Fireproofing Coatings for Wood Market Growth Driven by Mass Timber Construction, Green Building Regulations, and Aesthetic Fire Protection Solutions

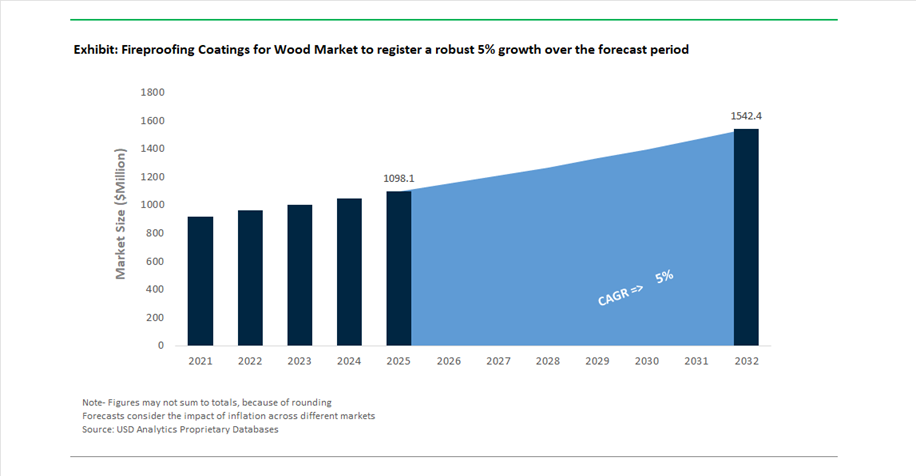

The global Fireproofing Coatings for Wood Market was valued at USD 1,098.1 million in 2025 and is projected to grow at a CAGR of 5% between 2025 and 2032, reaching USD 1,545.1 million by 2032. This growth is being driven by the increasing adoption of mass timber construction, stringent fire safety regulations, and the demand for aesthetically compatible fire protection systems in modern architecture.

A key structural driver is the rapid rise of engineered wood and mass timber buildings, including cross-laminated timber (CLT) structures used in mid- and high-rise construction. While wood offers sustainability and carbon sequestration benefits, it introduces fire safety challenges that must be addressed through intumescent and fire-retardant coatings. These coatings enable wood to meet stringent fire performance standards by forming a protective char layer that delays ignition and structural degradation.

Regulatory developments are significantly accelerating market demand. The implementation of EU Directive 2024/1275, which integrates energy efficiency with fire resilience in building renovations, is driving the retrofitting of historical wooden structures and interior paneling with certified fireproof coatings. Similarly, North America is witnessing increased adoption of UL-certified fire protection systems for wood in multi-story mixed-use developments, reflecting evolving building codes that support timber construction while ensuring safety compliance.

Sustainability is emerging as a critical innovation theme. Manufacturers are developing low-VOC, halogen-free, and bio-based fire-retardant coatings, addressing environmental concerns associated with traditional chemical systems. At the same time, advancements in transparent and thin-film intumescent coatings are enabling architects to preserve the natural grain and aesthetic appeal of wood, which has historically been a barrier to adoption.

Transparent Intumescent Innovation, Bio-Based Fire Retardants, and Regulatory Push Reshape Market Dynamics

The fireproofing coatings for wood market is undergoing a transformation driven by advanced coating technologies, sustainability innovations, and regional expansion strategies. In March 2024, Sherwin-Williams launched FIRETEX FX7002, a thin-film intumescent system offering up to two hours of fire resistance with minimal coating thickness. This innovation is particularly significant for wood applications, as it allows high-end architectural projects to maintain natural wood aesthetics without compromising fire safety.

Product innovation is also focusing on balancing performance and visual appeal. In March 2024, Teknos showcased its TEKNOSAFE range at Fensterbau Frontale, demonstrating fire protection solutions used in landmark projects such as Finland’s Oodi Public Library. These coatings provide IAC Gold-certified fire resistance while preserving the natural look of wood, addressing a critical adoption barrier in premium construction projects.

