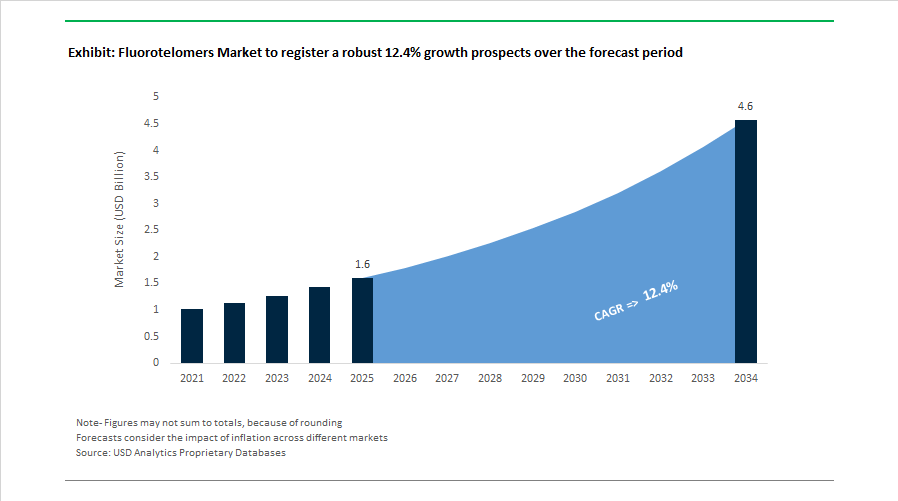

Fluorotelomers Market Size 2025–2034: $1.6 Billion to $4.6 Billion at 12.4% CAGR Amid PFAS Exit, Regulatory Overhaul and Non-Fluorinated Substitution

The Fluorotelomers Market is projected to grow from $1.6 billion in 2025 to $4.6 billion by 2034, registering a strong CAGR of 12.4%. Market dynamics are being shaped by aggressive PFAS regulatory scrutiny, supply chain restructuring, and rapid innovation in non-fluorinated surface treatment technologies. Fluorotelomers, widely used in water- and oil-repellent textiles, paper coatings, firefighting foams, and specialty fluoropolymers, are undergoing structural transformation as global manufacturers recalibrate portfolios to comply with environmental reporting mandates and evolving REACh and EPA requirements. Demand remains concentrated in high-performance semiconductor, EV, aerospace, and advanced coatings applications, even as legacy C6 and C8 chemistries face accelerated phase-out.

In early 2026, the U.S. Environmental Protection Agency advanced finalization of its comprehensive PFAS reporting rule, with submission timelines extending through November 2026. This rule compels companies to disclose historical manufacture and use of fluorotelomers and related PFAS compounds, significantly increasing compliance transparency across the sector. By January 2026, 3M confirmed the completion of its global exit from PFAS manufacturing, ending production of fluorotelomers by December 2025 and shifting focus toward supporting customer transition to non-fluorinated alternatives. Throughout 2025 and into 2026, the European Chemicals Agency’s universal PFAS restriction proposal intensified substitution programs, prompting manufacturers including Syensqo and Daikin to expand hydrocarbon-based oil- and grease-resistant coating technologies for textiles and packaging.

Strategic supply chain realignment accelerated in 2025. In August 2025, The Chemours Company entered into a partnership with SRF Limited in India to expand global fluoropolymer and fluoroelastomer supply without new capital-intensive buildouts, targeting semiconductor fabrication, electric vehicle components, and aerospace sealing systems. At China Interdye 2025, Daikin introduced hydrocarbon-based water repellent agents positioned as high-performance alternatives to fluorotelomer coatings in response to tightening textile environmental standards. In September 2025, Arkema highlighted its transition toward bio-based high-performance polymers at K2025, promoting materials such as Rilsan® Polyamide 11 as substitutes for certain fluorinated intermediates in industrial and consumer applications.

