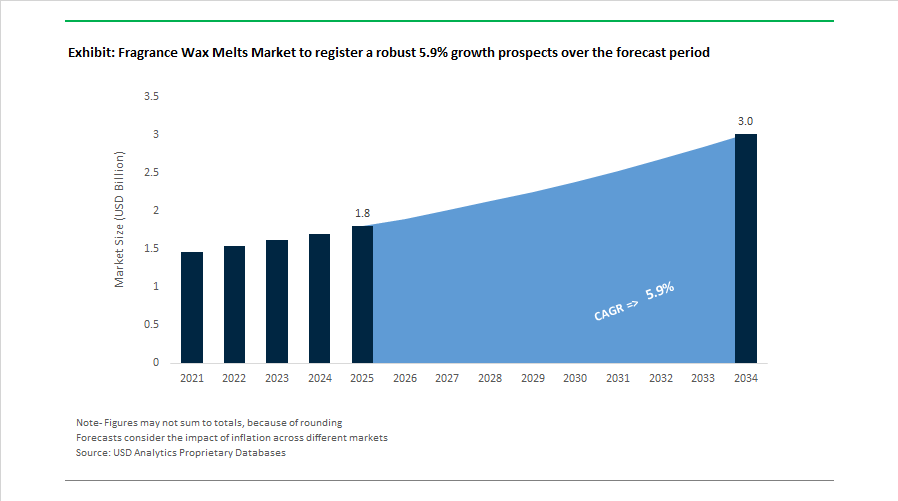

The Fragrance Wax Melts Market is projected to grow from $1.8 billion in 2025 to $3 billion by 2034, registering a CAGR of 5.9%. Market expansion is being driven by premium home fragrance positioning, subscription-based distribution models, licensed entertainment collaborations, and evolving consumer preferences toward sophisticated, hotel-inspired scent profiles. Paraffin blends, soy-based wax systems, dye-free proprietary formulations, and flame-free fragrance delivery formats are increasingly favored across North America and Europe. The rise of collectible wax bar series, immersive retail experiences, and AI-informed scent development is strengthening brand differentiation in the competitive home fragrance ecosystem.

In early 2026, Scentsy confirmed major sponsorship at the 2026 EPCOT International Flower & Garden Festival, introducing an immersive “Scent Garden” to showcase seasonal wax melt innovations. By February 2026, brands including Affinati and Village Candle reported strong consumer pivot toward “Grown-Up Vanilla” and wood-based profiles such as Vanilla & Amber and Mahogany Teakwood, reflecting demand for refined, hotel-lobby-inspired fragrance atmospheres. In February 2026, Scentsy expanded its licensed portfolio with The Aristocats Collection, reinforcing dominance in collectible wax melt segments following earlier Disney, Star Wars, and Encanto collaborations launched in 2025.

Premiumization intensified throughout 2025. In October 2025, Newell Brands introduced the Yankee Candle YC Collection, a dye-free proprietary wax blend targeting “quiet luxury” consumers through sophisticated scent profiles such as Dolce and Marine. In July 2025, Yankee Candle executed a comprehensive brand relaunch featuring updated packaging and a campaign with Brittany Snow aimed at younger demographics. In April 2025, Procter & Gamble named Vanilla Suede as the Febreze 2025 Scent of the Year, expanding its Blends Collection across wax melts and air care formats using molecular fragrance layering to evoke sanctuary-inspired environments. In early 2025, Village Candle launched its Spring Summer “Nature’s Revival” collection featuring herbal spa-inspired scents such as Yuzu Blush and Salted Sage & Woods. In January 2025, Newell Brands rolled out the “Hello, Italy!” themed collection with Mediterranean-inspired wax melts including Lemon Gelato and Capri Glow, capitalizing on experiential travel-driven fragrance narratives. Scentsy expanded its Whiff Box subscription program in January 2025, strengthening recurring revenue through curated wax melt assortments.

