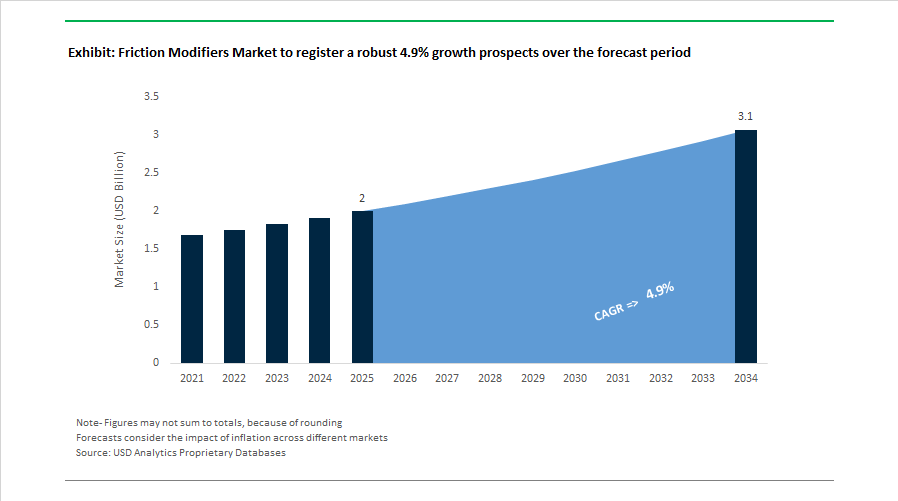

Friction Modifiers Market Size 2025–2034: $2 Billion to $3.1 Billion at 4.9% CAGR Driven by Ultra-Low Viscosity Oils and Hydrogen Engine Innovation

The Friction Modifiers Market is projected to grow from $2 billion in 2025 to $3.1 billion by 2034, registering a CAGR of 4.9%. Growth is primarily fueled by the transition toward ultra-low viscosity engine oils, hydrogen combustion engines, stricter emission norms, and advanced fuel economy standards across passenger and heavy-duty vehicles. Organic friction modifiers, molybdenum-based compounds, polyether hybrids, and next-generation dispersant-compatible systems are increasingly critical to achieving low-speed pre-ignition mitigation, timing chain durability, and fuel efficiency targets. Regulatory frameworks such as ILSAC GF-7 and ACEA C7 are reshaping additive chemistry requirements, compelling lubricant formulators to adopt advanced friction-reducing technologies compatible with low-SAPs formulations.

In early 2026, Infineum launched Infineum P6188, a Volkswagen-approved additive technology engineered for SAE 0W-20 formulations, requiring enhanced friction control under ultra-low viscosity conditions. During the same period, Infineum signed a strategic framework agreement with Rianlon Corporation to stabilize the Asia-Pacific supply chain for antioxidant and friction-modifying intermediates. In February 2026, Lubrizol expanded its regional innovation footprint with a new center in Shanghai, following the July 2025 opening of its Singapore Innovation Center, both focused on local-for-local development of friction modifiers tailored to regional driving conditions and climate variables.

Throughout 2025, technological advancements accelerated across the lubricant additive sector. In September 2025, Afton Chemical introduced HiTEC® 12582, the first dedicated additive for hydrogen heavy-duty engines, addressing distinct wear and friction challenges associated with hydrogen combustion. In September 2025, Chevron Oronite debuted OLOA® 55620 at the Asian Lubricant Exhibition, targeting passenger car, motorcycle, and scooter segments with advanced friction-modifying chemistry. In August 2025, Afton Chemical launched the HiTEC® 65522 series aligned with the TOP TIER+™ gasoline standard, enhancing deposit control and injector-tip friction reduction in GDI engines. Throughout 2025, BASF expanded commercialization of SYNATIVE® EEB 45, a polyether-based hybrid friction modifier designed to improve energy efficiency in automotive and industrial gear oils. In February 2025, Lubrizol introduced Solsperse™ W60 hyperdispersant technology to enhance compatibility of friction-reducing molecules in next-generation low-SAPs engine oils.

Regulatory and regional manufacturing developments shaped 2024 and early 2025. In March 2025, the ILSAC GF-7 engine oil specification was officially implemented, mandating improved LSPI mitigation and stricter phosphorus and sulfur thresholds, intensifying demand for advanced friction modifiers. Following the ACEA 2023 C7 update, 2024 and 2025 saw a surge in SAE 0W-16 compliant formulations requiring precise friction balance to achieve a 0.3% fuel economy gain over reference oils. In November 2024, Infineum announced expansion of its India blending facility, with trial production scheduled for mid-2025 and full operations by Q3 2025, strengthening supply of additive packages for the rapidly growing Indian automotive lubricant market.

