Flame Retardants for Engineering Resins Market Size, Growth Outlook, and Regulatory Transformation Driving Demand

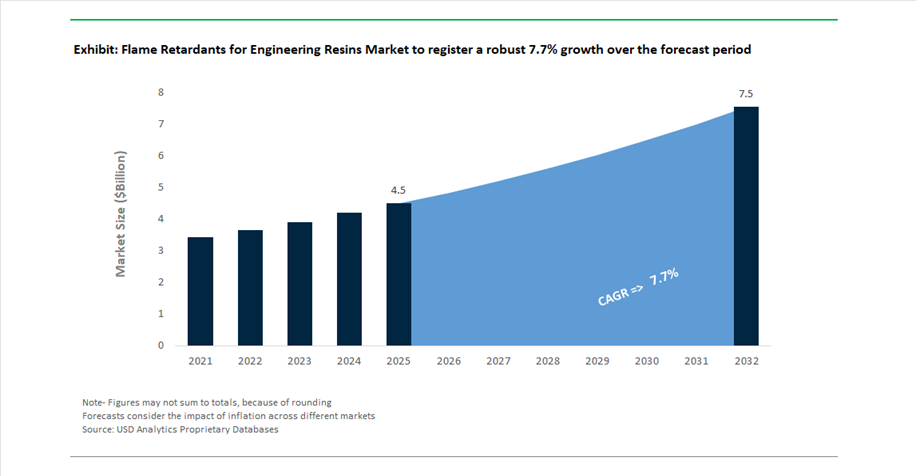

The global Flame Retardants for Engineering Resins Market stood at USD 4.5 billion in 2025 and is forecast to reach USD 7.6 billion by 2032, registering a CAGR of 7.7%, driven by a clear industry-wide transition toward high-performance, halogen-free flame retardant solutions. This shift is strongly influenced by tightening fire safety regulations, sustainability mandates, and the increasing complexity of engineering resin applications across advanced industries. Notably, non-halogenated flame retardants accounted for 65.08% of total demand in 2025, supported by regulatory restrictions on brominated compounds and the superior environmental and toxicological profiles of phosphorus-, nitrogen-, and aluminum-based chemistries.

Demand dynamics are being shaped by the rapid expansion of the electrical and electronics (E&E) sector, where each smart device integrates 8 to 12 grams of UL 94 V-0 compliant halogen-free flame retardants, emphasizing the need for miniaturized, thermally stable, and fire-safe polymer systems. Concurrently, infrastructure-led growth, particularly in emerging markets such as India, is accelerating adoption of LSZH (low-smoke zero-halogen) cable materials, while stringent regulations like the EU POPs framework are eliminating legacy brominated systems from recycling streams and increasing dependence on virgin, compliant resins. Sustainability is becoming a decisive procurement factor, with upcoming EU CO₂ disclosure requirements (2026) driving preference for low-carbon phosphorus-based flame retardants, especially in Polyamide 66, where improved life cycle assessment (LCA) performance supports ESG-aligned material selection and long-term competitive positioning.

Price Volatility, Regulatory Bans, and Halogen-Free Innovation Reshaping Market Dynamics

The Flame Retardants for Engineering Resins Market is undergoing a significant transformation shaped by regulatory tightening, cost inflation, and evolving material innovation. Pricing pressures have intensified, highlighted by LANXESS implementing price increases of up to 35% in March 2026 due to rising energy costs, raw material constraints, and geopolitical supply chain disruptions. This reflects a broader industry-wide trend of margin compression and procurement realignment, forcing OEMs and compounders to reevaluate sourcing strategies and supplier dependencies.

At the same time, the market is witnessing accelerated innovation in halogen-free, reactive flame retardant chemistries. ICL-IP introduced a phosphorus-based reactive flame retardant in October 2025 that chemically integrates into polymer matrices such as PIR and PUR foams, eliminating migration and enhancing long-term durability. Complementing this, BASF launched its Ultradur High Speed PBT grade, achieving UL 94 V-0 performance at just 0.75 mm thickness, directly addressing the miniaturization and thermal management demands of EV connectors and high-density electronic components. These developments signal a shift toward high-performance, application-specific, and lifecycle-optimized material solutions.

