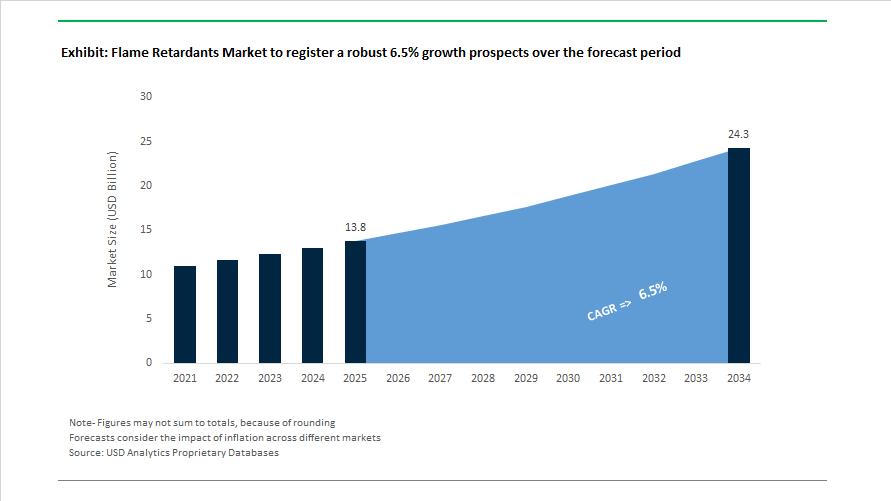

Flame Retardants Market Size 2025–2034: $13.8 Billion to $24.3 Billion at 6.5% CAGR Accelerated by EV, Electronics, and Halogen-Free Transition

The Flame Retardants Market is projected to expand from $13.8 billion in 2025 to $24.3 billion by 2034, registering a CAGR of 6.5%. Growth momentum is closely linked to electrification of mobility, miniaturization of electronics, expansion of renewable energy infrastructure, and tightening global fire safety regulations across building insulation, automotive components, and consumer appliances. Demand is shifting toward phosphorus-based, halogen-free, reactive, and low-migration flame retardant systems that comply with evolving environmental standards while maintaining high thermal stability, low smoke density, and mechanical performance in engineering plastics and polyurethane foams.

In February 2026, BASF showcased advanced recyclable flame-retardant engineering plastics at PlastIndia, demonstrating additive systems capable of maintaining fire safety ratings after multiple mechanical recycling loops. In November 2025, Clariant expanded its Exolit OP production capacity at Daya Bay, China, while simultaneously strengthening its Nylostab S-EED line in Cangzhou to support high-performance polyamide applications. That same month, BASF localized flame-retardant and hydrolysis-resistant Ultradur® PBT grades in India, enhancing supply chain responsiveness for electric vehicle battery housings and consumer electronics enclosures. In November 2025, Clariant and FUHUA announced a joint venture to construct a phosphorus-based flame retardant production facility in Leshan, China, targeting halogen-free solutions for automotive and electronics applications.

During 2025, product innovation intensified across reactive and polymeric flame retardant chemistries. At K 2025, LANXESS launched Levagard 2100, a reactive phosphorus-based phosphonate designed to chemically bond into rigid polyurethane and polyisocyanurate insulation matrices, reducing additive migration and volatile organic compound emissions. LANXESS also introduced Emerald Innovation 5000, a polymeric brominated flame retardant engineered to prevent blooming in engineering plastics, ensuring long-term fire performance stability. In Q1 2025, ICL Group reported increased flame retardant sales volumes in its Industrial Products segment, signaling recovery in electronics manufacturing and renewed demand for high-purity bromine-based fire safety additives.

Earlier developments in 2024 reinforced regulatory-driven portfolio realignment. In October 2024, Albemarle expanded its SAYTEX® brominated flame retardant portfolio, presenting lifecycle data positioning certain brominated grades as lower greenhouse gas alternatives in automotive applications. In September 2024, Asahi Kasei launched LASTAN™, a flame-retardant nonwoven fabric engineered for EV battery systems with thermal resistance up to 1,300°C, addressing thermal runaway mitigation requirements. In March 2024, Azelis secured exclusive distribution rights for LANXESS phosphorus flame retardants across key European CASE markets, strengthening regional penetration of halogen-free technologies. During late 2024 and into 2025, Clariant introduced a melamine-free Exolit AP variant aligned with SVHC-free building material standards, reinforcing the transition toward safer intumescent coatings and fire-stop systems.

