Geopolymers Market Overview: Rapid Geopolymer Adoption Fueled By Ultra-Low Carbon Binders, High-Temperature Stability, and Industrial By-Product Utilization

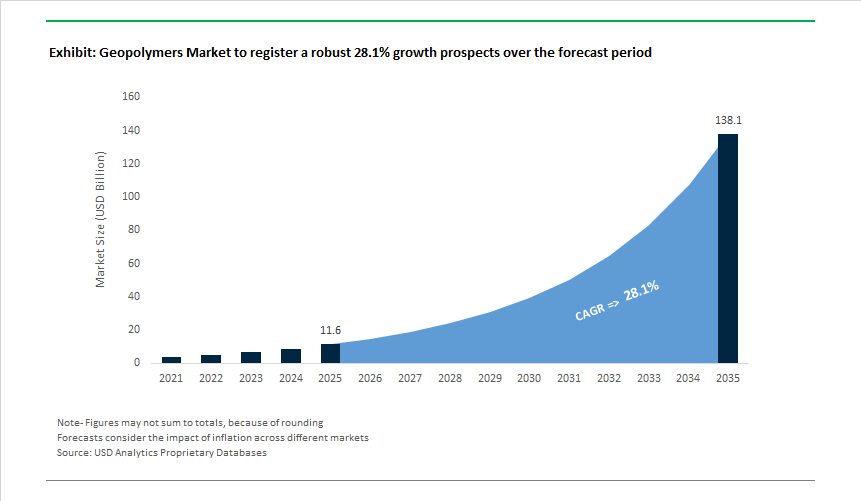

The Geopolymers Market is valued at USD 11.6 billion in 2025 and is expected to reach USD 138 billion by 2035, expanding at a strong 28.1% CAGR. Demand growth is rooted in geopolymer binders' ability to deliver 70-85% lower embodied carbon than Ordinary Portland Cement (OPC), while utilizing up to 100% industrial by-products-such as fly ash (Class F), GGBS, and red mud-as functional aluminosilicate feedstocks. Manufacturers like Wagners (Earth Friendly Concrete®) report compressive strengths above 40 MPa at 7 days without clinker-based cement, enabling faster construction cycles and competitive early-age performance in precast and in-situ systems. Geopolymer producers such as Banah UK and Zeobond (E-Crete) demonstrate minimal shrinkage, superior sulfate resistance, and exceptionally low chloride permeability, making geopolymer concretes suitable for marine, coastal, and steel-reinforced infrastructure exposed to aggressive ion environments.

A key technical driver is geopolymers’ inherent ceramic-like thermal stability, with leading formulations retaining structural cohesion after exposure to 1,100-1,200°C, far exceeding OPC concrete-which begins to experience microcracking and strength loss around 300-600°C. Independent furnace tests run by manufacturers show that geopolymer panels can remain load-bearing even after 2 hours of ISO 834 fire exposure, making them attractive for tunnels, battery storage buildings, petrochemical facilities, and defense infrastructure. In addition, alkali activation systems offered by class-leading activator suppliers allow engineered tunability of setting time, rheology, and acid resistance-enabling geopolymer mortars capable of surviving pH < 2 environments in industrial floors and wastewater treatment assets.

Manufacturers also highlight cost and sustainability advantages. Because geopolymer production relies on single-stage mixing without high-temperature calcination, operational energy consumption drops by over 60-70% relative to clinker production. Pilot lines from global precast manufacturers demonstrate 20-25% lower energy use during curing when switched to ambient-cured geopolymer mixes. Geopolymer rebar coatings, tiles, railway sleepers, façade panels, and 3D-printed building elements are rapidly entering mainstream adoption, validated by OEMs reporting high bond strengths, crack resistance, and superior freeze-thaw durability compared to OPC systems

Market Analysis: Rapid Scale-Up Of Geopolymer Plants, Government Procurement Signals, and Breakthrough Activation Chemistries Drive Market Maturity

