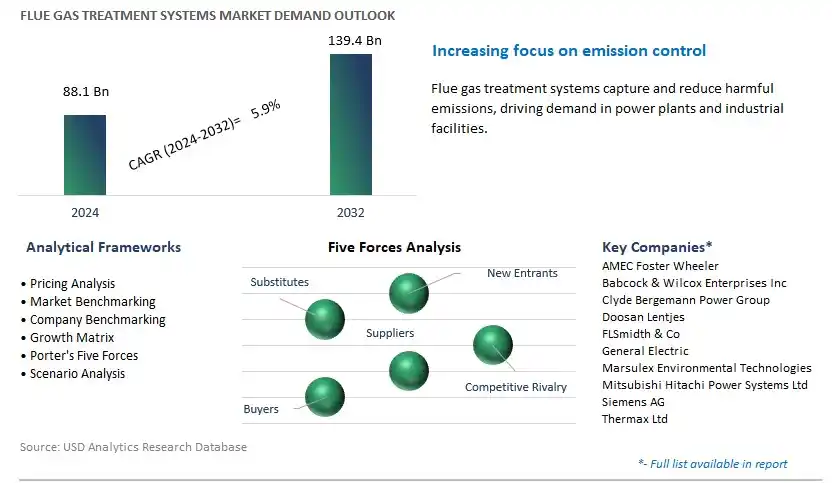

Global Flue Gas Treatment Systems Market Size is valued at $88.1 Billion in 2024 and is forecast to register a growth rate (CAGR) of 5.9% to reach $139.4 Billion by 2032.

The global Flue Gas Treatment Systems Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Pollutant Control System (Particulate Control, Flue Gas Desulfurization, DeNOx, Mercury Control, Others), By Business Type (System, Service), By End-User (Power, Cement, Iron & Steel, Non-Ferrous Metal, Chemical & Petrochemical, Others).

An Introduction to Flue Gas Treatment Systems Market in 2024

Flue gas treatment systems play a vital role in mitigating air pollution by removing harmful pollutants such as particulate matter, sulfur oxides (SOx), nitrogen oxides (NOx), and volatile organic compounds (VOCs) from industrial exhaust gases. In 2024, the market for flue gas treatment systems is witnessing rapid growth driven by stringent regulatory standards, increasing industrialization, and growing public concern over air quality. These systems employ a combination of technologies, including electrostatic precipitators, scrubbers, catalytic converters, and adsorption filters, to capture and neutralize pollutants before they are emitted into the atmosphere. Further, advancements in flue gas treatment technologies, such as multi-pollutant control systems and hybrid approaches, enable comprehensive and cost-effective solutions tailored to specific emission sources and regulatory requirements. As industries prioritize environmental stewardship and compliance, the demand for flue gas treatment systems is expected to escalate, driving further innovation and market expansion.

Flue Gas Treatment Systems Market Competitive Landscape

The market report analyses the leading companies in the industry including AMEC Foster Wheeler, Babcock & Wilcox Enterprises Inc, Clyde Bergemann Power Group, Doosan Lentjes, FLSmidth & Co, General Electric, Marsulex Environmental Technologies, Mitsubishi Hitachi Power Systems Ltd, Siemens AG, Thermax Ltd, and others.

Flue Gas Treatment Systems Market Dynamics

Market Trend: Growing Focus on Air Quality Improvement and Emissions Reduction

A prominent trend in the flue gas treatment systems market is the growing focus on air quality improvement and emissions reduction. With increasing awareness of environmental pollution and its impacts on public health and the environment, there is a heightened emphasis on implementing flue gas treatment systems to remove harmful pollutants from industrial and power plant emissions. Flue gas treatment systems, including electrostatic precipitators, fabric filters, and scrubbers, are deployed to capture particulate matter, sulfur dioxide (SO2), nitrogen oxides (NOx), and other hazardous gases from flue gas streams, thereby mitigating air pollution and complying with stringent emissions regulations. This trend reflects the industry's commitment to sustainable development, corporate responsibility, and regulatory compliance driving investment in flue gas treatment technologies to protect air quality and public health.

Market Driver: Stringent Environmental Regulations and Compliance Requirements

A key driver fueling the demand for flue gas treatment systems is the implementation of stringent environmental regulations and compliance requirements worldwide. Governments, regulatory agencies, and international bodies impose strict emission limits and air quality standards to mitigate the adverse effects of industrial emissions on the atmosphere, ecosystems, and human health. Industries operating coal-fired power plants, cement kilns, steel mills, chemical processing plants, and incinerators are required to install flue gas treatment systems to reduce pollutant emissions and achieve regulatory compliance. Additionally, the enforcement of emissions trading schemes, carbon taxes, and pollution control measures incentivizes industries to invest in flue gas treatment technologies as part of their environmental management strategies. The imperative for environmental stewardship and regulatory compliance drives market demand for flue gas treatment systems, supporting industry growth and innovation in emissions control technologies.

