Germany Water Treatment Chemicals Market Value Analysis and Forecast

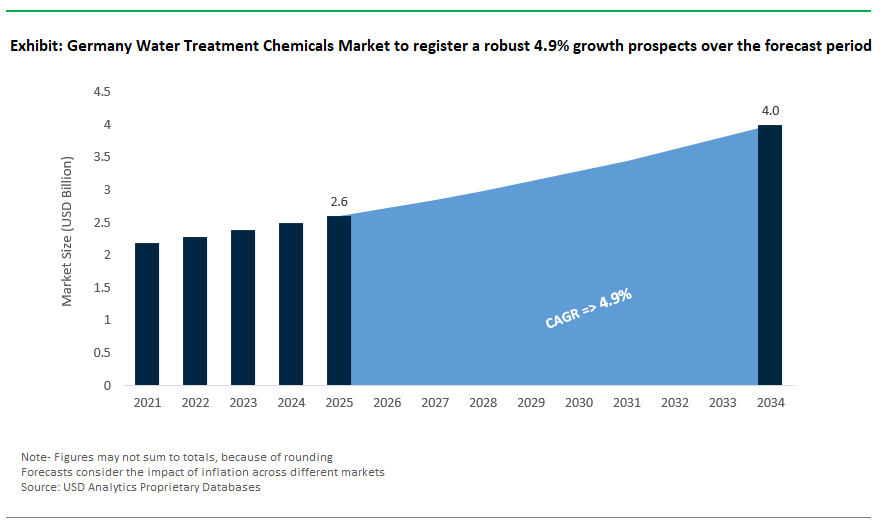

Germany Water Treatment Chemicals Market Size is estimated at $2.6 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 4.9% to reach $4 Billion by 2034.

Germany’s water treatment chemicals market is evolving rapidly, driven by a combination of environmental regulations, infrastructure modernization, and national efforts to promote circular economy practices. Stricter enforcement of the German Drinking Water Ordinance (TrinkwV) aligned with EU Drinking Water Directive standards has led utilities to intensify efforts to mitigate contaminants such as lead and disinfection byproducts. Lead control strategies, such as orthophosphate dosing, have become increasingly common, particularly in older distribution networks, to reduce lead solubility in pipes. This aligns with the EU’s revised lead limit of 5 µg/L under the updated Drinking Water Directive 2020/2184.

To ensure compliance with trihalomethane (THM) and haloacetic acid thresholds, utilities are adopting alternative disinfectants like chlorine dioxide (ClO₂) and supplementing with granular activated carbon (GAC) filtration. GAC systems are widely used in Germany and are capable of removing more than 90% of natural organic matter, thereby reducing DBP precursors.

In the industrial segment, companies particularly in the energy, manufacturing, and chemical industries are transitioning to phosphonate-free antiscalants and corrosion inhibitors such as polyaspartic acid (PASP) and polyepoxysuccinic acid (PESA). These chemicals are compliant with the REACH regulation and VDI 2035 guidelines, which emphasize non-hazardous treatment approaches. There is also a notable reduction in the use of zinc-based formulations due to environmental toxicity concerns.

Biocidal control practices are changing as well, particularly due to restrictions under the EU Biocidal Products Regulation (BPR). Safer alternatives like 2,2-Dibromo-3-nitrilopropionamide (DBNPA) and tetrakis(hydroxymethyl)phosphonium sulfate (THPS) are increasingly being adopted in place of substances like glutaraldehyde, which has been reclassified for higher toxicity risks.

Advanced industrial facilities are adopting Zero Liquid Discharge (ZLD) systems to reduce wastewater generation. These systems typically use terpolymer antiscalants, advanced oxidation processes, and membrane filtration to handle high Total Dissolved Solids (TDS) and Chemical Oxygen Demand (COD) levels. In Germany, Berlin Waterworks (Berliner Wasserbetriebe) has implemented struvite precipitation for phosphorus recovery, reportedly extracting over 18,000 tons of phosphorus annually, in compliance with the German Sewage Sludge Ordinance. This ordinance mandates phosphorus recovery from sludge for large wastewater treatment plants (>100,000 PE) starting in 2029 if phosphorus content exceeds 2% by dry weight.

Efforts to mitigate PFAS contamination have led to the piloting of hybrid ion exchange systems and advanced oxidation technologies, including plasma reactors. These technologies reportedly achieve >99% mineralization of PFAS under controlled laboratory and field trials, as documented by academic research partnerships (e.g., Karlsruhe Institute of Technology).

Seasonal factors also play a role Germany’s colder winters cause increased coagulant demand due to reduced reaction kinetics and higher water viscosity. Additionally, over 45% of Germany’s pipeline infrastructure predates 1970, necessitating customized chemical formulations for legacy systems.