Trends and Opportunities Shaping the Global Friction Modifiers Market

Formulation for Ultra-Low-Viscosity Oils and Electrified Drivetrains

The acceleration toward ultra-low-viscosity engine oils such as SAE 0W-8 is fundamentally redefining friction modifier chemistry. As OEMs prioritize fuel economy and thermal efficiency, lubricant film thickness is approaching boundary lubrication regimes where surface-active friction modifiers become the primary line of wear protection. In December 2025, LIQUI MOLY launched Special Tec AA 0W-8 to meet JASO GLV-1 requirements for next-generation hybrid powertrains. Such formulations rely heavily on advanced ashless organic friction modifiers to ensure immediate surface adsorption during cold starts and high-rev operating cycles.

Peer-reviewed research published across 2024 and 2025 confirms that migrating from 0W-20 to 0W-8 oils delivers fuel economy improvements in the range of 2 to 3%. However, the same studies highlight a potential 20% increase in boundary wear risk if friction modifiers are inadequately optimized. This has intensified demand for organic friction modifiers and trinuclear molybdenum systems that can form durable tribofilms under low-speed, high-load conditions.

Electrification adds another layer of complexity. Integrated e-axles and electric drivetrains require friction modifiers that are not only wear-protective but also electrically compatible. Industry technical assessments in 2024 identified a decisive shift toward sulfur-free Mo-amide systems and hydrolytically stable borated ester-amides. These chemistries maintain low electrical conductivity, preventing copper corrosion and short-circuit risks in high-voltage EV drivetrains where lubricants are in direct proximity to electrical components.

Strategic Shift Toward Bio-Based and Renewable Carbon Friction Modifiers

Sustainability mandates are accelerating the transition away from petroleum-derived friction modifiers toward renewable, bio-based alternatives. The EU Carbon Border Adjustment Mechanism and OEM Scope 3 emissions reporting are pushing lubricant formulators to redesign additive packages using oleochemical feedstocks without sacrificing performance.

In January 2025, the Society of Tribologists and Lubrication Engineers reported a sharp increase in adoption of fatty acid ester-based friction modifiers derived from high-oleic sunflower and canola oils. These next-generation bio-based modifiers are engineered to overcome historical oxidation and thermal stability limitations, achieving performance parity with synthetic esters in high-temperature engine environments.

Metals-free innovation is also gaining traction. In 2025, LANXESS commercialized its Additin RC 3502 organic friction modifier, demonstrating that a treat rate of approximately 0.5% by weight enables motor oils to exceed ILSAC GF-6 fuel economy thresholds. Its ashless, sulfur-free, and phosphorus-free profile aligns with tightening global emissions standards while maintaining high solubility in bio-based and Group III base oils. This trend reflects a broader market pivot toward friction modifiers that simultaneously support emissions compliance, renewable carbon sourcing, and long drain interval performance.

Energy Efficiency Optimization in Industrial Gearboxes and Compressors

Rising electricity prices and Scope 2 emissions disclosure requirements are reframing lubricants as direct energy efficiency tools in industrial operations. Advanced friction modifiers are increasingly deployed to reduce mechanical losses in gearboxes, compressors, and heavy-duty transmissions.

Strategic efficiency audits conducted in late 2024 demonstrated that optimized friction-modified gear oils can improve mechanical efficiency by more than 3.7% in spur and cycloidal gear systems. For energy-intensive manufacturing plants, this reduction in churning and sliding losses translates into substantial annual electricity cost savings per gearbox, creating a compelling near-term return on investment for plant operators.

Digitalization is further amplifying this opportunity. In early 2025, industrial OEMs began deploying IoT-enabled gear cases that monitor lubricant condition in real time. Friction modifier concentration is increasingly used as a proxy indicator for surface protection and gear health. This enables active additive replenishment strategies, opening a high-margin opportunity for chemical suppliers to provide on-demand friction modifier concentrates that maintain peak efficiency without requiring full oil drains.

Friction Control Solutions for the Emerging Hydrogen Economy

The transition toward hydrogen-powered systems represents a structurally new opportunity for friction modifier suppliers. In hydrogen combustion engines, particulate emissions originate almost exclusively from lubricant oil, as hydrogen itself produces no carbon soot. A 2025 CDC and NIOSH technical study highlighted the need for ultra-low-ash friction modifiers that do not generate metal-rich nanoparticles, ensuring compliance with zero-emission vehicle classifications for hydrogen heavy-duty transport.