Regulatory-driven technology transformation began intensifying in 2024. In August 2024, AGC announced development of a surfactant-free fluoropolymer manufacturing process eliminating fluorinated polymerization aids, with plans to scale industrially by 2030. In August 2024, Daikin committed over $300 million globally to enhance PFAS capture and water discharge systems, achieving 99% recovery of polymerization emulsifiers in major regions and targeting 99.9% capture by 2026. In January 2024, Daikin was recognized among the Global Top 100 Innovation leaders for sustainability-focused fluoroelastomer advancements. In January 2024, Asahi India Glass completed acquisition of AIS Adhesives, strengthening regional distribution capabilities for specialty surface treatment chemicals linked to high-performance coatings.

Trends and Opportunities in the Fluorotelomers Market

Accelerated Strategic Exit from Consumer-Facing and Discretionary Applications

Mounting litigation exposure and the finalization of near-universal PFAS restrictions across Europe and North America have forced Tier-1 producers to retreat decisively from consumer-facing fluorotelomer applications. In January 2024, 3M confirmed it was on track to exit all PFAS manufacturing by the end of 2025, impacting approximately USD 1.3 billion in annual net sales. The company has already reformulated or discontinued close to 25,000 products to remove fluorotelomer linkages, signaling a broader industry retreat from textiles, cookware, cosmetics, and waterproofing agents.

This withdrawal is being reinforced by hard regulatory deadlines. From January 1, 2026, several European jurisdictions, including France and Denmark, will prohibit the manufacture and sale of PFAS-containing clothing, cosmetics, and durable water-repellent coatings. As a result, fluorotelomer-based DWR chemistries are being rapidly displaced by silicone, wax, and hydrocarbon-based alternatives. These substitutes typically offer lower durability and oil repellency, but are increasingly accepted by brands prioritizing regulatory certainty and ESG alignment over maximum performance.

Litigation risk has further accelerated consolidation. The USD 450 million settlement reached in May 2025 between 3M and the State of New Jersey underscored the long-tail financial exposure associated with legacy fluorotelomer contamination. Across the sector, producers are now concentrating residual fluorotelomer capacity solely on high-margin industrial uses where regulatory derogations or “essential use” exemptions are more likely to persist.

Intensive Pivot Toward C6 Chemistries and Non-Fluorinated Substitutes

As long-chain C8 fluorotelomers are phased out globally, R&D spending has shifted toward short-chain C6 alternatives and advanced non-fluorinated surface treatment technologies. The objective is to preserve critical performance attributes such as low surface tension, thermal stability, and chemical resistance while reducing environmental persistence and bioaccumulation risk.

In August 2024, Daikin Industries disclosed cumulative investments exceeding USD 300 million to capture PFAS from wastewater streams and transition its fluoropolymer and fluoroelastomer production to more sustainable polymerization technologies by 2025. This includes reducing reliance on traditional fluorinated emulsifiers and improving end-of-pipe capture systems, reflecting the industry’s shift from dilution strategies to containment and minimization.

Despite these efforts, performance gaps remain. Field data from aerospace and industrial hydraulics applications in mid-2025 indicate that non-fluorinated fluids still struggle to match the fire resistance and high-temperature stability of PFPE and fluorotelomer-derived systems. This mismatch is driving a growing number of applications to seek “essential use” classification, particularly in safety-critical environments where substitution could compromise system integrity.

Commercialization of PFAS Destruction and Closed-Loop Remediation Technologies

One of the most significant growth opportunities lies not in producing new fluorotelomers, but in permanently destroying legacy PFAS and fluorotelomer waste streams. The market is shifting decisively from containment and disposal toward verified molecular destruction, creating a new value chain centered on advanced chemical engineering.

In November 2025, technical audits confirmed that the PFAS Annihilator®, developed by Battelle and operated commercially by Revive Environmental, achieved destruction efficiencies exceeding 99.9% for concentrated AFFF waste. Using supercritical water oxidation, the process breaks the carbon–fluorine bond under extreme temperature and pressure conditions, eliminating the long-term liability associated with incineration or landfilling.

