Graphene-Enhanced Batteries and Supercapacitors Market Overview

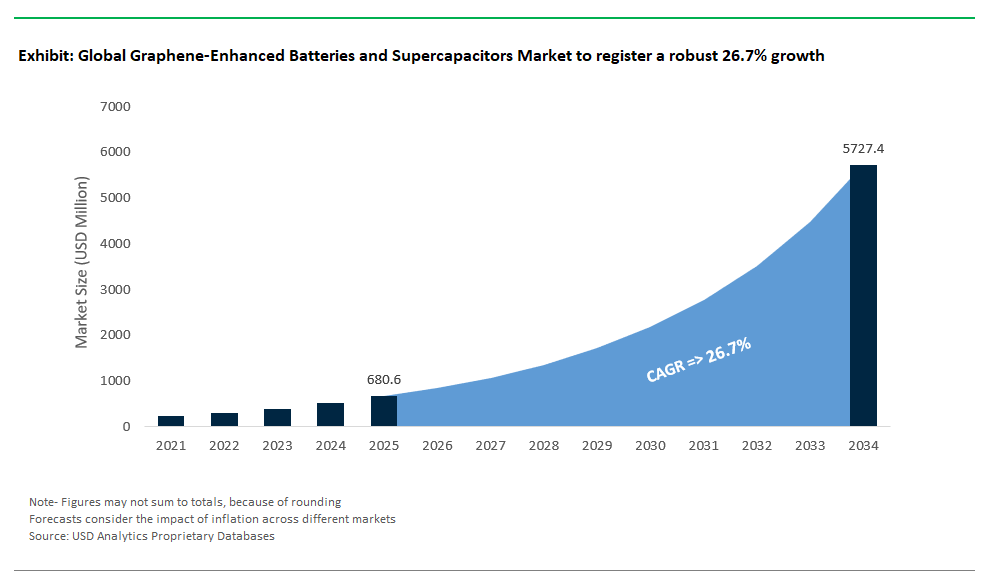

The graphene-enhanced batteries and supercapacitors market is set for substantial growth between 2025 and 2034, driven by the global race for advanced energy storage solutions across electric vehicles (EVs), grid storage, consumer electronics, and emerging beyond-lithium technologies. Industry analysts forecast this specialized market segment to achieve a robust CAGR of 26.7% over the period, potentially reaching a valuation of USD 680.6 million in 2025 to USD 5726.4 million by 2034, as manufacturers and end-users seek performance gains that conventional materials simply cannot deliver.

Leveraging exclusive data compiled by USDAnalytics, this current edition of the Graphene-Enhanced Batteries and Supercapacitors report provides an in-depth overview and forward-looking assessment of the graphene market across 21 nations and 18 leading companies- By Graphene-Enhanced Batteries (Lithium-ion batteries, Lithium-sulfur batteries, Solid-state batteries), By Graphene-Enhanced Supercapacitors (Electrochemical double-layer capacitors (EDLCs), Pseudocapacitors, Hybrid supercapacitors), By Application (Consumer Electronics, Automotive, Industrial & Energy Storage, Aerospace & Defense, Medical Devices), By Graphene Type (Graphene Oxide (GO), Reduced Graphene Oxide (rGO), Graphene Nanoplatelets (GNPs), Others).

This report delivers an in-depth analysis of the graphene-enhanced batteries and supercapacitors market, profiling key players, market shares, technology trends, and competitive strategies shaping this transformative segment. Stakeholders from EV battery manufacturers to grid-scale energy storage developers will gain critical insights into how graphene is poised to redefine performance benchmarks and competitive advantage across the global energy landscape through 2034.

Graphene Revolutionizes Energy Storage with High-Performance Batteries and Supercapacitors

Graphene’s superior electrochemical and thermal properties are transforming lithium-ion batteries (LIBs) by boosting capacity, charge speed, and safety. Graphene-modified LIB anodes can achieve up to three times the theoretical capacity of graphite. As a cathode coating, graphene enhances energy density and long-term stability, especially for LiFePO₄ cells. Its high conductivity and fast ion diffusion enable rapid charging—some graphene-LIBs can fully charge in just six minutes. In supercapacitors, graphene pushes energy densities up to 136 Wh/kg, far above traditional supercaps. These supercapacitors also maintain ultra-high power output and rapid frequency response. Applications range from electric vehicles and fast-charging stations to regenerative braking and AC filtering. Graphene is advancing sodium-ion and aluminum-ion batteries as well, offering more sustainable and cost-effective solutions. These breakthroughs address raw material supply concerns and global energy demands. Overall, graphene is enabling the next generation of high-performance, fast-charging, and reliable energy storage technologies.

