Global Green Coatings Market Growth Driven by Decarbonization, Bio-Based Innovation, and Low-VOC Technology Adoption

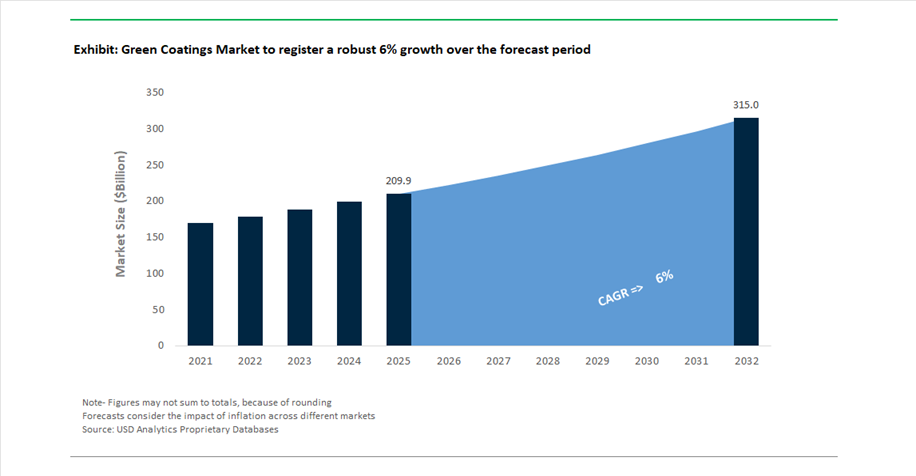

The global Green Coatings Market was valued at USD 209.9 billion in 2025 and is projected to grow at a CAGR of 6% between 2025 and 2032, reaching USD 315.6 billion by 2032. This large and rapidly expanding market is being reshaped by the convergence of regulatory pressure, sustainability mandates, and technological innovation across architectural, automotive, industrial, and marine sectors.

Green coatings encompass waterborne, powder, UV-cured, high-solids, and bio-based formulations, all designed to minimize environmental impact by reducing volatile organic compounds (VOCs), hazardous air pollutants (HAPs), and lifecycle carbon emissions. A primary growth driver is the global push toward net-zero construction and manufacturing, where coatings are no longer viewed as ancillary materials but as critical contributors to energy efficiency and emissions reduction.

Another major structural trend is the shift toward bio-based and circular raw materials, including the use of renewable feedstocks such as bio-naphtha, plant-derived resins, and recycled polymers. This transition is enabling manufacturers to maintain performance while significantly lowering the carbon footprint of coating systems. Additionally, functional green coatings—such as those that improve fuel efficiency, reduce drag, or enhance insulation—are gaining prominence as industries seek operational decarbonization beyond compliance.

Bio-Based Coatings Breakthroughs, and Data-Driven Sustainability Reshape Market Dynamics

The green coatings market is undergoing a structural transformation driven by industry consolidation, sustainable product innovation, and digital transparency tools. In November 2025, AkzoNobel and Axalta Coating Systems announced a $25 billion merger, creating a combined entity focused on leading the global green coatings transition. The collaboration aims to accelerate the development of 100% bio-based industrial coatings and low-VOC architectural systems, particularly targeting high-growth markets such as India and Vietnam.

Bio-based innovation is gaining strong commercial traction. In May 2025, BASF expanded its biomass-balanced automotive refinish portfolio into North America, enabling up to 20% CO₂ reduction without requiring changes to existing application processes. Similarly, AkzoNobel developed bio-based interior coatings for the KIA EV9, utilizing renewable raw materials such as rapeseed oil and pine rosin, marking a significant step toward sustainable automotive interiors.

Sustainability is increasingly quantified through performance metrics. In February 2026, Jotun reported that its high-performance marine coatings contributed to 11.8 million tonnes of avoided CO₂ emissions, highlighting the growing importance of functional green coatings that deliver measurable environmental benefits.

Low-VOC and zero-emission technologies are expanding rapidly. In December 2025, AkzoNobel launched its “It All Adds Up” campaign, promoting 100% solids UV coatings that eliminate VOC emissions entirely, reducing up to 500 grams of VOC per liter compared to traditional solvent-based systems. Complementing this, PPG Industries introduced its Productos ECO line in Latin America, incorporating recycled materials and low-emission formulations for green building applications.