Public sector funding is accelerating this opportunity. In May 2025, the U.S. EPA allocated an additional USD 1 billion under the Bipartisan Infrastructure Law to support PFAS testing and treatment at public water systems. This funding is catalyzing demand for modular, on-site destruction units that prevent liability transfer and enable utilities to manage fluorotelomer-laden media without offsite disposal risks. State-led AFFF takeback programs, now active in Ohio and New Hampshire, are providing consistent feedstock volumes and establishing a repeatable remediation model with global relevance.

“Essential Use” Specialization in the Semiconductor and Defense Sectors

The semiconductor industry represents one of the most defensible, high-margin niches for fluorotelomers, underpinned by technical necessity and geopolitical priorities. In August 2025, European Chemicals Agency revised its PFAS restriction proposal to include a “continued use under risk-controlled conditions” pathway. This explicitly recognizes the dependence of advanced semiconductor manufacturing on ultra-high-purity fluorinated surfactants used in photoresist development, etching, and immersion lithography.

As chip architectures shrink below the 3 nm node, the tolerance for surface defects and fluid instability approaches zero. This elevates specialized fluorotelomers into critical-path inputs where substitution is not yet technically viable. Suppliers capable of delivering traceable, ultra-low-impurity materials stand to benefit from long-term supply contracts aligned with the EU Chips Act and parallel capacity expansions in the United States and East Asia.

Defense-related applications further reinforce this opportunity. In August 2025, the U.S. Department of Defense extended statutory waivers allowing continued AFFF use at approximately 1,000 facilities until October 2026. While this extension supports the transition toward fluorine-free foams, it also sustains interim demand for compliant fluorotelomer chemistries and bridging solutions that meet MILSPEC requirements during the conversion period.

Fluorotelomers Market Share and Segmentation Insights

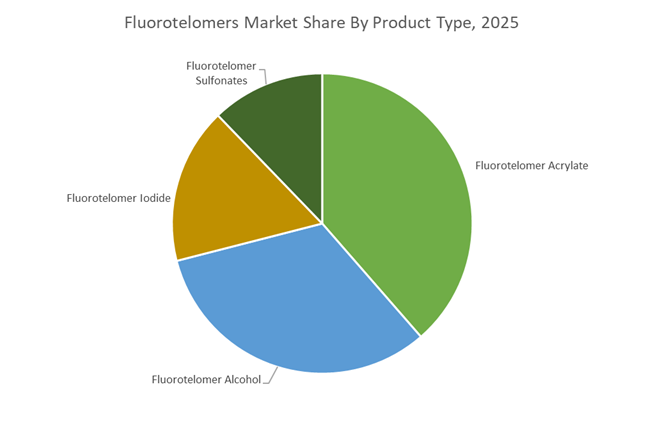

Fluorotelomer Acrylates Lead Fluorinated Surface Treatment Chemistry for Repellent Polymer Systems

Fluorotelomer Acrylates accounted for 38.60% of the Fluorotelomers Market share in 2025, making them the most widely used fluorinated intermediates in the production of high-performance water-repellent and oil-repellent coatings. These compounds serve as key building blocks for fluorinated polymers applied in textiles, paper coatings, specialty coatings, and surface treatment formulations. When polymerized, fluorotelomer acrylates impart strong hydrophobic and oleophobic properties, enabling surfaces to resist water, oils, and stains while maintaining breathability and durability. This functionality makes them critical components in protective textile finishes, food-contact paper coatings, and advanced industrial materials. In 2025, the fluorotelomer industry continues to undergo structural transformation driven by regulatory pressure on long-chain fluorinated chemistries. Historically, C8-based fluorotelomer chemistry dominated the market due to superior performance, but environmental regulations targeting long-chain PFAS compounds have pushed the industry toward C6-based fluorotelomer acrylates. These shorter-chain alternatives offer improved environmental compliance while retaining acceptable performance characteristics for commercial applications. However, increasing regulatory scrutiny in Europe and North America continues to drive research investment into next-generation fluorine-free surface treatment technologies, reshaping innovation strategies across the global fluorotelomers market.

