Glucaric Acid Market to Reach $2.7 Billion by 2034 at 7.7% CAGR Driven by U.S. Biomanufacturing Expansion and Phosphate-Free Industrial Reformulation

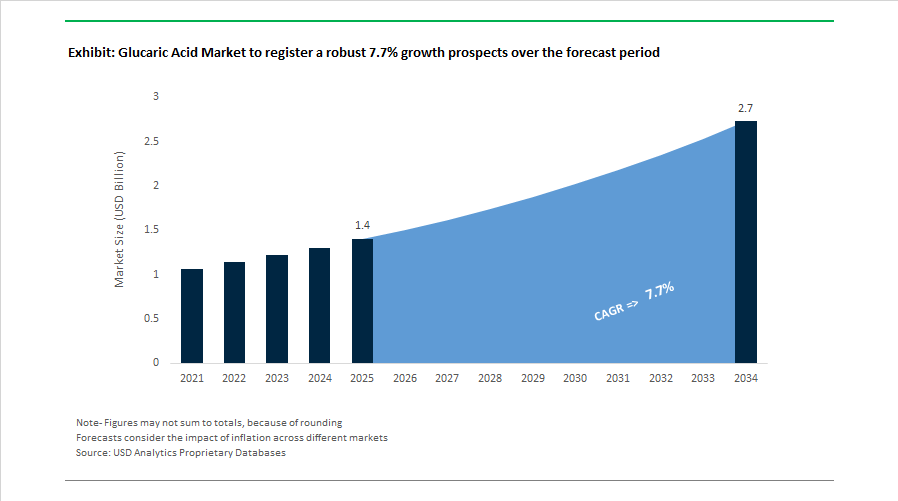

The Glucaric Acid Market is projected to grow from $1.4 billion in 2025 to $2.7 billion by 2034, registering a CAGR of 7.7%. Market expansion is being driven by rapid commercialization of bio-based organic acids, phosphate-free corrosion inhibitors, sustainable industrial detergents, and fermentation-derived specialty chemicals. Increasing regulatory pressure on phosphate discharge, infrastructure corrosion control mandates, and decarbonization of chemical manufacturing are positioning glucaric acid and its derivatives as strategic bio-based alternatives across water treatment, de-icing, cleaning formulations, and polymer synthesis.

In January 2024, Novonesis was formed through the merger of Chr. Hansen and Novozymes, consolidating enzyme and microbial strain capabilities critical for fermentation-based oxidized sugar production. In June 2024, Solugen Inc. secured a $213.6 million conditional loan guarantee from the U.S. Department of Energy to construct its Bioforge Marshall facility in Minnesota. The plant, co-located adjacent to Archer Daniels Midland’s corn processing complex, will source dextrose via pipeline to manufacture glucaric acid through enzymatic pathways, creating a vertically integrated bio-industrial loop. This model enhances feedstock efficiency and reduces carbon intensity compared to petrochemical oxidation routes.

Regulatory validation and industrial-scale production milestones accelerated adoption in 2024. The U.S. Food and Drug Administration granted GRAS status to Preventium®, a calcium D-glucarate product developed by Applied Food Sciences, enabling broader integration of glucarate derivatives into functional beverages and food applications targeting detoxification and cellular health. Kalion Inc. reported achieving full commercial-scale production of high-purity glucaric acid in 2024, supplying KSPG40, a glucarate-based corrosion inhibitor designed to replace phosphate-based water treatment chemistries. The Montana Department of Transportation validated glucaric acid formulations as reducing steel corrosion by 70%, accelerating adoption in de-icing and infrastructure protection programs.

Market diversification intensified through 2025. Industrial detergent suppliers aligned with Rivertop Renewables transitioned toward glucaric acid-based surfactants engineered for automotive Mega-Casting processes that require phosphate-free cleaning systems. In mid-2025, bio-chemical consortia initiated pilot projects utilizing glucarate-derived monomers in recyclable polyesters and bio-based nylons, targeting improved tensile strength and thermal performance in biodegradable plastics. Digital traceability pilots launched in 2025 by Solugen and Kalion incorporated blockchain analytics, enabling detergent and personal care manufacturers to verify renewable carbon content and lifecycle emissions data. Late 2025 tariff adjustments on specialty chemical imports from Asia triggered a shift toward domestic sourcing, increasing utilization rates at U.S. corn-based biorefineries.

