Glass Coatings Market Growth Driven by Smart Glazing, Energy Efficiency Mandates, and Advanced Functional Coatings

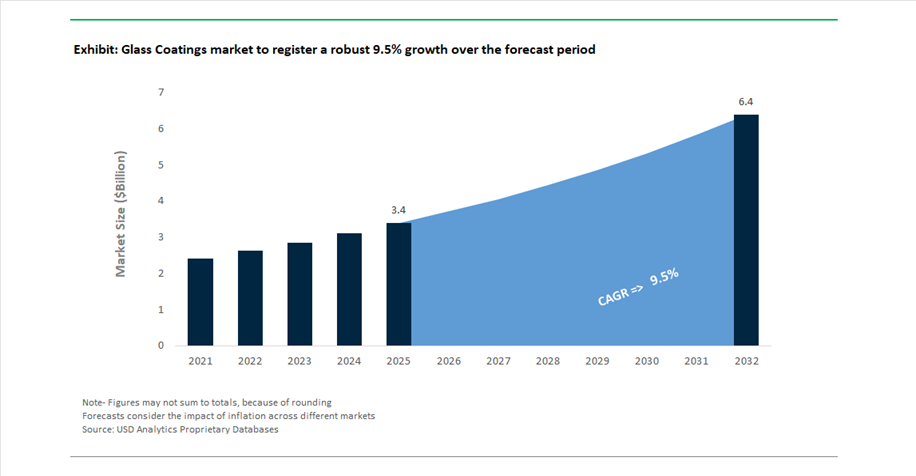

The global Glass Coatings Market was valued at USD 3.4 billion in 2025 and is projected to grow at a CAGR of 9.5% between 2025 and 2032, reaching USD 6.4 billion by 2032. This robust growth reflects rising demand for energy-efficient, multifunctional, and high-performance coated glass across architectural, automotive, and electronics applications.

Glass coatings are critical for enhancing thermal insulation, UV protection, anti-glare performance, scratch resistance, and solar control, making them indispensable in modern infrastructure and advanced devices. A key structural driver is the global push toward energy-efficient buildings, where Low-E (low emissivity) coatings are widely used to reduce heat transfer and improve indoor climate control. These coatings play a central role in achieving green building certifications and net-zero construction targets, particularly in Europe, North America, and rapidly urbanizing Asia-Pacific markets.

Another major growth catalyst is the integration of smart and multifunctional coating systems. Modern coated glass is evolving beyond passive protection to include dynamic light control, anti-reflective properties, and embedded functionalities for smart buildings and automotive displays. Additionally, the rapid expansion of automotive digital cockpits and consumer electronics is driving demand for coatings that improve visibility, durability, and user experience under high ambient light conditions.

Privatization Strategies, Smart Coating Integration, and Regulatory-Driven Innovation Reshape Market Dynamics

The glass coatings market is undergoing a structural transformation driven by corporate restructuring, technological innovation, and regulatory compliance requirements. In March 2026, Nippon Sheet Glass (NSG Group) announced its move to go private through an investment from Apollo Global Management. This strategic shift is designed to unlock long-term capital for accelerating investments in architectural and automotive coating technologies, particularly in high-performance glazing solutions.

Regulatory-driven product innovation is gaining momentum. In January 2026, Guardian Glass launched its Bird1st™ UV-coated glass, designed to meet stringent building regulations such as New York City’s Local Law 15. The coating is engineered to be visible to birds but invisible to humans, addressing ecological concerns while maintaining architectural aesthetics. The product also received validation from the American Bird Conservancy, strengthening its adoption in LEED-certified and government-backed projects.

Manufacturing expansion is supporting regional demand growth. In March 2025, Saint-Gobain expanded its production capacity in Chennai, India, focusing on high-performance coated glass for sustainable construction. This move aligns with increasing demand for energy-efficient glazing solutions in emerging markets.

Technological advancements are enhancing functionality across applications. In April 2026, AGC Inc. advanced its anti-glare (AG) coating technologies, enabling improved visibility for consumer electronics and automotive displays through micro-textured surface engineering. Additionally, industry developments in October 2025 highlighted the integration of smart glass functionalities into Low-E coating stacks, enabling a single layer to deliver both thermal insulation and dynamic light control.