Textile and Leather Finishing Applications Drive the Largest Demand for Fluorotelomer Surface Treatments

Textile and Leather represented 38.40% of the Fluorotelomers Market share in 2025, making it the largest end-use industry for fluorotelomer-based performance finishes. Fluorotelomer polymers are extensively used in fabric finishing and leather treatment processes to provide durable water repellency, stain resistance, and oil repellency, properties that are critical for both consumer apparel and technical textiles. These treatments are widely applied in outdoor clothing, sportswear, workwear, upholstery fabrics, automotive textiles, and protective garments, where long-lasting repellency and durability are essential. In 2025, the sector faces a growing challenge known as the “performance gap” between fluorinated and non-fluorinated finishing chemistries. Increasing regulatory pressure and sustainability initiatives are encouraging textile brands to evaluate alternatives such as silicone-based repellents, hydrocarbon-based finishes, and dendrimer-based coating systems. However, these alternatives often require higher application dosages, multiple finishing layers, or more frequent reapplication to achieve comparable repellency performance. As a result, despite regulatory scrutiny, fluorotelomer finishes continue to be widely used in applications where long-term durability, oil resistance, and consistent fabric performance are critical, maintaining strong demand within the global textile and leather processing industry.

Competitive Landscape in Fluorotelomers Market

Chemours Expands Short-Chain Fluorotelomer Leadership and Advanced Cooling Fluids

The Chemours Company remains a global leader in short-chain C6 fluorotelomer intermediates, leveraging deep vertical integration in fluorine chemistry and a broad intellectual property portfolio. The company reported $5.8 billion in net sales in 2025 and is targeting 3 to 5% consolidated growth in 2026 under its Pathway to Thrive strategy. In early 2026, Chemours finalized the $300 million divestment of its Kuan Yin TiO2 site to strengthen its balance sheet and fund sustainable chemistry investments. A mid-2025 partnership with Navin Fluorine initiated large-scale manufacturing of Opteon™ two-phase immersion cooling fluids beginning in 2026, addressing surging demand from AI-driven data centers requiring advanced thermal management. Chemours maintains strong positioning in fluorotelomer-based coatings and semiconductor materials, benefiting from global expansion in high-purity electronics applications. Its scale, patent depth, and short-chain compliance capabilities reinforce leadership in regulated fluorotelomer markets.

Daikin Invests Heavily in PFAS Capture and Sustainable Fluorochemical Production

Daikin Industries is advancing a Responsible PFAS framework through significant investment in emission control and sustainable manufacturing technologies. The company has committed more than $300 million through 2026 to enhance PFAS capture systems, targeting a 99.9% recovery rate in water discharge across global facilities. In 2025, Daikin transitioned fluoroelastomer production to more sustainable processing technologies, with full-scale commercial sales commencing in 2026. Under its FUSION 25 strategy, Daikin aims to reach ¥4,840 billion in revenue by fiscal 2025 to 2026, emphasizing green transformation and carbon neutrality. The company dominates high-purity fluorinated materials supply for semiconductor fabrication and EV battery components, including binders and electrolyte additives. Its leadership in performance fluorochemicals and environmental mitigation strengthens its position in the evolving fluorotelomer and advanced materials landscape.