Marketing innovation accelerated in 2024. In January 2024, Febreze launched Romance & Desire as its Scent of the Year, emphasizing intimate, mood-setting home fragrance. That same month, UK-based Ava May Aromas partnered with Sprii to introduce livestream shopping events, enabling real-time digital engagement for flame-free wax melt purchases. In June 2025, CandleScience launched its Summer 2025 Fragrance Flight, providing artisanal producers with curated seasonal fragrance oils that shaped independent wax melt market trends.

Premiumization has become a structural trend as consumers move away from petroleum-derived paraffin toward renewable and traceable wax blends. In early 2025, the United States Department of Agriculture highlighted that soy-based waxes have shifted from niche status to a primary growth driver due to their renewable profile and contribution to domestic agricultural value chains. This has reinforced soy and hybrid wax adoption across mass-premium and artisanal brands.

Regulatory compliance is accelerating reformulation cycles. The International Fragrance Association Amendment 51 mandates that all existing fragranced products meet updated sensitizer thresholds by October 30, 2025. As a result, manufacturers are rapidly transitioning to phthalate-free and paraben-free fragrance oils. Premium brands are increasingly using QR codes on packaging to provide direct access to safety data sheets, allergen disclosures, and botanical origin tracing, turning compliance into a brand trust asset.

Consumer perception of scent has also evolved. Research cited in 2025 indicates that approximately 80% of fragrance users associate scent with mood enhancement and self-care. This has driven demand for coconut, rapeseed, and soy hybrid waxes that offer cleaner combustion and stronger hot throw performance. These higher-cost blends are effectively repositioning wax melts into a prestige home fragrance category rather than an impulse purchase item.

The fragrance wax melts market is fragmenting into functional and experiential sub-segments, where scent is positioned as a tool for emotional regulation. In May 2025, dsm-firmenich reported that 75% of consumers view fragrance as a contributor to emotional well-being. This insight has fueled the growth of mood-based wax melts, including sleep-oriented lavender blends and focus-enhancing peppermint and citrus profiles.

Parallel to functionality, the rise of scent nostalgia has reshaped creative direction. Between 2024 and 2025, online search interest for nostalgic and unisex scent profiles increased by more than 50%. Indie and premium brands are leveraging olfactory storytelling through concepts inspired by environments such as rain-soaked stone, aged leather, or vintage libraries. This shift moves the category away from generic floral and fruity classifications toward narrative-driven differentiation.

Gender-neutral positioning has further expanded the addressable market. Strategic launches in 2025 emphasized woody, amber, resinous, and mineral accords such as granite or metallic dust. These profiles align home fragrance with interior design aesthetics, appealing to consumers who view scent as part of spatial identity rather than a gendered accessory.

Scientific scrutiny of indoor air quality is creating a high-value opportunity for safety-led product innovation. A February 2025 study in Environmental Science and Technology Letters reported that terpene reactions with indoor ozone can generate nanoparticles, even in flame-free wax melt systems. This finding has accelerated interest in low-VOC, ozone-stable fragrance chemistries positioned as cleaner air formulations.

There is also growing demand for low-melt temperature waxes that liquefy between 110°F and 120°F. These blends reduce burn risk in households with children and pets while maintaining structural stability during storage and transport. Chemical suppliers are developing proprietary bio-based systems that balance safe-touch performance with consistent scent diffusion, creating differentiation in a crowded marketplace.

Certification is becoming a procurement lever. Products achieving USDA BioPreferred status, typically requiring bio-based content above 90%, are increasingly favored in large retail contracts. This aligns with corporate ESG targets set for 2026 and creates a scalable opportunity for producers able to document renewable content and lifecycle impact.

The consumable nature of wax melts positions them as ideal candidates for smart home ecosystems and recurring revenue models. In 2025, the collaboration between Pura and Pantone demonstrated how exclusive, device-linked fragrances can drive demand through connected scent platforms. This opens opportunities for wax melt producers to develop exclusive refills or digitally identifiable products compatible with app-controlled warmers.