In line with the Circular Economy Act (KrWG), utilities are piloting biodegradable coagulants such as lignosulfonate-based formulations, which have demonstrated turbidity removal rates above 80% and biodegradability exceeding 95% in lab and pilot-scale trials.

Germany is also investing in next-generation technologies like boron-doped diamond (BDD) electrodes for oxidation of recalcitrant pollutants, including pharmaceuticals and PFAS. Moreover, AI-based chemical dosing systems are being deployed in several wastewater treatment plants to optimize chemical usage companies like Siemens and Veolia have integrated such systems to achieve 20–30% reduction in chemical consumption, supported by real-time sensor data.

Market Trend: Rise of Bio-Based Chemistry and Digital Optimization

Germany’s water treatment chemicals market is increasingly shaped by bio-based formulations and digital dosing innovations, aligned with climate and resource goals. The Chemikalien-Klimaschutzverordnung (ChemKlimaschutzV), passed in 2023, outlines a phased approach to achieving carbon-neutral chemical processes by 2035, reinforcing demand for plant-based and low-impact chemical alternatives.

One notable development is the adoption of Sokalan® BioPure a plant-derived coagulant developed by BASF at the Waßmannsdorf wastewater treatment plant in Berlin. Early case studies show up to 30% reduction in sludge volume, aiding compliance with circular economy targets.

In parallel, digital water platforms, such as Siemens' Water 4.0, are becoming mainstream. At Thyssenkrupp’s Duisburg steelworks, AI-powered dosing optimization reportedly reduced phosphate inhibitor consumption by 25%, lowering both operational costs and environmental discharge.

As the EU PFAS ban (phased-in from 2025 under REACH proposals) approaches, German manufacturers are transitioning to fluorine-free surfactants, siloxane-free defoamers, and other safer alternatives. This proactive shift positions Germany as a leader in green water treatment solutions across Europe.

Market Opportunity: Hydrogen and Battery Ecosystem as Growth Catalyst

Germany’s water treatment chemical demand is set to grow significantly alongside its clean energy and advanced manufacturing initiatives. The National Hydrogen Strategy supports green hydrogen production via PEM and alkaline electrolyzers, which require ultra-pure water (UPW) and specialty antiscalants. Siemens Energy’s “HyPure” chemical range, reportedly in use at the Lingen Hydrogen Hub, has demonstrated a 50% reduction in regenerant usage during pilot deployments.

Simultaneously, Germany’s efforts to close the loop in battery manufacturing and recycling are driving demand for advanced water treatment processes. BASF’s battery recycling facility in Schwarzheide incorporates water reuse technologies to recover lithium and cobalt from acidic leachates, achieving over 90% water reuse efficiency, which qualifies under Germany's circular economy funding mechanisms (e.g., BMUV subsidies of up to €200/ton recovered).

In the high-tech sector, facilities like Infineon’s Dresden semiconductor fab are adopting TOC-free biocides and membrane protectants that meet ultra-low contamination thresholds (<1 ppb). Merck KGaA is among suppliers offering such formulations its AquaPurge product line is tailored for high-purity water systems used in electronics and pharma.

The Federal Water Strategy (Nationale Wasserstrategie), launched in 2023, provides €1.4 billion in funding through 2030 to support climate-resilient and resource-efficient water infrastructure. This positions Germany as a strategic hub for green water treatment chemicals, with growing export potential to other EU markets and beyond.

Competitive Landscape: Germany Water Treatment Chemicals Market

Germany’s water treatment chemicals market features a complex and strategic competitive environment. Multinational companies, local specialty firms, and emerging innovators each use unique skills to meet the country’s strict regulatory standards and diverse industries. Global chemical leaders hold about 55% of the market. They are deeply linked with Germany’s major industries and have a strong presence in both municipal and industrial water markets. BASF, Ecolab, LANXESS, and Kemira make up the primary Tier 1 group. They use proprietary product platforms, real-time monitoring technologies, and sustainability-focused innovations to secure long-term contracts with key players in sectors like automotive, pharmaceuticals, food processing, and energy. These companies not only have the widest product ranges, from biodegradable scale inhibitors to advanced coagulants, but they also benefit from digital services such as BASF’s “Sensolute” and Ecolab’s “3D TRASAR.” These services are becoming standard in high-specification treatment processes.