Strategic portfolio restructuring is enabling companies to focus on high-margin sustainable technologies. In February 2026, AkzoNobel divested its Indian decorative business to JSW Paints, allowing it to redeploy capital toward premium green performance coatings, while strengthening JSW’s position in eco-certified architectural products.

Color and design innovation are also aligning with sustainability goals. In October 2025, BASF introduced its 2025–2026 color trends collection, incorporating renewable and recycled raw materials into high-performance pigments, demonstrating that sustainability can coexist with advanced aesthetics.

Financial performance is reinforcing the business case for green coatings. In March 2025, Hempel reported record EBITDA driven by its focus on sustainable marine and energy coatings, underscoring the profitability of environmentally advanced solutions.

Digitalization is emerging as a key differentiator. In December 2025, AkzoNobel launched a Carbon Footprint Calculator, enabling customers to quantify emissions reductions—up to 61% when switching to waterborne or UV systems—transforming sustainability into a data-driven decision-making tool.

Cradle-to-Cradle Certification Becoming a Core Specification in Commercial Real Estate

The green coatings industry is undergoing a structural shift as institutional investors and real estate developers increasingly adopt lifecycle-based sustainability frameworks such as Cradle-to-Cradle certification. Unlike traditional environmental compliance focused solely on VOC emissions, this approach evaluates full material health, recyclability, and supply chain transparency. As of 2026, commercial projects targeting advanced certifications such as LEED v4.1 and WELL v2 are prioritizing coatings that achieve Gold or Platinum material health ratings, ensuring the elimination of hazardous substances such as PFOA, halogenated flame retardants, and ortho-phthalates. This transition is directly influencing asset valuation, with certified green buildings demonstrating rental premiums of 7% to 11% in major global markets. Additionally, manufacturers are integrating recycled content into coating formulations, with leading products incorporating up to 35% recycled raw materials, supporting corporate Scope 3 emission reduction targets. The growing institutionalization of sustainability standards is evident in procurement practices, where over 50% of new office refurbishment projects in key European cities now mandate third-party certified green coatings in initial specifications. These developments are embedding lifecycle sustainability as a competitive differentiator, positioning certified green coatings as a default requirement in high-value commercial construction projects.

Bio-Renewable Antifouling Coatings Replacing Toxic Marine Systems Under EU Regulations

The marine coatings segment is experiencing a major chemical transition driven by regulatory restrictions on toxic biocidal substances under the European Union’s Biocidal Products Regulation. Traditional antifouling coatings, which relied on heavy metals and persistent toxins, are being replaced by bio-renewable systems based on rosin and natural derivatives. These coatings achieve bio-based carbon content levels between 40% and 60%, significantly reducing environmental impact while maintaining functional performance. Advances in controlled polishing technology enable these coatings to maintain smooth hull surfaces with roughness levels below 100 micrometers over extended operational cycles, contributing to fuel efficiency improvements of 6% to 9% in long-distance shipping routes. The shift toward non-toxic fouling release technologies, including silicone-hydrogel hybrids, is also reducing the need for in-water cleaning by approximately 25%, minimizing ecological disruption in marine ecosystems. Regulatory pressure has intensified following recent review cycles, with over 15 legacy biocidal substances facing restrictions, leading to a 30% increase in the adoption of copper-free antifouling systems. These developments are positioning bio-renewable marine coatings as a sustainable alternative that balances environmental compliance with operational efficiency in global shipping industries.

US GSA Mandates Driving Demand for Bio-Based and Ultra-Low VOC Coatings in Federal Buildings

The United States General Services Administration is significantly influencing the green coatings market through updated P100 Facilities Standards that mandate the use of sustainable materials in federal buildings. Under these guidelines, coatings used in government-owned and leased properties must meet strict bio-based content requirements, typically ranging from 20% to 25% under the USDA BioPreferred program. In parallel, VOC emission thresholds have been reduced to below 10 grams per liter for flat architectural coatings, effectively requiring the adoption of waterborne, near-zero emission technologies. These requirements are supported by substantial federal investment in building modernization programs, creating a large and stable demand base for compliant coatings. Additionally, all suppliers must provide Environmental Product Declarations supported by lifecycle assessments, increasing the importance of transparency and data-driven sustainability reporting. These stringent procurement criteria are creating high entry barriers while offering significant growth opportunities for manufacturers capable of delivering certified, low-emission, and bio-based coating solutions for large-scale public infrastructure projects.