Graphene-Enhanced Batteries and Supercapacitors Market Analysis (2024-2025)

The global market for graphene-enhanced batteries and supercapacitors has entered a dynamic growth phase, driven by significant breakthroughs in performance and ongoing commercial-scale initiatives. Between 2024 and 2025, the industry witnessed robust momentum across multiple energy storage technologies from lithium-ion and lithium-sulfur batteries to solid-state designs and supercapacitors confirming graphene’s role as a transformative material in the energy sector.

Graphene Innovations in Lithium-Ion Batteries (LIBs)

In lithium-ion batteries, several notable developments have showcased how graphene is redefining electrode materials and performance benchmarks. Talga Group has continued to advance its graphene-enhanced silicon anode material, Talnode®-Si, with recent developments highlighting its potential to deliver significant increases in energy density compared to traditional graphite anodes. This innovation targets the rapidly growing electric vehicle (EV) market, where extending driving range without sacrificing battery lifespan is critical for adoption. In the United States, NanoGraf partnered with the Department of Defense in 2023 to advance graphene-silicon anode batteries that deliver approximately 20% longer runtime. Such progress demonstrates how graphene can significantly boost the energy and power density of lithium-ion systems while addressing challenges like silicon’s volumetric expansion during charge cycles.

Advancements in Graphene-Enabled Lithium-Sulfur (Li-S) Batteries

The lithium-sulfur (Li-S) battery segment has also emerged as a promising frontier for graphene’s application. Lyten, a US-based innovator, made significant strides during 2024 and 2025 by scaling up its graphene-enabled Li-S batteries, which boast energy densities up to three times greater than those of conventional lithium-ion cells. These advancements are underpinned by strategic partnerships, including collaborations with major players like Stellantis and engagements with the US Army, signaling growing confidence in graphene’s commercial viability for high-energy-density EV applications. Meanwhile, in Europe, the Graphene Flagship program has achieved meaningful progress by demonstrating graphene-sulfur cathodes capable of reducing polysulfide shuttling a notorious problem that limits the cycle life of traditional Li-S batteries. This innovation represents a crucial step toward making Li-S technology commercially competitive and durable for large-scale deployments.

Graphene's Role in Solid-State Battery Development

Solid-state batteries attracting intense industry interest for their potential to enhance safety and energy density are also incorporating graphene to solve fundamental challenges. Solidion Technology in the USA is leveraging graphene in its solid-state designs to improve various aspects of performance, including ionic conductivity and overall cell stability. Such applications underscore graphene’s value not merely as an additive but as an enabler of entirely new battery architectures with superior safety profiles and energy storage capabilities.

Momentum in Graphene-Based Supercapacitors

The market for graphene-based supercapacitors has likewise gathered considerable momentum. Skeleton Technologies, operating across Estonia and Germany, deployed its “Curved Graphene” supercapacitors in 2023, reporting a 300% increase in power density compared to conventional devices. These supercapacitors target industrial sectors requiring rapid charge-discharge cycles and high power bursts, such as grid stabilization and heavy transportation systems. In the fast-growing micro-mobility market, Companies like ZapGo Ltd demonstrated graphene-enhanced supercapacitors capable of rapidly recharging e-bike batteries in as little as five minutes, representing a potential game-changer for urban mobility and last-mile logistics. Complementing these commercial efforts, researchers at the University of California, San Diego, achieved significant progress in 2024 by creating ultra-thin graphene supercapacitors suitable for flexible electronics, positioning graphene as a key material for wearable technology and bendable consumer devices.

Research & Development (R&D) and Government Initiatives in Graphene Energy Storage

Research initiatives and government support continue to play a pivotal role in accelerating graphene’s integration into advanced energy storage systems. In 2023, the US Department of Energy committed significant funding toward projects investigating graphene applications in battery anodes, as well as its role in thermal management, reflecting strong federal interest in graphene’s potential to enhance energy security and sustainability. In China, CATL, one of the world’s leading battery manufacturers, filed new patents in 2024 for graphene-coated battery electrodes designed to improve fast-charging capabilities a critical factor in the widespread adoption of electric vehicles and mobile devices. Additionally, groundbreaking academic research from the University of Manchester in 2023 revealed graphene oxide membranes capable of stabilizing lithium-metal anodes, a development that could enable safer and longer-lasting batteries with significantly higher energy densities.

Graphene-Enhanced Batteries and Supercapacitors Competitive Landscape

The graphene-enhanced batteries and supercapacitors market is rapidly reshaping the global energy storage landscape, as industries seek to boost power density, safety, and charging speed in applications ranging from electric vehicles (EVs) to consumer electronics and grid storage. Graphene’s superior electrical conductivity, thermal stability, and high surface area make it an ideal material for improving battery anodes, cathodes, and supercapacitor electrodes. As the electrification trend accelerates across transportation and renewable energy sectors, the competitive landscape is intensifying, with manufacturers worldwide racing to commercialize high-performance, graphene-enabled energy storage solutions.