Application expansion into health and biotechnology sectors gained momentum in 2025–2026. Research disseminated in late 2025 identified glucaric acid derivatives as selective prebiotic substrates that support butyrate-producing gut microbiota. In early 2026, pharmaceutical companies began filing applications for glucarate-based supplements targeting metabolic and gut health, expanding glucaric acid beyond industrial applications into nutraceutical and precision health markets.

The Glucaric Acid Market outlook reflects accelerated investment in enzymatic biomanufacturing, phosphate-free reformulation mandates, infrastructure corrosion mitigation, renewable polymer development, and precision nutrition innovation. Competitive positioning increasingly depends on feedstock integration, enzyme optimization, regulatory approvals, domestic production capacity, and verified carbon-reduction metrics across detergent, water treatment, polymer, and nutraceutical value chains.

Glucaric Acid Market Trends and High-Impact Growth Opportunities

Bio-Based Scale-Up Positions Glucaric Acid as a Core Water Treatment Chemical

The glucaric acid market is transitioning from pilot-scale bio-based chemistry into full industrial deployment, driven primarily by tightening environmental regulations in industrial water treatment. Phosphate-based corrosion inhibitors are increasingly restricted under the EU Water Framework Directive and U.S. EPA effluent guidelines, forcing utilities and industrial operators to adopt phosphorus-free alternatives. Glucaric acid is emerging as a structurally attractive solution due to its strong chelation performance, biodegradability, and zero phosphorus discharge profile.

A critical inflection point occurred in June 2024 when the U.S. Department of Energy backed a 500,000 square foot Bioforge facility in Marshall, Minnesota through a $213 million loan guarantee. This facility, developed by Solugen in partnership with ADM, is designed to produce up to 120 kilotonnes per year of organic acids, including glucaric acid, using carbon-negative processes. This scale fundamentally changes glucaric acid economics, moving it from a specialty bio-chemical to a competitively priced industrial input.

Performance data from 2025 confirms that glucaric-acid-based corrosion inhibitors can fully replace phosphonates in cooling tower systems while eliminating phosphorus discharge entirely. This is particularly significant in power generation, where cooling systems account for nearly half of U.S. freshwater withdrawals. Commercial momentum is accelerating through strategic partnerships. In June 2024, Kurita America entered a collaboration with Solugen to commercialize carbon-negative, phosphorus-neutral water treatment solutions. Together, these developments signal that glucaric acid is becoming a cornerstone molecule in next-generation industrial water chemistry.

Emergence of Ultra-High Purity Grades for Pharma and Cosmeceutical Use

Beyond bulk industrial applications, the glucaric acid market is bifurcating into technical-grade and ultra-high-purity segments, driven by advances in enzymatic bioproduction. Pharmaceutical and cosmeceutical manufacturers are increasingly demanding USP and Ph. Eur. compliant glucaric acid for regulated applications, prompting innovation in bio-catalysis and downstream purification. In May 2024, research conducted at Jiangnan University demonstrated a 17-fold increase in glucaric acid yield using engineered E. coli strains combined with SUMO-fusion enzyme stabilization. Achieving concentrations above 5.5 g/L significantly lowers production costs for pharmaceutical-grade intermediates.

This progress is expanding glucaric acid’s therapeutic relevance. D-glucaric acid-1,4-lactone is increasingly studied for its ability to inhibit beta-glucuronidase, an enzyme linked to hormone reactivation pathways in certain cancers. In parallel, pure saccharic acid is gaining traction in premium skincare formulations as a tyrosinase inhibitor, supporting skin-brightening and tone-evening claims. These applications are repositioning glucaric acid from an industrial chelant into a multifunctional bioactive ingredient, unlocking higher-margin markets with stringent quality requirements.