Policy signals, plant scale-ups, and R&D breakthroughs have accelerated geopolymer commercialisation and supply-chain formation. In May 2024, Suvo Strategic Minerals formed a strategic partnership with PERMAcast LLC to advance low-carbon geopolymer solutions and secure upstream mineral processing supply, a foundational move for feedstock certainty. July 2024 saw Climate Tech Cement (Australia) launch Colliecrete, a metakaolin-based geopolymer concrete reported to deliver up to 70% CO₂ reduction, demonstrating early commercial productization with regional by-products. In Dec 2024, Material Evolution (UK) commissioned its Mevo A1 ultra-low carbon cement plant (120,000 t/yr capacity) using an alkali-fusion process, while Suvo Strategic Minerals formed a joint venture with PT Huadi HBIP in Indonesia to commercialize geopolymer cement from nickel slag-both moves indicating upstream industrialization of geopolymer feedstock processing.

The momentum continued through 2025 with policy and research tailwinds. In Sep 2025, the UK Government (DESNZ) extended consultation on a voluntary policy framework to expand low-carbon industrial products via embodied emissions reporting, directly supporting market pull for geopolymers in infrastructure procurement. Oct 2025 brought an R&D advance from Purdue University and research partners investigating hybrid activation and mechanochemical activation of slags, enhancing compressive strength and industrial viability. In Dec 2025, an Indian pilot led by IIT Indore together with the Odisha Government trialed a cement-free geopolymer concrete (fly ash + GGBS) for a Capital Region Ring Road project-an important public-sector validation in a high-demand infrastructure market. Earlier, Dec 2024 and May 2024 also featured commercialization and start-up activity (Novacret in India claiming cost advantages and rapid strength in tropical climates), all signaling that geopolymer systems are moving from lab and pilot phases into large-scale, licensable, and government-backed deployment.

Geopolymers Market: Trends and Opportunities

Performance-Based Standards Unlock Geopolymers for Regulated Construction Markets

The single largest structural barrier to geopolymer adoption—absence of prescriptive codes—is being dismantled through a decisive shift toward performance-oriented specifications, enabling engineers to specify materials by outcomes (strength, durability, exposure class) rather than chemistry. This transition materially changes bankability for public infrastructure and large commercial projects. In September 2025, ASTM International finalized ASTM C1912, a landmark specification that creates a compliant pathway for non-traditional supplementary cementitious materials (SCMs), including geopolymer precursors, without origin-based compositional limits. The implication is profound: “off-spec” ashes and emerging aluminosilicates can now be qualified on performance, expanding feedstock optionality while reducing approval risk.

Europe is moving in parallel. At a June 2025 workshop led by the European Commission Joint Research Centre, the framework for Second-Generation Eurocodes was finalized, with EN 1992 (Eurocode 2) explicitly accommodating low-carbon binders for cross-border, EU-funded works. In the U.S., an August 2025 AASHTO–ASTM pilot aims to harmonize adoption for bridge decks and pavements, accelerating the use of no-cement binders across state DOTs. Quality assurance timelines are also compressing: RILEM’s R3 methods (ASTM C1897) allow geopolymer producers to quantify precursor reactivity in 24 hours, replacing 28-day cycles and materially improving project scheduling and risk control for contractors.

Localization of Feedstocks Redefines Supply-Chain Resilience and Cost Curves

As coal fly ash availability declines, geopolymer value creation is shifting to localized, non-traditional feedstocks that reduce transport exposure and stabilize input costs. Calcined clays, rice husk ash (RHA), and water treatment sludge (WTS) are moving from experimental to validated inputs. In November 2025, peer-reviewed results confirmed that clay-based systems reinforced with 15% RHA achieved 32.28 MPa compressive strength—meeting structural thresholds for stabilized earth elements while using 100% agro-industrial waste.

Municipal waste integration is advancing at scale. A 2025 program led by IIT Guwahati converted WTS into geopolymer subgrade stabilizers exceeding CBR requirements for heavy-traffic pavements, while immobilizing heavy metals within a three-dimensional aluminosilicate matrix—addressing environmental liability alongside performance. On the industrial side, Holcim reported (Feb 2025) the rollout of 22 calcined-clay projects across Europe and Latin America, underpinning low-clinker platforms compatible with geopolymer binders. The versatility frontier extends further: in October 2025, the Italian Space Agency presented GLAMS results demonstrating 3D-printed geopolymer modules made from simulated lunar regolith—proof of extreme feedstock flexibility and in-situ resource utilization potential.

Infrastructure Rehabilitation Creates Near-Term Demand with Clear Procurement Signals

Public procurement is rapidly aligning with low-embodied-carbon materials, creating a tangible near-term opportunity for geopolymer repair and rehabilitation systems that offer rapid strength gain and long service life. In 2025, the U.S. General Services Administration launched a $2.15 billion Buy Clean pilot prioritizing “substantially lower embodied carbon” materials, explicitly favoring geopolymers for landmark federal assets where lifecycle emissions reductions of up to 80% vs. OPC are achievable. Complementing this, IRA allocations via the U.S. Environmental Protection Agency and U.S. Department of Transportation opened $2 billion for low-carbon materials in disaster recovery—an ideal fit for geopolymer spray-on liners in sewer and culvert rehabilitation where rapid set and chemical resistance are decisive.

Resilience mandates are expanding demand envelopes. Following the 2025 NATO Summit’s infrastructure mobility targets, geopolymers are being specified for wide temperature deployment (-15°C to 60°C) and precision re-leveling. Geobear’s recent sub-millimeter releveling of aircraft assembly facilities underscores deployability at scale. In Europe, October 2025 analyses tied geopolymer repairs to ~30-year lifecycle extensions for salt-exposed bridge decks, driven by intrinsic resistance to chloride-induced corrosion.

Ceramic-Like Performance Opens High-Temperature and Acid-Resistant Industrial Uses

Beyond construction, geopolymers are emerging as functional industrial materials where Portland cement fails—acidic, high-temperature, and chemically aggressive environments. In 2025, independent testing showed geopolymer concrete maintaining integrity under 5% sulfuric and nitric acid, avoiding gypsum/ettringite formation that drives OPC spalling; stability is attributed to the N-A-S-H gel network. Thermal capability is equally differentiating: February 2025 research confirmed metakaolin-based geopolymers undergo a ceramic transition near 900°C, enabling refractory linings with 10–15% mass reduction versus castables—translating to easier handling and lower thermal inertia.

Industrial case studies released in 2025 reported ~0.5% mass loss after 12 months for geopolymer-lined containment in steel and petrochemical plants, compared with >15% for high-performance Portland systems. Circular manufacturing models are also taking shape. WASP showcased 3D-printed geopolymer modules (2024–2025) that replace fired clay in industrial habitats while acting as carbon sinks—signaling a scalable pathway for durable, low-carbon industrial architecture.

Geopolymers Market Share Analysis

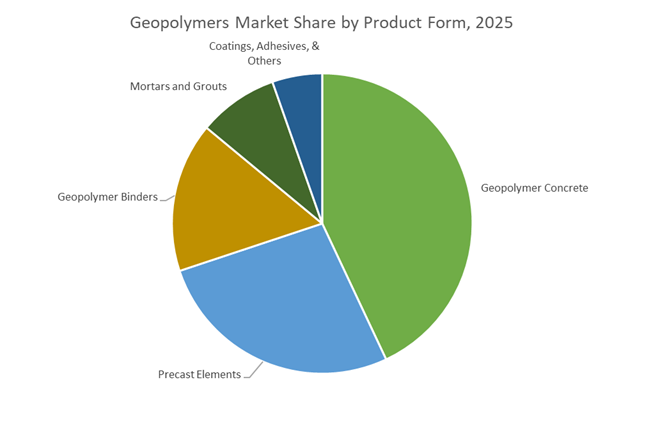

Market Share by Product Type: Geopolymer Concrete Emerges as the Scalable Low-Carbon Cement Alternative