Subscription commerce is emerging as a key growth lever. Home fragrance subscriptions expanded rapidly in 2024, and by late 2025, curated scent discovery boxes had become a leading customer acquisition tool. Data indicates that consumers are more than three times as likely to purchase full-size premium collections after engaging with limited-edition monthly assortments, improving lifetime value metrics.

Direct-to-consumer customization is further enhancing engagement. Build-your-own-blend platforms allow users to mix scent cubes and create personalized profiles, driving higher average order values through multi-pack kits. This scent mixology trend transforms wax melts into an interactive experience, strengthening brand loyalty while supporting premium pricing strategies.

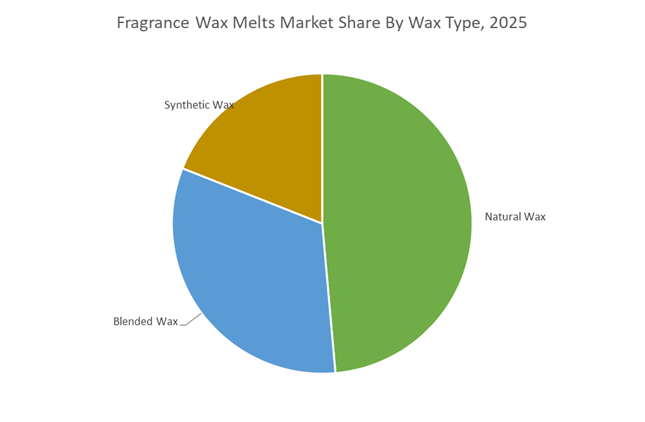

Natural Wax accounted for 48.60% of the Fragrance Wax Melts Market share in 2025, making it the leading wax type used in modern home fragrance melt products. Natural waxes—including soy wax, coconut wax, beeswax, and rapeseed wax—have gained strong market preference due to their plant-based origin, cleaner burning characteristics, and association with healthier indoor environments compared with traditional paraffin-based synthetic waxes. Consumers increasingly favor natural wax products because they are perceived as non-toxic, sustainable, and environmentally responsible, aligning with broader clean-living and eco-conscious consumer trends. These waxes also offer favorable performance characteristics for fragrance wax melts, including good scent throw, lower melting temperatures, and compatibility with essential oils and fragrance blends. In 2025, a major competitive factor within the natural wax segment is supply chain transparency and certified sourcing. Leading fragrance wax melt brands are increasingly providing detailed traceability of raw material sourcing, including non-GMO soy certification, sustainably farmed coconut wax supply chains, and responsible palm derivative sourcing under RSPO certification programs. By demonstrating transparent sourcing practices and direct relationships with agricultural producers, brands are able to position natural wax melt products at premium price points, strengthening consumer trust and differentiation in the rapidly expanding home fragrance market.

Residential applications represented 86.40% of the Fragrance Wax Melts Market share in 2025, reflecting the product’s strong association with personal home fragrance use. Fragrance wax melts are primarily purchased by consumers to enhance indoor ambiance, mask household odors, and create relaxing sensory environments within living spaces. Unlike traditional candles, wax melts offer flame-free fragrance diffusion through electric or tea-light warmers, making them an increasingly popular option for households seeking safer and more controlled fragrance experiences. Residential demand is further supported by the growing popularity of home décor, wellness rituals, and aromatherapy-inspired living environments, where fragrance plays an important role in shaping mood and comfort. In 2025, the residential wax melt market is experiencing rapid transformation driven by the expansion of direct-to-consumer fragrance subscription services. Many home fragrance brands now offer monthly scent subscription programs, delivering curated selections of seasonal, limited-edition, or themed fragrance melts directly to consumers’ homes. These subscription models create predictable recurring revenue streams for manufacturers while encouraging consumers to experiment with new scent profiles throughout the year.

