Gelcoat Market to Reach $18.6 Billion by 2034 at 13.6% CAGR Driven by Composites Expansion in Marine, Rail, and Wind Energy

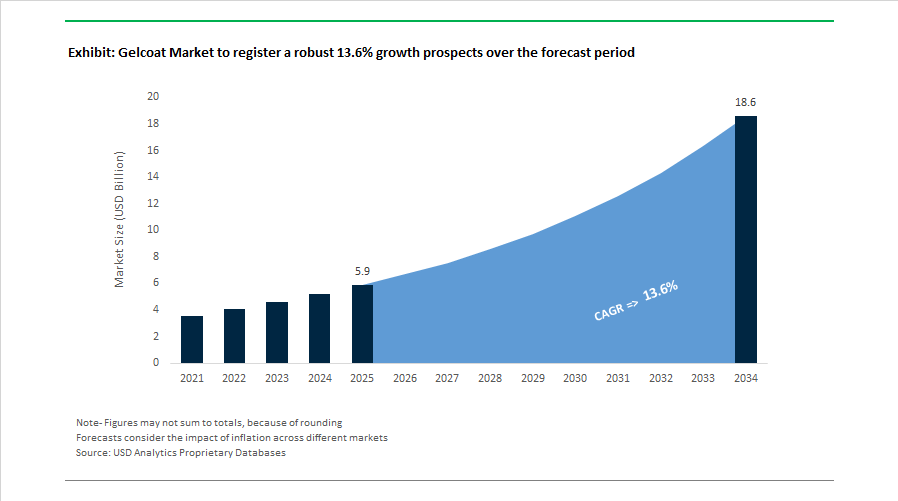

The Gelcoat Market is projected to expand from $5.9 billion in 2025 to $18.6 billion by 2034, registering a strong CAGR of 13.6% during the forecast period. Growth is anchored in accelerating demand for high-performance surface coatings used in fiber-reinforced composites across marine vessels, wind turbine blades, rail interiors, construction panels, automotive SMC components, and industrial equipment. Increasing infrastructure modernization, renewable energy capacity additions, and lightweight mobility solutions are driving consumption of advanced polyester and vinyl ester gelcoats engineered for UV resistance, corrosion protection, fire retardancy, and improved surface aesthetics.

In January 2024, Scott Bader Company Ltd. commissioned a £12.5 million manufacturing facility in Mocksville, North Carolina, dedicated to structural adhesives and Crystic gelcoats for marine, renewable energy, and e-mobility applications. In February 2024, AOC LLC brought a new production line online in Nanjing, significantly expanding regional capacity for gelcoats and composite resins serving Asia’s wind energy and infrastructure sectors. In December 2024, KPS Capital Partners entered a definitive agreement to acquire INEOS Composites for approximately €1.7 billion, consolidating a major global portfolio of unsaturated polyester resins, vinyl ester resins, and specialty gelcoats used in marine and industrial markets. These investments reflect capacity localization and portfolio integration across high-growth composite applications.

Sustainability and low-carbon material innovation intensified in 2024–2025. At InnoTrans 2024, Scott Bader launched 100% bio-based fire-retardant resins and gelcoats targeting rail and public transport sectors, aligning with stricter international fire safety and carbon reduction standards. In May 2025, BÜFA Composite Systems introduced the BÜFA®-rPET resin series incorporating recycled PET, engineered to integrate seamlessly with high-performance gelcoat systems for lower-carbon structural composites. In July 2025, LyondellBasell Industries and Polynt Group expanded collaboration to develop marine resins and gelcoats utilizing low-carbon styrene solutions, targeting reduced lifecycle emissions in luxury yachts and commercial vessels. These initiatives demonstrate the transition toward circular feedstocks and carbon-accountable composite manufacturing.