AGC Accelerates Surfactant-Free Fluoropolymer Manufacturing

AGC Inc. is repositioning its Performance Chemicals segment as a strategic growth engine under its AGC plus-2026 management framework. During 2024 and 2025, AGC developed a surfactant-free fluoropolymer manufacturing process designed to reduce regulatory exposure and environmental risk, with industrial-scale deployment targeted before 2030. In 2026, the Performance Chemicals division was elevated into the Strategic Business category to accelerate differentiated material development for 5G infrastructure and mobility solutions. AGC supplies Fluon® ETFE and fluorotelomer-based intermediates used in architectural membranes, automotive fuel hoses, and specialty coatings. Through its Blue Planet initiative, AGC is targeting a 30% reduction in carbon emissions from chemical synthesis by 2030. This blend of process innovation and sustainability-driven capital allocation enhances AGC’s competitive relevance in next-generation fluorotelomer chemistry.

Arkema Strengthens PVDF and Specialty Fluoropolymer Expansion

Arkema has completed its transition into a specialty materials pure player, reporting €9.1 billion in 2025 sales and implementing a streamlined organizational structure across Adhesive Solutions, Advanced Materials, and Coating Solutions. Major PVDF and Kynar® polymer capacity expansions commissioned in 2025 are expected to contribute €310 million in incremental EBITDA in 2026, driven by accelerating EV battery and energy storage demand. Arkema inaugurated a solvent-free electrode laboratory in late 2025, advancing dry coating technologies capable of reducing CO2 emissions by 40% in battery manufacturing. As a global leader in PVDF for lithium-ion batteries, Arkema benefits from substantial production investments in the United States and China. Its high-margin specialty focus, combined with fluoropolymer expertise and electrification exposure, secures a strong competitive position in fluorotelomer-derived performance materials.

Solvay Advances Fluorosurfactant Phase-Out and Circular Fluorine Chemistry

Solvay is proactively phasing out fluorosurfactants, committing to manufacture nearly 100% of its fluoropolymers without fluorosurfactants by 2026 at its Spinetta Marengo facility. The company has quadrupled research and innovation spending on non-fluorosurfactant technologies to preserve polymer performance while meeting ESG expectations. Solvay produces high-value fluorotelomer alcohols and acrylates serving textile repellents and food packaging barrier coatings. A €40 million investment in advanced water treatment systems supports its goal of achieving technical zero emissions of fluorinated substances by late 2026. The company also maintains a strong circular economy focus, recovering and recycling fluorinated fluids from industrial waste streams. This integration of performance chemistry and environmental stewardship reinforces Solvay’s strategic resilience in the regulated fluorotelomer market.

3M Exit Reshapes Competitive Dynamics and Supply Allocation

3M’s formal exit from all PFAS manufacturing as of December 31, 2025, marks a structural inflection point for the fluorotelomers market. The discontinuation of fluoropolymers, fluorinated fluids, and PFAS-based additives eliminated approximately $1.3 billion in annual sales, creating a measurable supply gap across semiconductor, electronics, and specialty coatings applications. The company is shifting toward non-PFAS alternatives while managing legacy liabilities, prompting customers to requalify suppliers in 2026. This exit materially strengthens the relative positioning of Chemours, Daikin, and Solvay, which are expanding compliant short-chain production and capture technologies to absorb displaced demand. The competitive landscape is therefore consolidating around fewer vertically integrated producers with advanced compliance infrastructure and sustainable fluorochemical innovation capabilities.

United States: Post-PFAS Exit Realignment and Compliance-Driven Technology Shifts

The United States fluorotelomers market entered a structural reset in 2025 following the completion of 3M’s exit from all PFAS manufacturing, including fluorotelomers, effective December 31, 2025. This withdrawal has forced rapid supply chain realignment across textile finishing, paper treatment, and surface protection applications that historically relied on 3M telomer inputs. Domestic processors are now diversifying sourcing strategies while reformulating performance chemistries to meet regulatory scrutiny without sacrificing oil and water repellency. The transition is accelerating adoption of short-chain C6 fluorotelomers and alternative barrier systems, particularly in packaging and technical textiles.