Procter & Gamble, through its Febreze brand, commands dominant share of the global fragrance wax melts market. The brand’s competitive edge lies in its proprietary Odor-Clear technology, engineered to neutralize malodor molecules rather than simply masking them, positioning its wax melts as functional air care solutions. In February 2026, Febreze launched its fifth annual Scent of the Year, Tranquil Cyprus Coves, built around citrus, nectarine, and marine notes aligned with the Island Life escapism trend. A defining strategy is multi-format integration, ensuring simultaneous availability across AIR sprays, PLUG diffusers, CAR fresheners, FABRIC refreshers, and wax melts to create a unified fragrance ecosystem. Backed by the Febreze Fragrance Group’s advanced consumer trend analytics and global R&D infrastructure, P&G continues to dominate the value-luxury mass market segment.

SC Johnson, via its Glade brand, remains a strong second player in home fragrance wax melts. The company leverages high-volume retail distribution and seasonal limited editions to maintain consumer engagement. Its 2025 to 2026 Winter Collection, featuring Pumpkin Spice and Vanilla Passion Fruit variants, delivers up to 96 hours of fragrance per 8-count pack, reinforcing performance claims around scent longevity. Glade differentiates through pressed wax technology that is dry to the touch and reduces oily residue, enhancing convenience. Nearly 44% of new product launches emphasize eco-certified fragrance ingredients and sustainable packaging under its Green Home positioning. Additionally, compact 3.1 oz format designs address minimalist home decor trends and compatibility with modern wax warmers.

Yankee Candle, owned by Newell Brands, remains a dominant force in the gifting and specialty retail segment. The company has transitioned its wax melt portfolio to plant-based blends using soy and coconut wax to improve clean burn characteristics and fragrance throw authenticity. Its Well Living Collection integrates essential oils and natural fibers to target the fast-growing aromatherapy and wellness-driven home fragrance segment in 2026. Yankee Candle is repositioning its portfolio around fragrance families such as Floral, Fresh, and Woody, simplifying consumer navigation while emphasizing emotional benefits like relaxation and focus. With over five decades of brand heritage and premium fragrance craftsmanship, the company maintains strong appeal in the mid-premium wax melt segment.

Scentsy dominates the direct-to-consumer wax melt segment through its global consultant network and experience-driven marketing model. In 2025 and 2026, the company expanded licensed collections featuring global entertainment properties such as Star Wars, Encanto, and Lilo & Stitch, increasing relevance among millennial and Gen Z consumers. The introduction of the Whiff Box monthly subscription leverages AI to personalize fragrance selections based on user purchase history and scent preferences. Scentsy places equal emphasis on warmer aesthetics, positioning products as decorative home accents rather than simple air fresheners. Its strong position in soy wax melts aligns with rising demand for eco-friendly and plant-based wax alternatives, making it a key growth driver in sustainable home fragrance.

Reckitt Benckiser’s Air Wick brand has strong penetration in Europe and North America. The company is advancing smart fragrance integration, developing wax warmers compatible with mobile app control and voice-enabled ecosystems such as Alexa and Google Home. This connectivity enhances automation and scent scheduling in modern households. Air Wick is leveraging its health and hygiene expertise to promote wellness-oriented fragrances tested for mood enhancement and stress relief. The brand is also expanding essential oil-infused wax melts to compete with artisanal aromatherapy brands gaining traction in specialty retail. This intersection of technology, automation, and functional fragrance strengthens Reckitt’s competitive positioning.

Nest Fragrances represents the prestige tier of the fragrance wax melts market, competing on olfactory complexity and luxury presentation. The brand uses perfume-grade fragrance oils consistent with its fine fragrance portfolio, enabling scent layering across candles, diffusers, and wax melts. In 2026, Nest experienced increased B2B demand from luxury hotels and boutique wellness centers aligned with the spa and relaxation trend. Its niche premiumization strategy emphasizes storytelling, artistic glass packaging, and sophisticated fragrance blends such as Charcoal and Birch. By maintaining high price points and focusing on experiential luxury, Nest strengthens its foothold in the high-margin segment of the global wax melts market.