Regulatory frameworks remain a critical force reshaping market dynamics across key regions. The United States Environmental Protection Agency finalized a TSCA rule banning deca-BDE from 2027, while the European Chemicals Agency is advancing restrictions on brominated flame retardants, accelerating adoption of alternatives such as aluminum diethylphosphinate (AlPi) and melamine polyphosphate. Additionally, the EU Construction Products Regulation (CPR) recast mandates EPDs and CO₂ disclosures, reinforcing sustainability-driven procurement. In response, companies like Huber Engineered Materials are expanding halogen-free product capacity, while Stratasys is advancing flame-retardant 3D printing resins for aerospace and medical applications. Collectively, these trends underscore a market pivot toward regulation-compliant, sustainable, and high-value flame retardant solutions.

Microencapsulated Red Phosphorus Driving High-Performance Flame Retardant Polyamides in EV Busbars

The flame retardants for engineering resins market is witnessing a resurgence of red phosphorus-based systems, particularly in high-voltage electric vehicle applications such as busbars and battery modules. Microencapsulated red phosphorus has emerged as a highly efficient flame retardant additive, enabling glass-fiber reinforced polyamide compounds to achieve UL 94 V-0 ratings at significantly lower loadings of 5% to 8%, compared to 20% to 30% required for alternative halogen-free systems. This low loading advantage preserves critical mechanical properties, including tensile strength and impact resistance, which are essential for safety-critical automotive components. Additionally, red phosphorus-based formulations consistently achieve Comparative Tracking Index Class 0 ratings above 600 volts, meeting the insulation requirements for advanced 800V and 900V EV architectures designed for ultra-fast charging systems. Technological advancements in microencapsulation have addressed historical challenges associated with moisture sensitivity, reducing the risk of phosphine gas emission by approximately 60% and enabling stable performance in humid operating environments. Improvements in pigment stabilization have also enhanced color versatility, allowing manufacturers to produce standardized signal orange busbar housings that comply with global high-voltage safety identification norms. These innovations are positioning red phosphorus as a key material in next-generation flame retardant polyamide solutions for electrified mobility applications.

China’s Mandatory RoHS Framework Accelerating Transition to Halogen-Free Flame Retardant Systems

China’s introduction of the GB 26572-2025 regulation marks a significant turning point in the global flame retardant engineering resins market, transitioning RoHS compliance from voluntary to mandatory enforcement. The regulation specifically targets the elimination of decabromodiphenyl ether in engineering plastics such as polybutylene terephthalate, with full compliance required by August 2027. In response, leading electronics manufacturers have initiated large-scale zero-halogen conversion programs beginning in early 2026 to align with substance limits of 0.1% by weight. This transition is driving increased adoption of polymeric brominated flame retardants such as brominated polystyrene, which provide approximately 25% improved thermal aging performance compared to legacy small-molecule additives. The updated regulation also expands restrictions to include key phthalates, necessitating reformulation of flexible thermoplastic elastomers and wire insulation materials used in consumer electronics. Enforcement is being standardized through the GB/T 39560 testing framework, creating a more stringent compliance environment that is expected to remove approximately 15% of non-compliant flame retardant masterbatches from the domestic market. These regulatory developments are accelerating innovation in halogen-free and compliant flame retardant systems, reshaping material selection strategies across the electronics and electrical manufacturing ecosystem.

US DOE Motor Cooling Initiatives Driving Demand for Flame Retardant High-Performance Engineering Resins

The United States Department of Energy’s focus on next-generation electric motor technologies is creating a strong growth opportunity for flame retardant engineering resins capable of operating under extreme thermal and chemical conditions. The transition toward oil-cooled motor architectures is significantly increasing performance requirements for materials used in stator insulation and structural components. Flame retardant polyphenylene sulfide and polyphthalamide resins are being developed to withstand continuous exposure to dielectric fluids such as automatic transmission fluid at temperatures up to 150°C for more than 3,000 hours without degradation or loss of dielectric strength beyond 10%. These materials must also integrate thermal conductivity values exceeding 1.5 W per meter Kelvin to support efficient heat dissipation in compact motor designs. Oil-cooled systems are capable of increasing motor power density by 50% to 70% compared to traditional cooling methods, but they require resins with exceptional resistance to hydrolytic degradation and chemical attack. Advances in formulation are enabling flame retardant resins to achieve UL 94 V-0 ratings at wall thicknesses as low as 0.4 millimeters, allowing for tighter copper packing and more efficient motor architectures. These developments are positioning flame retardant engineering resins as a critical enabler of high-efficiency electric powertrain systems.