Fuel cell systems present additional niche requirements. High-speed air compressors used in hydrogen fuel cells must operate in moist, oxygen-rich environments without contaminating catalyst membranes. This creates demand for non-volatile, non-silicone friction modifiers in specialty greases that deliver long-term wear protection while maintaining chemical inertness.

Materials compatibility is emerging as a critical differentiator. Recent patented developments focus on pairing friction modifiers with magnesium-based detergents and nitrogen-containing dispersants to mitigate hydrogen embrittlement in steel components. This challenge is particularly acute in hydrogen infrastructure, where traditional lubricant packages were not designed for prolonged hydrogen exposure. Suppliers that can address embrittlement risk while maintaining friction reduction performance are positioned to secure early mover advantage in this blue-ocean segment.

Friction Modifiers Market Share and Segmentation Insights

Organic Friction Modifiers Lead Lubricant Additive Technologies Through Boundary Film Performance

Organic Friction Modifiers accounted for 72.80% of the Friction Modifiers Market share in 2025, establishing them as the dominant additive category used in modern lubricant formulations. These compounds—including fatty acids, esters, amines, amides, and organometallic additives such as molybdenum-based compounds—work by forming protective boundary films on metal surfaces, significantly reducing friction and wear under boundary lubrication conditions. Organic friction modifiers are widely used in engine oils, transmission fluids, industrial lubricants, and specialty greases, where they help improve energy efficiency, component durability, and lubricant performance. Their strong market position stems from their chemical tunability and compatibility with different base oil systems, allowing lubricant formulators to tailor additive packages to specific application requirements. In 2025, the friction modifier market is witnessing growing specialization in organic molybdenum compounds, particularly molybdenum dithiocarbamate (MoDTC) and trinuclear molybdenum additives, which deliver superior friction reduction and fuel economy benefits. New generations of these additives are engineered with lower sulfur content and improved thermal stability, ensuring compatibility with low-viscosity engine oils formulated to meet modern API and ACEA fuel efficiency standards. These advancements reinforce the leadership of organic friction modifiers in the global lubricant additives market.

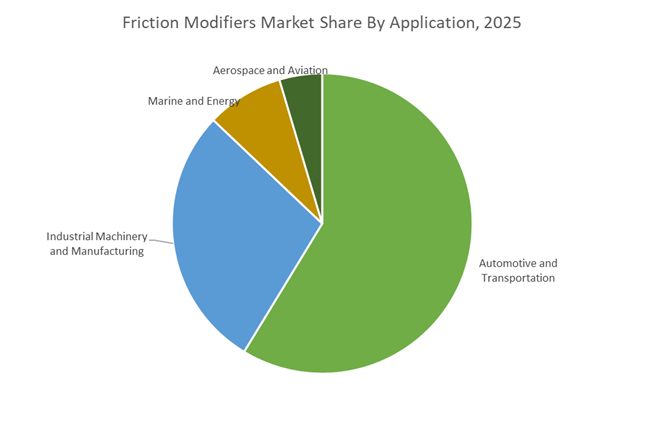

Automotive and Transportation Sector Drives the Largest Demand for Friction-Reducing Lubricant Additives

Automotive and Transportation represented 58.70% of the Friction Modifiers Market share in 2025, reflecting the sector’s dominant consumption of lubricants and lubricant additives worldwide. Passenger vehicles, commercial trucks, buses, and off-highway equipment require advanced lubricant formulations to reduce engine friction, improve fuel efficiency, protect mechanical components, and extend maintenance intervals. Friction modifiers are essential additives in engine oils, automatic transmission fluids, gear oils, and driveline lubricants, where they help maintain smooth operation under high-load and high-temperature conditions. In 2025, the automotive lubricant landscape is evolving due to the rapid adoption of electric vehicles (EVs), which is reshaping lubricant requirements. While EVs eliminate the need for traditional internal combustion engine oils, they introduce new lubrication challenges in electric drive units, reduction gears, e-axles, and thermal management systems. EV driveline fluids must provide gear protection, wet clutch compatibility, and electrical insulation properties, requiring specialized friction modifier technologies designed for electrified powertrains. As a result, lubricant manufacturers are developing next-generation friction modifier chemistries optimized for EV transmission fluids and e-mobility lubrication systems, creating a rapidly expanding niche within the automotive friction modifiers market.