Regional consolidation and distribution optimization strengthened competitive positioning. Effective September 2024, Polynt merged Reichhold do Brasil into Polynt Composites Brazil LTDA, unifying South American operations and streamlining specialty gelcoat production for marine and industrial customers. In June 2024, Scott Bader established Scott Bader Brasil following the buyout of its joint venture partner, focusing on Crystic gelcoats and tooling systems for wind energy and building sectors. In January 2025, IP Corporation integrated Interplastic Corporation and HK Research Corporation, merging sales operations to create the largest vertically integrated gelcoat entity in the United States. In 2025, Scott Bader strengthened its European presence through a distribution partnership with Sandtech in France, enhancing localized supply chain support for marine and rail industries.

Product innovation for performance durability also advanced. In November 2024, AOC introduced a UV-resistant automotive system for Sheet Molding Compound parts featuring specialized gelcoat-like finishes designed to protect truck and off-road vehicle components from solar degradation. In September 2024, BÜFA Composite Systems received the Railway Award 2024 for its specialty gelcoats delivering enhanced surface quality and safety compliance in train interiors and exteriors.

The Gelcoat Market outlook reflects rapid composites adoption in wind energy blades, sustainable marine manufacturing, rail safety upgrades, automotive exterior protection, and circular resin technologies. Competitive advantage is increasingly defined by bio-based formulations, recycled feedstock integration, vertical resin-gelcoat integration, regional production expansion, and low-carbon styrene innovation aligned with global decarbonization objectives.

Gelcoat Market Trends and Strategic Growth Opportunities

Regulatory-Driven Transition Toward Low-VOC and Low-Styrene Gelcoat Technologies

The global gelcoat market is undergoing a compliance-led transformation as environmental regulations tighten across marine, transportation, and construction composites. Regulatory updates aligned with the EU Industrial Emissions Directive and the implementation of the FuelEU Maritime Regulation from January 2025 are accelerating the phase-out of conventional high-styrene polyester gelcoats. Industry data indicate that traditional solvent-based polyester and vinyl ester gelcoats generate close to 2.8 tons of volatile organic compound emissions per 100 tons of resin processed, making them increasingly untenable under evolving air quality standards.

In response, manufacturers are rapidly shifting toward low-styrene and low-VOC gelcoat formulations that preserve surface durability, gloss retention, and osmotic blister resistance while reducing hazardous air pollutants by approximately 35 to 40%. Styrene-free product innovation is gaining particular momentum in Europe, where rail, marine, and public infrastructure projects face strict emissions and fire safety benchmarks. In 2024 and 2025, Scott Bader expanded its Crestafire portfolio with styrene-free, low-smoke gelcoats engineered to comply with EN 45545 fire performance requirements for rail interiors and exterior composite panels.

In the United States, tightening National Emission Standards for Hazardous Air Pollutants under the Environmental Protection Agency are driving gelcoat producers to prioritize styrene-suppressed chemistries. By August 2025, more than one-third of gelcoat manufacturers cited regulatory compliance as the dominant driver of R&D spending, accelerating adoption of neopentyl glycol-enhanced polyester systems that balance emissions control with mechanical performance and weathering resistance.

Strategic Shift Toward In-Mold Gel Coating and Closed-Mold Processing

Application innovation is emerging as a decisive competitive lever in the gelcoat market, with manufacturers and fabricators moving away from labor-intensive spray-up methods toward in-mold gel coating and closed-mold technologies. Although spray application still accounts for surface finishing across more than 37 million square meters of recreational boat hulls annually, resin transfer molding and vacuum infusion are expanding at a faster rate due to superior finish consistency, lower rework rates, and improved environmental performance.

Closed-mold processing enables the use of specialized low-drag gelcoats that co-infuse with structural resins, reducing overspray losses by an estimated 15 to 20% while improving material utilization. In parallel, self-leveling gelcoat chemistries introduced during 2025 are enabling uniform thickness control in the 20 to 25 mil range, significantly reducing surface pinholes and post-mold finishing. These attributes are particularly valuable in high-throughput automotive body panels, sanitary ware, and modular composite structures, where cycle time reduction directly impacts unit economics and scalability.