Corporate growth strategies are also strengthening market reach. In February 2026, Sherwin-Williams reported strong financial performance driven by the integration of Suvinil, enhancing its ability to distribute protective glass coatings across Latin America.

Leadership and strategic direction are influencing regional growth. In March 2025, Saint-Gobain appointed new leadership for its Asia-Pacific operations, signaling an intensified focus on lightweight, sustainable construction materials, including advanced glass coatings.

Innovation in coating durability and performance continues to evolve. In March 2026, PPG Industries was recognized for its innovation in electrocoat and digital technologies, contributing to advancements in durable and thermally efficient glass coatings for industrial and automotive applications.

High-Transparency TCO Coatings Enabling Building-Integrated Photovoltaics (BIPV)

The glass coatings industry is undergoing a transformation as building-integrated photovoltaics gain momentum as a core component of energy-efficient architecture. Transparent conductive oxide coatings, including fluorine-doped tin oxide and aluminum-doped zinc oxide, are being engineered to optimize both visible light transmission and near-infrared performance, enabling glass facades to function as active energy-generating surfaces. Modern TCO coatings achieve visible light transmission levels exceeding 90% while enhancing near-infrared transmission, allowing thin-film solar cells integrated into glass structures to improve energy conversion efficiency by approximately 21%. Material selection is also evolving, with aluminum-doped zinc oxide gaining traction due to cost advantages and improved spectral tuning, leading to nearly 48% growth in adoption for large-scale facade applications. Additionally, advancements in optical engineering are reducing surface reflection losses to below 2%, significantly improving overall system efficiency compared to conventional architectural glass. Durability remains a key focus area, with hard-coat TCO systems extending operational lifespans by approximately 27%, ensuring compatibility with the 25-year lifecycle requirements of building components. These developments are positioning TCO-coated glass as a central technology in the convergence of construction and renewable energy systems.

Silver-Ion Antimicrobial Glass Coatings Becoming Standard in Automotive Interiors

The increasing integration of digital interfaces in vehicle interiors is driving demand for antimicrobial glass coatings that enhance hygiene and durability in high-touch environments. Silver-ion-based coatings are emerging as the preferred solution, offering continuous antimicrobial protection by disrupting microbial cell activity at the surface level. These coatings demonstrate efficacy levels of up to 99.99% reduction in bacterial populations and approximately 99.8% reduction in viral presence, significantly reducing contamination risks in shared mobility environments. Unlike temporary surface treatments, silver-ion coatings are integrated into the glass during the chemical strengthening process, ensuring long-term durability and resistance to wear. Performance testing indicates that these coatings maintain effectiveness even after more than 10,000 abrasive cleaning cycles, making them suitable for automotive applications requiring long service life. Additionally, modern formulations combine antimicrobial functionality with anti-glare and anti-reflective properties, ensuring compatibility with high-definition display systems used in advanced infotainment and control interfaces. By early 2026, antimicrobial coatings are being incorporated into approximately 63% of next-generation vehicle touchscreen systems, reflecting strong adoption driven by consumer hygiene expectations and regulatory focus on occupant safety.

EU EPBD Mandates Driving Adoption of Low-Emissivity and Solar-Integrated Glass Coatings

The revised Energy Performance of Buildings Directive is creating a substantial opportunity for advanced glass coatings in Europe by mandating large-scale building retrofits and the transition toward zero-emission construction. The directive requires the renovation of the least energy-efficient buildings by 2030, driving demand for high-performance glazing systems incorporating multi-layer low-emissivity coatings capable of achieving U-values below 1.0 W per square meter Kelvin. These coatings play a critical role in reducing heat transfer, improving insulation, and lowering overall energy consumption in commercial and residential buildings. Additionally, the directive mandates the integration of solar technologies in large public buildings, creating direct demand for transparent conductive oxide coatings used in building-integrated photovoltaic systems. With buildings accounting for approximately 40% of total energy consumption in the European Union, the widespread adoption of coated glass solutions is expected to contribute to a 16% reduction in energy use by 2030 compared to 2020 levels. These regulatory drivers are positioning energy-efficient glass coatings as a cornerstone of sustainable building design and renovation strategies across Europe.