Competitive Landscape in Friction Modifiers Market

Lubrizol Strengthens Zinc-Free and API SQ-Compliant Friction Modifier Portfolio

The Lubrizol Corporation, a Berkshire Hathaway company, remains the dominant global force in specialty lubricant chemistry with a strong Local-for-Local innovation strategy. In October 2025, Lubrizol introduced Lubrizol® AH933ZF, a zinc-free hydraulic additive package engineered for environmentally sensitive sectors such as forestry and marine equipment. The company expanded its Southeast Asia Innovation Center in Jurong in July 2025 and launched a Foam Center of Excellence in South Korea to accelerate materials collaboration. In February 2026, Lubrizol strengthened its U.S. West Coast distribution through a strategic partnership with Commerce Hose & Industrial Products. Its PV1710 series is specifically engineered to meet the latest API SQ and ILSAC GF-7 specifications, positioning Lubrizol at the forefront of passenger vehicle fuel economy standards and next-generation engine oil performance requirements.

Afton Chemical Expands eMobility-Focused Friction Modifiers in Asia

Afton Chemical Corporation continues to lead in driveline and engine oil additives, with a strategic emphasis on electrified transmission fluids and hybrid drivetrain durability. In 2025, Afton completed a S$380 million Phase II expansion at its Jurong Island facility in Singapore, significantly increasing production capacity for ashless dispersants and anti-wear components while doubling local workforce strength. In January 2026, the company launched its eVolving eMobility initiative, introducing friction modifiers tailored for Electrified Transmission Fluids requiring stability under high-torque electric motor loads. Early 2026 R&D priorities included gear oil additives designed to prevent micropitting in industrial gear lubricants while aligning with stricter OEM efficiency targets. The Singapore facility now operates with automated full traceability systems, reinforcing quality assurance in global additive supply chains.

Infineum Advances Low-SAPS and Hybrid Vehicle Lubrication Technologies

Infineum International Ltd., a joint venture between Shell and ExxonMobil, specializes in high-performance fuel and lubricant additives aligned with sustainability and decarbonization goals. In 2026, Infineum positioned its portfolio to support the Internal Combustion Engine 2.0 era, optimizing friction modifiers for hybrid vehicles characterized by frequent stop-start cycles. In February 2026, the company emphasized lower-viscosity commercial vehicle oils under PC-12 specifications to balance hardware durability with measurable fuel economy improvements. Infineum has developed novel low-SAPS friction modifiers engineered to protect advanced aftertreatment systems in heavy-duty engines. Parallel efforts are underway to reduce product carbon footprint through bio-based organic friction modifiers that maintain boundary lubrication performance, reinforcing its role in sustainable lubricant chemistry.

BASF Leverages Verbund Integration for Hybrid and Renewable Friction Additives

BASF SE utilizes its integrated Verbund chemical platform to supply advanced organic and hybrid friction modifiers across automotive and industrial lubricant markets. Its IRGALUBE® FE1 and SYNATIVE® EEB Energy Efficiency Booster leverage polyether-based hybrid structures to improve oil compatibility while delivering measurable friction reduction. For fiscal year 2026, BASF projects EBITDA before special items between €6.2 billion and €7.0 billion, with Chemicals and Nutrition & Care segments as primary earnings drivers. In March 2026, BASF implemented acrylate price adjustments in Asia-Pacific to offset raw material volatility while advancing specialized Elastollan® TPU production in Shanghai. Through high-renewable-content additives such as IRGALUBE® F 10 A, which combines friction modification with antioxidant functionality, BASF emphasizes fuel efficiency gains and enhanced thermo-oxidative stability.

Chevron Oronite Targets Marine and Motorcycle Friction Performance Standards

Chevron Oronite Company LLC remains a critical supplier in marine lubricants, power generation oils, and small engine formulations. In January 2026, the company announced leadership changes and expanded African distribution through a partnership milestone with Azelis South Africa. Its OLOA® 22028T additive package dominates the motorcycle segment, meeting both JASO T903:2016 and updated 2023 specifications while incorporating friction modification without compromising wet clutch compatibility. Through participation in Lube Expo Europe and other 2025 to 2026 industry forums, Oronite has showcased differentiated solutions for water-cooled engines and small engine oils targeting reduced ring groove deposits and enhanced anti-scuff performance. Deep expertise in ashless additive chemistry for two-stroke and four-stroke marine outboards reinforces its position as a benchmark supplier in specialized friction modifier applications.