Geopolymer concrete accounts for approximately 40% of the global Geopolymers Market, reflecting its position as the most commercially viable and scalable geopolymer product for mainstream construction activity. This dominance is driven by geopolymer concrete’s ability to function as a direct substitute for Ordinary Portland Cement (OPC) concrete while delivering a materially superior environmental profile. By eliminating the high-temperature calcination step inherent to OPC production, geopolymer concrete achieves 75–90% lower embodied carbon, making it one of the most effective decarbonization levers available to developers facing tightening ESG mandates and carbon disclosure requirements. Market share is further reinforced by rapid strength development, which allows geopolymer concrete to reach structural capacity within days rather than weeks, enabling faster project cycles and earlier asset utilization. From a performance perspective, lower drying shrinkage significantly reduces cracking risk, allowing larger pours and lowering long-term maintenance costs—an important economic consideration for infrastructure owners and commercial developers. On a project-by-project basis, the carbon savings achieved per cubic meter of geopolymer concrete translate into substantial emissions reductions at scale, positioning it as a preferred solution for large-volume pours where sustainability metrics are scrutinized most closely. Collectively, geopolymer concrete’s combination of carbon intensity reduction, construction efficiency, and structural reliability explains why it anchors the largest share of the global geopolymer product landscape.

Market Share by Application: Building and Construction Drive Commercial Adoption of Geopolymers

The building and construction segment represents approximately 30% of total geopolymer demand, making it the largest application area and the primary engine for market expansion. Adoption in this segment is driven not only by sustainability targets but also by superior fire, thermal, and chemical performance compared to conventional concrete systems. Geopolymer concrete’s inherent resistance to high temperatures—without explosive spalling—has elevated it as a preferred material for structural slabs and load-bearing elements in safety-critical buildings. Thermal stability further strengthens its value proposition, as lower thermal conductivity reduces heat transfer through structural elements, contributing to measurable reductions in building energy consumption over the asset lifecycle. In chemically aggressive construction environments, such as industrial zones or contaminated soils, geopolymers offer long-term durability advantages that significantly outperform OPC-based materials, reducing repair and replacement risks. Market share is also reinforced by the segment’s increasing reliance on green building certifications, where geopolymer use directly supports LEED and BREEAM innovation credits through verified Environmental Product Declarations. As regulatory, environmental, and performance expectations converge, building and construction remain the commercial gateway for large-scale geopolymer adoption, sustaining their leading share in the global market.

Competitive Landscape: Technology Leaders, Licensing Models, and Raw-Material Integration

Leading geopolymer participants differentiate via proprietary activation chemistries, license-based manufacturing models, upstream raw-material control (GGBS, fly ash, nickel slag), rapid strength formulations, and engineering certification pathways. Buyers and infrastructure clients evaluate suppliers on engineering compliance (AS3600, local codes), demonstrable large-pour workability, proof of long-term durability, and secure feedstock or JV access.

Wagners - Earth Friendly Concrete® At Commercial Scale For Certified Low-Carbon Projects

Wagners’ Earth Friendly Concrete (EFC) eliminates OPC from the mix and claims >70% embodied carbon reduction, with project deployments including marine works and institutional buildings (Pinkenba Shipping Wharf; University of Queensland). The company has demonstrated large continuous pours (310 m³) for commercial slabs, evidencing scalability and workability for logistics/warehouse applications, and is actively pursuing engineering certifications (e.g., AS3600) to accelerate government and infrastructure adoption.

Zeobond - Academic-Led Geopolymer IP and Licensee Expansion Into Developing Markets

Founded by geopolymer pioneer Professor Jannie S.J. van Deventer, Zeobond leverages deep technical IP and a licensing model to commercialise total cement replacement technologies using industrial by-products. As an influencer on Australia’s Green Building Council Expert Review Panel, Zeobond helps shape sustainable concrete standards while expanding licensee operations across Victoria, Queensland and Western Australia-aligning technology transfer with fast-growing regional infrastructure demand.

JSW Cement - Integrated GGBS Supply and Industrial Scale Roll-Out in India

JSW Cement’s strategic advantage rests on abundant GGBS reserves and a distribution network that can scale geopolymer blends across India’s infrastructure pipeline. Active collaboration with research institutions targets price-competitive geopolymer mixes for mass-market adoption (soil stabilization, non-structural applications), and JSW’s positioning enables rapid piloting within national road and urban projects-critical for lowering unit costs and achieving wide deployment.