US DOE SETO Programs Driving Development of Anti-Soiling Glass Coatings for Solar Installations

The United States Department of Energy’s Solar Energy Technologies Office is accelerating innovation in anti-soiling glass coatings, particularly for utility-scale solar installations in arid and desert environments. Dust accumulation is a major challenge in these regions, with the potential to reduce solar panel output by more than 30% if not effectively managed. Advanced anti-soiling coatings are being developed to minimize this impact, targeting performance benchmarks that limit energy loss to less than 1% under real-world conditions. These coatings combine hydrophobic and hydrophilic properties to enable self-cleaning behavior, where minimal moisture from dew or light rainfall is sufficient to remove accumulated dust particles. The economic impact is significant, with large-scale installations benefiting from reduced manual cleaning requirements and lower operational costs. For solar farms exceeding 100 megawatts, the adoption of anti-soiling coatings can reduce maintenance expenses by approximately 15% to 20% over the first five years of operation. With the global market for solar glass coatings projected to reach several billion dollars over the next decade, these developments are positioning anti-soiling technologies as a critical enabler of efficient and cost-effective solar energy generation.

Glass Coatings Market Share 2025: Magnetron Sputtering and Flat Glass Applications Lead Growth

Coating Process Insights: Magnetron Sputtering Dominates Low-E Glass Production

The magnetron sputtering segment leads the glass coatings market with a 42% market share in 2025, driven by its critical role in the large-scale production of low-emissivity (Low-E) coated glass for energy-efficient buildings. This advanced coating process enables the deposition of multi-layer silver-based coatings with precise thickness control, ensuring optimal thermal insulation and solar control performance. Magnetron sputtering is widely adopted in architectural applications, particularly for commercial facades, curtain walls, and high-performance windows, where energy efficiency and aesthetics are paramount. A key advantage is its ability to coat jumbo glass substrates up to 3.2m × 6m with exceptional uniformity (±2% thickness variation), meeting the stringent quality requirements of modern construction projects. As global demand for energy-efficient glazing solutions and green building materials continues to rise, magnetron sputtering will remain the dominant coating technology in the glass coatings market.

Glass Type Insights: Flat Glass Leads with Construction and Automotive Demand

The flat glass segment dominates the glass coatings market with a 55% market share in 2025, supported by strong demand from the construction and automotive industries. Coated flat glass is extensively used in windows, facades, skylights, and automotive glazing, offering functionalities such as solar control, anti-reflective properties, and self-cleaning surfaces. The push for green building certifications like LEED and BREEAM, along with stringent energy efficiency regulations across Europe, China, and North America, is driving widespread adoption of Low-E coated flat glass in residential and commercial construction. Additionally, the growing popularity of electric vehicles (EVs) with large panoramic glass roofs is increasing the need for coatings that provide heat rejection and UV protection. As sustainability and energy efficiency become central to infrastructure development, flat glass coatings will continue to dominate the global glass coatings market.

Glass Coatings Market Competitive Landscape: Energy-Efficient Glazing, Smart Coatings, and Sustainable Technologies Driving Growth

The glass coatings market is highly competitive, driven by demand for energy-efficient glazing, low-E coatings, and advanced functional glass in construction, automotive, and electronics. Key players are focusing on sustainable formulations, AI-driven design tools, and high-performance coatings to meet green building and next-generation communication requirements.

PPG leads global glass coatings innovation with sustainable sol-gel technologies and OEM dominance

PPG Industries is a global leader in the glass coatings market, supported by strong financial performance and innovation in high-performance glazing solutions. The company reported Q1 2026 adjusted EPS of $1.83, a 6% year-over-year increase, driven by demand across industrial and transportation coatings. Building on its $15.9 billion 2025 revenue, PPG introduced advanced glass coatings with superior scratch resistance and chemical durability for extreme environments. With operations in over 50 countries, it maintains leadership in automotive OEM and architectural glass coatings. 44% of its 2026 sales come from sustainably advantaged products, including low-VOC and energy-efficient sol-gel coatings. This combination of scale, sustainability, and performance innovation reinforces PPG’s competitive edge.