Sustainability-driven breakthroughs are reshaping the competitive landscape. In January 2025, Nordtreat introduced bio-based, lignin-derived fire retardant coatings, offering fully biodegradable and halogen-free alternatives to conventional systems. This innovation aligns with the growing demand for environmentally friendly fire protection solutions, particularly in green building projects and eco-conscious markets.

Technological adaptation from other coating segments is expanding capabilities. In February 2026, PPG Industries introduced water-based intumescent technology through its STEELGUARD 652 platform, with adaptations underway for wooden substrates. This approach enables low-VOC, on-site fireproofing applications, supporting sustainable construction practices and improving installation efficiency.

Advanced hybrid coatings are also extending application scope. In November 2025, Jotun launched Jotachar 1709XT, a high-durability passive fire protection system initially developed for industrial environments but now being adapted for heavy timber structures requiring long-term performance in harsh conditions.

Strategic expansion and vertical integration are strengthening market positioning. In March 2025, Nippon Paint Holdings acquired AOC, enhancing access to advanced resin technologies for transparent fire-retardant wood coatings, addressing issues such as yellowing and durability. Additionally, in May 2025, Teknos expanded into Central Europe through the integration of Finnproduct, targeting growing demand in mass timber construction hubs.

Market expansion in emerging regions is also gaining momentum. In January 2026, Sherwin-Williams leveraged its integration of Suvinil to introduce fire-retardant wood coatings in Latin America, particularly in luxury hospitality and eco-tourism projects.

Clear Intumescent Coatings Enabling Fire-Safe Mass Timber High-Rise Construction

The fireproofing coatings for wood industry is experiencing strong momentum as mass timber construction gains global traction, particularly in high-rise applications utilizing cross-laminated timber and glulam systems. Architects and developers are increasingly specifying clear intumescent coatings to achieve stringent fire-resistance ratings while preserving the natural aesthetic of exposed wood surfaces. Modern formulations are engineered to deliver ASTM E84 Class A flame spread performance while remaining visually indistinguishable from conventional polyurethane finishes, enabling seamless integration into high-end architectural designs. The growth of the cross-laminated timber market, valued at approximately 1.68 billion dollars by early 2026, is reinforcing demand for advanced fireproof coatings that support structural safety without compromising design intent. Unlike traditional sacrificial charring approaches, thin-film intumescent coatings form an insulating char barrier when exposed to heat, maintaining the load-bearing capacity of timber elements during fire events. This capability is critical in high-rise applications where structural integrity is paramount. Additionally, the increasing adoption of biophilic design principles in commercial interiors is contributing to a 15% year-over-year rise in the specification of fireproofed wood surfaces, particularly in WELL-certified office environments. These dynamics are positioning clear intumescent coatings as a core enabling technology for the expansion of fire-safe, aesthetically driven mass timber construction.

Wildland-Urban Interface Codes Driving Exterior Fireproofing Coatings for Wood Structures

The expansion of wildfire-prone zones across the Western United States is driving a regulatory transformation that is significantly impacting the fireproofing coatings market for wood applications. The introduction of the 2025 California Wildland-Urban Interface Code, effective January 2026, replaces earlier frameworks with more stringent requirements for ignition-resistant materials used in exterior wood assemblies such as siding, decking, and shingles. These updated standards emphasize resistance to ember intrusion, a leading cause of structure ignition during wildfires. As a result, exterior fireproofing coatings are now being rigorously tested under ASTM E2910 and ASTM E2886 protocols to ensure they can withstand prolonged exposure to burning embers without igniting. Manufacturers are actively seeking certification under the CAL FIRE Building Materials Listing program, with over 120 specialized coating products evaluated by late 2025, highlighting the rapid expansion of compliant solutions in the market. In addition to regulatory drivers, insurance incentives are reinforcing adoption, with homeowners in high-risk zones eligible for premium reductions of 10% to 15% when certified fire-resistant coatings are applied. These combined regulatory and economic factors are accelerating the adoption of exterior fireproof coatings, positioning them as essential components in wildfire resilience strategies for residential and commercial wood structures.