Sustainable Deicing and Anti-Icing Solutions for Aviation and Infrastructure

One of the most compelling growth opportunities for glucaric acid lies in sustainable deicing and anti-icing fluids. Aviation authorities and transport agencies are actively seeking alternatives to acetate- and glycol-based deicers due to corrosion damage and aquatic toxicity. Salts of glucaric acid, particularly sodium and potassium glucarate, are emerging as best-in-class solutions due to their non-corrosive behavior and rapid biodegradation.

Glucaric-acid-based formulations have been pre-qualified under the SAE AMS 1435E standard updated in March 2024, confirming their suitability for runway and aircraft deicing applications. Unlike traditional salts, glucarates demonstrate strong ice-melting efficiency without corroding aluminum airframes or concrete infrastructure. In cold-climate regions such as Canada and the Nordic countries, public procurement policies are increasingly favoring glucaric acid deicers to extend infrastructure lifespan and prevent oxygen depletion in nearby waterways caused by glycol runoff. This positions glucaric acid as a premium, regulation-aligned alternative in a traditionally cost-driven market.

Phosphate-Free Detergent Builders and Hard-Water Chelation Systems

The expansion of phosphate bans in household and industrial cleaning products is creating a large addressable opportunity for glucaric acid as a next-generation detergent builder. In the global detergent market, valued at over 100 billion dollars, formulators are seeking biodegradable chelants that perform under hard-water conditions without contributing to eutrophication. Glucaric acid exhibits strong sequestration capacity for calcium and magnesium ions, outperforming citrate-based systems in preventing scale formation, spotting, and filming.

By 2025, several multinational consumer goods companies were evaluating glucarate-enhanced automatic dishwashing detergents as a pathway to maintain cleaning efficacy in low-phosphate formulations. Trade dynamics further strengthen this opportunity. New U.S. tariffs and trade barriers introduced in early 2025 on imported bio-based chemicals are incentivizing domestic sourcing. This creates a strategic opening for North American producers such as Kalion and Solugen to capture share in the clean-label cleaning segment with locally produced, cost-competitive glucaric acid derivatives.

Glucaric Acid Market Share and Segmentation Insights

Calcium D-Glucarate Leads the Glucaric Acid Market Through Strong Nutraceutical Adoption

Calcium D-Glucarate accounted for 38.60% of the Glucaric Acid Market share in 2025, establishing it as the most commercially significant product type within the glucaric acid derivatives industry. Calcium D-glucarate is widely recognized for its use in dietary supplements and nutraceutical formulations, where it is promoted for its potential role in detoxification support, hormone balance, and metabolic health management. The compound functions by influencing beta-glucuronidase enzyme activity, which is associated with the body’s detoxification pathways and elimination of certain metabolic byproducts. Because of this biological relevance, calcium D-glucarate has gained traction in preventive wellness formulations targeting liver health, hormonal balance, and antioxidant protection. In 2025, the segment is experiencing expansion through growing clinical research and validation of glucaric acid derivatives. Supplement manufacturers are investing in standardized calcium D-glucarate formulations supported by clinical studies, allowing them to provide more substantiated health positioning. This shift is gradually moving calcium D-glucarate from niche detox supplement categories into mainstream preventive healthcare and functional nutrition markets.