The United States fragrance wax melts market is entering a structurally important phase where regulatory scrutiny, digital integration, and consumer safety narratives are collectively reshaping product development and marketing strategies. In 2025, intensified reviews by the Environmental Protection Agency around volatile organic compounds in home fragrance products accelerated the shift toward clean-label positioning. Manufacturers are increasingly aligning wax melt formulations with MADE SAFE certification requirements, prioritizing phthalate-free fragrance oils and transparent ingredient disclosures. This regulatory environment is reinforcing trust-based purchasing behavior among health-conscious consumers and is materially influencing supplier qualification across retail and direct-to-consumer channels.

Product innovation is moving in parallel with connected-home adoption. In 2025, Pura, working alongside established scent houses, introduced smart-controlled wax warmers that allow mobile-based scheduling and intensity modulation. This integration of wax melts into smart home ecosystems positions the category closer to premium air care devices rather than traditional candles. Material substitution is another defining trend. Data from the United States Department of Agriculture confirms rising use of domestically sourced soy wax, strengthening the appeal of soy and beeswax melts as renewable alternatives to petroleum-derived paraffin.

Safety advocacy is further accelerating adoption. With public statistics highlighting an average of nearly 20 candle-related home fires per day, the National Candle Association and leading brands such as Yankee Candle are actively promoting wax melts as the flameless safety standard for 2026. Commercial models are also evolving. In early 2026, Scentsy expanded its Midwest logistics footprint to support growth in its subscription-based Scent of the Month program. At the premium end, Bath & Body Works introduced a gourmand-focused Culinary Curiosities wax melt line in late 2025, leveraging proprietary ScentTrack technology to recreate layered bakery aromas without synthetic aftertastes.

The United Kingdom fragrance wax melts market is being reshaped by post-Brexit regulatory tightening and a clear shift toward premium gifting formats. Updated Classification, Labelling, and Packaging rules effective in late 2025 now require more granular allergen disclosures for wax melts, placing compliance pressure on small artisanal sellers operating via Etsy and Shopify. This regulatory shift is increasing documentation and reformulation costs while favoring brands with in-house regulatory expertise and compliant fragrance oil sourcing.

Packaging regulation is equally influential. Amendments to the Plastic Packaging Tax in 2025 have compelled major suppliers such as Candle Shack to replace plastic clamshell packaging with biodegradable wood-pulp and recycled cardboard formats. This transition is reinforcing sustainability credentials at the point of sale and aligning wax melts with broader environmental purchasing criteria. On the demand side, premiumization is accelerating. Industry publications in late 2025 highlight luxury wax melt bars designed to resemble chocolate slabs as the fastest-growing gift-oriented format, particularly during seasonal retail cycles.

Fragrance formulation standards are also tightening. UK fragrance houses, including CPL Aromas, completed compliance with the International Fragrance Association 51st Amendment by October 2025, phasing out prohibited substances such as 3-Acetyl-2,5-dimethylfuran due to genotoxicity concerns. This has elevated formulation transparency and reinforced the role of IFRA-aligned suppliers within the UK wax melt ecosystem.

China’s fragrance wax melts market is distinguished by cultural integration, experiential scent marketing, and rapid digital commerce adoption. In 2025, the Ministry of Culture and Tourism reported strong growth in New Chinese Style home fragrance concepts. Wax melts are increasingly used to deliver traditional scents such as osmanthus and sandalwood during Lunar New Year and Lantern Festival periods, positioning the category as both modern and culturally resonant.

Commercial demand is expanding beyond residential use. ScentAir expanded its China operations in 2025, targeting boutique hotels in Shanghai and Beijing with industrial-grade wax melting systems designed for controlled scent diffusion. This highlights growing acceptance of wax-based fragrance delivery in hospitality environments. Distribution dynamics are equally transformative. National media sources indicate that more than 40% of niche wax melt sales now originate from scent storytelling-driven livestreaming on platforms such as Douyin and Xiaohongshu, where influencer narratives and cultural symbolism significantly influence conversion rates.