US Forest Service Grants Accelerating Innovation in Fireproof Coatings for Mass Timber Applications

The United States Forest Service is playing a pivotal role in advancing the fireproofing coatings for wood industry through substantial funding initiatives aimed at promoting sustainable forestry and fire-safe construction. In 2025, the agency allocated approximately 80 million dollars under its Wood Innovations and Wood Product Infrastructure Grant programs, with a significant portion directed toward projects that enhance the fire performance of mass timber materials. These grants are supporting research and commercial demonstration of innovative fireproofing coatings designed to improve the safety and market viability of small-diameter timber sourced from forest thinning operations. Typical funding awards ranging from 300,000 to 500,000 dollars are enabling pilot-scale production and real-world testing of advanced coating technologies for cross-laminated and mass-ply panels. The program also emphasizes the development of domestic supply chains, encouraging collaboration between coating manufacturers and local sawmills to establish factory-applied fireproofing processes. This integration is improving product consistency, reducing application costs, and accelerating adoption in large-scale construction projects. By linking wildfire risk reduction with material innovation, these funding initiatives are creating a sustainable growth pathway for fireproofing coatings that enhance both environmental resilience and building safety.

Japan Building Standards Reform Expanding Market for Fireproofed Timber in Mid-Rise Construction

Japan’s 2025 revision of its Building Standards Law is creating a significant opportunity for fireproofing coatings by enabling broader use of timber in urban construction while maintaining strict fire safety requirements. The removal of the previous exemption for small-scale wooden buildings now mandates comprehensive fire safety verification for all two-story structures and multi-family developments, increasing demand for certified fireproofing solutions. At the same time, regulatory changes have introduced flexibility by allowing large wooden buildings exceeding 3,000 square meters to retain exposed timber elements when treated with approved fireproofing systems. This is driving the adoption of intumescent coatings and fire-retardant-treated wood in commercial and residential projects seeking both compliance and aesthetic appeal. For mid-rise buildings between five and nine floors, reduced fire resistance requirements of approximately 90 minutes are making fireproofed wood construction more economically viable, expanding its applicability in urban housing developments. Additionally, rising construction costs are encouraging large-scale renovation projects where existing wooden structures are upgraded with modern fireproof coatings to meet updated seismic and energy efficiency standards without full reconstruction. These regulatory reforms are positioning Japan as a key growth market for advanced wood fireproofing coatings, particularly in the context of sustainable and cost-effective urban development.

Fireproofing Coatings for Wood Market Share 2025: Intumescent Technology and Spray Application Lead Growth

Coating Type Insights: Intumescent Coatings Dominate with Advanced Fire Protection for Timber Structures

The intumescent coatings segment commands a leading 58% market share in the fireproofing coatings for wood market in 2025, driven by its superior fire protection performance and compliance with global building codes. These coatings provide char-forming fire resistance, expanding under high temperatures to create a thick insulating barrier that can delay wood ignition and preserve structural integrity for up to 120 minutes in standardized fire tests. This capability is critical as the construction industry increasingly adopts mass timber solutions such as cross-laminated timber (CLT) and glued laminated timber (glulam) in mid- and high-rise buildings. Intumescent coatings allow architects and developers to meet IBC and Eurocode fire safety requirements without compromising the natural wood aesthetic, making them highly desirable in modern sustainable construction. As timber-based construction gains momentum globally, intumescent fireproof coatings will continue to dominate market demand.

Application Method Insights: Spraying Emerges as the Preferred Technique for Large-Scale Projects

The spraying segment leads the market with a substantial 65% share in 2025, reflecting its efficiency and scalability in applying fireproofing coatings on wood surfaces. Techniques such as airless spraying and HVLP (high-volume low-pressure) systems enable contractors to achieve uniform coating thickness across large areas, including beams, ceilings, and CLT panels, significantly faster than traditional brush or roller methods. This speed advantage is particularly important in commercial and large-scale construction projects, where timelines are critical. Additionally, spraying reduces labor intensity and minimizes rework, allowing single operators to efficiently coat complex geometries such as decorative timber trusses and architectural wood elements. The resulting cost savings and improved application consistency make spraying the preferred choice among contractors. As demand for high-performance fire-resistant wood coatings grows, spray application technology will remain a key enabler of market expansion.