Japan’s DENAN Law Revision Driving Conversion to Flame Retardant Engineering Plastics in Home Appliances

Japan’s revision of the Electrical Appliance and Material Safety Law is creating a substantial opportunity for flame retardant engineering resins in the home appliance sector. The updated regulation, effective August 2025, aligns national standards with international safety benchmarks and introduces stricter ignition resistance requirements for unattended appliances. Manufacturers are now required to meet glow wire ignition temperature thresholds of 775°C, driving a significant material shift from conventional plastics such as ABS to flame retardant polycarbonate and PC/ABS blends. This transition is evident in early 2026 market data, which shows widespread conversion of internal appliance components to high-performance flame retardant resins capable of meeting these stringent safety criteria. The harmonization of Japanese standards with international frameworks has also reduced barriers for global manufacturers, facilitating the entry of halogen-free flame retardant polybutylene terephthalate and polyamide materials into the domestic market. Additionally, enhanced labeling requirements under the PSE certification system are increasing demand for third-party certified, high-quality flame retardant resins, with a reported 20% increase in preference for branded materials over generic alternatives. These regulatory changes are strengthening the adoption of advanced flame retardant engineering plastics in Japan’s appliance manufacturing industry.

Flame Retardants for Engineering Resins Market Share 2025: Masterbatch Dominance and Direct Sales Expansion

Form Insights: Masterbatches Lead with Superior Dispersion and Processing Efficiency

The masterbatches segment dominates the flame retardants for engineering resins market with a 44% market share in 2025, driven by its ability to deliver clean, dust-free handling and consistent additive dispersion. Masterbatches enable uniform integration of flame retardant chemistries such as phosphorus-based compounds and melamine cyanurate into high-performance engineering resins including polyamide (PA), polybutylene terephthalate (PBT), and PC/ABS blends. This uniformity reduces equipment wear, particularly screw abrasion during compounding, while ensuring reliable fire safety performance. Additionally, the rise of just-in-time compounding in injection molding operations is significantly boosting demand, as manufacturers prefer masterbatches for on-site customization of color and flame retardancy, avoiding large inventories of pre-compounded materials. This flexibility allows faster adaptation to UL94 fire safety ratings and evolving product specifications, making masterbatches the preferred form in advanced polymer processing industries.

Distribution Channel Insights: Direct Sales Dominate with OEM-Centric Customization and Compliance Support

The direct sales segment holds the largest 52% share in the flame retardants for engineering resins market in 2025, reflecting the growing need for customized formulations and regulatory expertise. Major OEMs in the automotive, electrical, and electronics sectors rely on direct partnerships with leading suppliers such as Clariant, Lanxess, and ICL to secure proprietary flame retardant systems tailored to specific requirements, including halogen-free solutions, brominated compounds, and glow wire ignition resistance (GWIT) compliance. These direct relationships enable long-term supply agreements and ensure consistent product performance. Furthermore, manufacturers benefit from comprehensive regulatory compliance support, including documentation for REACH, RoHS, and WEEE standards, which are critical for global market access. Given the complexity of fire safety regulations and material performance requirements, direct sales channels will continue to play a pivotal role in driving growth and innovation in the engineering resins flame retardants market.

Flame Retardants for Engineering Resins Market Competitive Landscape Driven by Halogen-Free Innovation, EV Electrification, and Advanced Additive Technologies

The flame retardants for engineering resins market is highly competitive, driven by demand from EVs, electronics, and high-performance polymers. Key players are focusing on halogen-free solutions, phosphorus-based additives, and vertically integrated supply chains to meet stringent fire safety standards and sustainability regulations.

LANXESS strengthens engineering resin flame retardants with brominated leadership and Levagard® expansion

LANXESS AG maintains a strong position in the flame retardants for engineering resins market through its leadership in the brominated segment, supported by the Emerald Innovation™ series. The company is executing its FORWARD! plan to deliver €150 million in annual cost savings by 2026, improving operational efficiency. Its Levagard® phosphorus-based portfolio is expanding rapidly to meet growing demand for halogen-free flame retardants in polyurethane engineering applications. LANXESS is enhancing vertical integration across bromine and phosphorus supply chains to mitigate raw material price volatility. This strategy ensures supply stability amid fluctuations in antimony feedstocks. These capabilities position LANXESS as a key supplier of high-performance flame retardant additives for engineering resins.

Clariant drives halogen-free flame retardants growth with Exolit™ innovations and Asia-Pacific expansion

Clariant AG is advancing its presence in the engineering resins flame retardants market through its Exolit™ portfolio, highlighted by the launch of OP 1266 for 800V+ e-mobility systems requiring high CTI performance. Its Exolit™ OP Terra products offer a 20% lower carbon footprint while maintaining UL 94 V-0 ratings even after multiple recycling cycles. The company has expanded its production capacity with a CHF 100 million Daya Bay facility, strengthening supply capabilities in the Asia-Pacific region, which accounts for 35.7% of global demand. Clariant also introduced AddWorks® PPA, a PFAS-free processing aid that enhances extrusion quality without surface defects. These innovations align with sustainability and performance requirements in advanced engineering plastics. Clariant continues to lead in phosphorus-based flame retardant technologies.

ICL Group enhances flame retardant portfolio with VeriQuel™ and bromine-based solutions for EV applications

ICL Group is strengthening its position in the flame retardants for engineering resins market through its Industrial Products segment, with projected EBITDA between $1.4 billion and $1.6 billion in 2026. The company introduced VeriQuel™ R100, a reactive phosphorus-based flame retardant designed to replace traditional additives in polyurethane systems. Its strategic focus on high-purity bromine extraction from Dead Sea resources supports demand from the EV battery safety market. ICL reports sustained bromine price strength due to rising electronics demand, despite construction sector softness. The company is prioritizing specialty-driven growth to enhance profitability. These initiatives position ICL as a key supplier of advanced flame retardants for engineering resins.

BASF advances engineering resin flame retardants with Ultramid® innovations and smart manufacturing integration

BASF SE is reinforcing its leadership in the flame retardants for engineering resins market through advanced material innovation and digital manufacturing. The company introduced Ultramid® T6000 PPA, designed for extreme thermal cycling in EV terminal blocks and busbars. BASF is implementing AI-driven production systems at its Zhanjiang Verbund site to ensure consistent quality and efficiency. Its flame-retardant polyamides are increasingly derived from circular feedstocks, including ocean plastic waste, supporting sustainability goals. The company is targeting growth in the electronics sector, through localized production in Asia. These strategies position BASF as a leader in high-performance and sustainable engineering resin solutions.

Albemarle strengthens engineering resin flame retardants with SAYTEX® solutions and energy transition focus

Albemarle Corporation continues to play a critical role in the flame retardants for engineering resins market through its SAYTEX® portfolio, including SAYTEX ALERO® polymeric flame retardants. These products offer improved processability and recyclability across engineering plastics applications. The company’s SAYTEX® 8010 remains widely used as a DBDPE alternative in consumer electronics, providing essential fire protection. Albemarle is aligning its strategy with the energy transition by supplying flame retardants for lithium-ion battery systems. Its focus on safety performance enhances fire escape time in residential and industrial applications. These initiatives reinforce Albemarle’s leadership in both traditional and next-generation flame retardant solutions.

Italmatch Chemicals drives niche leadership with phosphinate flame retardants for automotive engineering resins

Italmatch Chemicals S.p.A. is a niche leader in the flame retardants for engineering resins market, specializing in phosphinate-based additives for high-performance polymers. Its Phoslite® product line supports glass-fiber-reinforced polyamides and PBT resins widely used in automotive applications. The company has integrated its global manufacturing network to ensure supply chain resilience and consistent product availability. Italmatch is developing hybrid intumescent systems combining phosphorus and nitrogen chemistries to achieve UL 94 V-0 ratings at lower additive loadings. Its products are specified in over 30% of new-energy vehicle power distribution units worldwide. These capabilities position Italmatch as a critical supplier in EV and advanced engineering plastics markets.

Germany Flame Retardants for Engineering Resins Market: Halogen-Free Standards and High-Voltage EV Applications Driving Leadership

Germany is the global leader in flame retardants (FR) for engineering resins, driven by strict sustainability regulations and advanced automotive requirements. The market is rapidly transitioning toward non-halogenated flame retardants (NHFRs), with new formulations eliminating red phosphorus while achieving high Comparative Tracking Index (CTI >600V)—critical for EV connectors.

Regulatory frameworks are a key catalyst. Under the Eco-design for Sustainable Products Regulation (ESPR), manufacturers must provide Digital Product Passports, accelerating adoption of bio-based and recyclable FR systems. Innovation is also strong in laser-transparent FR resins, enabling welding of complex sensor housings without compromising fire safety. Additionally, investments exceeding €250 million in smart manufacturing hubs are boosting production of UL 94 V-0 rated glass-fiber reinforced resins, particularly for high-temperature applications such as FR-PPA in power electronics (>180°C).

United States Flame Retardants for Engineering Resins Market: Aerospace Standards and Data Center Expansion Driving Demand

The U.S. market is focused on high-performance FR systems for aerospace, data centers, and medical devices. Updated FAA standards are increasing demand for FR-PEI and FR-PPS, which must meet strict smoke density and toxicity (FST) requirements.

Technology is evolving toward efficiency and thermal management. New liquid-cooling-compatible FR-PBT grades are supporting high-heat server architectures, while Department of Energy (DOE) initiatives are funding domestic production of low-viscosity FR additives for thin-wall plastics. Regulatory pressure under TSCA Section 6 is accelerating the phase-out of DecaBDE, shifting ~40% of demand toward phosphorus- and polymeric brominated alternatives. Additionally, growth in defense and telecom sectors is driving adoption of FR-LCP materials for high-frequency circuit boards.

China Flame Retardants for Engineering Resins Market: EV Battery Safety and Material Control Driving Global Scale

China dominates the global market, leveraging its scale and control over key raw materials. Tightened export restrictions on antimony trioxide have reshaped global supply chains, pushing manufacturers toward alternative synergists like zinc borate and stannates.

The EV sector is the primary growth engine. Compliance with GB 38031-2020 battery safety standards is driving demand for intumescent FR-polypropylene and FR-polyamide in battery enclosures. Additionally, solar expansion is increasing use of UV-stable FR-PC/ABS blends for junction boxes, while innovations in nano-clay additives are reducing overall chemical loading in engineering resins. Regulatory enforcement has also centralized production, with closure of over 200 small-scale halogenated FR facilities, reinforcing China’s position as a high-quality manufacturing hub.

South Korea Flame Retardants for Engineering Resins Market: Semiconductor Precision and EV Safety Driving Innovation

South Korea is a global leader in high-purity FR engineering resins, particularly for semiconductors and EV battery systems. Following recent EV safety incidents, regulations now mandate UL 94 5VA-rated materials for battery housings, boosting demand for advanced FR solutions.

Innovation is focused on precision and performance. Development of antistatic FR-polyethersulfone (PES) is enabling safe semiconductor transport, while low-moisture-absorption FR-PA9T resins are improving reliability in electronic components. Additionally, translucent FR-polycarbonate is being used in automotive displays without compromising optical clarity. Government subsidies are also promoting halogen-free FR materials for EV motor insulation, while new recycling laws are encouraging adoption of recyclable FR additives.

India Flame Retardants for Engineering Resins Market: Infrastructure Growth and Electronics Manufacturing Driving Rapid Expansion

India is one of the fastest-growing markets, driven by urbanization and domestic manufacturing initiatives under Atmanirbhar Bharat. The implementation of Quality Control Orders (QCO) ensures that all flame retardants meet BIS certification, improving overall product quality.

Key growth sectors include transportation and electronics. The Vande Bharat train expansion is driving demand for EN 45545-2 compliant FR resins for interiors, while the PLI scheme is supporting local production of FR-PC/ABS materials, with demand growing at ~30% CAGR in mobile manufacturing. Infrastructure projects such as FTTH expansion are increasing use of FR-PBT in optical fiber systems, while appliances are shifting toward halogen-free FR plastics to meet export standards. Additionally, global chemical companies are establishing technical service centers in India to customize formulations for high-humidity conditions.

Japan Flame Retardants for Engineering Resins Market: Bio-Based Innovation and Miniaturization Driving Advanced Applications

Japan is at the forefront of bio-based and high-precision FR engineering resins, particularly in electronics and automotive sectors. A major breakthrough is the commercialization of V-0 rated bio-polycarbonate derived from isosorbide, combining sustainability with high fire performance.

Innovation is driven by miniaturization and advanced materials. Development of ultra-high-flow FR-LCP resins enables extremely thin connectors (~0.12 mm thickness) for 5G devices. Regulatory updates under the Chemical Substances Control Law (CSCL) are restricting brominated FRs, accelerating adoption of silicone-based alternatives. Additionally, automotive manufacturers are replacing metal components with FR-PPS materials, reducing weight by ~25%, while partnerships are advancing carbon-fiber-reinforced FR resins for EV battery structures. These developments position Japan as a leader in precision and sustainable flame-retardant technologies.

Flame Retardants for Engineering Resins Market Report Scope

Flame Retardants for Engineering Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.5 Billion

|

|

Market Size (2032)

|

$7.6 Billion

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By Type (Brominated Flame Retardants, Phosphorus-based Flame Retardants, Antimony Compounds, Nitrogen-based Flame Retardants, Inorganic, Other Specialty Additives), By Application (Polyamide, Polycarbonate, Acrylonitrile Butadiene Styrene, Polyethylene Terephthalate, PC, Other Engineering Plastics), By Form (Powder, Liquid, Granules, Masterbatches), By Mechanism of Action (Additive Flame Retardants, Reactive Flame Retardants), By End-Use Industry (Electrical and Electronics, Automotive and Transportation, Building and Construction, Aerospace and Defense, Consumer Appliances, Industrial Machinery), By Performance (Halogenated, Halogen-Free, Low Smoke Zero Halogen), By Distribution Channel (Direct Sales, Chemical Distributors and Wholesalers, Specialty Compounding Partners)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Albemarle Corporation, ICL Group Ltd., LANXESS AG, BASF SE, Clariant AG, J.M. Huber Corporation, Italmatch Chemicals S.p.A., Nabaltec AG, ADEKA Corporation, Budenheim, SABIC, Daikin Industries, Ltd., Tosoh Corporation, Jiangsu Yoke Technology Co., Ltd., RTP Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flame Retardants for Engineering Resins Market Segmentation

By Type

- Brominated Flame Retardants

- Phosphorus-based Flame Retardants

- Antimony Compounds

- Nitrogen-based Flame Retardants

- Inorganic

- Other Specialty Additives

By Application

- Polyamide

- Polycarbonate

- Acrylonitrile Butadiene Styrene

- Polyethylene Terephthalate

- PC

- Other Engineering Plastics

By Form

- Powder

- Liquid

- Granules

- Masterbatches

By Mechanism of Action

- Additive Flame Retardants

- Reactive Flame Retardants

By End-Use Industry

- Electrical and Electronics

- Automotive and Transportation

- Building and Construction

- Aerospace and Defense

- Consumer Appliances

- Industrial Machinery

By Performance

- Halogenated

- Halogen-Free

- Low Smoke Zero Halogen

By Distribution Channel

- Direct Sales

- Chemical Distributors and Wholesalers

- Specialty Compounding Partners

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Flame Retardants for Engineering Resins Market

- Albemarle Corporation

- ICL Group Ltd.

- LANXESS AG

- BASF SE

- Clariant AG

- J.M. Huber Corporation

- Italmatch Chemicals S.p.A.

- Nabaltec AG

- ADEKA Corporation

- Budenheim

- SABIC

- Daikin Industries, Ltd.

- Tosoh Corporation

- Jiangsu Yoke Technology Co., Ltd.

- RTP Company

*- List not Exhaustive