South Korea G-SEED 2026 Revision Accelerating Adoption of Low-Emission and Carbon-Negative Coatings

South Korea’s revised Green Standard for Energy and Environmental Design is creating a strong growth opportunity for green coatings, particularly in high-density residential developments. The updated framework introduces a weighted scoring system that incentivizes the use of low-emission and bio-based materials, with additional certification points awarded for coatings that meet stringent environmental criteria. Projects utilizing coatings certified under the Korea Eco-Label and demonstrating ultra-low emissions, including total volatile organic compound rates below 0.02 milligrams per square meter per hour, can gain a competitive advantage in securing approvals and financing. The revision also introduces incentives for carbon-negative materials derived from renewable or captured carbon sources, encouraging innovation in sustainable coating chemistries. These regulatory changes are aligned with national air quality improvement initiatives, particularly in urban centers such as Seoul, where large residential developments must demonstrate high levels of environmental compliance. Market adoption is accelerating, with more than 65% of construction firms indicating a transition toward bio-green material specifications to qualify for government-backed financing programs. These dynamics are positioning South Korea as a key market for advanced green coatings aligned with next-generation sustainability standards.

Green Coatings Market Share 2025: Low-VOC Formulations and Contractor Adoption Lead Sustainability Shift

Formulation Insights: Low-VOC Coatings Dominate with Regulatory Compliance and Performance Balance

The low-VOC segment leads the green coatings market with a 38% market share in 2025, driven by stringent environmental regulations and growing demand for sustainable coating solutions. Regulatory frameworks such as EPA standards in the United States, REACH regulations in Europe, and China’s GB standards mandate strict limits on volatile organic compound emissions, making low-VOC coatings the baseline requirement for architectural and industrial applications. These formulations strike an optimal balance between environmental compliance and performance, offering comparable durability, adhesion, and gloss to conventional coatings at a relatively moderate cost premium. This makes them highly attractive for commercial construction, infrastructure projects, and institutional buildings where both sustainability and budget considerations are critical. As global policies continue tightening around emissions and indoor air quality, low-VOC coatings will remain the cornerstone of growth in the green coatings market.

User Type Insights: Professional Contractors Drive Adoption Through Compliance and Efficiency

The professional contractors and applicators segment dominates the green coatings market with a 52% share in 2025, reflecting their central role in executing specification-driven sustainable construction projects. Architects, developers, and facility managers increasingly mandate the use of eco-friendly, low-VOC or zero-VOC coatings in tenders for government buildings, healthcare facilities, educational institutions, and commercial spaces, making contractors key adopters. Additionally, green coatings offer a significant low-odor advantage, reducing worker exposure to harmful emissions and enabling faster re-occupancy of renovated spaces—a critical factor for projects such as hotels, hospitals, and office refurbishments. Contractors leverage these benefits to improve project timelines and client satisfaction. As sustainability certifications and indoor air quality standards gain importance globally, professional contractors will continue to be the primary drivers of green coatings market expansion.

Green Coatings Market Competitive Landscape: Low-VOC Innovation, Circular Economy Materials, and Sustainable Infrastructure Driving Market Leaders

The green coatings market is highly competitive, driven by low-VOC formulations, bio-based resins, and circular economy initiatives. Leading players are focusing on sustainable product portfolios, digital efficiency tools, and capacity expansion to meet rising demand across construction, automotive, packaging, and industrial applications.

PPG drives sustainable coatings leadership with recycled materials and digital efficiency platforms

PPG Industries is strengthening its leadership in the green coatings market through a strong shift toward sustainably advantaged products, which now account for 44% of its total 2026 sales. Its ENVIROLUXE™ Plus powder coatings integrate recycled plastic content, reinforcing circular economy principles in industrial coatings. The company has scaled HOBA® Pro 2848 non-BPA coatings, gaining traction in the aluminum beverage packaging segment. PPG is investing $380 million in a new aerospace coatings facility in North Carolina to produce low-emission, high-performance coatings. Its MOONWALK® automated paint mixing system has reached 3,000 installations globally, reducing material waste by 15% in automotive refinish applications. This integration of sustainability, automation, and innovation positions PPG as a leader in eco-friendly coatings.