India’s fragrance wax melts market is developing through a combination of festive demand, export-oriented manufacturing, and wellness positioning. Seasonal gifting plays a decisive role. In October 2025, IRIS Home Fragrances launched Diwali-specific gift sets featuring wax melts as smoke-free alternatives to oil-based diyas, aligning modern home fragrance consumption with traditional celebrations.

Export capability is strengthening. The Ministry of Commerce and Industry reported rising exports of natural wax melts to the European Union, supported by a ₹200 crore investment in organic essential oil extraction facilities in Uttar Pradesh. This upstream investment is improving traceability and compliance with European sustainability and allergen standards. Domestically, government-backed wellness initiatives in 2025 have increased adoption of wax melts within urban yoga studios and spa centers, positioning aromatherapy wax melts as tools for stress management and mental wellness rather than purely decorative products.

|

Country |

Regulatory or Cultural Driver |

Key Innovation Focus |

Market Direction |

|

United States |

VOC scrutiny and consumer safety advocacy |

Smart warmers, soy and beeswax, gourmand scents |

Subscription growth, flameless positioning |

|

United Kingdom |

Post-Brexit CLP and packaging regulation |

Luxury gift formats, sustainable packaging |

Premiumization and compliance-led consolidation |

|

China |

Cultural scent integration and livestream commerce |

Traditional fragrance profiles, hospitality scenting |

Digitally driven discovery and cultural alignment |

|

India |

Festive gifting and wellness initiatives |

Natural wax exports, aromatherapy use |

Export expansion and urban wellness adoption |

|

Parameter |

Details |

|

Market Size (2025) |

$1.8 Billion |

|

Market Size (2034) |

$3 Billion |

|

Market Growth Rate |

5.9% |

|

Segments |

By Wax Type (Natural Wax, Synthetic Wax, Blended Wax), By Fragrance Category (Fresh and Citrus, Floral, Warm and Spicy, Gourmand, Functional and Wellness), By Application (Residential, Commercial), By Melting Method (Electric Wax Warmers, Flame-Based Warmers) |

|

Study Period |

2019- 2025 and 2026-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

Newell Brands, S. C. Johnson & Son, Inc., Procter & Gamble, Reckitt Benckiser Group plc, Scentsy, Inc., Rimports Limited, Bath & Body Works, Inc., Millennium Fragrances, Happy Wax, Candle Shack Ltd., ScentAir, Village Candle, NEST New York, Diptyque, The Fragrance Shop |

|

Countries |

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa |

*- List not Exhaustive

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Fragrance Wax Melts Market Landscape & Outlook (2026–2034)

2.1. Introduction to Fragrance Wax Melts Market

2.2. Market Valuation and Growth Projections (2026–2034)

2.3. Premiumization in Home Fragrance and Hotel-Inspired Scent Profiles

2.4. Growth of Subscription-Based Commerce and Collectible Wax Melt Series

2.5. Shift Toward Flame-Free Fragrance Delivery and Sustainable Wax Systems

3. Innovations Reshaping the Fragrance Wax Melts Market

3.1. Trend: Premiumization Through Ingredient Transparency and Bio-Based Wax Systems

3.2. Trend: Neuro-Scenting and Experiential Fragrance Profiles in Home Fragrance Products

3.3. Opportunity: Safety-Centric Innovation Through Low-Melt and Air-Quality-Conscious Formulations

3.4. Opportunity: Smart Home Integration and Subscription-Led Commerce Models

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Fragrance Wax Melts Market

5.1. By Wax Type

5.1.1. Natural Wax

5.1.2. Synthetic Wax

5.1.3. Blended Wax

5.2. By Fragrance Category

5.2.1. Fresh and Citrus

5.2.2. Floral

5.2.3. Warm and Spicy

5.2.4. Gourmand

5.2.5. Functional and Wellness

5.3. By Application

5.3.1. Residential

5.3.2. Commercial

5.4. By Melting Method

5.4.1. Electric Wax Warmers

5.4.2. Flame-Based Warmers

5.5. By Region

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. South and Central America

5.5.5. Middle East and Africa

6. Country Analysis and Outlook of Fragrance Wax Melts Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Fragrance Wax Melts Market Size Outlook by Region (2026–2034)