North American Leaders in Graphene Energy Storage

North America is home to several innovators advancing graphene-based energy storage solutions. Companies like NanoXplore Inc., Nanotech Energy, and Ionic Materials are pushing the boundaries in battery technologies, targeting applications from EVs to grid storage and wearables. Each is carving out a unique niche through materials innovation, manufacturing scale-up, and strategic partnerships.

-

NanoXplore Inc. is a North American leader producing GrapheneBlack® for lithium-ion battery anodes and supercapacitor electrodes, with a production capacity of 4,000 metric tons per year in Montreal and plans to expand to 20,000 tons by 2027 to serve EVs, energy storage, and electric transportation markets.

-

Nanotech Energy in the U.S. is developing graphene-Organolyte™ batteries that emphasize non-flammable, safe lithium-ion solutions for grid storage and EVs, supported by its Chico 2 manufacturing plant and partnerships like ST Advanced Precision Co., Ltd.

-

Ionic Materials focuses on advanced battery technologies, including solid-state concepts that may leverage graphene’s properties to enhance performance and safety for applications in EVs, aerospace, and wearables.

European & Australian Innovators in Graphene Battery & Supercapacitor Technology

European and Australian innovators are making notable progress in advancing graphene-based battery and supercapacitor technologies. Companies like Skeleton Technologies, Graphene Manufacturing Group, and Talga Group are driving breakthroughs ranging from ultra-fast charging to sustainable anode materials. Their efforts are shaping the future of energy storage for electric vehicles, industrial applications, and beyond.

-

Skeleton Technologies, based in Estonia and Germany, leads in graphene-enhanced supercapacitors using proprietary curved graphene architectures for rapid charging and long cycle life, with their SuperBattery™ hybrid systems winning contracts in transport sectors and expansion underway in Germany.

-

Graphene Manufacturing Group (GMG) in Australia is developing graphene aluminum-ion batteries showing promising ultra-fast charging potential, minimal heat generation, and progress toward pouch cells, while partnering with Rio Tinto to explore mining and minerals applications.

-

Talga Group, operating in Australia and Sweden, is commercializing vertically integrated graphitic anode materials like Talnode® silicon-graphene anodes for high-capacity EV batteries, focusing on sustainable, ethically sourced graphite from its Swedish mine and securing significant European supply deals and manufacturing growth.

Asia's Dominance in Graphene Battery Commercialization (China, South Korea, Japan)

Asia remains at the forefront of commercializing graphene-based energy storage technologies, with Chinese, South Korean, and Japanese companies driving advances in high-performance batteries, thermal management, and large-scale materials production. These innovators are shaping the future of electric vehicles, electronics, and broader energy applications. Meanwhile, players outside Asia, like ZapGo, are also contributing breakthroughs in fast-charging technologies.

-

CATL (China), one of the world’s largest battery producers, is innovating in advanced materials and thermal management for EV batteries, unveiling lithium-metal prototypes reaching 500 Wh/kg and leading fast-charging LFP technology that may integrate graphene for performance gains.

-

BTR New Material Group (China), a major global supplier of anode materials, has reached a production capacity of 575,000 tonnes per year as of March 2025 and includes graphene-coated anodes among its advanced offerings, with expansion plans in Indonesia and Morocco.

-

Huawei (China) is leveraging graphene for advanced thermal management in both 5G infrastructure and consumer electronics, continuously filing patents to maintain its technological edge in high-performance devices and networks.

Key Market Trends & Opportunities in Graphene Energy Storage

Trend: Integration of Graphene Hybrid Architectures in Next-Generation Batteries

The Graphene-Enhanced Batteries and Supercapacitors Industry is rapidly evolving as manufacturers and researchers move beyond basic graphene doping toward the engineering of sophisticated hybrid architectures that combine graphene with other advanced materials such as silicon, sulfur, and MXenes. This trend is unlocking a new era of high-performance, durable, and energy-dense storage solutions across electric vehicles, aerospace, and grid applications. Notably, silicon-graphene anodes represent a transformational leap from conventional graphite, with the capacity to achieve up to 4,200 mAh/g—more than ten times that of graphite—while simultaneously addressing silicon’s notorious expansion and degradation issues. Companies such as Sila Nanotechnologies and NanoGraf are at the forefront, scaling these advanced anodes for electric vehicle batteries, with ambitious targets to push energy densities significantly beyond current benchmarks a milestone that could extend EV driving ranges and accelerate adoption. In parallel, graphene oxide membranes are enabling the commercial viability of lithium-sulfur (Li-S) batteries by acting as highly selective ion sieves. This innovation effectively suppresses polysulfide shuttling, paving the way for theoretical energy densities of 2,600 Wh/kg—five times higher than traditional lithium-ion batteries. Industry leaders like Lyten are piloting these graphene-enhanced Li-S batteries for the demanding aerospace sector, where weight and energy density are critical. Solid-state batteries are also benefitting from graphene’s unique capabilities: by incorporating graphene scaffolds, manufacturers are enhancing ionic conductivity within solid electrolytes, significantly reducing the risk of dendrite formation. Toyota’s R&D has reported prototype cells achieving significantly enhanced ion transfer speeds, marking a substantial advancement in both safety and performance. These hybrid battery architectures not only promise to redefine energy density and cycle life benchmarks but also set the stage for the next generation of safe, high-efficiency energy storage systems across automotive, aerospace, and renewable energy sectors.

Opportunity: Decentralized Manufacturing of Graphene-Based Supercapacitors for Renewable Microgrids

An exciting opportunity is emerging in the Graphene-Enhanced Supercapacitors Market, where the unique properties of graphene are enabling the deployment of modular, decentralized energy storage solutions tailored for off-grid and microgrid systems—particularly in remote or underserved regions. Unlike conventional batteries, graphene supercapacitors deliver instantaneous energy buffering, smoothing the variable output from solar and wind resources with sub-second response times that are critical for the stability of rural mini-grids. Their virtually unlimited cycle life, exceeding 100,000 charge-discharge cycles compared to the typical 5,000 cycles for lithium-ion batteries, drastically reduces long-term maintenance and replacement costs—making them a highly attractive solution for low-infrastructure environments. Equally transformative is the rise of scalable, localized fabrication methods. Emerging techniques such as laser-induced graphene (LIG) enable the on-site production of supercapacitors using locally sourced carbon feedstocks like agricultural biomass, effectively bypassing complex global supply chains and reducing logistical challenges. This approach not only empowers communities to develop custom-fit energy solutions but also aligns with broader sustainability goals by supporting renewable, circular manufacturing practices. As renewable microgrids and distributed generation continue to expand, the integration of graphene-based supercapacitors will be central to ensuring resilient, cost-effective, and scalable energy access for emerging markets and remote locations, driving robust growth and new business models across the global Graphene-Enhanced Energy Storage Industry.

Market Share and Segmentation Analysis: Graphene-Enhanced Batteries and Supercapacitors Market

Lithium-Ion Batteries Anchor Market, Solid-State Emerges as a Game Changer

In 2025, graphene-enhanced lithium-ion batteries stand as the clear market leader, representing 69% of the total segment. This position reflects their established role in electric vehicles and consumer electronics, where graphene enables greater energy density and faster charging. While lithium-sulfur and solid-state batteries each hold a smaller share, solid-state batteries are forecast to exhibit the fastest growth, driven by innovations in safety and performance.

Supercapacitors: EDLCs Dominate, Hybrid Designs Gain Momentum

Among supercapacitors, electrochemical double-layer capacitors (EDLCs) lead with 55% market share due to their high-power density and reliability in consumer electronics and industrial systems. Hybrid supercapacitors, blending battery-like storage with the quick response of EDLCs, are rapidly emerging as industry seeks higher energy storage and efficiency.

Automotive: The Prime Growth Engine

The automotive sector commands the largest share of demand for graphene-enhanced energy storage, accounting for 40% of total applications in 2025. This is primarily propelled by the rapid expansion of electric vehicles and next-gen mobility solutions that require fast-charging, long-range batteries. Aerospace and defense, while smaller, is noteworthy for its high growth trajectory, as lightweight, high-power solutions become central to the industry’s evolution.

.png)

China Accelerates Global Leadership in Graphene-Enhanced Battery Innovation

China has asserted itself as the unrivaled leader in the global graphene-enhanced batteries and supercapacitors market, consistently driving the majority of new patents and industrial deployments. The country is home to more than 60% of global graphene energy storage patents, buoyed by government-backed powerhouses like the Beijing Graphene Institute and Ningbo Graphene Innovation Center. Industrial giants such as CATL and Huawei have mainstreamed graphene into high-performance EV batteries and fast-charging supercapacitors. In 2023, Huawei launched Li-ion batteries utilizing graphene for superior thermal stability—tackling safety and performance bottlenecks in EVs and smartphones. The momentum continues, as CATL’s ongoing investment in graphene solid-state batteries is poised to reach commercialization by 2025–26, further expanding China’s dominance in next-gen energy storage. Notably, ChaoYang Technology’s 2024 launch of graphene-enhanced silicon anode batteries underscores the market’s rapid shift from research to mass adoption, with deep institutional and venture support propelling large-scale rollouts across automotive, grid, and portable electronics sectors.

United States Ramps Up R&D and Commercialization of Graphene-Based Energy Storage

The United States stands at the forefront of graphene energy storage innovation, fueled by robust government funding and industry-academic collaboration. The Department of Energy (DOE) has allocated over $50 million to graphene battery projects, supporting leading research from MIT, Stanford, and UCLA. U.S. applications span aerospace (notably NASA), military, and a growing electric vehicle ecosystem, with Tesla and Nanotech Energy leading commercialization. Nanotech Energy’s 2023 debut of non-flammable graphene batteries marked a milestone in energy storage safety and durability. Meanwhile, Graphene Manufacturing Group’s (GMG) facility expansion in Texas exemplifies the U.S. drive to localize high-volume graphene battery production. Recent funding rounds, such as Lyten’s $200 million raise for lithium-sulfur batteries, reflect surging investor confidence in graphene’s commercial readiness for advanced mobility and grid-scale applications. The synergy between federal investment, private capital, and elite research universities positions the United States as a powerful force in global graphene energy storage.

South Korea Propels Graphene Battery Tech in Consumer Electronics and Mobility

South Korea’s renowned electronics sector has become a major catalyst for the development and deployment of graphene-enhanced batteries and supercapacitors. Samsung SDI and LG Chem have heavily invested in graphene anode R&D, aiming to support the country’s dominant position in smartphones and EVs. In 2024, Samsung secured a patent for graphene-coated batteries designed for ultra-fast charging and improved lifecycle—an innovation likely to reshape the consumer electronics and EV landscape. LG Energy Solution is actively trialing graphene-enhanced batteries in next-generation electric vehicles from Hyundai and Kia, seeking to extend range and durability. The research community, led by KAIST, has delivered breakthroughs such as a graphene-hybrid supercapacitor with double the energy density of previous generations (2024). South Korea’s market trajectory is set by a unique interplay of advanced research, rapid prototyping, and direct integration into global tech supply chains.

Japan Focuses on Industrialization and Consumer Applications of Graphene Supercapacitors

Japan’s graphene energy storage sector is supported by substantial public investment, with NEDO funding exceeding $30 million for graphene-related battery projects. Companies like Sony, Panasonic, and Hitachi Zosen are pushing commercial frontiers, with Hitachi Zosen’s 2023 rollout of graphene supercapacitors for industrial applications leading the way. Toyota is intensifying research into graphene’s use in solid-state batteries, targeting next-gen EV and hybrid platforms. Osaka University’s 2024 achievement—a 40% boost in graphene battery lifespan—demonstrates the nation’s focus on reliability and long-term performance. The Japanese ecosystem excels at transforming lab-scale research into high-volume, quality-driven consumer and industrial products, reinforcing its legacy in electronics, automotive, and battery sectors.

United Kingdom Drives Graphene Battery Progress Through University-Industry Partnerships

The United Kingdom is leveraging its status as the birthplace of graphene (University of Manchester) to build a formidable presence in the graphene battery and supercapacitor market. The University of Manchester remains a hub of advanced research, closely connected to commercial ventures such as Britishvolt (EVs) and aerospace leader Rolls-Royce. In 2023, ZapGo released graphene supercapacitors designed for electric vehicles, while Paragraf is ramping up battery materials production. Strategic partnerships—like Graphene@Manchester and Rolls-Royce in 2024—highlight the UK’s ability to transfer academic discoveries into industrial and aerospace-scale innovation. The UK’s focus on clean energy, advanced mobility, and high-value manufacturing secures its growing influence in global graphene energy storage.

Germany Pushes Automotive Electrification with Graphene Supercapacitors and Batteries

Germany, the automotive and engineering powerhouse of Europe, is channeling investment from BMW, BASF, and other titans into graphene-enhanced energy storage for both vehicles and grid solutions. Companies such as Skeleton Technologies (operating in Estonia and Germany) have rolled out graphene supercapacitors for industrial and automotive uses, delivering performance improvements in charging speed and power density. The Fraunhofer Institute’s 2024 breakthrough in graphene-enhanced solid-state batteries adds R&D credibility and a technology pipeline for OEMs like Porsche and Volkswagen. Germany’s market focus is on electrification, reliability, and industrial-scale energy solutions, positioning it as a top innovator and adopter within the EU.

Australia Advances Graphene Battery Materials for Energy and Mining Sectors

Australia is rapidly scaling its presence in the global graphene batteries and supercapacitors market, with CSIRO leading pioneering research on production technologies. Graphene Manufacturing Group (GMG) has commercialized graphene-aluminum-ion batteries, a leap that aligns with the country’s mining and renewable energy priorities. The University of Queensland’s 2024 work, achieving a 50% efficiency improvement in graphene supercapacitors, illustrates a strong R&D pipeline and technology transfer. Australia’s strategy leverages its mineral wealth, world-class research, and a focus on clean energy and mining applications to carve out a robust and specialized market segment.

Canada Expands Graphene Battery Manufacturing and Grid Applications

Canada is making strides in both high-volume graphene production and deployment in advanced battery applications. Montreal-based NanoXplore has scaled graphene manufacturing for automotive and energy storage use-cases, while Hydro-Québec’s 2023 trials with graphene-Li-ion batteries and NRC’s 2024 partnership with VoltaXplore for a battery gigafactory signal a maturing ecosystem. Canadian firms are also exploring collaborations with major EV manufacturers and utilities, supporting grid storage and clean mobility. Strategic government-industry alliances ensure Canada’s growing competitiveness in the North American and global graphene battery supply chains.