Trends and Opportunities in the Flame Retardants Market

Regulatory-Driven Phase-Out of Halogenated Flame Retardants Across Core End-Use Industries

A coordinated regulatory push across Europe and North America is accelerating the phase-out of brominated flame retardants and forcing downstream industries to redesign material systems. In October 2025, the European Commission adopted Delegated Regulation (EU) 2025/1482 under the POP Recast, reducing the allowable concentration of PBDEs in products from 500 mg/kg to 10 mg/kg with immediate effect. Transitional thresholds for recycled materials are set to decline further to 200 mg/kg by December 2027, effectively eliminating halogenated flame retardants from EU-bound electronics, appliances, and building materials.

In the United States, regulatory pressure has followed a similar trajectory. The U.S. EPA finalized amendments to TSCA Section 6(h) in October 2024, setting a 0.1% by weight limit for decaBDE in products and articles. The rule also introduced stringent worker exposure controls and zero-discharge requirements for water releases during manufacturing. Together, these measures are pushing manufacturers to adopt phosphorus-based, nitrogen-based, and mineral flame retardants such as aluminum trihydrate and magnesium hydroxide.

Producers are responding with targeted capacity expansion for halogen-free alternatives. In October 2025, Clariant completed a CHF 100 million investment at its Daya Bay facility in China, expanding production of its Exolit OP phosphinate range. The investment is strategically aligned with rising demand from Asian electronics, electrical infrastructure, and e-mobility markets that must now comply with global halogen-free specifications to access export markets.

Commercialization of Reactive and Bio-Based Flame Retardant Systems

Beyond regulatory substitution, the market is moving toward structurally integrated flame retardancy. Reactive flame retardants that chemically bond to polymers are gaining preference over additive systems that can migrate, volatilize, or degrade mechanical properties over time. This shift is particularly visible in engineering plastics and fiber-reinforced composites, where long-term performance stability is critical.

In late 2024, LANXESS introduced Emerald Innovation NH 500, a phosphorus-based flame retardant designed for glass-fiber-reinforced polyamides such as PA6 and PA66. The product addresses a long-standing challenge in engineering thermoplastics by maintaining tensile strength and impact resistance while achieving stringent fire performance ratings.

At the same time, bio-based flame retardants are moving from research to early commercialization. In May 2025, Fraunhofer WKI presented translucent fire-protection coatings based on plant-derived phytic acid at LIGNA 2025. These systems convert agricultural byproducts into ammonium phytates suitable for wood furniture and interior applications, combining fire resistance with low toxicity and renewable content.

Public funding is accelerating this transition. In 2025, projects supported by Germany’s Federal Ministry of Food and Agriculture began scaling the use of lignin and other agricultural residues as active flame-retardant components in construction adhesives. This trend reflects a broader move toward circular, bio-based material systems in the building sector, where embodied carbon is becoming a procurement criterion alongside fire performance.

Critical Safety Enablers for Electric Vehicle Battery Architectures

Electric vehicles have transformed flame retardants into a high-margin, safety-critical materials segment. Battery packs must withstand thermal runaway events exceeding 1,000°C while preventing flame propagation between cells, creating demand for advanced flame-retardant polymers, coatings, and insulation systems.

China’s mandatory standard GB 38031-2025, taking effect in July 2026, introduces rigorous requirements for thermal propagation resistance and post-fast-charging safety. Battery systems must now demonstrate the ability to delay fire spread for a minimum of five minutes, forcing OEMs and Tier-1 suppliers to upgrade material specifications across housings, busbars, and insulating components.

In response, SABIC and Clariant showcased next-generation halogen-free solutions at K 2025. Clariant’s Exolit OP 1242 TP and 1266 TP are engineered for 800-volt architectures, achieving UL 94 V-0 ratings at wall thicknesses as low as 0.4 mm while delivering a Comparative Tracking Index of 600 volts. These properties are critical for high-voltage insulation in compact battery designs.