High-Durability Gelcoats for Offshore Wind and Marine Infrastructure

The rapid expansion of offshore wind capacity is opening a high-value application niche for advanced gelcoats engineered for extreme environmental exposure. Global offshore wind installations are projected to reach approximately 139 gigawatts in 2025, with turbine blade lengths and rotational speeds increasing sharply. Modern blades now operate at tip speeds approaching 110 meters per second, exposing leading edges to severe rain erosion, saltwater immersion, and particulate impact.

Next-generation gelcoats reinforced with nanofillers such as carbon nanotubes and graphene are emerging as critical leading-edge protection layers. Research published in 2025 demonstrated that these nano-enhanced systems can improve erosion resistance by up to 60 to 99%, significantly extending maintenance intervals and lowering lifetime operating costs for offshore assets. In August 2025, epoxy-based nanocomposite gelcoats incorporating graphene nanoplatelets showed nearly 39% lower material loss under high-pressure rain erosion testing, outperforming conventional polyurethane coatings while offering an isocyanate-free safety profile. These advances position gelcoats as performance-critical materials rather than cosmetic finishes in marine renewable infrastructure.

Fire-Retardant and Low-Smoke Gelcoats for Mass Transit and Urban Infrastructure

The growing use of composites in passenger rail, electric buses, and architectural facades is creating strong demand for fire, smoke, and toxicity compliant gelcoat systems. Updated safety frameworks such as the 2026 edition of NFPA 130 and EN 45545-2 HL3 are setting stringent benchmarks, requiring gelcoats to achieve flame spread indices below 25 and smoke development indices under 100 while maintaining high-gloss aesthetics and long-term durability.

This regulatory environment is creating a clear opportunity for halogen-free fire-retardant gelcoats based on phosphorus chemistry or alumina trihydrate fillers. Transit OEMs and infrastructure developers are increasingly prioritizing non-toxic fire retardant systems to minimize corrosive gas release during fire events, a shift that is expected to redefine material specifications for rolling stock, stations, and composite building envelopes through 2030. For gelcoat manufacturers, these requirements represent a structurally attractive growth avenue characterized by high qualification barriers, long project lifecycles, and premium pricing tied to safety-critical performance.

Gelcoat Market Share and Segmentation Insights

Polyester Gelcoat Leads Composite Surface Protection Due to Cost Efficiency and Broad Resin Compatibility

Polyester Gelcoat accounted for 68.40% of the Gelcoat Market share in 2025, making it the dominant resin type used in fiberglass composite surface finishing. Polyester gelcoats are widely applied in fiber reinforced plastic (FRP) components because they provide an effective balance of cost efficiency, UV resistance, mechanical durability, and compatibility with polyester and vinyl ester composite resin systems. These characteristics make polyester gelcoats the preferred surface coating for large-scale composite manufacturing across marine structures, transportation components, construction panels, and industrial equipment housings. The material also provides critical surface smoothness, corrosion protection, and long-term weather resistance, helping maintain both structural integrity and visual quality of composite products. In 2025, polyester gelcoat formulations are evolving in response to increasingly strict volatile organic compound (VOC) regulations governing styrene emissions. Manufacturers are introducing low-styrene emission gelcoats and styrene-suppressed resin technologies, allowing composite fabricators to reduce VOC emissions during spray and mold applications while maintaining the high-gloss surface quality required in marine and automotive finishes.

Marine Industry Drives the Largest Demand for Gelcoat in Fiberglass Boat Manufacturing

Marine applications represented 42.80% of the Gelcoat Market share in 2025, making it the largest end-use sector for gelcoat materials used in composite manufacturing. Gelcoat plays a crucial role in the construction of fiberglass boats, yachts, personal watercraft, and marine components, where it serves as the outer protective layer applied to molds before composite layup. This coating provides essential UV protection, water resistance, corrosion protection, and high-gloss aesthetic finishes, enabling vessels to withstand prolonged exposure to harsh marine environments. In addition to new vessel production, the marine sector also drives significant gelcoat consumption through aftermarket repair, refinishing, and maintenance activities required for aging fiberglass boats. In 2025, the marine industry is experiencing a shift influenced by the emergence of electric watercraft technologies and the expansion of luxury yacht markets. New vessel categories such as electric runabouts, e-foils, and hybrid propulsion yachts demand high-performance gelcoat formulations with enhanced UV stability, color retention, and long-term durability, supporting premium composite surface finishes in high-value marine vessels.