Graphene-Enhanced Batteries and Supercapacitors Market Report Scope

Graphene-Enhanced Batteries and Supercapacitors Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$680.6 Million

|

|

Market Size (2034)

|

$5726.4 Million

|

|

Market Growth Rate

|

26.7%

|

|

Segments

|

By Type (Organic, Conventional), By Form (Whole Chia Seeds, Powdered Chia Seeds, Chia Seed Oil), By End-User (Food and Beverages, Pharmaceuticals and Nutraceuticals, Personal Care and Cosmetics, Others), By Distribution Channel (Online, Offline)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Samsung SDI (South Korea), Panasonic (Japan), LG Chem (South Korea), CATL (Contemporary Amperex Technology Co. Limited) (China), BYD Company (China), Nanotech Energy (USA), Graphenano (Spain), Skeleton Technologies (Germany), ZapGo Ltd. (UK), Talga Group (Australia), Graphene Manufacturing Group (GMG) (Australia), Haydale Graphene Industries (UK), Lyten (USA), Echion Technologies (UK), ZincFive (USA), StoreDot (Israel), Nawa Technologies (France), CAP-XX (Australia), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Graphene-Enhanced Batteries and Supercapacitors Market Segmentation

By Graphene-Enhanced Batteries

Lithium-ion batteries

Lithium-sulfur batteries

Solid-state batteries

By Graphene-Enhanced Supercapacitors

Electrochemical double-layer capacitors (EDLCs)

Pseudocapacitors

Hybrid supercapacitors

By Application

Consumer Electronics

Automotive

Industrial & Energy Storage

Aerospace & Defense

Medical Devices

By Graphene Type

Graphene Oxide (GO)

Reduced Graphene Oxide (rGO)

Graphene Nanoplatelets (GNPs)

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Graphene-Enhanced Batteries and Supercapacitors Market: Profiles & Strategies

Samsung SDI (South Korea)

Panasonic (Japan)

LG Chem (South Korea)

CATL (Contemporary Amperex Technology Co. Limited) (China)

BYD Company (China)

Nanotech Energy (USA)

Graphenano (Spain)

Skeleton Technologies (Germany)

ZapGo Ltd. (UK)

Talga Group (Australia)

Graphene Manufacturing Group (GMG) (Australia)

Haydale Graphene Industries (UK)

Lyten (USA)

Echion Technologies (UK)

ZincFive (USA)

StoreDot (Israel)

Nawa Technologies (France)

CAP-XX (Australia)

* List Not Exhaustive

Methodology: Graphene-Enhanced Batteries and Supercapacitors Market Research Approach

This report leverages a robust, multi-stage research methodology to deliver comprehensive and credible analysis on the global graphene-enhanced batteries and supercapacitors market. Extensive secondary research was conducted using scientific literature, patents, company filings, industry association reports, and regulatory databases to establish the foundational market landscape, key trends, and recent innovations. This was complemented by primary research, including structured interviews and surveys with executives from leading graphene, battery, and supercapacitor manufacturers, as well as experts from end-user industries such as automotive, energy, and consumer electronics. Market sizing and forecasts were derived using both bottom-up and top-down modeling, cross-validated with proprietary datasets, trade data, and expert insights, ensuring accuracy and depth across all major segments and geographies. Competitive intelligence, technology benchmarking, and country-level analysis were further enriched through continuous monitoring of strategic partnerships, product launches, and government initiatives.

Research Coverage and Deliverables

Market Segmentation:

-

By Graphene-Enhanced Batteries: Lithium-ion, Lithium-sulfur, Solid-state batteries

-

By Graphene-Enhanced Supercapacitors: EDLCs, Pseudocapacitors, Hybrid supercapacitors

-

By Application: Consumer Electronics, Automotive, Industrial & Energy Storage, Aerospace & Defense, Medical Devices

-

By Graphene Type: Graphene Oxide (GO), Reduced Graphene Oxide (rGO), Graphene Nanoplatelets (GNPs), Others

-

By Geography: North America, Europe, Asia-Pacific, South America, Middle East & Africa; with deep-dives into 21 countries

Competitive Landscape:

- Profiles and strategies of 18+ leading companies, including recent product launches, R&D pipelines, collaborations, and capacity expansions

Technology & Innovation Analysis:

- Coverage of hybrid architectures, new electrode materials, fast-charging solutions, and scalable manufacturing methods

Market Sizing & Forecasts (2025–2034):

- Revenue projections, volume analysis, and CAGR calculations for all major segments and regions

Strategic Insights:

- Analysis of trends, growth opportunities, regulatory impact, and investment climate

Deliverables:

- Full PDF report, customizable Excel data pack, segment-wise charts and tables, executive summary, and analyst support for queries

Table of Contents: Graphene-Enhanced Batteries and Supercapacitors Market (2025–2034)

1. Executive Summary

1.1 Market Overview and Key Highlights

1.2 Growth Drivers and Future Outlook

1.3 Key Segmentation Insights

2. Graphene-Enhanced Batteries and Supercapacitors Market Overview (2021- 2034)

2.1 Market Definition and Scope

2.2 Market Size and Forecast (2025–2034)

2.3 Graphene’s Role in Energy Storage: Technical Advantages and Breakthroughs

3. Market Analysis: Graphene-Enhanced Batteries and Supercapacitors

3.1 Industry Dynamics and Recent Developments (2024-2025)

3.1.1 Graphene Innovations in Lithium-Ion Batteries (LIBs)

3.1.1.1 Talga Group: Graphene-Enhanced Silicon Anodes

3.1.1.2 NanoGraf: Graphene-Silicon Anode Batteries for Defense

3.1.2 Advancements in Graphene-Enabled Lithium-Sulfur (Li-S) Batteries

3.1.2.1 Lyten: Scaling Graphene-Enabled Li-S Batteries

3.1.2.2 Graphene Flagship: Progress in Graphene-Sulfur Cathodes

3.1.3 Graphene's Role in Solid-State Battery Development

3.1.3.1 Solidion Technology: Graphene in Solid-State Designs

3.1.4 Momentum in Graphene-Based Supercapacitors

3.1.4.1 Skeleton Technologies: Curved Graphene Supercapacitors

3.1.4.2 University of California, San Diego: Ultra-thin Graphene Supercapacitors

3.2 Research & Development (R&D) and Government Initiatives

3.2.1 US Department of Energy Funding

3.2.2 CATL Patent Activity

3.2.3 University of Manchester Research

3.3 Key Market Trends

3.3.1 Trend: Integration of Graphene Hybrid Architectures in Next-Generation Batteries

3.4 Market Opportunities

3.4.1 Opportunity: Decentralized Manufacturing of Graphene-Based Supercapacitors for Renewable Microgrids

4. Competitive Landscape of the Graphene-Enhanced Batteries and Supercapacitors Market

4.1. Global Competitive Overview

4.2. Strategic Initiatives and Collaborations

5. Global Market Share and Segmentation Analysis: Graphene-Enhanced Batteries and Supercapacitors Market (2021-2034)

5.1 Market Share Analysis by Graphene-Enhanced Batteries

5.1.1 Lithium-ion Batteries

5.1.2 Lithium-sulfur Batteries

5.1.3 Solid-state Batteries

5.2 Market Share Analysis by Graphene-Enhanced Supercapacitors

5.2.1 Electrochemical Double-Layer Capacitors (EDLCs)

5.2.2 Pseudocapacitors

5.2.3 Hybrid Supercapacitors

5.3 Market Share Analysis by Application

5.3.1 Consumer Electronics

5.3.2 Automotive

5.3.3 Industrial & Energy Storage

5.3.4 Aerospace & Defense

5.3.5 Medical Devices

5.4 Market Share Analysis by Graphene Type

5.4.1 Graphene Oxide (GO)

5.4.2 Reduced Graphene Oxide (rGO)

5.4.3 Graphene Nanoplatelets (GNPs)

5.4.4 Others

6. Country Analysis and Outlook of Graphene-Enhanced Batteries and Supercapacitors Market, 2021- 2034

6.1. North America

6.1.1. United States: Ramps Up R&D and Commercialization of Graphene-Based Energy Storage

6.1.2. Canada: Expands Graphene Battery Manufacturing and Grid Applications

6.1.3. Mexico: Growing Adoption of Graphene in Consumer Electronics and Emerging Automotive Sector

6.2. Europe

6.2.1. Germany: Leading European Innovation in Graphene Battery and Automotive Integration

6.2.2. United Kingdom: Strong Research Hub and Emerging Graphene Production Capabilities

6.2.3. France: Advancing Graphene for Aerospace and Renewable Energy Storage

6.2.4. Spain: Fostering Graphene Applications in Energy and Industrial Sectors

6.2.5. Italy: Focus on Graphene for Lightweight Composites and Energy Efficiency

6.2.6. Russia: Developing Domestic Graphene Production and Application in Specific Industries

6.2.7. Rest of Europe: Diverse Applications and Collaborative Research Efforts

6.3. Asia-Pacific

6.3.1. China: Accelerates Global Leadership in Graphene-Enhanced Battery Innovation and Production

6.3.2. India: Rapidly Expanding Graphene R&D and Application in EVs and Electronics

6.3.3. Japan: Pioneering Graphene in Advanced Electronics and Solid-State Battery Technologies

6.3.4. South Korea: Dominant Player in Graphene-Enhanced Battery Component Manufacturing

6.3.5. Australia: Rich in Raw Materials and Advancing Graphene for Energy Storage

6.3.6. South East Asia: Emerging Market with Growing Demand for Graphene in Consumer Devices

6.3.7. Rest of Asia: Other Developing Markets with Increasing Graphene Adoption

6.4. South America

6.4.1. Brazil: Investing in Graphene Production and Applications for Industrial Growth

6.4.2. Argentina: Exploring Graphene for Energy Storage and Material Science Research

6.4.3. Rest of South America: Nascent Market with Potential for Graphene Integration

6.5. Middle East & Africa

6.5.1. United Arab Emirates: Driving Graphene Research and Commercialization for Diversification

6.5.2. Saudi Arabia: Significant Investments in Renewable Energy and Advanced Materials

6.5.3. South Africa: Utilizing Graphene in Mining Technology and Energy Solutions

6.5.4. Rest of Middle East & Africa: Developing Infrastructure and Growing Interest in Graphene Technologies

7. Graphene-Enhanced Batteries and Supercapacitors Market Size Outlook by Region

7.1. North America Graphene-Enhanced Batteries and Supercapacitors Market Size Outlook to 2034

7.1.1. By Graphene-Enhanced Batteries (Lithium-ion, Lithium-sulfur, Solid-state)

7.1.2. By Graphene-Enhanced Supercapacitors (EDLCs, Pseudocapacitors, Hybrid)

7.1.3. By Application (Consumer Electronics, Automotive, Industrial & Energy Storage, Aerospace & Defense, Medical Devices)

7.1.4. By Graphene Type (Graphene Oxide, Reduced Graphene Oxide, Graphene Nanoplatelets, Others)

7.2. Europe Graphene-Enhanced Batteries and Supercapacitors Market Size Outlook to 2034

7.2.1. By Graphene-Enhanced Batteries (Lithium-ion, Lithium-sulfur, Solid-state)

7.2.2. By Graphene-Enhanced Supercapacitors (EDLCs, Pseudocapacitors, Hybrid)

7.2.3. By Application (Consumer Electronics, Automotive, Industrial & Energy Storage, Aerospace & Defense, Medical Devices)

7.2.4. By Graphene Type (Graphene Oxide, Reduced Graphene Oxide, Graphene Nanoplatelets, Others)

7.3. Asia Pacific Graphene-Enhanced Batteries and Supercapacitors Market Size Outlook to 2034

7.3.1. By Graphene-Enhanced Batteries (Lithium-ion, Lithium-sulfur, Solid-state)

7.3.2. By Graphene-Enhanced Supercapacitors (EDLCs, Pseudocapacitors, Hybrid)

7.3.3. By Application (Consumer Electronics, Automotive, Industrial & Energy Storage, Aerospace & Defense, Medical Devices)

7.3.4. By Graphene Type (Graphene Oxide, Reduced Graphene Oxide, Graphene Nanoplatelets, Others)

7.4. South America Graphene-Enhanced Batteries and Supercapacitors Market Size Outlook to 2034

7.4.1. By Graphene-Enhanced Batteries (Lithium-ion, Lithium-sulfur, Solid-state)

7.4.2. By Graphene-Enhanced Supercapacitors (EDLCs, Pseudocapacitors, Hybrid)

7.4.3. By Application (Consumer Electronics, Automotive, Industrial & Energy Storage, Aerospace & Defense, Medical Devices)

7.4.4. By Graphene Type (Graphene Oxide, Reduced Graphene Oxide, Graphene Nanoplatelets, Others)

7.5. Middle East & Africa Graphene-Enhanced Batteries and Supercapacitors Market Size Outlook to 2034

7.5.1. By Graphene-Enhanced Batteries (Lithium-ion, Lithium-sulfur, Solid-state)

7.5.2. By Graphene-Enhanced Supercapacitors (EDLCs, Pseudocapacitors, Hybrid)

7.5.3. By Application (Consumer Electronics, Automotive, Industrial & Energy Storage, Aerospace & Defense, Medical Devices)

7.5.4. By Graphene Type (Graphene Oxide, Reduced Graphene Oxide, Graphene Nanoplatelets, Others)

8. Company Profiles (Top Players in Graphene-Enhanced Batteries and Supercapacitors Market)

8.1 Samsung SDI

8.2 Panasonic

8.3 LG Chem

8.4 CATL (Contemporary Amperex Technology Co. Limited)

8.5 BYD Company

8.6 Nanotech Energy

8.7 Graphenano

8.8 Skeleton Technologies

8.9 Talga Group

8.10 Graphene Manufacturing Group (GMG)

8.11 Haydale Graphene Industries

8.12 Lyten

8.13 Echion Technologies

8.14 ZincFive

8.15 StoreDot

8.16 Nawa Technologies

8.17 CAP-XX

9. Methodology

9.1 Research Scope

9.2 Market Research Approach

9.3 Data Sources (Primary and Secondary)

9.4 Market Estimation and Forecasting Model

9.5 Assumptions and Limitations

10. Appendix

10.1 Acronyms and Abbreviations

10.2 List of Tables

10.3 List of Figures