Tier 2 participants mainly include German specialty chemical firms and some European companies with local operations, capturing around 30% of the market. Their competitive strength comes from targeted solutions, regional technical support, and cost advantages with generic formulations. Companies like Brenntag and Kurita Europe customize water treatment solutions for mid-sized manufacturers and important infrastructure clients. They often focus on ultra-pure water systems, alternatives that comply with REACH, and cooling water chemistries. Their ability to price their commoditized products 10 to 15% lower than global competitors allows them to maintain a strong position, especially in areas where price matters more than brand recognition or digital features.

The final 15% of the market is held by a growing number of German startups and innovative small to medium-sized enterprises (SMEs) that are quickly gaining ground, particularly in regulatory-focused and technological niches. Companies such as Aqualytix and GreenWater Tech are creating AI-based dosing systems, enzyme-driven anti-biofouling agents, and PFAS-free disinfection technologies, often supported by public funding, like BMWi or Horizon Europe. These disruptors leverage Germany’s engineering expertise to target local municipal utilities and hard-to-treat pollutants while also preparing for export in markets that value European green-tech standards.

Geographically, the competitive landscape reflects Germany’s industrial clusters. The Ruhr Valley is the hub for heavy industry water treatment, favoring companies with strong corrosion and scale control solutions. Bavaria, known for semiconductors and automotive, requires ultra-pure and precisely dosed solutions. Lower Saxony’s food processing sector prefers low-cost, high-volume coagulants and microbial controls. In these areas, success increasingly hinges on combining chemical effectiveness with digital integration, local customization, and foresight regarding regulations. This is particularly relevant as REACH guidelines tighten, regulations on microplastics increase, and PFAS bans raise compliance standards.

Germany Water Treatment Chemicals Market– Segmentation Insights (2025–2034)

Germany Water Treatment Chemicals Market: Coagulants Lead, Membrane Cleaning Chemicals Accelerate

In the Germany water treatment chemicals market, coagulants and flocculants are projected to hold the largest market share at 24.6% in 2025, driven by stringent compliance requirements under the EU Urban Wastewater Treatment Directive and local environmental protection regulations. These chemicals are essential in municipal and industrial wastewater treatment plants, where removal of suspended solids and turbidity is prioritized to meet effluent discharge norms. Germany’s long-standing commitment to high-quality wastewater processing and sludge minimization continues to fuel demand for advanced polymer-based flocculants and metal salt coagulants. Meanwhile, membrane cleaning chemicals are set to record the fastest growth with a CAGR of 5.7% through 2034, reflecting the increasing use of reverse osmosis (RO) and nanofiltration (NF) systems in both municipal and industrial facilities. As Germany scales up its reliance on membrane technologies for ultrapure water production and effluent recycling, the use of chemical agents designed to prevent membrane fouling, scaling, and biofilm formation becomes critical. This dual dynamic regulatory compliance on one hand and membrane expansion on the other is reshaping the chemical demand profile across the nation’s water treatment ecosystem.

.png)

Germany Water Treatment Chemicals Market: Municipal Sector Dominates, Industrial Sector Grows Fastest

Municipal water treatment is expected to lead the German market with a 44.2% share in 2025, sustained by extensive public investments in drinking water safety, sewage infrastructure, and decentralized treatment systems. Germany’s municipal authorities operate under some of the world’s most rigorous water quality standards, which require continuous dosing of coagulants, disinfectants, pH adjusters, and corrosion inhibitors to ensure compliance with national and EU guidelines. The push for integrated nutrient removal, especially nitrogen and phosphorus, is also intensifying chemical demand in wastewater utilities. However, industrial water treatment is forecast to be the fastest-growing segment, expanding at a CAGR of 6.8% during forecast period. This growth is propelled by rising water consumption and effluent generation in industries such as automotive, food & beverage, and chemicals sectors where Germany holds global leadership. In response to circular economy policies and water reuse targets, these industries are adopting advanced water treatment technologies that rely heavily on specialty chemicals for boiler feed conditioning, cooling system treatment, and closed-loop process water management. This dual-market structure is strengthening Germany’s position as a mature yet innovation-driven market for water treatment chemicals in Europe.

Germany Water Treatment Chemicals Report Scope

Germany Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.6 Billion

|

|

Market Size (2034)

|

$4 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Biocides and Disinfectants, pH Adjusters and Softeners, Corrosion and Scale Inhibitors, Defoamers and Antifoaming Agents, Oxygen Scavengers, Membrane Cleaning Chemicals, Other Specialty Chemicals), By Application (Municipal Water Treatment, Industrial Water Treatment, Commercial Water Treatment), By End-User Industry (Municipal (Water and Sewage Utilities), Power Generation, Chemical and Petrochemical, Manufacturing), By Form of Chemical (Liquid, Powder/Solid