Competitive Landscape in Gelcoat Market

Ashland Inc. Strengthens High-Performance Marine and Sanitaryware Gelcoats

Ashland Inc. is positioning itself as a premium specialty gelcoat manufacturer. In Q1 2026, the company reported sales of $386 million, reflecting resilience despite broader portfolio optimization initiatives. Its Maxguard™ and Enguard™ gelcoat series remain industry benchmarks for marine hulls and sanitaryware composites due to superior UV resistance, gloss retention, and hydrolytic stability. The company continues to exit lower-margin construction segments to concentrate on advanced coatings and specialty additives. In February 2026, EPA approval of its agrimer™ eco-coat platform reinforced Ashland’s commitment to bio-based polymer technologies that align with sustainable gelcoat development and regulatory compliance.

Polynt-Reichhold Group Leads Through Vertical Integration and Resin Scale

Polynt-Reichhold Group operates 36 manufacturing plants globally and reported €2.16 billion in turnover in 2024, reinforcing its leadership in unsaturated polyester resins, the foundational chemistry for gelcoats. The company leverages internal production of maleic and phthalic anhydrides to ensure raw material security and cost-competitive Dion® and Polygel® gelcoat systems. In late 2025, integration of Reichhold do Brasil strengthened its footprint in the South American composites market. A July 2025 collaboration with LyondellBasell targets next-generation marine resins and gelcoats with improved Life Cycle Assessment performance. Vertical integration enables consistent quality, supply stability, and enhanced margin control across marine, construction, and transportation composites.

INEOS Composites Advances Operational Excellence Under New Ownership

Acquired by KPS Capital Partners for €1.7 billion in March 2025, INEOS Composites generates over €800 million in annual sales across 17 global sites. Its Neogel® and Optus® gelcoat lines are widely specified in marine vessels, wind turbine blades, automotive panels, and fire-retardant composite structures. Under new ownership in 2026, the company initiated an Operational Excellence program focused on production modernization, cost discipline, and commercial expansion in emerging markets. Strategic engagement in sustainable carbon fiber partnerships, including high-performance motorsport initiatives, underscores its integration of advanced gelcoat technologies into lightweight composite systems. Emphasis on durability, fire performance, and chemical resistance strengthens its position in regulated transportation sectors.

Scott Bader Expands Bio-Based and Marine Gelcoat Manufacturing Capacity

Scott Bader Company Ltd., an employee-owned enterprise, is recognized for its Crystic gelcoat technology used extensively in marine, rail, and renewable energy composites. In early 2026, the company ramped up its £12.5 million North Carolina facility to produce structural adhesives and gelcoats tailored for the North American marine and wind energy markets. A planned £30 million investment between 2025 and 2030 will modernize its UK manufacturing infrastructure, enhancing resin synthesis and gelcoat production capabilities. The company achieved EcoVadis Gold status for the second consecutive year in late 2025, reflecting leadership in bio-based and fire-retardant resin systems. Participation at JEC World 2026 highlights its focus on lightweighting, corrosion resistance, and long-term durability.

BÜFA Composite Systems Specializes in Fire-Retardant and Tooling Gelcoats

BÜFA Composite Systems is a European leader in system-based composite solutions, particularly fire-retardant gelcoats for rail and public transportation applications. In September 2025, the company introduced VE 6699 mould-making resin for emission-free infusion processes, completing its Tooling Conductive system that integrates nano-carbon technology. With eight distribution centers across Europe, BÜFA is expanding exports of sustainable and fire-compliant gelcoat systems to North America and Asia in 2026. A joint presentation with AOC at JEC Show 2026 emphasizes ready-to-use gelcoat formulations engineered for regulatory safety and production efficiency. The company’s strategic focus on safety, performance, and low-emission composite coatings positions it strongly in infrastructure and transportation composites markets.