Climate Tech Cement - Colliecrete and Licensing Strategy For Rapid Commercial Uptake

Climate Tech Cement commercialized Colliecrete in July 2024, a metakaolin-based geopolymer engineered for rapid strength gain and ~70% CO₂ reduction. The company focuses on proprietary low-carbon formulations and a licensing model that targets regional manufacturing partnerships (including JV activity in Southeast Asia) to secure resources such as nickel slag. Colliecrete’s accelerated curing performance and targeted structural specifications make it a compelling option for time-sensitive projects and retrofit schemes.

Australia continues to set the global benchmark for geopolymer commercialization by embedding alkali-activated binders into formal infrastructure specifications rather than pilot trials. The harmonization of state and national standards has reduced procurement risk for road, marine, and port authorities, enabling geopolymer concrete to compete head-to-head with OPC on durability, lifecycle cost, and embodied carbon. Revised Low Carbon Concrete mandates in New South Wales have further accelerated adoption by making geopolymer binders a primary compliance pathway for state-funded assets. From a supply-side perspective, industrial deployment by Wagners Holding Company demonstrates that high-strength, non-metallic geopolymer systems can be delivered at scale for aggressive marine environments, reinforcing Australia’s leadership in specification-driven demand rather than subsidy-led growth.

United States’ Tariff Shock and Federal Funding Reshaping Binder Economics

In the United States, geopolymer adoption is being catalyzed by a rare alignment of trade policy and infrastructure funding. New clinker and cement tariffs introduced in 2025 have materially altered cost curves, improving the price competitiveness of domestically produced geopolymer binders derived from fly ash and aluminosilicate by-products. Federal grants under the Bipartisan Infrastructure Law are also strengthening upstream feedstock security by supporting rare-earth recovery and advanced mineral processing-both of which generate high-purity geopolymer precursors. Beyond civil construction, defense and aviation procurement is emerging as a high-value niche, with rapid-setting geopolymer systems increasingly specified for airfield repair due to superior thermal resistance and fast strength gain. This dual civilian–defense pull positions the U.S. market as economically driven rather than purely regulatory.

European Union (Germany & France) Using Regulation to Force Low-Carbon Substitution

Across the European Union, geopolymer penetration is being driven by regulatory transparency rather than direct mandates. The revised Construction Products Regulation has made Environmental Product Declarations compulsory, structurally advantaging geopolymer binders with dramatically lower CO₂ intensity. Concurrent updates to Eurocodes have removed key technical barriers by allowing performance-based acceptance of non-traditional binders. French and German producers are scaling commercial geopolymer platforms within broader green-growth strategies, with companies such as Holcim integrating geopolymer technologies into mainstream product portfolios. Europe’s market trajectory is defined by regulatory pull and carbon accounting discipline, creating durable long-term demand signals for geopolymer suppliers.

India’s Fly Ash Management Mission Turning Waste into Strategic Feedstock

India’s geopolymer market is expanding rapidly as industrial waste management policy converges with infrastructure demand. The Fly Ash Management and Utilization Mission has effectively transformed fly ash from a disposal liability into a regulated construction input, guaranteeing feedstock availability within defined logistics radii. Public-sector utilities have invested heavily in dry fly ash extraction and bulk transport infrastructure, enabling consistent supply for geopolymer cement and masonry producers. On the demand side, approvals for geopolymer-stabilized subgrades in national highway projects are creating large, predictable consumption volumes. India’s approach is distinctive in that geopolymer adoption is driven less by carbon pricing and more by waste utilization mandates and infrastructure scale.

China’s Capacity Conversion and High-End Geopolymer Pivot

China’s geopolymer strategy reflects a structural response to slowing traditional cement demand. As real-estate-linked cement output contracts, producers are repurposing idle capacity toward specialty geopolymer manufacturing aligned with the country’s “Three-High” development goals. Joint ventures between international technology providers and domestic building materials groups-such as the expansion involving CNBM-are accelerating urban deployment of proprietary geopolymer platforms. At the policy level, geopolymer solidification of hazardous industrial waste has been elevated as a metric for green factory certification, embedding demand within China’s industrial decarbonization framework rather than standalone construction policy.