Regulatory enforcement is further reshaping production economics. In 2025, the U.S. Environmental Protection Agency finalized the National Primary Drinking Water Regulation covering six PFAS, compelling fluorotelomer producers to deploy closed-loop filtration and effluent capture systems to prevent telomer discharge. Parallel pressure is emerging from the aviation sector, where the Federal Aviation Administration accelerated the transition to fluorine-free foams at commercial airports, sharply reducing demand for 6:2 fluorotelomer sulfonates traditionally used in aqueous film-forming foams. Against this backdrop, The Chemours Company’s Fayetteville Works thermal oxidizer upgrade, designed to destroy over 99.9% of PFAS air emissions, has become a reference model for compliance-led capital investment across the U.S. fluorotelomers value chain.

China: Semiconductor Self-Sufficiency and Digitally Enforced Fluorotelomer Controls

China’s fluorotelomers market is increasingly shaped by strategic industrial policy and granular environmental governance. In 2025, the Ministry of Industry and Information Technology extended targeted grants to support semiconductor-grade fluoropolymer and fluorotelomer intermediates, enabling producers such as Zhonghao Chenguang to scale ultra-pure inputs required for sub-7 nm wafer fabrication. These fluorotelomer-based intermediates are critical for chemical resistance and contamination control in advanced chip manufacturing, anchoring demand in high-value electronics rather than legacy textile applications.

At the same time, regulatory oversight is tightening. Under the Action Plan for New Pollutants Governance, China’s Ministry of Ecology and Environment added specific fluorotelomer alcohols to the strictly restricted list, mandating digital tracking for industrial sales and exports. This has increased compliance costs while improving traceability across downstream markets. In response, Daikin Industries implemented AI-driven dosing controls at its Changshu facility in October 2025, optimizing C6 fluorotelomer synthesis to minimize byproduct formation while preserving oil-repellency for food packaging. China’s trajectory reflects a dual strategy of scaling precision fluorotelomers for strategic sectors while enforcing technology-enabled environmental controls.

India: Capacity Expansion Balanced by Bio-Based Substitution Pressures

India’s fluorotelomers market is evolving through a combination of domestic capacity expansion and policy-driven substitution. In 2025, Gujarat Fluorochemicals Limited expanded its Dahej facility, targeting rising demand for fluorosurfactants and telomer-based chemistries used in electronics manufacturing and electric vehicle battery components. This investment strengthens India’s position as a regional supplier of specialty fluorotelomers, reducing reliance on imports for high-purity applications.

Concurrently, regulatory and policy signals are moderating long-term reliance on persistent chemistries. The 2025 BioE3 Policy has funded biomanufacturing R&D hubs to explore bio-based surfactants as alternatives to conventional telomers, particularly for textile repellency in export-oriented segments. Additional pressure is coming from the Food Safety and Standards Authority of India, which has enforced tighter migration limits for fluorinated grease-proofing agents effective January 2026. This has accelerated the shift toward short-chain C6 fluorotelomers and non-fluorinated barrier coatings in food packaging, reshaping demand toward compliant and lower-persistence solutions.

Germany: EU Regulatory Momentum Driving Fluorine-Free Transition

Germany serves as a regulatory bellwether for the European fluorotelomers market, with developments closely aligned to EU-wide policy. Throughout 2025, the European Chemicals Agency advanced deliberations on a near-total PFAS restriction, prompting German chemical producers to reallocate R&D budgets toward fluorine-free textile finishes and high-performance lubricants. This shift is progressively eroding demand for traditional fluorotelomers in apparel and industrial coatings, while elevating alternative chemistries.

Environmental infrastructure investments are reinforcing this transition. Arkema commissioned a large-scale activated carbon filtration unit at its Pierre-Bénite hub in early 2025 to capture telomer residues before discharge into the Rhône river system. At the regional level, Bavaria’s Circular Fluorine initiative launched in September 2025 is funding collection and destruction systems for fluorinated firefighting foams from industrial refineries. Collectively, these measures position Germany as a compliance-driven market where fluorotelomer usage is increasingly constrained to critical, non-substitutable applications.