Saint-Gobain dominates low-E glass coatings with high-growth European infrastructure and green building solutions

Saint-Gobain is a dominant player in coated glass, particularly in Europe and North America, driven by strong demand for energy-efficient building materials. The company is leveraging a strong growth in advanced glass to secure high-margin infrastructure projects. Its magnetron sputtering coatings are industry benchmarks for thermal insulation performance. The ECLAZ® low-E glass technology enhances natural light transmission while delivering insulation equivalent to triple glazing, supporting green building mandates. Through its “Grow & Impact” strategy, Saint-Gobain provides integrated solutions combining coatings with laminated safety glass, targeting the 40.5% laminated segment share. This integration strengthens its leadership in sustainable architectural glazing.

NSG Group accelerates restructuring to focus on solar and automotive glass coatings for energy transition

NSG Group is undergoing a major strategic transformation to strengthen its position in the glass coatings market. In March 2026, the company agreed to a $3.7 billion acquisition by Apollo Funds, enabling delisting and capital restructuring. A 165 billion yen investment will reduce debt and fund R&D in energy-efficient architectural glass technologies. Its Pilkington Activ™ product remains a global benchmark in self-cleaning glass coatings, using UV radiation to break down organic contaminants. The “New NSG Group” strategy prioritizes solar energy glass and advanced automotive glazing. This repositioning enhances its competitiveness in sustainable and e-mobility-driven glass coating markets.

Guardian Glass advances AI-driven coating selection and solar control glass for next-generation buildings

Guardian Glass is strengthening its market position through digital innovation and sustainable glass coating solutions. In January 2026, Merritt Gaunt was appointed CEO to lead the company’s next phase of growth. The launch of CLARIA™, an AI-powered assistant, enables architects and processors to optimize coating selection and thermal performance in real time. Guardian has achieved verified Health Product Declarations for its vacuum-coated and UltraMirror® products, aligning with clean construction standards. Its Resource Hub and Training Center provide continuous technical support, enhancing adoption of Solar Management Glass Xtra for optimal light and heat control. This focus on digitalization and sustainability positions Guardian as a leader in smart glass coatings.

AGC leads Asia-Pacific glass coatings with advanced anti-glare and high-frequency communication solutions

AGC Inc. is a dominant force in the glass coatings market, particularly in the Asia-Pacific region where it holds a robust share supported by a vast network of subsidiaries. The company reported consolidated revenue of 20,588 billion yen, reflecting its scale and diversified portfolio. AGC is a global leader in anti-glare glass coatings, a segment projected to grow significantly due to rising demand in automotive displays and consumer electronics. Its integration of electronics and chemical businesses enables the development of low-dielectric coatings for 6G communication infrastructure. The company showcased next-generation Fine Glass products in high-speed communication technologies. This innovation-driven approach strengthens AGC’s leadership in advanced functional glass coatings.

Sherwin-Williams enhances decorative and industrial glass coatings with AI-driven color forecasting and design support

The Sherwin-Williams Company is expanding its presence in the glass coatings market through advanced color systems and industrial coating solutions. In February 2026, the company launched SHIFT, its industrial color trend forecast featuring 18 curated colors for glass coating applications. Its General Industrial Coatings division has scaled high-durability liquid and powder coatings for beverage packaging and architectural decorative glass. Through the Colormix Foresight program, Sherwin-Williams provides design-to-application support, helping manufacturers reduce production lead times. Its DesignHouse platform delivers data-driven insights on coating longevity and color stability for long-term projects. This integration of design intelligence and technical expertise strengthens its competitive position in decorative and functional glass coatings.

United States Glass Coatings Market: Smart Glazing, Aerospace Coatings, and Solar Efficiency Breakthroughs

The United States glass coatings market is at the forefront of smart glass technologies, aerospace-grade coatings, and energy-efficient glazing systems, driven by stringent federal energy mandates and advanced manufacturing ecosystems. In late 2025, the U.S. Department of Energy updated building energy codes, accelerating the adoption of high-performance green glazing solutions, particularly triple-silver Low-E coatings designed to achieve whole-window U-values of ≤1.4 W/m²K. This regulatory push is significantly increasing demand for low-emissivity (Low-E) glass coatings, thermochromic coatings, and electrochromic smart glass technologies across commercial and residential infrastructure.