AkzoNobel accelerates green coatings dominance through mega-merger and carbon-neutral innovation

AkzoNobel N.V. is redefining the green coatings market through strategic consolidation and sustainability-driven innovation. The company is progressing toward a $25 billion merger with Axalta, aiming to create the world’s largest performance and sustainable coatings entity. It has introduced heat-reflective “sunscreen” coatings that reduce building temperatures and energy consumption, supporting urban cooling initiatives. Through its “Sustainability Trio” partnership with BASF and Arkema, AkzoNobel is developing low-carbon architectural powder coatings for infrastructure projects. The company has achieved 100% reusable waste across several European plants, aligning with its goal to halve value-chain emissions by 2030. Its Dulux Better Living Air Clean paint, using bio-based resins, continues to lead the healthy interiors segment.

Sherwin-Williams expands green coating leadership with AI-driven design and Latin America dominance

The Sherwin-Williams Company is enhancing its position in the green coatings market through strategic acquisitions and digital innovation. The integration of BASF’s Suvinil business has strengthened its dominance in eco-friendly architectural coatings across Latin America. The company introduced the SHIFT AI-driven color forecast in 2026, offering 18 optimized colors for low-VOC industrial and commercial applications. Its 2026 EPS guidance of $11.50 to $11.90 reflects strong performance driven by sustainable infrastructure demand. With a network of over 5,000 stores, Sherwin-Williams delivers GreenPro and LEED-certified coatings through localized supply chains, reducing transport-related emissions. This combination of scale, digitalization, and sustainability reinforces its leadership in green building coatings.

BASF strengthens circular economy leadership with bio-based resins and sustainable chemical innovation

BASF SE is repositioning its role in the green coatings market by focusing on circular economy solutions and renewable feedstocks. The company is finalizing the €7.7 billion divestiture of its automotive coatings business to prioritize low-carbon chemical intermediates under its “Winning Ways” strategy. BASF leads in bio-mass balanced resins, which serve as key inputs for high-performance green coatings. Its collaboration with AkzoNobel aims to replace petroleum-derived raw materials with plant-based alternatives in decorative paints. BASF’s advanced R&D in additives, including surfactants and light stabilizers, enables waterborne coatings to match the durability of solvent-based systems. This upstream innovation positions BASF as a critical enabler of sustainable coating technologies.

Nippon Paint drives Asia-Pacific growth with water-based coatings and green certification leadership

Nippon Paint Holdings is a dominant player in the green coatings market, particularly in Asia-Pacific where it holds a 41.06% share. The company is expanding production capacity in India by 10% to 15% to meet rising demand for water-based decorative and industrial coatings. Its dedicated Wood Coatings Business Unit is accelerating the adoption of low-odor and anti-formaldehyde finishes in furniture applications. Nippon Paint’s NIPSEA ecosystem extends beyond coatings into eco-friendly construction chemicals and waterproofing solutions. The company has secured GreenCo Gold and GreenPro certifications, validating its commitment to lead-free and heavy-metal-free products. This regional scale and sustainability focus strengthen its competitive positioning in emerging markets.

Asian Paints accelerates premium green coatings adoption with bio-based innovation and rural market penetration

Asian Paints Limited is expanding its influence in the green coatings market through innovation and strong domestic demand. The company introduced the ColourNext 2026 forecast featuring “Moonlit Silk,” alongside the IRL palette emphasizing biofabrication and tactile finishes such as mycelium-based and plant-dyed coatings. Its premium Green Assure range is experiencing steady growth in urban residential projects. Asian Paints continues to lead rural market transformation with its Neo-Bharat series, promoting the shift from traditional distemper to low-VOC waterborne enamels. Despite cost pressures from crude derivatives, the company has implemented strategic pricing adjustments to maintain margins. This blend of innovation, sustainability, and market penetration reinforces its leadership in India’s green coatings sector.

China Green Coatings Market: Transition to Absolute Emission Caps Driving Waterborne Coatings Demand

China continues to dominate the global green coatings market, driven by its large-scale industrial base and aggressive environmental reforms. The country is undergoing a structural transformation toward water-based coatings and low-VOC formulations, aligning with the upcoming 15th Five-Year Plan (2026–2030). A landmark regulatory shift announced in late 2025 mandates the transition from intensity-based emission controls to absolute emission caps, accelerating the phase-out of solvent-borne coatings—particularly across the highly industrialized Pearl River Delta. This regulatory overhaul is significantly boosting demand for eco-friendly coatings, sustainable industrial coatings, and advanced waterborne coating technologies.