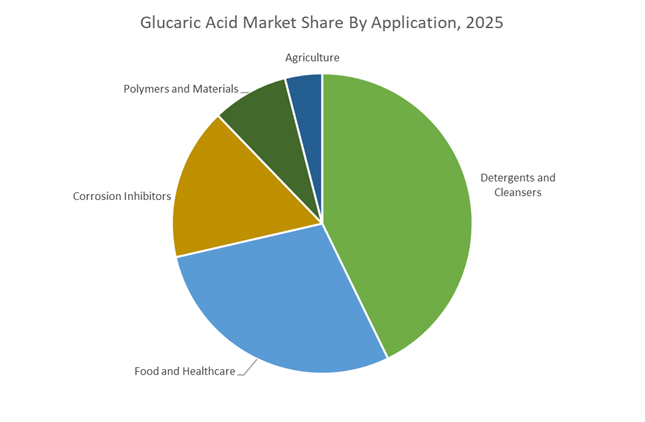

Detergents and Cleansers Drive the Largest Demand for Glucaric Acid Derivatives

Detergents and Cleansers represented 42.80% of the Glucaric Acid Market share in 2025, making it the largest application segment for glucaric acid-based chemicals. In detergent formulations, glucaric acid derivatives such as sodium glucarate act as biodegradable chelating agents and detergent builders, helping improve cleaning performance by binding mineral ions that interfere with surfactant activity. These compounds have gained significant attention as environmentally friendly alternatives to phosphate-based detergent builders, which have historically contributed to water pollution and eutrophication in aquatic ecosystems. As environmental regulations increasingly restrict phosphate use in household cleaning products, detergent manufacturers are reformulating products using bio-based glucarate builder systems that provide comparable cleaning performance without environmental drawbacks. In 2025, expanding phosphate bans across North America, Europe, and parts of Asia have accelerated adoption of glucaric acid derivatives in laundry detergents and automatic dishwasher formulations. Major consumer brands are integrating these ingredients into mainstream cleaning products, significantly increasing production volumes and strengthening glucaric acid’s role in sustainable detergent chemistry.

Competitive Landscape in Glucaric Acid Market

ADM Accelerates Commercial Scale Bio-Based Sodium Glucarate Production

Archer Daniels Midland Company is leveraging its global glucose processing infrastructure to establish large-scale commercial production of bio-based glucaric acid and sodium glucarate. Through partnerships with Johnson Matthey and technology licensed from Rennovia, ADM is advancing catalytic oxidation pathways designed for industrial scalability in 2026. Its product focus centers on high-purity sodium glucarate as a phosphate-free alternative in automatic dishwasher detergents, addressing tightening environmental regulations on eutrophication. Vertical integration across fermentation and catalytic conversion assets provides feedstock security and pricing stability against glucose volatility. ADM has positioned glucaric acid within its Sustainable Solutions portfolio, targeting growth in the expanding bio-based chemical market projected to exceed $1.6 billion by 2030.

Kalion Sets Benchmark in Fermentation-Derived High-Purity Glucaric Acid

Kalion, Inc. remains a technology-driven innovator in microbial fermentation-based D-glucaric acid production. During 2025 and 2026, the company scaled its machine-learning-optimized fermentation platform, achieving superior purity levels and reduced waste compared to traditional nitric acid oxidation methods. Recognition through the EPA Green Chemistry Challenge Award reinforces its positioning as a low-carbon, low-waste producer. Kalion is targeting advanced applications in high-performance polymers, water treatment formulations, and specialty coatings, where glucaric acid derivatives enhance tensile strength and chelation efficiency. Continued National Science Foundation and Department of Energy support through 2025 supports research into metabolic pathway optimization to increase yield and production economics.

Rivertop Renewables Expands Biodegradable Glucarate Solutions for Industrial Markets

Rivertop Renewables commercializes sugar-derived acids through its proprietary oxidation platform, marketing the Riose® line of glucarates for corrosion inhibition and industrial cleaning applications. The company is collaborating with global formulators in 2026 to replace non-biodegradable synthetic polymers in concrete admixtures and textile processing chemicals. Its scalability-focused production model aims to reduce capital intensity while addressing a broader market potential estimated in the tens of billions across specialty chemicals. Rivertop’s glucarate salts are increasingly utilized in hard-water environments due to strong chelation performance and improved dispersion stability. Strategic research collaborations continue to address complex mineral binding challenges in municipal and industrial water systems.

Jungbunzlauer Strengthens European Leadership in Calcium D-Glucarate

Jungbunzlauer Suisse AG positions itself as a premium supplier of fermentation-derived glucaric acid derivatives in Europe. The company is a major producer of high-purity calcium D-glucarate used in dietary supplements targeting liver detoxification and estrogen metabolism support. In early 2026, Jungbunzlauer reinforced alignment with the EU Green Deal by maintaining strict environmental compliance across its bio-acid production processes. Its Basel-based research and development capabilities focus on optimizing glucarate performance in de-icing agents and biodegradable detergent builders. The company maintains a strong presence in clean-label specialty ingredients, supplying non-toxic, bio-based alternatives for food, healthcare, and detergent markets.