7.1. North America Fragrance Wax Melts Market Size Outlook to 2034

7.1.1. By Wax Type

7.1.2. By Fragrance Category

7.1.3. By Application

7.1.4. By Melting Method

7.1.5. By Region

7.2. Europe Fragrance Wax Melts Market Size Outlook to 2034

7.2.1. By Wax Type

7.2.2. By Fragrance Category

7.2.3. By Application

7.2.4. By Melting Method

7.2.5. By Region

7.3. Asia Pacific Fragrance Wax Melts Market Size Outlook to 2034

7.3.1. By Wax Type

7.3.2. By Fragrance Category

7.3.3. By Application

7.3.4. By Melting Method

7.3.5. By Region

7.4. South America Fragrance Wax Melts Market Size Outlook to 2034

7.4.1. By Wax Type

7.4.2. By Fragrance Category

7.4.3. By Application

7.4.4. By Melting Method

7.4.5. By Region

7.5. Middle East and Africa Fragrance Wax Melts Market Size Outlook to 2034

7.5.1. By Wax Type

7.5.2. By Fragrance Category

7.5.3. By Application

7.5.4. By Melting Method

7.5.5. By Region

8. Company Profiles: Leading Players in the Fragrance Wax Melts Market

8.1. Newell Brands

8.2. S. C. Johnson & Son, Inc.

8.3. Procter & Gamble

8.4. Reckitt Benckiser Group plc

8.5. Scentsy, Inc.

8.6. Rimports Limited

8.7. Bath & Body Works, Inc.

8.8. Millennium Fragrances

8.9. Happy Wax

8.10. Candle Shack Ltd.

8.11. ScentAir

8.12. Village Candle

8.13. NEST New York

8.14. Diptyque

8.15. The Fragrance Shop

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

The Fragrance Wax Melts Market is expected to grow from $1.8 billion in 2025 to $3 billion by 2034, registering a CAGR of 5.9%. Growth is supported by premium home fragrance trends, increased adoption of flame-free fragrance delivery systems, and expanding subscription-based scent discovery models. Consumer demand for curated fragrance experiences and sophisticated scent profiles is further strengthening long-term market expansion.

Natural wax accounted for 48.6% of the market share in 2025, driven by rising consumer preference for plant-based and eco-friendly home fragrance products. Materials such as soy, coconut, beeswax, and rapeseed wax are widely adopted due to their cleaner melting performance and lower environmental footprint compared with paraffin-based alternatives. Transparency around sourcing and certified agricultural supply chains is also enabling brands to position natural wax melts in premium product segments.

Subscription-based fragrance programs are transforming how consumers discover and purchase wax melts. Monthly curated scent boxes and limited-edition fragrance collections allow brands to introduce new scent profiles while building recurring revenue streams. These models also increase customer lifetime value and product experimentation, with many consumers purchasing full-size products after experiencing curated sample assortments.

Key trends include premium fragrance storytelling, wellness-oriented aromatherapy scents, and smart home integration. Mood-enhancing fragrances such as lavender for sleep or citrus for focus are gaining traction alongside nostalgic and gender-neutral scent profiles. In addition, connected wax warmers and app-controlled fragrance devices are enabling personalized scent scheduling within smart home ecosystems.

Leading companies in the Fragrance Wax Melts Market include Procter & Gamble (Febreze), SC Johnson (Glade), Newell Brands (Yankee Candle), Reckitt Benckiser (Air Wick), Scentsy, Bath & Body Works, Village Candle, NEST New York, Rimports, and ScentAir. These companies are investing in premium fragrance collections, plant-based wax formulations, digital scent personalization, and direct-to-consumer subscription models to strengthen their market positions.