Fireproofing Coatings for Wood Market Competitive Landscape Driven by Sustainable Intumescent Systems and CLT Protection Demand

The fireproofing coatings for wood market is highly competitive, driven by rising adoption of cross-laminated timber (CLT), green building standards, and low-VOC fire-retardant coatings. Key players are focusing on bio-based formulations, intumescent technologies, and aesthetic-preserving coatings for architectural wood applications.

Sherwin-Williams advances fireproof wood coatings with bio-based systems and high-performance lacquer innovation

The Sherwin-Williams Company is strengthening its position in the fireproofing coatings for wood market through bio-attributed and plant-based coating systems aligned with sustainability trends. The company showcased its Lympha collection at Milano Design Week 2026, combining botanical aesthetics with fire-resistant wood coatings for premium interior applications. Its solvent-based fire-retardant lacquer system upgrades MDF substrates to Bs1d0 classification under EN13501-1, enhancing fire safety for oak veneer structures. Sherwin-Williams leverages its network of over 5,000 stores to ensure rapid delivery of Laqva Top Bio and Laqvin Top coatings, supporting demand from transportation and interior fit-out sectors. Its integrated CO2 calculator enables architects to evaluate carbon savings from using eco-friendly coatings. This combination of performance and sustainability strengthens its leadership in fireproof wood coatings.

AkzoNobel expands fire-retardant wood coatings with formaldehyde-free systems and Asia-Pacific growth strategy

AkzoNobel is reinforcing its competitive position in the fireproof wood coatings market through its Sikkens portfolio, including "Beyond" formaldehyde-free and "Quantum" PU-acrylic fire-retardant systems for furniture and joinery applications. The company reported a strong 14.2% EBITDA margin, supported by a price-driven growth strategy and expansion into Asia-Pacific, which accounts for 45.3% of global demand. Its ongoing merger with Axalta is expected to enhance R&D capabilities in waterborne intumescent technologies. AkzoNobel is focusing on performance coatings for heritage preservation and green building envelopes requiring durable, translucent finishes. These coatings maintain natural wood aesthetics while delivering fire resistance. This strategy positions the company as a leader in sustainable decorative fireproof coatings.

PPG Industries drives CLT fireproofing coatings innovation with low-VOC intumescent systems

PPG Industries is advancing the fireproofing coatings for wood market by adapting its low-VOC waterborne intumescent technologies for wood substrates, offering coatings with up to 20-year durability. Following its portfolio optimization, PPG is focusing on high-margin industrial OEM and protective wood coatings. The company is a key player in cross-laminated timber (CLT) fire protection, providing coatings that reduce flame spread and ignition risk in mass timber structures. 44% of its revenue is derived from sustainably advantaged products, reflecting strong demand for eco-certified fireproof coatings. Its solutions are increasingly used in modern timber construction projects worldwide. This positions PPG as a leader in advanced fire-resistant coatings for engineered wood.

Teknos leads European fireproof wood coatings with UV-curable systems and aesthetic preservation technologies

Teknos Group is a leading manufacturer in the fireproof wood coatings market, holding a dominant share in Europe’s industrial wood finishing segment. The company offers FR-certified coatings with clear fillers and sealers that preserve the natural appearance of wood while meeting strict EU fire safety standards. Its expertise in waterborne UV-curable coatings enables production speeds up to 50% faster, making it ideal for fire-rated doors and panels. Teknos is expanding into the Middle East and Africa, where demand is growing due to infrastructure and hospitality developments. Its focus on combining aesthetics with fire resistance enhances its competitive positioning. These capabilities make Teknos a preferred supplier for high-performance decorative fireproof coatings.

BASF supports fireproof wood coatings market with advanced intumescent additives and sustainable chemistry

BASF SE plays a critical role in the fireproof wood coatings market as a supplier of high-performance resins and additives used in third-party coating formulations. The company is forecasting EBITDA of €6.2 billion to €7.0 billion, supported by demand for advanced chemical solutions. At the 2026 American Coatings Show, BASF introduced next-generation intumescent additives that reduce coating thickness by 20% while maintaining fire protection performance. Its focus on non-halogenated flame retardants aligns with regulatory demand for low-toxicity smoke emissions. Following its divestment of its Brazilian coatings business, BASF is concentrating on core chemical innovations. This positions BASF as a key enabler of next-generation fireproof wood coatings.