Financial mechanisms are further accelerating this transition. Jiangsu province’s “1+N+N” transition finance system, introduced in early 2025, is channeling capital into green chemistry innovations, including bio-based coatings and low-VOC alternatives. Additionally, green bond issuance in China’s chemicals sector surged by 56.5% in late 2025, targeting modernization of coating production infrastructure. The rapid expansion of the emission trading system (ETS) into sectors like steel is also driving demand for corrosion-resistant green protective coatings. Meanwhile, innovation in nano-filler waterborne dispersions is enabling coatings with equivalent performance to heavy-duty epoxy systems while reducing VOC emissions by up to 90%. The integration of solvent-free PVDF binder coatings in EV battery gigafactories further highlights China’s pivotal role in scaling sustainable coating solutions globally.

United States Green Coatings Market: PFAS-Free Formulations and High-Tech Manufacturing Reshoring

The United States green coatings market is entering a high-growth phase fueled by advanced manufacturing reshoring, regulatory enforcement, and innovation in sustainable materials. The EPA’s TSCA Section 8(a)(7) regulation has catalyzed a nationwide shift toward PFAS-free coatings, transforming both architectural coatings and industrial coatings segments. This regulatory push is driving the adoption of eco-friendly surfactants and next-generation coating formulations with reduced environmental impact.

Simultaneously, the Inflation Reduction Act (IRA) has accelerated investments in sustainable infrastructure, particularly in cool roof coatings and high-reflectivity finishes for federal buildings. The reshoring of semiconductor manufacturing—supported by over $20 billion in new cleanroom facilities—is increasing demand for ultra-low-outgassing green coatings essential for contamination-sensitive environments. Innovation is also advancing rapidly, with the commercialization of 100% bio-based polyurethane coatings for aerospace applications and the introduction of cryogenic-stable coatings designed for liquid hydrogen systems in the emerging space economy. Strategic collaborations between chemical companies and biotech startups are further pushing the boundaries, including the development of fungal mycelium-based binders, positioning the U.S. as a leader in sustainable coating innovation.

Germany Green Coatings Market: REACH Compliance and Smart Manufacturing Accelerating Sustainable Coatings

Germany stands as a central hub for sustainable industrial coatings in Europe, driven by stringent REACH regulations and the EU Green Deal. The country is at the forefront of adopting environmentally friendly coatings technologies, particularly in automotive, construction, and industrial machinery sectors. Regulatory mandates from the European Chemicals Agency (ECHA) in 2025 have enforced the use of migration-tested green coatings in food-processing equipment, significantly expanding the market for compliant and non-toxic coatings.

Technological innovation remains a key growth driver. The adoption of UV-LED curing systems across automotive supply chains in Baden-Württemberg is reducing energy consumption by up to 40%, reinforcing Germany’s leadership in energy-efficient coating technologies. Additionally, advancements such as de-coatable coatings for glass and metal enable full recyclability, aligning with circular economy goals. The expansion of specialty coating centers in North Rhine-Westphalia is further supporting the development of waterborne powder coatings for green hydrogen infrastructure. Urban applications are also growing, with photocatalytic coatings being widely deployed to reduce NOx emissions on building facades in major cities like Berlin and Munich.

India Green Coatings Market: Infrastructure Boom and Low-VOC Paint Adoption Under Smart Cities Initiative

India’s green coatings market is experiencing rapid expansion, fueled by urbanization, infrastructure development, and government-led sustainability initiatives. The PMAY-U 2.0 housing scheme, backed by significant public investment, has driven the adoption of Eco-mark certified low-VOC paints across hundreds of thousands of residential units. This surge in housing demand is a major catalyst for environmentally friendly architectural coatings.

Large-scale investments in Petroleum, Chemicals & Petrochemicals Investment Regions (PCPIRs) are expected to strengthen domestic production of specialty coatings and sustainable chemicals. Additionally, India’s expanding metro rail network—already exceeding 1,000 km—has standardized the use of waterborne anti-graffiti coatings, enhancing durability and reducing maintenance costs. Regulatory interventions, such as mandatory BIS quality control orders for low-VOC coatings, are eliminating non-compliant imports and boosting domestic manufacturing. The Smart Cities initiative is also accelerating the adoption of solar-reflective coatings to mitigate urban heat island effects, while the EV push under “Make in India” is driving demand for specialized green coatings in electric motor components and wiring systems.