Merck KGaA Supplies Pharmaceutical-Grade Glucaric Acid Derivatives

Merck KGaA, through its Life Science division, provides high-purity glucaric acid derivatives for pharmaceutical manufacturing and analytical research. Its portfolio includes D-glucaric acid-1,4-lactone and potassium sodium D-glucarate, widely used in precision medicine research and cancer prevention studies. In 2026, Merck emphasized digital integration of its chemical supply chain to ensure real-time traceability, quality documentation, and regulatory compliance for highly controlled healthcare applications. The company’s global distribution network supports availability across Asia-Pacific and North America, where demand for pharmaceutical-grade bio-based intermediates is expanding. By focusing on analytical-grade consistency and regulatory adherence, Merck maintains strong positioning in the life sciences segment of the glucaric acid market.

United States Glucaric Acid Market: $213.6M DOE-Backed Bioforge Facility and 95% Yield Biomanufacturing Breakthrough

The United States Glucaric Acid Market remains the global innovation hub for bio-based platform chemicals, driven by advanced biomanufacturing infrastructure, federal funding, and strong commercialization pathways. In mid-2024, the U.S. Department of Energy Loan Programs Office issued a $213.6M conditional loan guarantee to Solugen to finance the Bioforge Marshall facility in Minnesota. This plant, breaking ground in 2024 and scaling production through 2026, represents a cornerstone investment for domestic glucaric acid manufacturing. The facility integrates enzymatic and catalytic chemistry through Solugen’s carbon-negative process, achieving integrated yields exceeding 95%, significantly lowering the cost of renewable organic acid production.

Commercial deployment is accelerating across multiple sectors. Applied Food Sciences secured FDA GRAS status in late 2024 for Preventium (Calcium D-Glucarate), enabling immediate use in functional beverages and nutrition bars. Meanwhile, Archer Daniels Midland is advancing commercial-scale glucaric acid production through licensing agreements with Johnson Matthey and Rennovia, targeting high-demand applications such as eco-friendly de-icing agents and anti-corrosion additives. Research partnerships between Kalion Inc and the Agile BioFoundry are using machine learning to optimize microbial fermentation pathways capable of producing 99% high-purity glucaric acid at costs below traditional nitric acid oxidation processes. Additionally, research from North Carolina State University shows glucaric acid additives can increase the tensile strength of polyvinyl alcohol fibers by 3x, unlocking emerging applications in biodegradable textiles and absorbent hygiene products.

China Glucaric Acid Market: Green Chemical Subsidies, 15% Export Growth, and Zero-Waste Industrial Policy

China’s Glucaric Acid Market is expanding rapidly due to government mandates promoting bio-based platform chemicals and strong domestic glucose feedstock availability. Under the national 14th Five-Year Plan, authorities are prioritizing the replacement of petroleum-derived intermediates with renewable chemicals such as saccharic acid, providing financial incentives for producers investing in industrial-scale fermentation technologies.

Industrial producers including Shanghai Meicheng Chemical are expanding production of D-Glucaric Acid-1,4-Lactone to meet growing demand from the domestic pharmaceutical and oncology sectors. China’s Zero-Waste City initiatives introduced in 2025 require municipalities to adopt biodegradable chelating agents in water treatment systems, increasing demand for glucaric acid as a sustainable alternative to EDTA. Export momentum is also accelerating, with Chinese customs data indicating a 15% year-on-year increase in Calcium D-Glucarate shipments to European nutraceutical manufacturers during 2024. Meanwhile, the Ministry of Agriculture and Rural Affairs of China is promoting glucaric acid-based feed additives to enhance detoxification pathways in livestock as part of the Healthy China 2030 initiative. The introduction of Green Product certification programs in 2025 further incentivizes detergent producers to replace phosphate builders with glucaric acid-based alternatives.

Germany Glucaric Acid Market: Circular Chemistry Strategy and Phosphate-Free Industrial Applications

Germany leads Europe’s transition toward circular bio-based chemistry, positioning glucaric acid as a sustainable replacement for traditional industrial chemicals. Tightening EU REACH restrictions on toxic corrosion inhibitors have encouraged companies such as BASF and LANXESS to explore glucaric acid as a biodegradable corrosion inhibitor for cooling water systems and industrial cleaning formulations.

Germany’s National Circular Economy Strategy launched in 2024 emphasizes carbon cycle technologies and bio-refinery integration. This policy framework has accelerated research into glucaric acid as a precursor for bio-based adipic acid used in sustainable Nylon-6,6 production. Consumer product leaders including Henkel are reformulating premium detergent products to include glucaric acid due to its superior chelation capacity and 100% biodegradability. The Federal Ministry of Education and Research is funding projects between 2025 and 2026 to develop advanced biorefinery systems converting lignocellulosic biomass into high-purity glucaric acid. Additionally, pilot studies across German infrastructure projects demonstrate that glucaric acid additives can extend concrete durability while reducing construction-sector carbon emissions by ~12%, strengthening its role in sustainable building materials.

India Glucaric Acid Market: ₹13,000 Crore BioPharma SHAKTI Program and Fermentation-Based Chemical Expansion

India is rapidly emerging as a key growth market in the Glucaric Acid Industry due to strong pharmaceutical manufacturing capabilities and government support for bio-based chemical production. In 2025, the Ministry of Chemicals and Fertilizers launched the BioPharma SHAKTI initiative with an investment of ₹13,000 crore to develop specialized chemical parks supporting fermentation-based production of organic acids including glucaric acid.

Demand from the domestic nutraceutical sector is rising as Indian generic pharmaceutical companies increasingly incorporate Calcium D-Glucarate in liver-support and detox supplements. The launch of the Indian Carbon Credit Trading Scheme (CCTS) in 2026 is also encouraging chemical producers to adopt bio-based glucaric acid processes to reduce industrial carbon footprints. Environmental regulation is another growth catalyst, with recommendations from the National Green Tribunal prompting detergent manufacturers to replace phosphate builders with biodegradable glucaric acid chelants. Industrial demand is expanding as India’s thermal power and cooling sectors report a ~20% increase in demand for eco-friendly corrosion inhibitors during 2025. Supporting long-term innovation, the Department of Biotechnology partnered with startups in 2024 to develop cost-efficient yeast-based fermentation pathways optimized for Indian feedstocks and climate conditions, positioning India as a future global supplier of sustainable glucaric acid derivatives.

Glucaric Acid Market Report Scope

Glucaric Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2034)

|

$2.7 Billion

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By Product Type (Glucaric Acid, Calcium D-Glucarate, D-Glucaric Acid Lactone, Sodium and Potassium Glucarates, Glucarate Esters), By Production Method (Chemical Catalysis, Biotechnological and Fermentation Processes, Electrochemical Oxidation), By Application (Detergents and Cleansers, Food and Healthcare, Corrosion Inhibitors, Polymers and Materials, Agriculture)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kalion, Inc., Applied Food Sciences, Inc., Solvay S.A., Archer Daniels Midland Company, Jungbunzlauer Suisse AG, CarboSynth Ltd., Cayman Chemical, Hunan Province Huateng Pharmaceutical Co., Ltd., Merck KGaA, Zhejiang Chem-Tech Group Co., Ltd., Rivertop Renewables, Givaudan, Bio-Technical Resources, Glucan Bio, SVA Organics

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glucaric Acid Market Segmentation

By Product Type

- Glucaric Acid

- Calcium D-Glucarate

- D-Glucaric Acid Lactone

- Sodium and Potassium Glucarates

- Glucarate Esters

By Production Method

- Chemical Catalysis

- Biotechnological and Fermentation Processes

- Electrochemical Oxidation

By Application

- Detergents and Cleansers

- Food and Healthcare

- Corrosion Inhibitors

- Polymers and Materials

- Agriculture

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Glucaric Acid Industry

- Kalion, Inc.

- Applied Food Sciences, Inc.

- Solvay S.A.

- Archer Daniels Midland Company

- Jungbunzlauer Suisse AG

- CarboSynth Ltd.

- Cayman Chemical

- Hunan Province Huateng Pharmaceutical Co., Ltd.

- Merck KGaA

- Zhejiang Chem-Tech Group Co., Ltd.

- Rivertop Renewables

- Givaudan

- Bio-Technical Resources

- Glucan Bio

- SVA Organics

*- List not Exhaustive