United Kingdom: Additive Manufacturing Convergence and Low-Carbon Marine Composites

The United Kingdom gelcoat industry is moving decisively toward additive manufacturing convergence and sustainability-led marine innovation. In October 2025, Scott Bader confirmed a strategic investment in Crestaform 3D resins at Formnext, positioning gelcoats as an integral surface solution for 3D-printed composite parts. This development directly addresses a long-standing limitation in additive manufacturing by enabling colored, high-finish gelcoat layers to be integrated onto printed marine components. The approach is particularly relevant for short-run, high-value marine structures where traditional mold-based gelcoating is cost-inefficient. As a result, the UK market is emerging as a testing ground for hybrid manufacturing workflows that combine digital fabrication with premium gelcoat aesthetics.

In parallel, Scott Bader’s 2025 operational focus on energy-efficient processing and recyclability reflects tightening UK industrial sustainability mandates coming into force in 2026. The company’s marine composite R&D pipeline emphasizes high-elongation and high-tear-strength resin systems that maintain surface integrity under dynamic loading. These formulations are designed to enhance gelcoat adhesion and durability on functional prototypes, reinforcing the UK’s role as a center for advanced maritime engineering rather than volume gelcoat production.

Germany: Fire Safety Leadership and Circular Gelcoat Systems

Germany continues to define regulatory-led innovation in the gelcoat industry, with a strong emphasis on fire safety, circularity, and automotive collaboration. At JEC World 2025, BÜFA Composite Systems introduced Firestop-Gelcoat-S 320, a halogen-free system engineered to meet EN 45545-2 HL3 requirements for rail interiors. This launch positions gelcoats not merely as cosmetic layers but as functional components within certified fire-retardant composite systems, a critical differentiator for European rail and mass transit OEMs.

Beyond rail, BÜFA’s collaboration with Volkswagen on the ID. Buzz electric van illustrates how gelcoats are being adapted for lightweight, bio-based vehicle structures. The project integrates flax fibers and CO₂-reduced resins with specialized gelcoats to preserve surface quality while lowering lifecycle emissions. By late 2025, BÜFA also scaled its rPET-based resin systems containing up to 30% recycled PET, increasingly paired with durable gelcoats for sanitaryware and transport applications. This alignment with Europe’s 2026 circular economy targets is accelerating the substitution of virgin polyester systems in regulated markets.

China: Policy-Driven Scale and Export-Oriented Manufacturing Resilience

China’s gelcoat industry is being reshaped by industrial policy, automation, and export diversification. In September 2025, the Ministry of Industry and Information Technology released a two-year work plan for green building materials, targeting sector revenues exceeding 300 billion yuan by 2026. This directive directly incentivizes the use of high-performance gelcoats alongside advanced inorganic non-metallic materials in construction, particularly for façade panels, sanitary modules, and prefabricated housing components.

Despite external trade pressures, Chinese fiberglass and gelcoat producers have demonstrated export resilience through investments in automated weaving, precision dosing, and advanced composite matrices. By early 2026, manufacturers had diversified shipments toward the Middle East and Southeast Asia, offsetting tariff-related risks in Western markets. The growing adoption of automated weaving and optimized gel-coated woven roving is positioning China as a competitive supplier of lightweight construction panels where surface finish consistency and throughput efficiency are decisive purchasing criteria.

United States: Localized Supply Expansion and Regulatory-Driven Marine Demand

In the United States, gelcoat demand is being shaped by capacity localization and environmental regulation in maritime corridors. Polynt Group is completing a multi-year expansion of alkyd and polyester resin capacity across North America, scheduled to be fully operational by 2026. This expansion strengthens regional gelcoat supply chains for architectural façades and marine composites, reducing reliance on imported resins and improving lead-time reliability for U.S. boatbuilders.

Regulatory pressure is also influencing gelcoat specifications. California’s at-berth emission control rules, effective January 1, 2025, have increased demand for advanced marine surface technologies that reduce biofouling and hydrodynamic drag. In parallel, Axalta introduced its Alesta e-PRO dielectric coating line in October 2025. Although positioned for EV battery protection, these high-temperature, electrically insulating coatings highlight a convergence between traditional gelcoat protection and advanced functional coatings, particularly for next-generation transportation platforms.