Japan Green Coatings Market: Advanced Functional Coatings and Bio-Polymer Innovation Leadership

Japan’s green coatings market is defined by precision engineering, advanced materials science, and high-performance applications. The country is leading innovation in nano-coatings, optical coatings, and bio-based resin systems. In early 2026, Japanese manufacturers achieved a breakthrough with anti-fogging nano-coatings capable of maintaining 99% clarity in extreme humidity conditions, targeting high-end applications in surgical imaging and automotive sensors.

The development of bio-derived FEVE resins is reducing reliance on petrochemical inputs while maintaining durability for infrastructure such as high-speed rail. Government-backed R&D initiatives are also advancing recycled fluoropolymer coatings, promoting a closed-loop system for high-value materials. Japan’s dominance in optical coatings is evident in the development of high-transmittance anti-reflective coatings for AR/VR devices, enabling lighter and more efficient designs. Additionally, strict regulatory oversight ensures that coatings used in consumer appliances are free from hazardous substances like PFOA and PFOS, reinforcing Japan’s commitment to sustainable and safe coating technologies.

Brazil Green Coatings Market: Aerospace Expansion and Green Mobility Driving Demand

Brazil is emerging as a key growth market for green coatings in Latin America, supported by infrastructure investments and a strong aerospace industry. The government’s large-scale infrastructure concessions program introduced in 2025 mandates the use of high-performance green coatings for roads, railways, and sanitation systems, significantly boosting demand for durable and eco-friendly coatings.

The aerospace sector is a major contributor, with Embraer’s long-term investment in sustainable aircraft driving the adoption of chromate-free, waterborne aerospace coatings. Global coating manufacturers are expanding operations in Brazil, establishing automated blending centers that optimize production efficiency and reduce waste. The country’s abundant natural resources, particularly titanium dioxide, are enabling localized supply chains for sustainable paint formulations. Additionally, Brazil’s Green Mobility initiatives are promoting hybrid vehicle production, increasing the use of anti-corrosive coatings for lightweight aluminum structures. Updated fire safety regulations are also driving demand for flame-retardant coatings in public infrastructure, further expanding the market scope.

Green Coatings Market Report Scope

Green Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$209.9 Billion

|

|

Market Size (2032)

|

$315.6 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Technology (Water-borne Coatings, Powder Coatings, High-Solids Coatings, Radiation-Cured Coatings), By Source (Vegetable Oils, Soybean-based, Corn-based, Clay and Mineral-based, Recycled Content), By Formulation (Low-VOC, Zero-VOC, Solvent-Free, Bio-based, Biodegradable), By End-Use Industry (Architectural and Construction, Automotive and Transportation, Industrial Manufacturing, Packaging, Wood and Furniture, Aerospace and Defense, Marine and Protective), By Substrate (Metal, Wood, Concrete and Masonry, Plastics and Composites, Paper and Paperboard), By Application Method (Spray Applied, Roll and Curtain Coating, Electrostatic Powder Coating, Dip and Flow Coating), By User Type (Industrial OEMs, Professional Contractors and Applicators, DIY)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., BASF SE, Axalta Coating Systems Ltd., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., RPM International Inc., Jotun A/S, Asian Paints Limited, Hempel A/S, Sika AG, Arkema S.A., Berger Paints India Limited, Tikkurila Oyj

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Green Coatings Market Segmentation

By Technology

- Water-borne Coatings

- Acrylic

- Alkyd

- Epoxy

- Polyurethane

- Powder Coatings

- High-Solids Coatings

- Radiation-Cured Coatings

By Source

- Vegetable Oils

- Soybean-based

- Corn-based

- Clay and Mineral-based

- Recycled Content

By Formulation

- Low-VOC

- Zero-VOC

- Solvent-Free

- Bio-based

- Biodegradable

By End-Use Industry

- Architectural and Construction

- Automotive and Transportation

- Industrial Manufacturing

- Packaging

- Wood and Furniture

- Aerospace and Defense

- Marine and Protective

By Substrate

- Metal

- Wood

- Concrete and Masonry

- Plastics and Composites

- Paper and Paperboard

By Application Method

- Spray Applied

- Roll and Curtain Coating

- Electrostatic Powder Coating

- Dip and Flow Coating

By User Type

- Industrial OEMs

- Professional Contractors and Applicators

- DIY

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Green Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- BASF SE

- Axalta Coating Systems Ltd.

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- RPM International Inc.

- Jotun A/S

- Asian Paints Limited

- Hempel A/S

- Sika AG

- Arkema S.A.

- Berger Paints India Limited

- Tikkurila Oyj

*- List not Exhaustive