Nordtreat leads bio-based fireproof wood coatings with Nor-X technology and timber architecture adoption

Nordtreat AS is emerging as a niche leader in the fireproof wood coatings market, specializing in bio-based, VOC-free fire retardant solutions. Its Nor-X technology provides durable fire protection for exterior wood facades without leaching under UV exposure or heavy rainfall. The company has secured major contracts for high-rise timber buildings, where maintaining exposed wood aesthetics is critical. Nordtreat collaborates with leading CLT manufacturers to deliver factory-applied fire protection, ensuring consistent quality and regulatory compliance. Its eco-friendly formulations meet stringent environmental standards while delivering high fire resistance. This positions Nordtreat as a key innovator in sustainable fireproof coatings for modern timber construction.

China Fireproofing Coatings for Wood Market: CLT Expansion and Low-VOC Transition Driving Scale

China is rapidly scaling its fireproof coatings for wood market, supported by the rise of Cross-Laminated Timber (CLT) construction and the Dual-Carbon mandate. Regulatory updates now require certified fire-rated coatings for every square meter of structural timber, significantly boosting demand.

Sustainability regulations are accelerating transformation. Strict VOC limits in regions like the Greater Bay Area have driven a ~55% shift toward waterborne intumescent coatings. Innovation is also strong, with nano-clay and carbon nanotube-enhanced coatings reducing char depth by ~15% in fire tests. Additionally, AI-driven spray systems are improving coating thickness precision for compliance, while tax incentives for net-zero timber housing are encouraging adoption of photocatalytic, self-cleaning fireproof coatings.

United States Fireproofing Coatings for Wood Market: Mass Timber Growth and Bio-Based Innovation Driving Demand

The United States is the largest regional market, driven by mass timber construction and sustainability initiatives. The THINKOnWood program (2025–2026) is promoting fire-resilient timber structures, especially in wildfire-prone areas.

Innovation is focused on safety and aesthetics. New bio-based fire-retardant wood coatings achieve Class A performance without toxic leaching, while transparent intumescent coatings preserve natural wood appearance in commercial spaces. Regulatory shifts have increased adoption of waterborne coatings (≈74% share) due to low VOC emissions and moisture control. Additionally, modular construction trends are driving demand for factory-applied UV-cured coatings, improving uniformity by ~22%, while insurance incentives are encouraging BIM-verified fireproofing systems.

Germany Fireproofing Coatings for Wood Market: Bio-Polymer Chemistry and Circular Economy Driving Sustainability

Germany leads Europe in sustainable fireproof wood coatings, with a strong focus on eliminating hazardous chemicals. Breakthroughs include lignin-based polyurethane coatings, which significantly reduce carbon emissions compared to conventional systems.

Regulatory compliance is a key driver. Germany is advancing halogen-free, phosphorus-rich intumescent coatings to meet upcoming EU bans on harmful substances. The Renovation Wave is also fueling demand, with a $300 million retrofit backlog for historic wooden structures requiring fireproof coatings. Additionally, Digital Twin monitoring systems are being used to track coating performance over time, while partnerships between major chemical companies are accelerating development of weather-resistant exterior fire coatings.

Canada Fireproofing Coatings for Wood Market: Modular Construction and Bio-Based Materials Driving Growth

Canada is leveraging its forestry resources to become a leader in factory-applied fireproof coatings for wood, particularly in mass timber construction. Federal funding (2026) is supporting large-scale projects integrating fire-rated coatings into structural timber components.

Innovation is focused on efficiency and sustainability. Automated curtain-coating systems are reducing material waste by ~18%, while modular construction is increasing demand for rapid-cure fireproof coatings that withstand transport stresses. The availability of wood pulp byproducts is enabling coatings with ≥12% bio-content, aligning with LEED and WELL standards. Additionally, housing development trends are shifting spending toward structural fire protection rather than decorative coatings, reinforcing long-term demand.

