inc., 3M Company, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Etex Group, Hilti Corporation, Rudolf Hensel GmbH, Teknos Group, Isolatek International

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fire Protection Coatings Market Segmentation

By Coating Type

- Intumescent Coatings

- Cementitious Coatings

- Ablative Coatings

- Specialty

By Technology

- Water-borne

- Solvent-borne

- 100% Solids

- Powder-based Fire Protection

By Substrate

- Structural Steel

- Concrete and Masonry

- Wood

- Cables and Electrical Penetrations

- Composites and Plastics

By Fire Scenario

- Cellulosic Fire Protection

- Hydrocarbon Fire Protection

- Cryogenic Spill Protection

- Jet Fire Protection

By Application Method

- Spray Applied

- Brush and Roller Applied

- Trowel Applied

By End-Use Industry

- Building and Construction

- Residential

- Commercial

- Institutional

- Oil and Gas

- Upstream

- Midstream and Downstream

- Industrial Manufacturing

- Transportation

- Marine and Shipbuilding

- Aerospace and Defense

- Rail and Tunnels

- Energy and Power

- Conventional Power Plants

- Renewable Energy

By Sales Channel

- New Construction

- Maintenance and Retrofitting

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Fire Protection Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Jotun A/S

- Hempel A/S

- Sika AG

- RPM International Inc.

- 3M Company

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Etex Group

- Hilti Corporation

- Rudolf Hensel GmbH

- Teknos Group

- Isolatek International

*- List not Exhaustive