United States: Regulatory Convergence and Powertrain Diversification Driving Formulation Shifts

The United States friction modifiers market is undergoing accelerated reformulation as regulatory oversight and powertrain diversification converge. Under the Modernization of Cosmetics Regulation Act and heightened scrutiny from the U.S. Environmental Protection Agency, manufacturers supplying consumer-facing lubricants are now required to submit comprehensive safety dossiers for ashless and surface-active additives. This has materially reduced tolerance for PFAS-containing chemistries and increased adoption of biodegradable friction modifiers derived from esters, amides, and advanced polymers. Regulatory alignment is therefore reshaping the competitive landscape in favor of suppliers with strong toxicological data, traceable raw materials, and compliant lifecycle profiles.

Technology-led demand is expanding beyond conventional internal combustion engines. In September 2025, Afton Chemical introduced the first dedicated additive package for hydrogen-combustion heavy-duty engines, incorporating friction modifier systems engineered to manage atypical moisture ingress and elevated thermal cycling. At the same time, Lubrizol launched its PV1710 series to meet API SQ and ILSAC GF-7 requirements, emphasizing fuel economy retention and LSPI protection in turbocharged GDI engines. Electric mobility is also influencing formulation priorities. With increased 2025 funding from the U.S. Department of Energy, suppliers such as BASF are developing polyether-based friction modifiers optimized for ultra-low viscosity EV driveline fluids, addressing boundary lubrication challenges in high-speed electric motors.

Singapore: Asia-Centric Manufacturing and Sustainability Certification Hub

Singapore has strengthened its role as a regional friction modifiers manufacturing and innovation hub, anchored by Jurong Island’s integrated chemical infrastructure. Afton Chemical reached full-scale production at its expanded Jurong Island facility in 2025, positioning the site as a core supplier of friction-reducing components under a Made in Asia for Asia strategy. This localization reduces supply chain risk for regional engine oil blenders while enabling faster customization for ASEAN vehicle platforms.

Innovation and sustainability credentials are reinforcing this position. In December 2025, Singapore inaugurated a new Southeast Asia Innovation Center focused on specialty coatings and additive blending, supporting automotive and industrial customers across the ASEAN manufacturing corridor. In parallel, Singapore’s Green Plan 2030 has accelerated adoption of ISCC PLUS certified production pathways. Infineum achieved ISCC PLUS certification at regional sites in late 2025, enabling mass-balance sourcing of renewable feedstocks for friction modifiers supplied into Asia-Pacific lubricant markets.

China: Materials Engineering and Bio-Based Substitution at Scale

China’s friction modifiers market is evolving through a combination of advanced materials engineering and state-backed sustainability mandates. In November 2025, Lubrizol opened a Film and Coating Center of Excellence in Shanghai, dedicated to molecular design of friction-modifying polymers for paint protection films and high-performance industrial coatings. This reflects expanding demand beyond lubricants into surface protection, electronics, and advanced manufacturing applications.

Policy direction is reinforcing bio-based substitution. The Ministry of Industry and Information Technology’s 2025–2026 Work Plan targets sustained growth in eco-friendly chemical value addition, explicitly promoting bio-based esters as alternatives to molybdenum-based friction modifiers. Industrial circularity is also gaining traction. In early 2025, BASF commissioned its first commercial Loopamid facility in Shanghai, enabling recycled polyamide 6 monomers to be used as building blocks for sustainable friction-modifying additives in textiles and industrial formulations.

Germany: EU Compliance and Stationary Power Generation Focus

Germany remains a regulatory and technology bellwether for the friction modifiers market in Europe. With the EU Chemical Strategy for Sustainability and F-Gas related measures taking effect from January 2026, German producers have pivoted toward ashless friction modifiers with higher renewable content to avoid exposure to quota-linked cost escalation. Product portfolios now emphasize chemistries such as IRGALUBE FE1 that align with European Green Deal objectives while maintaining performance in demanding lubricant environments.

Industry knowledge exchange continues to shape innovation pathways. At the April 2025 UNITI Mineral Oil Technology Congress in Stuttgart, Chevron Oronite outlined its 2026 roadmap for gas engine oils, highlighting metallic-organic friction modifiers capable of preserving oxidative stability under continuous high-heat operation in stationary power generation. Sustainability governance is also extending across borders. German-based management oversight supported ISCC PLUS certification at the Vado Ligure site in late 2025, securing lower-carbon friction modifier supply for the wider EMEA lubricants value chain.