In aerospace and defense, Sherwin-Williams and PPG Industries have introduced next-generation polyurethane-based glass coatings offering enhanced UV resistance and anti-static performance for cockpit transparencies. PPG Industries has also completed a $300 million capacity expansion (2024–2025), strengthening supply of glass primers and specialty coatings for semiconductor cleanrooms, a segment boosted by CHIPS Act investments. In the renewable energy sector, anti-reflective (AR) and anti-soiling coatings are delivering measurable gains, with 2025 field data indicating a 3% to 6% improvement in solar PV conversion efficiency. With North America accounting for 33% of global smart coating revenues in 2025, the U.S. continues to lead innovation in self-healing glass coatings, semiconductor-grade coatings, and high-performance architectural glazing.

China Glass Coatings Market: Regulatory Transformation, EV Integration, and Solar Control Leadership

The China glass coatings market is rapidly transitioning toward high-value, environmentally compliant coating technologies, supported by stringent regulations and large-scale industrial demand. Effective June 1, 2026, new national standards (GB 30981.1-2025 and GB 30981.2-2025) will enforce strict limits on harmful substances, accelerating the shift toward water-based and high-solid-content glass coatings. Regulatory oversight from bodies such as the China Classification Society and policy direction from the Ministry of Industry and Information Technology are reinforcing the adoption of low-VOC and sustainable glass coating formulations.

China accounted for approximately 26% of global revenues in the high-strength coated glass segment in 2025, driven by extensive deployment of solar-reflective glass in super-tall commercial buildings. In the automotive sector, Chinese OEMs are integrating infrared-reflective (IRR) coatings that reduce cabin temperatures by up to 10°C, improving EV battery range by nearly 7%, aligning with the country’s dominance in electric vehicle production. Maritime applications are also expanding, with shipyards in Ningbo adopting anti-fouling glass coatings for underwater sensor systems. Additionally, China’s leadership in consumer electronics manufacturing is driving localization of nano-coatings and super-finish lapping films for smartphone displays, reducing dependency on imports and strengthening its role in electronics-grade glass coatings.

Germany Glass Coatings Market: Passive House Standards, Circular Chemistry, and PFAS-Free Innovation

The Germany glass coatings market represents the global benchmark for sustainable glass coating technologies, passive house standards, and circular economy-driven innovation. Under the EU’s Ecodesign for Sustainable Products Regulation (ESPR), glass coatings sold in Germany from 2026 must include a Digital Product Passport (DPP), ensuring transparency in material composition, recyclability, and lifecycle carbon footprint. This requirement is accelerating adoption of eco-friendly glass coatings and recyclable coating chemistries.

Germany’s updated residential standards mandate a 31% improvement in energy performance compared to 2013 levels, driving demand for argon-filled double and triple glazing combined with advanced Low-E coatings. The country is also pioneering hydrogen-resistant glass coatings for inspection windows in hydrogen infrastructure, aligning with its national energy transition strategy. Under REACH regulations, Germany is leading the phase-out of PFAS-based chemistries, prompting R&D into fluoropolymer-free hydrophobic coatings. In automotive applications, premium OEMs such as BMW and Mercedes-Benz have achieved a 58% integration rate of IRR coatings, enhancing thermal comfort and reducing HVAC loads. Advanced AI-driven coating systems are further optimizing application efficiency, reducing material waste by approximately 12% in industrial glass processing.

India Glass Coatings Market: Solar PV Expansion, Infrastructure Boom, and Thermal Management Demand

The India glass coatings market is expanding rapidly, supported by solar energy investments, infrastructure development, and increasing demand for energy-efficient glazing solutions. Government initiatives such as the Production Linked Incentive (PLI) scheme for high-efficiency solar PV modules are catalyzing domestic manufacturing of anti-reflective and self-cleaning glass coatings, critical for improving solar panel performance in high-irradiance conditions.

Infrastructure growth under the Sagarmala Program is driving demand for marine-grade epoxy-glass primers for port terminals and logistics hubs, while metro rail expansions in Mumbai and Delhi are standardizing anti-carbonation coatings for structural glass applications. The commercial real estate boom, particularly in IT parks and Special Economic Zones (SEZs), is increasing adoption of solar control glass coatings and energy-efficient glazing systems. Additionally, the growing automotive aftermarket is fueling demand for solar-reflective window coatings, addressing thermal management challenges in high-temperature urban environments. Regulatory enforcement by the Bureau of Indian Standards through stricter QCOs is ensuring that domestic glass coatings meet global benchmarks for durability, VOC emissions, and performance reliability.