European Union: Recycling Mandates and Energy-Efficient Marine Surfaces

At the regional level, the European Union is redefining gelcoat innovation priorities through recycling mandates and energy efficiency regulations. A self-imposed industry ban on landfilling wind turbine blades takes effect on January 1, 2026, triggering intensive R&D into recyclable epoxy-based gelcoats and thermoplastic systems that can be separated from fibers. This shift is moving gelcoats from thermoset end-of-life constraints toward design-for-recycling principles across the wind energy value chain.

These efforts are reinforced by the Horizon Europe Blades2Build program, a €15.4 million initiative entering its final phase in March 2026. The project includes dedicated workstreams for recovering fibers from gel-coated blade components, directly influencing future gelcoat chemistries. In maritime applications, the January 2025 implementation of FuelEU Maritime has increased uptake of low-friction gelcoats that contribute to vessel energy efficiency by reducing surface resistance, positioning gelcoats as an indirect but measurable lever in ship decarbonization strategies.

Comparative Overview of Gelcoat Industry Dynamics by Region

Gelcoat Market County Level Snapshot

|

Region

|

Strategic Focus

|

Market Implication

|

|

United Kingdom

|

3D printing integration and marine R&D

|

Hybrid manufacturing and premium prototype surfaces

|

|

Germany

|

Fire safety and circular materials

|

Functional, regulation-compliant gelcoat systems

|

|

China

|

Policy-backed scale and export diversification

|

High-volume, automated gelcoat production

|

|

United States

|

Local capacity expansion and marine compliance

|

Stable regional supply and performance-driven demand

|

|

European Union

|

Recycling and energy efficiency mandates

|

Shift toward recyclable and low-friction gelcoats

|

Gelcoat Market Report Scope

Gelcoat Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.9 Billion

|

|

Market Size (2034)

|

$18.6 Billion

|

|

Market Growth Rate

|

13.6%

|

|

Segments

|

By Resin Type (Polyester Gelcoat, Vinyl Ester Gelcoat, Epoxy Gelcoat, Specialty Resin Gelcoats), By Application Method (Sprayable Gelcoat, Brushable Gelcoat), By End-Use Industry (Marine, Transportation, Wind Energy, Construction and Architecture, Aerospace), By Product Functionality (Standard and Clear Gelcoats, Colored and Pigmented Gelcoats, Fire Retardant Gelcoats, Tooling Gelcoats, Antimicrobial and Bio-based Gelcoats)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

INEOS Composites, Polynt-Reichhold Group, Scott Bader Company Ltd., AOC, BÜFA Composite Systems, HK Research Corporation, Interplastic Corporation, Turkuaz Polyester, Jushi Group Co., Ltd., Binani Industries, BÜFA Composites, Syrgis Performance Initiators, Resins and Plastics Ltd., Allnex, Strongwell Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Gelcoat Market Segmentation

By Resin Type

- Polyester Gelcoat

- Vinyl Ester Gelcoat

- Epoxy Gelcoat

- Specialty Resin Gelcoats

By Application Method

- Sprayable Gelcoat

- Brushable Gelcoat

By End-Use Industry

- Marine

- Transportation

- Wind Energy

- Construction and Architecture

- Aerospace

By Product Functionality

- Standard and Clear Gelcoats

- Colored and Pigmented Gelcoats

- Fire Retardant Gelcoats

- Tooling Gelcoats

- Antimicrobial and Bio-based Gelcoats

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Gelcoat Industry

- INEOS Composites

- Polynt-Reichhold Group

- Scott Bader Company Ltd.

- AOC

- BÜFA Composite Systems

- HK Research Corporation

- Interplastic Corporation

- Turkuaz Polyester

- Jushi Group Co., Ltd.

- Binani Industries

- BÜFA Composites

- Syrgis Performance Initiators

- Resins and Plastics Ltd.

- Allnex

- Strongwell Corporation

*- List not Exhaustive