United Kingdom’s Rail and Tunnel Decarbonization Use-Case

In the United Kingdom, geopolymer adoption is being validated through complex retrofit and heritage infrastructure projects where conventional cement solutions are constrained. High-profile tunnel stabilization works have demonstrated faster installation, lower carbon intensity, and superior durability under aggressive groundwater conditions. National action plans now explicitly recognize geopolymer binders for rail preservation and nuclear waste containment, signaling confidence in long-term chemical stability and service life. The UK market is therefore emerging as a reference case for geopolymer performance in technically demanding, carbon-constrained applications rather than greenfield construction alone.

National Strategic Development Matrix: Geopolymers Market (2025)

Geopolymers Market Development Matrix by Country

|

Country / Region

|

Primary Strategic Driver

|

Key 2025 Policy or Project Trigger

|

Core Application Focus

|

|

Australia

|

Standardization & procurement reform

|

MRTS270 and Low Carbon Concrete mandates

|

Roads, marine works, ports

|

|

United States

|

Tariffs & federal infrastructure funding

|

Cement tariffs and DOE grants

|

Public works, defense airfields

|

|

EU (Germany & France)

|

Regulatory transparency (EPDs)

|

Revised CPR and Eurocode updates

|

Structural concrete, green buildings

|

|

India

|

Fly ash utilization mandate

|

CPCB directives and NHAI approvals

|

Highways, bricks, subgrades

|

|

China

|

Capacity conversion & green factories

|

JV scale-up and MIIT guidelines

|

Urban infrastructure, waste stabilization

|

|

United Kingdom

|

Infrastructure decarbonization

|

Rail and tunnel geopolymer retrofits

|

Rail assets, heritage tunnels

|

Geopolymers Market Report Scope

Ion Exchange Membranes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.1 Billion

|

|

Market Size (2035)

|

$1.7 Billion

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Membrane Charge Type (Cation Exchange, Anion Exchange, Bipolar, Amphoteric, Mosaic), By Material Type (Hydrocarbon, Perfluorocarbon, Inorganic, Composite, Partially Halogenated), By Structure (Homogeneous, Heterogeneous), By Application (Water Treatment & Desalination, Energy & Power, Chemical & Process Industry, Electronics & Semiconductors, Pharmaceutical & Biotechnology)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours Inc., AGC Inc., SUEZ S.A., Toray Industries Inc., LANXESS AG, 3M Company, Ion Exchange (India) Limited, Mitsubishi Chemical Group, FUJIFILM Corporation, Samyang Corporation, Merck KGaA, Ionomr Innovations Inc., Saltworks Technologies Inc., Hyproof Technology (Shanghai) Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Geopolymers Market Segmentation

By Raw Material Type

- Fly Ash-Based

- Slag-Based

- Metakaolin-Based

- Natural Aluminosilicate-Based

- Other Sources

- Hybrid Systems

By Product Form

- Geopolymer Binders

- Geopolymer Concrete

- Precast Elements

- Mortars and Grouts

- Coatings and Adhesives

By Application

- Building and Construction

- Infrastructure and Transportation

- Marine Structures

- Repair and Rehabilitation

- Industrial

- Oil and Gas and Mining

- Composites

- Art and Decoration

By Curing Method

- Ambient Curing

- Heat Curing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Geopolymers Market

- BASF SE

- Schlumberger Limited

- CEMEX, S.A.B. de C.V.

- Wagners Holding Company

- Imerys S.A.

- Tata Steel Limited

- PCI Augsburg GmbH

- Zeobond Pty Ltd.

- Geopolymer Solutions LLC

- banah UK Ltd.

- Heidelberg Materials AG

- Milliken & Company, Inc.

- Coromandel International Limited

- Corning Incorporated

*- List not Exhaustive