Japan: Precision Telomer Chemistry for Energy and Safety Applications

Japan’s fluorotelomers market remains focused on precision engineering and controlled-release applications rather than volume consumption. In 2025, AGC Inc. expanded its FORBLUE portfolio, introducing ion-exchange membranes that utilize proprietary telomer chemistry for green hydrogen electrolysis. These membranes deliver chemical durability while avoiding long-chain persistence issues, aligning fluorotelomers with Japan’s decarbonization agenda.

In parallel, niche innovation is emerging in safety and maritime equipment. Sinloihi Co., Ltd. trialed nano-encapsulation techniques for fluorotelomer-based pigments in late 2025, improving light-fastness while preventing chemical leaching into marine environments. Japan’s market evolution underscores a shift toward tightly controlled, application-specific fluorotelomer use cases supported by advanced encapsulation and materials science.

Country-Level Strategic Drivers in the Fluorotelomers Market

Fluorotelomers Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Implications for Fluorotelomers

|

|

United States

|

PFAS exit and federal regulation

|

Supply chain restructuring and closed-loop compliant production

|

|

China

|

Semiconductor self-sufficiency and digital governance

|

Growth in ultra-pure C6 telomers with enforced traceability

|

|

India

|

Domestic capacity growth and bio-policy

|

Expansion in electronics demand alongside substitution pressure

|

|

Germany

|

EU-led PFAS restrictions

|

Accelerated transition toward fluorine-free alternatives

|

|

Japan

|

Energy transition and precision safety uses

|

High-performance, encapsulated telomer chemistries

|

Fluorotelomers Market Report Scope

Fluorotelomers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.6 Billion

|

|

Market Size (2034)

|

$4.6 Billion

|

|

Market Growth Rate

|

12.4%

|

|

Segments

|

By Product Type (Fluorotelomer Alcohol, Fluorotelomer Acrylate, Fluorotelomer Iodide, Fluorotelomer Sulfonates), By Method of Synthesis (Telomerization, Electrochemical Fluorination), By Application (Textiles and Apparel, Firefighting Foams, Food Packaging, Personal Care, Electronics, Industrial and Oilfield Applications), By End-Use Industry (Textile and Leather, Chemical Processing, Packaging and Paper, Automotive and Aerospace, Semiconductors and Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Chemours Company, Daikin Industries, Ltd., AGC Inc., Gujarat Fluorochemicals Limited, Arkema S.A., Solvay S.A., Honeywell International Inc., Shin-Etsu Chemical Co., Ltd., Zhonghao Chenguang Research Institute of Chemical Industry, Shanghai Huayi New Materials Co., Ltd., Indoflor, Maflon S.p.A., Tyco Fire Products, Advanced Polymer, Inc., S&D Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fluorotelomers Market Segmentation

By Product Type

- Fluorotelomer Alcohol

- Fluorotelomer Acrylate

- Fluorotelomer Iodide

- Fluorotelomer Sulfonates

By Method of Synthesis

- Telomerization

- Electrochemical Fluorination

By Application

- Textiles and Apparel

- Firefighting Foams

- Food Packaging

- Personal Care

- Electronics

- Industrial and Oilfield Applications

By End-Use Industry

- Textile and Leather

- Chemical Processing

- Packaging and Paper

- Automotive and Aerospace

- Semiconductors and Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Fluorotelomers Industry

- The Chemours Company

- Daikin Industries, Ltd.

- AGC Inc.

- Gujarat Fluorochemicals Limited

- Arkema S.A.

- Solvay S.A.

- Honeywell International Inc.

- Shin-Etsu Chemical Co., Ltd.

- Zhonghao Chenguang Research Institute of Chemical Industry

- Shanghai Huayi New Materials Co., Ltd.

- Indoflor

- Maflon S.p.A.

- Tyco Fire Products

- Advanced Polymer, Inc.

- S&D Chemicals

*- List not Exhaustive