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE (Germany), Ecolab Inc. (U.S.), Kurita Water Industries Ltd. (Japan), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Floerger (France), Veolia Water Technologies (France), The Dow Chemical Company (U.S.), Nouryon (The Netherlands), Solvay S.A. (Belgium), SUEZ S.A. (France), Lonza Group (Switzerland), EnviroChemie GmbH (Germany), Judo Wasseraufbereitung GmbH (Germany), Feralco Deutschland GmbH (Germany),

|

Germany Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Biocides and Disinfectants

- pH Adjusters and Softeners

- Corrosion and Scale Inhibitors

- Defoamers and Antifoaming Agents

- Oxygen Scavengers

- Membrane Cleaning Chemicals

- Other Specialty Chemicals

By Application

- Municipal Water Treatment

- Drinking Water Treatment Plants

- Municipal Wastewater Treatment

- Industrial Water Treatment

- Cooling Water Treatment

- Boiler Water Treatment

- Process Water Treatment

- Industrial Wastewater Treatment

- Water Reuse and Recycling

- Sludge Treatment and Management

- Commercial Water Treatment

By End-User Industry

- Municipal (Water and Sewage Utilities)

- Power Generation

- Chemical and Petrochemical

- Manufacturing

- Automotive

- Food and Beverage

- Pharmaceutical

- Pulp and Paper

- Textile

- Mining and Metallurgy

- Electronics and Semiconductors

- Other Industrial Manufacturing

By Form of Chemical

Top Companies in Germany Water Treatment Chemicals Market

- BASF SE (Germany)

- Ecolab Inc. (U.S.)

- Kurita Water Industries Ltd. (Japan)

- Solenis LLC (U.S.)

- Kemira Oyj (Finland)

- SNF Floerger (France)

- Veolia Water Technologies (France)

- The Dow Chemical Company (U.S.)

- Nouryon (The Netherlands)

- Solvay S.A. (Belgium)

- SUEZ S.A. (France)

- Lonza Group (Switzerland)

- EnviroChemie GmbH (Germany)

- JudWasseraufbereitung GmbH (Germany)

- FeralcDeutschland GmbH (Germany)

* List Not Exhaustive

Research Coverage

This report by USDAnalytics provides an in-depth analysis of the Germany Water Treatment Chemicals Market, offering actionable insights for stakeholders across the municipal, industrial, and commercial water treatment value chain. The study examines critical factors such as regulatory enforcement under TrinkwV and EU directives, the shift toward bio-based and PFAS-free formulations, and the adoption of digital dosing technologies. It evaluates growth catalysts like green hydrogen initiatives, semiconductor manufacturing, and battery recycling, which are driving demand for ultrapure water (UPW) chemicals and high-performance corrosion inhibitors.

Scope Includes:

- Segmentation Scope:

- By Type of Chemical: Coagulants & Flocculants, Biocides & Disinfectants, pH Adjusters & Softeners, Corrosion & Scale Inhibitors, Oxygen Scavengers, Membrane Cleaning Chemicals, Defoamers, and Other Specialty Chemicals

- By Application: Municipal Water Treatment (Drinking Water, Wastewater), Industrial Water Treatment (Cooling, Boiler, Process, Reuse, Sludge), Commercial Water Treatment

- By End-User: Municipal Utilities, Power Generation, Automotive, Chemical & Petrochemical, Electronics & Semiconductors, Food & Beverage, Pharmaceutical, Pulp & Paper, Textile, Mining & Metallurgy

- By Form: Liquid, Powder/Solid

- Geographic Scope: Analysis covers Germany in detail with relevance to EU trends.

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

- Key Players: BASF SE, Ecolab Inc., Kurita Water Industries Ltd., Solenis LLC, Kemira Oyj, SNF Floerger, Veolia Water Technologies, Nouryon, SUEZ S.A., Lonza Group, and leading German innovators such as EnviroChemie GmbH and JudWasseraufbereitung GmbH.

Methodology

- This research is built on a hybrid methodology combining primary and secondary data sources, ensuring the highest accuracy for projections and market sizing. The approach includes:

- Primary Research: Interviews with municipal water utilities, industrial plant managers, and procurement heads in key German industries, along with discussions with chemical manufacturers and environmental regulators.

- Secondary Research: Analysis of policy documents from BMUV, Umweltbundesamt (UBA), REACH, and EU water directives; market data from trade associations; and corporate financial disclosures.

- Data Modeling: Uses top-down and bottom-up estimation techniques, validated by demand-side and supply-side triangulation.

- Forecasting Models: Incorporates regulatory impact modeling, industrial expansion indices, and ESG-linked procurement trends to predict future demand dynamics.

- Validation: Cross-checked through multiple datasets, including performance benchmarks from Germany’s leading industrial clusters and municipal water authorities.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements