Market Overview: High-Performance Thermal Conductivity and Miniaturization Driving Graphite Film Market Growth

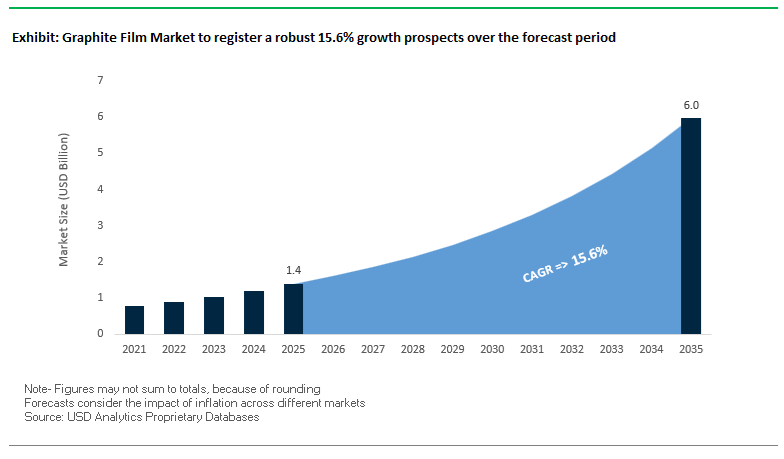

The Graphite Film Market, valued at USD 1.4 billion in 2025, is forecast to reach USD 6 billion by 2035, expanding at a strong CAGR of 15.6% from 2025 to 2035. This rapid scale-up is driven by escalating performance demands in consumer electronics, electric vehicles, semiconductor packaging, industrial sealing systems, and next-generation computing platforms. Manufacturers and vendors are increasingly focusing on ultra-high thermal conductivity synthetic graphite films, flexible graphite sheets, and ultra-thin, customizable film formats designed to address thermal bottlenecks in compact, high-power-density environments. The market is also benefiting from the surge in EV adoption, requiring durable graphite-based thermal interfaces across battery packs, chargers, inverters, and power modules.

Key performance benchmarks reflect the industry’s technological advancement: synthetic graphite films now achieve in-plane thermal conductivities of up to 800 W/m·K, far outperforming copper–aluminum composite heat spreaders, while thicknesses as low as 25–50 µm enable their integration into ultra-thin smartphones and wearables. In EV battery systems and automotive electronics, graphite films are providing stable thermal performance across an extreme temperature range from –55°C to 400°C. Flexible graphite, widely used in industrial gaskets, demonstrates oxidation stability above 400°C, maintaining sealing integrity in corrosive, high-pressure environments. Additionally, simulations in semiconductor packaging show that embedding ultra-thin graphite sheets into flip-chip packages can reduce maximum chip temperature by up to 4.8°C, highlighting the material’s importance in HPC and AI workloads.

Key Industry Insights

- Synthetic graphite films achieve ~800 W/m·K in-plane thermal conductivity, far exceeding metal heat spreaders.

- Ultra-thin films of 25–50 µm are now essential for premium smartphone and wearable thermal design.

- Graphite films maintain thermal reliability across –55°C to 400°C, supporting EV battery thermal management.

- Flexible graphite gaskets withstand continuous temperatures above 400°C, serving oil, gas, and chemical industries.

- Embedding thin graphite sheets in semiconductor packages can reduce chip temperatures by up to 4.8°C at 250 W/cm² loads.

Market Analysis: EV Thermal Interface Innovation, Semiconductor Packaging Integration, and Flexible Graphite IP Expansion

The Graphite Film Market continues to evolve rapidly due to major product launches, portfolio restructuring, semiconductor packaging improvements, and IP strengthening across the value chain. In November 2025, Panasonic Industry released updated technical sheets for its EYG-S and EYG-R Thermal Interface Materials, confirming the integration of PGS Graphite Sheets into EV chargers and automotive power modules. This marks a strategic move as automakers and Tier-1 suppliers increasingly prioritize graphite-based thermal spreading solutions for high-power EV electronics. Earlier, in July 2025, Resonac Holdings reiterated its materials technology pivot toward functional chemicals for semiconductors and mobility applications, emphasizing sustained R&D investment into high-performance synthetic graphite films.

Semiconductor thermal design innovation gained momentum when IBM researchers presented findings at ECTC 2025, highlighting a method to embed thin graphite sheets within organic flip-chip packages to significantly enhance heat spreading performance. This reinforces graphite film adoption in AI accelerators, HPC workloads, and high-bandwidth chip architectures. Meanwhile, the industry is witnessing shifts in product positioning, as Panasonic discontinued its Graphite-PAD line in December 2023 / early 2024, signaling a refined focus toward its higher-performance PGS product variants. This portfolio realignment aligns with increasing demand for Z-directional thermal performance, superior flexibility, and longer material life cycles in modern device designs.

Beyond thermal management, flexible graphite remains a crucial material for industrial sealing, with NeoGraf Solutions highlighting ongoing IP protection for its GraFoil® products (e.g., U.S. Patents 5,830,809; 5,981,072; 6,669,919). Continuous patent reinforcement strengthens barriers to entry in gasket and sealing markets, especially for nuclear and chemical process industries. Innovation is also emerging from smaller firms, which in October 2025 began gaining traction with new adhesive-enhanced graphite films designed for foldable displays and medical devices. Meanwhile, an August 2025 industry report emphasized rising demand for tailorable graphite film thicknesses and form factors, enabling thermal designers in wearables, smartphones, tablets, and EV batteries to specify custom sizes for improved heat dissipation. Collectively, these developments illustrate an industry undergoing rapid sophistication, with emerging technologies reshaping materials engineering across consumer, automotive, and advanced computing markets.

Next-Generation Thermal Conductivity Trends Driving AI Compute, EV Battery Safety, and Composite Integration

Market Trend 1: Commercial Deployment of Ultra-High-Thermal-Conductivity Graphite Films for AI Processors and Advanced Server Modules

A defining trend in the Graphite Film Market is the rapid commercialization of ultra-high thermal conductivity (UHT) pyrolytic graphite films tailored for extreme heat loads in AI accelerators, high-power GPUs, and co-packaged optics. These films achieve 1,500–1,900 W/m·K in-plane thermal conductivity, which is 3–4.5× higher than copper’s 400 W/m·K, offering unmatched heat spreading for dense compute architectures.

Their density of ≈2.1 g/cm³ results in ~80% weight reduction relative to copper heat spreaders of equal volumetric capacity—an essential advantage for rack-density-constrained AI data centers where weight impacts rack mechanics, airflow design, and serviceability. UHT graphite films are also engineered in ultra-thin profiles (10–100 μm), enabling placement within tight inter-component gaps such as between HBM memory stacks, chiplet bridges, and optical modules—areas where conventional metal heat spreaders cannot be integrated.

These films deliver measurable thermal benefits, with hot-spot temperature reductions of 8–12°C versus standard isotropic thermal interface materials. Their anisotropic heat spreading efficiency enables efficient redirection of thermal flux away from localized hotspots, enhancing AI chip reliability, preventing throttling under peak workloads, and supporting next-generation 1 kW-class processor modules.

Market Trend 2: Integration of High-Performance Graphite Films into Composite Battery Enclosures to Enhance EV Safety and EMI Protection

A second major trend is the structural integration of graphite film technology into composite battery enclosures for electric vehicles. The incorporation of thin graphite layers provides >30 dB EMI shielding effectiveness across critical automotive frequency bands, protecting sensitive BMS electronics, ADAS modules, and in-pack sensors from electromagnetic interference.

Graphite films also contribute significantly to thermal runaway mitigation. When embedded within the composite enclosure, the films create passive heat transfer pathways that reduce cell-to-cell temperature gradients and slow down thermal propagation events. This enhanced heat spreading introduces valuable time for detection, warning, and containment in high-energy battery systems.

Composite-compatibility studies reveal that even <5% graphite loading can increase the through-plane thermal conductivity by 100–300%, improving the enclosure’s ability to dissipate heat during fast charging or high-load operation. Notably, the films maintain weight neutrality, as their minimal mass addition is offset by improved composite strength and elimination of heavier metallic shielding solutions. This convergence of structural, thermal, and EMI benefits positions graphite films as a central material in next-generation lightweight EV battery architecture.

High-Growth Commercial Opportunities in Flexible Electronics, Space-Grade Components, and Precision Thermal Systems

Market Opportunity 1: Engineering of Die-Cuttable, Insulated Graphite Films for Wearables and Flexible Electronic Systems

A major emerging opportunity lies in the development of patternable and die-cuttable graphite films with integrated insulation layers for flexible and wearable electronics. These films must withstand extremely tight bending radii of ~1 mm for 10,000+ cycles without delamination—critical for foldable smartphones, flexible OLED displays, and advanced wearables.

Electrical insulation layers, often made of PET or PI, are engineered to maintain dielectric withstand voltages >1 kV while remaining only tens of microns thick. This ensures the graphite film’s high thermal conductivity does not compromise electrical isolation when placed adjacent to processors, RF modules, or metal housings.

Durability under mechanical stress is another requirement: high-performance flexible graphite films must show <5% thermal resistance increase after tensile and compression cycling reflective of human motion or device flexing. Manufacturers are targeting total laminated stack thickness <150 μm (film + adhesive + insulation) to support aggressive miniaturization in smartwatches, AR glasses, and body-mounted sensors.

Market Opportunity 2: Standardization of High-Reliability Graphite Films for Space Systems and Automotive LiDAR Thermal Control

Graphite film suppliers are also positioned to benefit from rising demand in space-grade thermal management systems and automotive LiDAR modules, both of which require extremely high reliability under harsh conditions. Space-qualified graphite films must comply with stringent NASA/ESA outgassing standards (TML <1.0%, CVCM <0.1%) to avoid deposition on optics, imaging sensors, and thermal radiators in vacuum environments.

These films are further validated through repeated thermal cycling between −40°C and 85°C, with performance benchmarks requiring <3% change in thermal resistance after hundreds of cycles—ensuring long-term reliability in orbit or in automotive LiDAR exposed to extreme ambient fluctuations.

Radiation tolerance is essential for satellites and deep-space systems, as UV and cosmic radiation can degrade organic binders used in certain graphite-composite laminates. High-purity pyrolytic or synthetic films demonstrate superior radiation hardness, enabling stable long-duration use.

In the automotive sector, LiDAR manufacturers test graphite films under harsh random vibration loads of ~10 grms across 20–2000 Hz, ensuring the films do not detach, crack, or shift during vehicle operation. These stringent qualification requirements are driving demand for standardized, automotive-grade and space-grade graphite film materials with predictable, certifiable performance.

Graphite Film Market Share Analysis

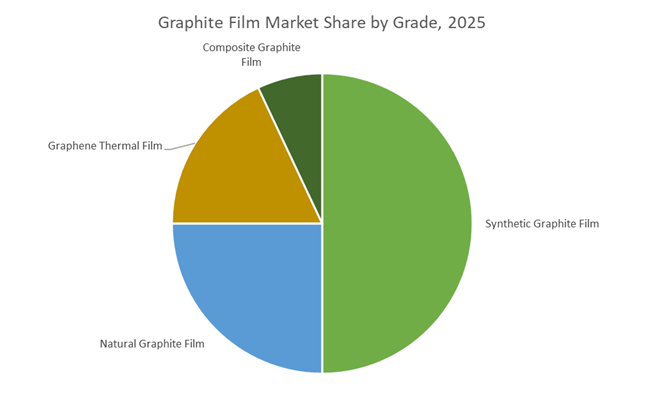

Market Share by Grade: Synthetic Graphite Film Leads Due to Superior Thermal Performance and Manufacturing Precision

Synthetic graphite film holds the largest share of the global graphite film market—approximately 50% in 2025—because it delivers unmatched thermal conductivity, structural uniformity, and reliability required for next-generation electronic and industrial devices. Unlike natural graphite film, which is limited by inherent variability in flake morphology and purity, synthetic graphite film is produced under highly controlled high-temperature graphitization or CVD-based manufacturing conditions, resulting in extremely high in-plane thermal conductivity levels reaching 700–1,500 W/m·K and, in some engineered grades, exceeding 2,000 W/m·K. This superior thermal spreading capability is essential for devices with concentrated heat sources such as 5G processors, multi-camera modules, high-wattage charging circuits, and compact power electronics. Additionally, its exceptional purity (often >99.9% carbon) ensures longer operational life, reduced oxidation risk, and stable performance under repeated thermal cycling, which is critical for flagship consumer devices and EV battery platforms. The ability to precisely tailor thickness, flexibility, and crystalline orientation further cements synthetic graphite film as the preferred solution for OEMs developing ultra-thin, high-power, thermally constrained devices. As thermal design margins tighten across electronics, automotive, and telecom equipment, synthetic graphite film maintains a commanding lead over natural and composite alternatives.

Market Share by End-User Industry: Consumer Electronics Dominates as Thermal Management Becomes Mission-Critical

The consumer electronics sector accounts for roughly 45% of global graphite film demand, driven by the intensifying need for advanced thermal management solutions in compact, high-performance devices. As smartphones, tablets, laptops, wearables, VR headsets, and gaming consoles continue to become thinner while integrating increasingly powerful chipsets, the industry faces severe heat dissipation challenges that cannot be addressed by conventional cooling technologies. Graphite film has emerged as the indispensable heat-spreading material, enabling OEMs to manage localized temperature spikes, prevent thermal throttling, and protect sensitive microcomponents without adding bulk or compromising device design. The transition to 5G, AI-on-edge computing, high-wattage fast charging, and multi-camera imaging systems has further amplified thermal loads, significantly increasing the adoption of high-performance synthetic graphite films. Battery thermal management is another key demand driver, especially in high-capacity smartphone batteries and emerging foldable device architectures where graphite film offers the ideal combination of flexibility, thinness, and thermal conductivity. As consumer electronics lifecycles shrink and performance expectations rise, manufacturers are scaling their integration of graphite film across premium and mid-range devices, solidifying this segment as the largest and fastest-evolving end-use market for graphite films worldwide.

Country Analysis: Global Hotspots for Graphite Film Innovation

Japan: Ultra-Thin High-Thermal-Conductivity Graphite Films and Advanced Materials Leadership

Japan remains the global epicenter of high-performance graphite film innovation, driven by decades of leadership in synthetic graphite, ultra-thin film engineering, and precision manufacturing for high-end electronics. The country’s pioneering role is exemplified by Panasonic Corporation’s continued commercialization of its PGS (Pyrolytic Graphite Sheet), which in June 2024 received renewed market positioning as a premier Thermal Interface Material (TIM) for next-generation power modules including IGBT, SiC, and GaN devices. These modules demand extremely low thermal resistance and stable performance across wide thermal cycles, making Panasonic’s high thermal conductivity solutions essential for automotive inverters, converters, and advanced power control units. Panasonic’s soft graphite-based TIM—GraphiteTIM—further elevates Japan’s leadership, offering an impressive 13 W/mK through-plane conductivity, specifically engineered for high-power automotive applications.

Beyond electronics, Japan’s material science giants are expanding graphite film capabilities into strategic industrial and aerospace markets. Toray Industries’ Project AP-G 2025 underscores the nation’s commitment to high-added-value thermal materials within its Sustainability Innovation (SI) and Digital Innovation (DI) business pillars. Japanese manufacturers are now deploying flexible graphite films in lightweight composite materials for aircraft interiors and industrial machinery, leveraging superior heat diffusion, low mass, and reliability to meet stringent aerospace standards. This cross-sector expansion highlights Japan’s unmatched precision, enabling graphite films optimized for premium smartphones, EV power modules, HPC systems, and mission-critical aerospace components.

China: Vertical Integration in Graphite Materials, Massive Consumer Electronics Manufacturing, and Advanced CVD Breakthroughs

China plays a dominant role in global Graphite Film demand and increasingly in supply, supported by its world-leading consumer electronics ecosystem and rapidly scaling EV industry. Chinese companies specializing in synthetic graphite anode materials—such as Sunrise New Energy—are capitalizing on their existing expertise in graphitization furnaces, micro-powder refinement, and precision carbon processing to expand into thermal graphite sheet production for EV battery modules. This vertical integration approach strengthens cost competitiveness and ensures secure supply for thermal management components as EV platforms continue to diversify. Demand is further fueled by China’s status as the world’s largest manufacturing hub for smartphones, wearables, and laptops, where multilayer graphite heat-spreading films are essential for thermal regulation in increasingly compact form factors.

China is also accelerating innovation in Chemical Vapor Deposition (CVD) and advanced laser processing technologies to yield graphite films exceeding 2500 W/mK in-plane thermal conductivity. These advancements respond directly to the extreme thermal demands of 5G base stations, HPC servers, and data center infrastructure—sectors that require ultra-thin, high-diffusivity films capable of managing rapid heat flux. Continuous investments in fabrication standardization and mass-scale quality control reflect China’s ambition to become a global leader not only in graphite film consumption but also in the production of ultra-high-performance thermal materials for advanced electronics.

South Korea: EV Battery Thermal Management Expansion and Semiconductor Cooling Innovation

South Korea’s advanced manufacturing ecosystem—anchored by global EV battery giants and leading semiconductor fabrication facilities—creates a high-value environment for the adoption and innovation of graphite film technologies. The rapid expansion of Korea’s EV battery sector, which generated $3.07 billion in 2024 in advanced thermal systems investment, has intensified demand for graphite heat spreaders used to prevent thermal runaway, maintain cell uniformity, and improve the safety of high-density lithium-ion battery packs. Graphite films offer unique advantages over aluminum and copper due to their superior in-plane thermal conductivity and low weight, aligning with battery makers' need for high-performance thermal dissipation solutions.

Korea is also benefiting from international research collaboration. Joint NSF–Korean government funding initiatives announced in 2024 aim to resolve semiconductor thermal bottlenecks, a priority as chips move toward higher power density and increasingly compact architectures. These collaborations support the development of innovative graphite-based materials for advanced system-on-chip (SoC) cooling. In addition, South Korea’s global leadership in flexible OLED displays continues to accelerate demand for mechanically robust, flexible graphite films capable of maintaining performance in foldable and rollable devices. This convergence of EV, semiconductor, and display technologies positions South Korea as a critical driver of next-generation graphite film adoption.

United States: High-Value Graphite Films for Aerospace, Defense, and Advanced Battery Systems

The United States holds a strong position in high-value, application-specific graphite film technologies catering to aerospace, defense, and next-generation battery systems. Companies like NeoGraf Solutions remain key innovators, with their eGraf® SpreaderShield™ graphite films engineered specifically for weight-constrained aerospace platforms such as satellites, UAVs, and defense-grade thermal modules. NeoGraf’s materials offer significant mass reduction—one-third the weight of aluminum for equivalent heat spreading—making them essential for spacecraft, avionics, and high-altitude unmanned systems requiring precise thermal stability and minimal structural load.

In the energy sector, U.S. material developers are integrating synthetic graphite heat spreaders into advanced battery architectures to reduce thermal propagation risks and improve safety in electric vehicles and stationary storage systems. This strategic shift reflects increasing demand for safer, more efficient thermal management alternatives to aluminum. At the research frontier, U.S. universities and national labs are pioneering 3D nanostructured thermal interfaces, including graphene–nanowire hybrid structures achieving exceptionally low thermal resistance (~0.24 mm²·K/W). These breakthroughs signal a new wave of next-generation graphite film technologies tailored for quantum computing, high-density AI chips, and extreme-environment electronics.

Competitive Landscape: Leading Players Driving Thermal Materials Innovation and Industrial Graphite Applications

The global Graphite Film Market features prominent players specializing in synthetic graphite films, flexible graphite materials, semiconductor thermal solutions, and advanced carbon processing. Companies such as Panasonic, Resonac Holdings, NeoGraf Solutions, GrafTech International, and SGL Carbon are shaping the competitive environment through innovations in thermal interface materials, functional chemical integration, IP-protected flexible graphite technologies, and highly engineered carbon composites. Their market strategies integrate supply-chain modernization, semiconductor alignment, EV electrification, and high-temperature industrial sealing applications.

Panasonic advances PGS Graphite Sheets for high-power EV and electronics thermal systems

Panasonic Corporation’s Industry division remains a technology leader in synthetic graphite thermal interface materials, driven by its flagship PGS Graphite Sheet portfolio. These ultra-high conductivity films provide excellent in-plane heat spreading while offering mechanical stability and long-term reliability superior to thermal greases. Panasonic’s materials eliminate grease pump-out under severe thermal cycling (–40°C to 100°C), making them indispensable for inverters, converters, automotive LEDs, car-mounted cameras, and server base stations. In November 2025, Panasonic released new product sheets highlighting the integration of its PGS graphite TIMs into EV chargers and power modules, reinforcing its strategic alignment with global vehicle electrification trends.

Resonac Holdings accelerates functional chemical innovation for semiconductor and mobility markets

Resonac Holdings (formerly Showa Denko) maintains a strong presence in synthetic graphite films and carbon-based advanced materials. Under its Vision 2030 transformation, the company is prioritizing functional materials for industries with steep thermal requirements such as semiconductors and electric mobility. With deep carbon process expertise, Resonac offers integrated thermal solutions combining graphite film with other semiconductor back-end process materials. By July 2025, the company had completed over 15 divestitures to streamline its portfolio and sharpen its focus on high-margin, next-generation materials, enabling greater R&D investment in high-performance graphite film technologies.

NeoGraf Solutions dominates flexible graphite sealing markets through proprietary GraFoil® technology

NeoGraf Solutions, the original creator of GraFoil® flexible graphite, remains the industry standard for high-temperature sealing and gasketing applications. Its materials exhibit exceptional resistance to fire, corrosion, aggressive chemicals, and extreme temperatures, making them critical in oil and gas infrastructure, chemical plants, nuclear systems, and automotive sealing. NeoGraf supplies rolls, sheets, laminates, and nuclear-grade variants used in mission-critical industrial applications. The company’s competitive position is backed by strong intellectual property protection across multiple U.S. and foreign patents, ensuring sustained leadership in the global flexible graphite domain.

GrafTech International leverages deep carbon processing expertise for advanced graphite materials

Although now primarily focused on UHP graphite electrodes, GrafTech International retains deep legacy expertise in the expansion and processing of natural graphite flakes for flexible applications. Its decades of experience in high-temperature graphitization (up to 3000°C) and proprietary needle coke processing underpin its relevance in the graphite materials supply chain. While flexible graphite is no longer its primary commercial focus, GrafTech’s world-class carbon processing capabilities continue to influence raw material markets and ensure the availability of ultra-pure carbon materials used across thermal management and high-performance carbon products.

SGL Carbon strengthens SIGRAFLEX® flexible graphite portfolio for industrial and energy applications

SGL Carbon SE is a global leader in carbon-based engineered materials, supplying high-performance SIGRAFLEX® flexible graphite foils and sheets across automotive, chemical processing, and power generation sectors. The company offers reinforced and laminated graphite composites engineered for superior creep resistance, chemical durability, and mechanical integrity under high-temperature conditions. SGL’s strong focus on composite materials science enables it to produce advanced graphite sealing solutions with enhanced oxidation stability, supporting the needs of green energy infrastructure, high-efficiency pumps, and industrial sealing environments that demand performance beyond traditional elastomers.

Graphite Film Market Report Scope

Graphite Film Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2035)

|

$6 Billion

|

|

Market Growth Rate

|

15.6%

|

|

Segments

|

By Grade (Synthetic Graphite Film, Natural Graphite Film, Graphene Thermal Film, Composite Graphite Film), By Film Structure (Single-Layer Films, Multilayer Films), By Thickness (Ultra-Thin, Thin, Standard), By Application Function (Heat Spreaders, Thermal Interface Materials, EMI Shielding & ESD Protection, Thermal Runaway Protection), By End-User Industry (Consumer Electronics, Automotive & EV Systems, Telecommunications & IT, Industrial & Power Electronics, Aerospace & Defense)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Panasonic, Toray Industries, TATSUTA Electric Wire & Cable, GrafTech International, NeoGraf Solutions, SGL Carbon, Boyd Corporation, T-Global Technology, Fuji Electric, Avery Dennison, Laird (DuPont), Sunrise New Energy, Zibo Dahao New Material, Dexerials, Shin-Etsu Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Graphite Film Market Segmentation

By Grade

- Synthetic Graphite Film

- Natural Graphite Film

- Graphene Thermal Film

- Composite Graphite Film

By Film Structure

- Single-Layer Films

- Multilayer Films

By Thickness

- Ultra-Thin (Below 25 μm)

- Thin (25–100 μm)

- Standard (Above 100 μm)

By Application Function

- Heat Spreaders

- Thermal Interface Materials (TIM)

- EMI Shielding / ESD Protection

- Thermal Runaway Protection

By End-User Industry

- Consumer Electronics

- Automotive & EV Systems

- Telecommunications & IT

- Industrial & Power Electronics

- Aerospace & Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Graphite Film Market

- Panasonic

- Toray Industries

- TATSUTA Electric Wire & Cable

- GrafTech International

- NeoGraf Solutions

- SGL Carbon

- Boyd Corporation

- T-Global Technology

- Fuji Electric

- Avery Dennison

- Laird (DuPont)

- Sunrise New Energy

- Zibo Dahao New Material

- Dexerials

- Shin-Etsu Chemical

*- List not Exhaustive

Research Coverage: Graphite Film Market

The latest Graphite Film Market study from USDAnalytics provides a deep-dive intelligence framework that connects technology roadmaps with commercial scaling across electronics, EV platforms, semiconductor packaging, and industrial sealing. Building on extensive primary interviews and secondary datasets, this report investigates how ultra-high thermal conductivity films, flexible graphite sheets, and composite graphite laminates are reshaping thermal design in compact, high-power-density systems. The study tracks material science breakthroughs in synthetic graphite films, evolving thickness profiles, integration into EV battery packs and power modules, and the migration of graphite-based solutions into AI servers and space-grade hardware. Our multi-layered analysis reviews pricing dynamics, capacity additions, portfolio repositioning, and IP-driven differentiation in flexible graphite, while comparing adoption curves between consumer electronics, automotive & EV systems, and telecom/IT infrastructure. The report highlights performance benchmarks such as in-plane thermal conductivity, thermal cycling reliability, and EMI shielding effectiveness, and links them to design-in decisions by OEMs and Tier-1s. With scenario-based forecasting, competitive benchmarking, and ecosystem mapping, this report is an essential resource for product managers, materials scientists, sourcing leaders, and investors seeking to understand how graphite films will underpin next-generation thermal management and miniaturization strategies over the coming decade, supported by the analytical rigor and sector-specific insight of USDAnalytics.

Scope Highlights

- Segmentation (By Grade, Film Structure, Thickness, Application Function, End-User Industry)

- By Grade: Synthetic Graphite Film, Natural Graphite Film, Graphene Thermal Film, Composite Graphite Film

- By Film Structure: Single-Layer Films, Multilayer Films

- By Thickness, Ultra-Thin (Below 25 μm), Thin (25–100 μm), Standard (Above 100 μm)

- By Application Function: Heat Spreaders, Thermal Interface Materials (TIM), EMI Shielding / ESD Protection, Thermal Runaway Protection

- By End-User Industry: Consumer Electronics, Automotive & EV Systems, Telecommunications & IT, Industrial & Power Electronics, Aerospace & Defense

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Horizon: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies: Includes detailed analysis and profiles of 15+ leading graphite film manufacturers and thermal materials specialists.