India Fireproofing Coatings for Wood Market: Urbanization and Regulatory Formalization Driving Rapid Growth

India is the fastest-growing market in Asia-Pacific, driven by urbanization, infrastructure expansion, and stricter fire safety norms. Premium real estate developers are now standardizing 120-minute waterborne intumescent coatings for interior wooden cladding in Grade-A office spaces.

Infrastructure and transportation are key drivers. The expansion of Vande Bharat trains is increasing demand for EN 45545-2 compliant fire-retardant coatings for wooden interiors. Policy support through PLI schemes (2026) is promoting domestic production of phosphorus-based flame retardants, reducing import dependence. Additionally, the JSW–AkzoNobel integration is lowering costs of fire-rated coatings by ~20%, while new municipal laws mandate digital fire safety logs, including coating thickness documentation. Growth in hospitality—especially heritage hotel refurbishment—is also boosting demand for aesthetic fireproof coatings.

Australia Fireproofing Coatings for Wood Market: Bushfire Resilience and Regulatory Leadership Driving Demand

Australia’s market is shaped by extreme climate conditions and strict fire safety regulations, particularly under the National Construction Code (2025). New rules allow timber construction in bushfire-prone areas only if coatings meet BAL 40 fire resistance standards.

Innovation is focused on durability. The launch of hybrid-silicone fireproof coatings provides resistance to UV degradation and high-velocity rain, critical for coastal regions. Insurance requirements are also influencing adoption, with AS 3959-compliant coatings now mandatory for financing projects in bushfire zones. Additionally, investments in CLT manufacturing are integrating vacuum-coating systems for deep-penetration fire retardants, while government programs are supporting development of coatings tailored to native hardwood species.

Fireproofing Coatings for Wood Market Report Scope

Fireproofing Coatings for Wood Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1098.1 Million

|

|

Market Size (2032)

|

$1545.1 Million

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Technology (Water-borne, Solvent-borne, UV-Cured, Powder-based), By Resin Type (Acrylic, Polyurethane, Epoxy, Silicone, Alkyd, Bio-based), By Coating (Intumescent Coatings, Non-intumescent, Halogen-Free Coatings, Halogenated Coatings), By Application Area (Interior Applications, Exterior Applications), By Substrate Type (Softwood, Hardwood, Engineered Wood), By End-Use Industry (Building and Construction, Furniture Manufacturing, Marine, Aviation and Aerospace, Electrical and Electronics), By Application Method (Spraying, Brush and Roller Applied, Vacuum)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., RPM International Inc., Jotun A/S, Sika AG, Hempel A/S, Benjamin Moore & Co., Teknos Group, ICA Group, Lonza Group, Koppers Inc., FlameOFF® Coatings, Inc., Intumescent Systems Ltd., RUDOLF HENSEL GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fireproofing Coatings for Wood Market Segmentation

By Technology

- Water-borne

- Solvent-borne

- UV-Cured

- Powder-based

By Resin Type

- Acrylic

- Polyurethane

- Epoxy

- Silicone

- Alkyd

- Bio-based

By Coating

- Intumescent Coatings

- Non-intumescent

- Halogen-Free Coatings

- Halogenated Coatings

By Application Area

- Interior Applications

- Exterior Applications

By Substrate Type

- Softwood

- Hardwood

- Engineered Wood

By End-Use Industry

- Building and Construction

- Residential

- Commercial

- Institutional

- Furniture Manufacturing

- Marine

- Aviation and Aerospace

- Electrical and Electronics

By Application Method

- Spraying

- Brush and Roller Applied

- Vacuum

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Fireproofing Coatings for Wood Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- RPM International Inc.

- Jotun A/S

- Sika AG

- Hempel A/S

- Benjamin Moore & Co.

- Teknos Group

- ICA Group

- Lonza Group

- Koppers Inc.

- FlameOFF® Coatings, Inc.

- Intumescent Systems Ltd.

- RUDOLF HENSEL GmbH

*- List not Exhaustive