Metal-to-plastic substitution is amplifying this opportunity. SABIC’s STAMAX FR resins demonstrated resistance to a 1,100°C flame for five minutes without burn-through, compared with aluminum plates that typically fail within 30 seconds under similar conditions. This performance gap is driving adoption of intumescent thermoplastic compounds in battery trays and covers, creating a structurally attractive growth avenue for flame retardant suppliers embedded in EV material platforms.

Intumescent Protection for Structural Steel and Mass Timber Construction

Decarbonization-driven construction trends are opening a parallel growth corridor for intumescent flame retardants in mass timber and hybrid structures. The 2024 International Building Code and International Fire Code significantly expanded allowances for Type IV mass timber buildings. Under the updated code, Type IV-B structures may leave 100% of beams and ceilings exposed, provided they achieve fire-resistance ratings of 60 to 120 minutes through approved intumescent treatments.

This regulatory shift is accelerating demand for advanced coatings and fire-integrated adhesives. The FireSafe-CLT project, updated in May 2025 through collaboration between Jowat and TU Braunschweig, demonstrated the feasibility of embedding bio-based flame retardants directly into cross-laminated timber adhesives. This approach ensures fire protection is inherent to the material rather than dependent on surface treatments, improving durability and lifecycle compliance.

As mass timber buildings scale to 18 stories and beyond, steel connectors and fasteners have emerged as critical fire-risk points. Protecting these components with high-performance intumescent coatings represents a high-value niche within the broader flame retardants market. Specialty coating suppliers capable of delivering thin-film, durable, and aesthetically acceptable intumescent systems are positioned to capture disproportionate value as timber-hybrid construction expands globally.

Flame Retardants Market Share and Segmentation Insights

Non-Halogenated Flame Retardants Lead Market Transformation Amid Regulatory and Sustainability Pressures

Non-Halogenated Flame Retardants accounted for 58.70% of the Flame Retardants Market share in 2025, establishing them as the dominant technology category across global fire safety materials. These flame retardants—including aluminum trihydrate (ATH), magnesium hydroxide, phosphorus-based compounds, and nitrogen-based additives—are increasingly preferred due to their lower environmental impact, reduced toxic emissions during combustion, and compliance with evolving global chemical regulations. Regulatory frameworks such as RoHS (Restriction of Hazardous Substances), WEEE directives, and restrictions on certain halogenated compounds associated with PFAS concerns have accelerated the shift away from brominated and chlorinated flame retardants, particularly in Europe and North America. A major development shaping the market in 2025 is the rapid expansion of phosphorus-based non-halogenated flame retardant technologies. These materials offer improved thermal stability, char formation efficiency, and compatibility with engineering plastics such as polyamide, polycarbonate, and epoxy resins, enabling their use in high-performance applications previously dominated by brominated systems. As a result, phosphorus-based flame retardants are gaining strong adoption across electrical components, automotive electronics, and high-temperature polymer systems, reinforcing the structural shift toward halogen-free flame retardant materials in the global flame retardants market.

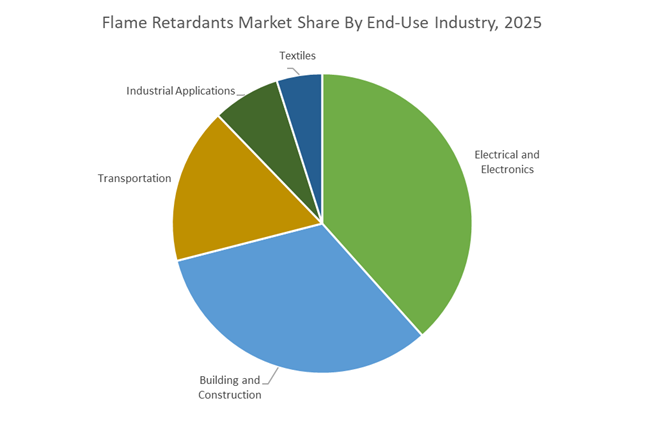

Electrical and Electronics Industry Drives Largest Demand for Advanced Flame Retardant Materials