Market Opportunity: Adoption of Advanced and Integrated Flue Gas Treatment Solutions

Amidst the evolving landscape of the flue gas treatment systems market, there exists a significant opportunity for the adoption of advanced and integrated solutions for emissions control. Manufacturers and technology providers can capitalize on this opportunity by offering comprehensive flue gas treatment systems that combine multiple pollutant removal technologies, such as selective catalytic reduction (SCR), flue gas desulfurization (FGD), and dry scrubbing, into integrated systems. Integrated flue gas treatment solutions provide benefits such as higher removal efficiencies, reduced footprint, simplified operation, and lower lifecycle costs compared to individual emission control devices. Additionally, incorporating digitalization, automation, and remote monitoring capabilities into flue gas treatment systems enables real-time performance optimization, predictive maintenance, and data-driven decision-making. By offering advanced and integrated flue gas treatment solutions, companies can address the evolving needs of industries for efficient and cost-effective emissions control, secure market share, and drive sustainable growth in the global flue gas treatment systems market.

Flue Gas Treatment Systems Market Share Analysis: Flue Gas Desulfurization (FGD) segment generated the highest revenue in 2024

The Flue Gas Desulfurization (FGD) segment is the largest in the Flue Gas Treatment Systems Market. Flue gas desulfurization systems are essential for controlling sulfur dioxide (SO2) emissions, a major contributor to air pollution and acid rain formation. With increasing environmental regulations aimed at reducing harmful emissions from industrial and power generation facilities, the demand for FGD systems has surged significantly. FGD systems utilize various techniques, including wet scrubbing, dry scrubbing, and semi-dry scrubbing, to remove sulfur dioxide from flue gas streams. Wet FGD systems, in particular, are widely adopted due to their high efficiency and reliability in sulfur removal. Additionally, FGD systems play a crucial role in mitigating environmental impact and ensuring compliance with emissions standards, making them indispensable for industries subject to strict regulatory requirements. Moreover, the widespread adoption of FGD systems is driven by the growing awareness of environmental sustainability and the need to address air quality concerns globally. Over the forecast period, the Flue Gas Desulfurization segment's critical role in emissions control and environmental protection solidifies its position as the largest segment in the Flue Gas Treatment Systems Market.

Flue Gas Treatment Systems Market Share Analysis: Service is poised to register the fastest CAGR over the forecast period

The Service segment is the fastest-growing segment in the Flue Gas Treatment Systems Market. As industries face increasingly stringent environmental regulations and strive for sustainability, there is a growing demand for comprehensive service solutions to optimize the performance, efficiency, and compliance of flue gas treatment systems. Service providers offer a range of services, including system maintenance, performance optimization, upgrades, retrofits, and consulting services, to help industries maximize the effectiveness and lifespan of their flue gas treatment systems. Moreover, outsourcing flue gas treatment system services allows companies to focus on their core operations while leveraging the expertise and specialized capabilities of service providers. Additionally, the shift towards service-based business models offers cost-saving opportunities for industries, as they can benefit from flexible service contracts tailored to their specific needs, reducing upfront capital investments and long-term operational costs. With the increasing emphasis on operational efficiency, emissions reduction, and regulatory compliance, the Service segment is poised for rapid growth as industries prioritize comprehensive service solutions to address their flue gas treatment needs.

Flue Gas Treatment Systems Market Share Analysis: Power segment generated the highest revenue in 2024

The Power segment stands as the largest in the Flue Gas Treatment Systems. Power generation facilities, including coal-fired, natural gas-fired, and biomass power plants, are major contributors to air pollution and greenhouse gas emissions. As environmental regulations become increasingly stringent worldwide, power plants are under pressure to reduce their emissions of pollutants such as sulfur dioxide (SO2), nitrogen oxides (NOx), particulate matter, and mercury. Flue gas treatment systems are crucial for power plants to comply with emissions standards and mitigate environmental impact. These systems include various technologies such as flue gas desulfurization (FGD), selective catalytic reduction (SCR), electrostatic precipitators (ESP), and fabric filters (FF), which remove pollutants from flue gas streams before they are emitted into the atmosphere. Additionally, the growing demand for electricity, driven by population growth, urbanization, and industrialization, further fuels the adoption of flue gas treatment systems in the power generation sector. Over the forecast period, the Power segment's significant contribution to emissions control and environmental protection solidifies its position as the largest segment in the Flue Gas Treatment Systems Market.