Brazil: Integrated Distribution and Expansion into Personal Care Applications

Brazil’s friction modifiers market is being reshaped by supply chain consolidation and diversification into non-automotive applications. In April 2025, Chevron Oronite appointed ICONIC Base Oil Solutions as its official distributor, operational by June 2025. This partnership integrates PARATONE viscosity modifiers with OLOA friction-reducing additives, creating a unified supply platform for automotive and industrial lubricants across the Mercosur region.

Beyond lubricants, Brazil is emerging as an innovation base for sensory friction modifiers in beauty and personal care. The announcement of the Beauty Research Institute Brazil in December 2025 signals growing investment in rheology modifiers and tactile enhancers derived from local biodiversity. These materials are being tailored for diverse Latin American skin and hair types, expanding the functional scope of friction-modifying chemistries into cosmetics and personal care formulations.

South Korea: Advanced Materials and Export-Oriented Compliance

South Korea is positioning itself as a technology-driven supplier of friction-modifying polymers for advanced applications. In November 2025, Lubrizol established a Foam Center of Excellence in Seoul, focusing on friction-modifying materials for specialized foams used in automotive seating, consumer electronics, and ergonomic applications. This underscores the role of friction control beyond lubricants, particularly in comfort and durability-critical components.

Regulatory compliance is reinforcing export competitiveness. Throughout 2025, South Korean chemical manufacturers accelerated reformulation to meet K-REACH requirements, systematically removing restricted alkylphenols from friction modifier portfolios slated for 2026 export. This proactive alignment is strengthening South Korea’s position in supplying compliant additives to Europe and North America, where regulatory thresholds continue to tighten.

Summary of Country-Level Strategic Drivers in the Friction Modifiers Market

Friction Modifiers Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Implications for Friction Modifiers

|

|

United States

|

Regulatory convergence and new powertrains

|

Shift to PFAS-free, EV and hydrogen-optimized additives

|

|

Singapore

|

Regional manufacturing and sustainability

|

Asia-focused supply with ISCC PLUS certification

|

|

China

|

Bio-based mandates and circular materials

|

Growth of ester-based and recycled polymer modifiers

|

|

Germany

|

EU sustainability regulation

|

Expansion of ashless, renewable-content modifiers

|

|

Brazil

|

Supply chain integration and personal care

|

Broader application base beyond lubricants

|

|

South Korea

|

Advanced materials and K-REACH compliance

|

Export-ready, high-performance friction-modifying polymers

|

Friction Modifiers Market Report Scope

Friction Modifiers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2 Billion

|

|

Market Size (2034)

|

$3.1 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Product Type (Organic Friction Modifiers, Inorganic Friction Modifiers), By Lubricant Type (Engine Oils, Transmission Fluids, Gear Oils and Axle Fluids, Hydraulic and Metalworking Fluids, Industrial Lubricants and Greases), By Application (Automotive and Transportation, Industrial Machinery and Manufacturing, Aerospace and Aviation, Marine and Energy), By Form (Liquid, Powder)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Lubrizol Corporation, Infineum International Ltd., Afton Chemical Corporation, Chevron Oronite Company LLC, BASF SE, Croda International Plc, Evonik Industries AG, Vanderbilt Chemicals, LLC, LANXESS AG, ADEKA Corporation, Dover Chemical Corporation, Kings Industries, Inc., BRB International BV, Sanyo Chemical Industries, Ltd., Clariant AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Friction Modifiers Market Segmentation

By Product Type

- Organic Friction Modifiers

- Inorganic Friction Modifiers

By Lubricant Type

- Engine Oils

- Transmission Fluids

- Gear Oils and Axle Fluids

- Hydraulic and Metalworking Fluids

- Industrial Lubricants and Greases

By Application

- Automotive and Transportation

- Industrial Machinery and Manufacturing

- Aerospace and Aviation

- Marine and Energy

By Form

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Friction Modifiers Industry

- The Lubrizol Corporation

- Infineum International Ltd.

- Afton Chemical Corporation

- Chevron Oronite Company LLC

- BASF SE

- Croda International Plc

- Evonik Industries AG

- Vanderbilt Chemicals, LLC

- LANXESS AG

- ADEKA Corporation

- Dover Chemical Corporation

- Kings Industries, Inc.

- BRB International BV

- Sanyo Chemical Industries, Ltd.

- Clariant AG

*- List not Exhaustive