Electrical and Electronics accounted for 38.40% of the Flame Retardants Market share in 2025, making it the most significant end-use sector for fire-resistant additives. Flame retardants play a critical role in enhancing fire safety and thermal stability within electronic components, including printed circuit boards (PCBs), electrical connectors, wire and cable insulation, semiconductor housings, and consumer electronics enclosures. Electrical faults, overheating components, and short circuits can quickly trigger fire propagation, making flame retardant materials essential for meeting strict global safety standards such as UL 94 flammability ratings and IEC 60335 electrical safety requirements. In 2025, the electronics industry is experiencing a major shift driven by device miniaturization and increasing power density. As smartphones, laptops, electric vehicles, and industrial electronics become smaller yet more powerful, internal operating temperatures rise while available material space decreases. This trend is pushing manufacturers to develop high-efficiency flame retardant formulations that deliver UL V-0 fire resistance at significantly lower additive loadings, preserving mechanical strength and electrical performance in advanced polymers. Consequently, next-generation flame retardants with high thermal stability, low smoke generation, and improved polymer compatibility are gaining widespread adoption across the rapidly evolving electronics manufacturing and electrical components industry.

Competitive Landscape in Flame Retardants Market

LANXESS AG Expands Reactive Phosphorus and Sustainable Brominated Solutions

LANXESS AG maintains one of the industry’s most comprehensive portfolios spanning brominated flame retardants and phosphorus-based flame retardants. Its Levagard® series leads in organophosphorus chemistries, while Emerald Innovation® represents advanced polymeric brominated solutions engineered for high-performance engineering plastics. During 2025 and 2026, LANXESS emphasized Levagard® 2100, a reactive phosphonate that chemically bonds to polyurethane matrices, significantly reducing volatile organic compound emissions and additive migration in flexible foams. In April 2025, the company finalized its portfolio transformation by divesting its Urethane Systems business, positioning itself as a pure-play specialty chemicals manufacturer. Backward integration into phosphorus building blocks in Germany strengthens supply chain resilience and cost control. Additionally, ramp-up of Emerald Innovation 5000 provides a sustainable alternative to decabromodiphenyl ethane for demanding automotive and electrical applications, reinforcing LANXESS’ role in next-generation flame retardant chemistry.

Albemarle Corporation Leads High-Performance Brominated Fire Safety for Electronics

Albemarle Corporation is the global leader in bromine-based flame retardants, with a strong footprint in electrical and electronics and electric vehicle battery protection. Its SAYTEX® portfolio includes high-efficacy brominated flame retardants engineered for circuit boards, connectors, and charging infrastructure components. The introduction of SAYTEX ALERO™ in 2025 addressed extreme fire safety requirements of high-voltage EV architectures, supporting thermal runaway mitigation strategies. Albemarle emphasizes sustainability through bromine chemistry, highlighting lower energy intensity during production compared to certain phosphorus alternatives. The company is also investing in circular economy technologies aimed at recovering brominated flame retardants from post-consumer electronic waste streams. By combining high thermal stability, strong char formation performance, and recycling initiatives, Albemarle maintains dominance in high-stress polymer systems used in advanced electronics and automotive platforms.

Clariant AG Strengthens Halogen-Free Solutions for E-Mobility and High-Voltage Systems

Clariant AG is widely recognized as the global leader in halogen-free flame retardants, particularly organophosphorus-based Exolit® OP and ammonium polyphosphate-based Exolit® AP solutions. The company invested more than CHF 100 million in its Daya Bay facility, with the second major production line fully operational in late 2025 to support the Asian electric vehicle supply chain. Clariant’s Exolit OP 1266 (TP) was specifically engineered for polybutylene terephthalate applications requiring a Comparative Tracking Index of 600V, addressing safety needs in high-voltage connectors and EV charging modules. Recognition through the 2025 Schneider Electric Outstanding Supplier Award underscores its strategic importance within the global electrical value chain. With large-scale hubs in Knapsack and Daya Bay, Clariant’s local-for-local supply model ensures secure sourcing for OEMs transitioning toward sustainable, halogen-free flame retardant systems.

ICL Group Leverages Bromine Resources and Reactive Phosphorus Technologies

ICL Group benefits from direct access to concentrated bromine resources from the Dead Sea, enabling structural cost advantages and low energy intensity production. Its PolyQuel® polymeric bromine solutions and VeriQuel™ phosphorus-based flame retardants target building insulation foams and energy storage systems where thermal stability and long-term performance are critical. In 2025, ICL intensified deployment of its SAFR® methodology, a proprietary tool allowing customers to evaluate sustainability and fire safety profiles tailored to specific polymer applications. The company is advancing reactive flame retardant chemistries that integrate into polymer backbones, reducing migration and improving durability. ICL is also developing tracer technologies embedded in plastics to improve identification and recycling of flame-retardant materials. This upstream resource control combined with downstream sustainability analytics strengthens ICL’s strategic position in the global flame retardants market.

Huber Engineered Materials Dominates Mineral-Based Halogen-Free Flame Retardants

Huber Engineered Materials leads the global market for mineral-based, non-halogenated flame retardants, particularly aluminum trihydrate and magnesium hydroxide chemistries marketed under Martinal® and Magnifin® brands. Following the integration of Magnifin, Huber reinforced its dominance in the low-smoke, zero-halogen cable compound segment, which accounts for nearly 42% of demand in the low-smoke flame retardant market as of 2026. These mineral flame retardants release water upon decomposition, diluting flammable gases and suppressing smoke generation in wire and cable insulation. Recent innovation in surface-treated mineral grades allows higher filler loading without compromising polymer flexibility, enhancing mechanical performance in construction and transportation applications. Huber’s halogen-free positioning aligns strongly with life-safety regulations governing public infrastructure, tunnels, and rail interiors, securing its leadership in non-toxic flame retardant systems.

China: Joint Ventures and Green Chemistry Mandates Reshape Domestic Supply

China’s flame retardants market in the 2025–2026 cycle is being redefined by joint ventures, electric vehicle demand, and a decisive regulatory shift toward non-halogenated systems. A pivotal development occurred in November 2025 when Clariant partnered with FUHUA to establish a joint venture focused on next-generation phosphorus-based, non-halogenated flame retardants. This collaboration is structured for mass-scale production and is directly aligned with China’s rapidly expanding construction materials and automotive components sectors, where halogen-free compliance is increasingly non-negotiable.

Capacity expansion is reinforcing this shift. Clariant’s second Exolit OP production line at its Daya Bay site became operational following a CHF 100 million investment, ensuring localized availability for EV battery systems and consumer electronics. At the policy level, the MIIT 2026 Green Growth Plan mandates that 90% of new high-end fine chemicals used in construction must meet enhanced environmental safety profiles by 2026. This requirement is accelerating the replacement of brominated systems with bio-based amino acids and mineral synergists. At the same time, domestic innovators such as Jiangsu Yoke Technology are embedding AI-driven molecular modeling into R&D, cutting development cycles for customized polyolefin flame retardants by an estimated 30%. Collectively, these factors position China as a scale-driven yet compliance-focused hub for next-generation flame retardant technologies.

United States: State-Level Bans and Advanced Material Innovation

In the United States, regulatory fragmentation and innovation-led substitution are simultaneously shaping flame retardant demand. In 2025, Trinseo launched PFAS-free flame retardant grades under its Emerge brand, targeting polycarbonate and PC/ABS blends for consumer electronics. These products directly respond to mounting state-level legislative pressure to eliminate fluorinated additives while preserving mechanical and thermal performance.

Regulatory enforcement intensified further with Massachusetts Regulation 310 CMR 78.00, effective January 2025, which bans specified flame retardants such as TDCPP, TCEP, and antimony trioxide above 1,000 ppm in bedding, children’s toys, and residential furniture. Innovation is emerging alongside regulation. In November 2025, Zentek introduced a graphite gel-based fire retardant that leverages graphite’s thermal conductivity to create a physical heat barrier. This solution is being positioned for North American energy storage and battery enclosures. Looking ahead, the EPA’s early 2026 TSCA reassessment of brominated flame retardants signals a likely move toward mandatory labeling for articles containing decaBDE, reinforcing a structural transition toward non-halogenated and mineral-based alternatives.

European Union (Germany and France): Trace Contaminant Limits and Application-Specific Compliance

The European Union remains the global epicenter of regulatory stringency for flame retardants, with Germany and France at the forefront. Commission Delegated Regulation (EU) 2025/1482 revised the Unintentional Trace Contaminant limits for five PBDEs, capping recovered material content at 350 mg/kg from December 30, 2025, and tightening further to 200 mg/kg by late 2027. These thresholds are forcing recyclers and compounders to redesign material flows to avoid legacy brominated contamination.