Flue Gas Treatment Systems Market

By Pollutant Control System

Particulate Control

Flue Gas Desulfurization

DeNOx

Mercury Control

Others

By Business Type

System

Service

By End-User

Power

Cement

Iron & Steel

Non-Ferrous Metal

Chemical & Petrochemical

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Flue Gas Treatment Systems Companies Profiled in the Study

AMEC Foster Wheeler

Babcock & Wilcox Enterprises Inc

Clyde Bergemann Power Group

Doosan Lentjes

FLSmidth & Co

General Electric

Marsulex Environmental Technologies

Mitsubishi Hitachi Power Systems Ltd

Siemens AG

Thermax Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Flue Gas Treatment Systems Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Flue Gas Treatment Systems Market Size Outlook, $ Million, 2021 to 2032

3.2 Flue Gas Treatment Systems Market Outlook by Type, $ Million, 2021 to 2032

3.3 Flue Gas Treatment Systems Market Outlook by Product, $ Million, 2021 to 2032

3.4 Flue Gas Treatment Systems Market Outlook by Application, $ Million, 2021 to 2032

3.5 Flue Gas Treatment Systems Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Flue Gas Treatment Systems Industry

4.2 Key Market Trends in Flue Gas Treatment Systems Industry

4.3 Potential Opportunities in Flue Gas Treatment Systems Industry

4.4 Key Challenges in Flue Gas Treatment Systems Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Flue Gas Treatment Systems Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Flue Gas Treatment Systems Market Outlook by Segments

7.1 Flue Gas Treatment Systems Market Outlook by Segments, $ Million, 2021- 2032

By Pollutant Control System

Particulate Control

Flue Gas Desulfurization

DeNOx

Mercury Control

Others

By Business Type

System

Service

By End-User

Power

Cement

Iron & Steel

Non-Ferrous Metal

Chemical & Petrochemical

Others

8 North America Flue Gas Treatment Systems Market Analysis and Outlook To 2032

8.1 Introduction to North America Flue Gas Treatment Systems Markets in 2024

8.2 North America Flue Gas Treatment Systems Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Flue Gas Treatment Systems Market size Outlook by Segments, 2021-2032

By Pollutant Control System

Particulate Control

Flue Gas Desulfurization

DeNOx

Mercury Control

Others

By Business Type

System

Service

By End-User

Power

Cement

Iron & Steel

Non-Ferrous Metal

Chemical & Petrochemical

Others

9 Europe Flue Gas Treatment Systems Market Analysis and Outlook To 2032

9.1 Introduction to Europe Flue Gas Treatment Systems Markets in 2024

9.2 Europe Flue Gas Treatment Systems Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Flue Gas Treatment Systems Market Size Outlook by Segments, 2021-2032

By Pollutant Control System

Particulate Control

Flue Gas Desulfurization

DeNOx

Mercury Control

Others

By Business Type

System

Service

By End-User

Power

Cement

Iron & Steel

Non-Ferrous Metal

Chemical & Petrochemical

Others

10 Asia Pacific Flue Gas Treatment Systems Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Flue Gas Treatment Systems Markets in 2024

10.2 Asia Pacific Flue Gas Treatment Systems Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Flue Gas Treatment Systems Market size Outlook by Segments, 2021-2032

By Pollutant Control System

Particulate Control

Flue Gas Desulfurization

DeNOx

Mercury Control

Others

By Business Type

System

Service

By End-User

Power

Cement

Iron & Steel

Non-Ferrous Metal

Chemical & Petrochemical

Others

11 South America Flue Gas Treatment Systems Market Analysis and Outlook To 2032

11.1 Introduction to South America Flue Gas Treatment Systems Markets in 2024

11.2 South America Flue Gas Treatment Systems Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Flue Gas Treatment Systems Market size Outlook by Segments, 2021-2032

By Pollutant Control System

Particulate Control

Flue Gas Desulfurization

DeNOx

Mercury Control

Others

By Business Type

System

Service

By End-User

Power

Cement

Iron & Steel

Non-Ferrous Metal

Chemical & Petrochemical

Others

12 Middle East and Africa Flue Gas Treatment Systems Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Flue Gas Treatment Systems Markets in 2024

12.2 Middle East and Africa Flue Gas Treatment Systems Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Flue Gas Treatment Systems Market size Outlook by Segments, 2021-2032

By Pollutant Control System

Particulate Control

Flue Gas Desulfurization

DeNOx

Mercury Control

Others

By Business Type

System

Service

By End-User

Power

Cement

Iron & Steel

Non-Ferrous Metal

Chemical & Petrochemical

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

AMEC Foster Wheeler

Babcock & Wilcox Enterprises Inc

Clyde Bergemann Power Group

Doosan Lentjes

FLSmidth & Co

General Electric

Marsulex Environmental Technologies

Mitsubishi Hitachi Power Systems Ltd

Siemens AG

Thermax Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Pollutant Control System

Particulate Control

Flue Gas Desulfurization

DeNOx

Mercury Control

Others

By Business Type

System

Service

By End-User

Power

Cement

Iron & Steel

Non-Ferrous Metal

Chemical & Petrochemical

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)