Japan Glass Coatings Market: Nano-Coatings Leadership, Precision Optics, and Smart Manufacturing Excellence

The Japan glass coatings market is globally recognized for its leadership in nano-structured coatings, precision optics, and high-performance electronics applications. Japanese manufacturers are driving innovation in nano-scale lapping films and coatings for semiconductor wafer processing, supported by a 46% year-over-year increase in global demand for advanced semiconductor materials as of 2026.

In transportation, East Japan Railway Company has implemented nano-composite glass coatings for Shinkansen windshields, ensuring resistance to high-velocity debris while maintaining 99.9% optical clarity. Japan’s advanced manufacturing ecosystem emphasizes robotic, sensor-integrated coating systems, enabling real-time monitoring of coating thickness and tool wear in “lights-out” production environments. Building codes focused on disaster resilience are promoting high-elongation epoxy-based glass coatings capable of withstanding seismic stress without structural failure. Companies such as AGC Inc. are leading the shift toward carbon-neutral glass coating production, utilizing renewable energy to meet stringent ESG requirements and reinforcing Japan’s dominance in high-tech, sustainable glass coatings markets.

Glass Coatings Market Report Scope

Glass Coatings market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.4 Billion

|

|

Market Size (2032)

|

$6.4 Billion

|

|

Market Growth Rate

|

9.5%

|

|

Segments

|

By Resin Type (Acrylic, Polyurethane, Epoxy, Silicone, Alkyd, Fluoropolymers, Bio-based Resins), By Technology (Water-borne, Solvent-borne, Nano-based Coatings, Radiation-Cured), By Coating Process (Physical Vapor Deposition, Chemical Vapor Deposition, Liquid Phase Deposition, Magnetron Sputtering), By Function (Low-Emissivity, Solar Control, Anti-Reflective, Hydrophobic, Anti-Fog, Scratch and Abrasion Resistant, Anti-Microbial, Decorative, Conductive), By Glass Type (Flat Glass, Container Glass, Specialty, Electronic Display Glass), By End-Use Industry (Architecture and Construction, Automotive and Transportation, Energy, Consumer Electronics, Appliances and Food Service, Aerospace and Marine, Healthcare and Medical Devices)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Saint-Gobain S.A., AGC Inc., PPG Industries, Inc., Nippon Sheet Glass Co., Ltd., Guardian Industries, The Sherwin-Williams Company, AkzoNobel N.V., Arkema S.A., Vitro, S.A.B. de C.V., SCHOTT AG, Cardinal Glass Industries, Inc., Fuyao Glass Industry Group Co., Ltd., Central Glass Co., Ltd., Sisecam Group, Hempel A/S

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glass Coatings Market Segmentation

By Resin Type

- Acrylic

- Polyurethane

- Epoxy

- Silicone

- Alkyd

- Fluoropolymers

- Bio-based Resins

By Technology

- Water-borne

- Solvent-borne

- Nano-based Coatings

- Radiation-Cured

By Coating Process

- Physical Vapor Deposition

- Chemical Vapor Deposition

- Liquid Phase Deposition

- Magnetron Sputtering

By Function

- Low-Emissivity

- Solar Control

- Anti-Reflective

- Hydrophobic

- Anti-Fog

- Scratch and Abrasion Resistant

- Anti-Microbial

- Decorative

- Conductive

By Glass Type

- Flat Glass

- Container Glass

- Specialty

- Electronic Display Glass

By End-Use Industry

- Architecture and Construction

- Automotive and Transportation

- Energy

- Consumer Electronics

- Appliances and Food Service

- Aerospace and Marine

- Healthcare and Medical Devices

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Glass Coatings Market

- Saint-Gobain S.A.

- AGC Inc.

- PPG Industries, Inc.

- Nippon Sheet Glass Co., Ltd.

- Guardian Industries

- The Sherwin-Williams Company

- AkzoNobel N.V.

- Arkema S.A.

- Vitro, S.A.B. de C.V.

- SCHOTT AG

- Cardinal Glass Industries, Inc.

- Fuyao Glass Industry Group Co., Ltd.

- Central Glass Co., Ltd.

- Sisecam Group

- Hempel A/S

*- List not Exhaustive