From a materials innovation standpoint, BASF expanded production of its Ultramid T6000 polyamide in January 2025. This grade maintains dielectric strength after 1,000 thermal shock cycles and is tailored for high-power EV chargers and solar inverters. German manufacturers are also accelerating the shift toward melamine-free phosphorus solutions such as Exolit AP 422 to meet REACH requirements while preserving smoke suppression in technical textiles. Consumer safety regulation is adding another layer, with the updated EN 71-2 toy safety standard becoming fully enforceable in June 2026, mandating stricter ignition resistance and prohibiting specific flammable materials in childcare products.

India: EV-Driven Demand and Domestic Capacity Building

India’s flame retardants market is increasingly shaped by electric mobility, infrastructure expansion, and bio-based innovation. The BioE3 Policy entered its operational phase in 2025, offering fiscal incentives for lignocellulosic and biomass-derived flame retardants. This policy framework is designed to reduce reliance on imported brominated grades while fostering domestic intellectual property in sustainable fire protection materials.

Demand acceleration is closely tied to mobility electrification. The 78% budget increase for the FAME II scheme in 2024–2025 has amplified requirements for flame-retardant plastics that comply with AIS-156 battery safety standards. In response, manufacturers are prioritizing halogen-free formulations for battery enclosures, wiring, and connectors. Capacity expansion is underway in industrial corridors such as Gujarat, where Fine Organic Industries and other domestic players expanded non-silicone and mineral-based additive production in 2025. These investments support India’s Smart Cities program, where fire-rated cabling and construction materials are becoming mandatory across public infrastructure.

Strategic Snapshot: Flame Retardants Market by Country (2025–2026)

Flame Retardants Market County Level Snapshot

|

Region

|

Key Regulatory or Strategic Trigger

|

Dominant Technology Shift

|

Market Implication

|

|

China

|

MIIT green chemistry mandate

|

Phosphorus and mineral systems

|

Large-scale halogen-free substitution

|

|

United States

|

State bans and TSCA reassessment

|

PFAS-free and graphite-based solutions

|

Rapid product reformulation cycles

|

|

European Union

|

PBDE UTC limits and REACH

|

Melamine-free phosphorus chemistries

|

High compliance costs, premium materials

|

|

India

|

BioE3 and FAME II alignment

|

Bio-based and halogen-free plastics

|

Domestic capacity and import substitution

|

Flame Retardants Market Report Scope

Flame Retardants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.8 Billion

|

|

Market Size (2034)

|

$24.3 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Type (Non-Halogenated Flame Retardants, Halogenated Flame Retardants), By Application (Polyolefins, Epoxy Resins, Polyvinyl Chloride, Engineering Thermoplastics, Polyurethane, Rubber and Styrenics), By End-Use Industry (Electrical and Electronics, Building and Construction, Transportation, Textiles, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Albemarle Corporation, LANXESS AG, ICL Group Ltd., BASF SE, Clariant AG, Huber Engineered Materials, Italmatch Chemicals S.p.A., Dow Inc., Budenheim Chemicals KG, Jiangsu Yoke Technology Co., Ltd., Adeka Corporation, Daihachi Chemical Industry Co., Ltd., DIC Corporation, Thor Group, Nabaltec AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flame Retardants Market Segmentation

By Type

- Non-Halogenated Flame Retardants

- Halogenated Flame Retardants

By Application

- Polyolefins

- Epoxy Resins

- Polyvinyl Chloride

- Engineering Thermoplastics

- Polyurethane

- Rubber and Styrenics

By End-Use Industry

- Electrical and Electronics

- Building and Construction

- Transportation

- Textiles

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Flame Retardants Industry

- Albemarle Corporation

- LANXESS AG

- ICL Group Ltd.

- BASF SE

- Clariant AG

- Huber Engineered Materials

- Italmatch Chemicals S.p.A.

- Dow Inc.

- Budenheim Chemicals KG

- Jiangsu Yoke Technology Co., Ltd.

- Adeka Corporation

- Daihachi Chemical Industry Co., Ltd.

- DIC Corporation

- Thor Group

- Nabaltec AG

*- List not Exhaustive