Market Analysis: Strategic Acquisitions and Technological Breakthroughs Propel the 3D Printing in Healthcare Market

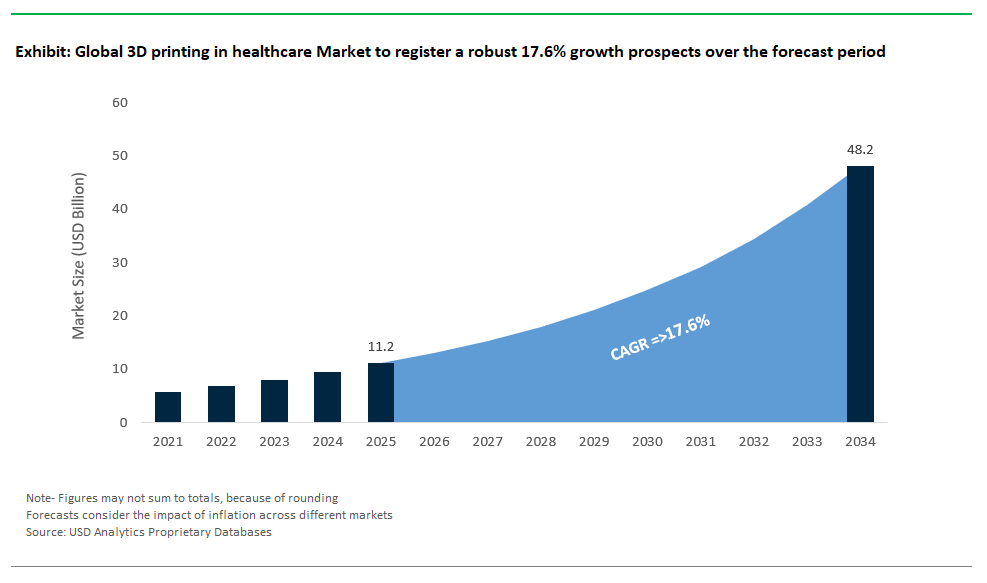

The Global 3D printing in healthcare Market Size is estimated at $11.2 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 17.6% to reach $48.2 Billion by 2034.

The 3D printing in healthcare market is experiencing a surge of innovation, driven by strategic mergers, advanced robotics, bioprinting milestones, and the rising synergy between AI and additive manufacturing. In July 2025, Zimmer Biomet a global leader in medical technology announced the acquisition of Monogram Technologies, marking a major milestone in the integration of 3D printing, AI, and robotic-assisted surgery. Monogram’s semi-autonomous, CT-based total knee arthroplasty (TKA) robotic system, which secured FDA 510(k) clearance in March 2025, showcases how patient-specific implants and personalized surgical planning are being elevated through the convergence of artificial intelligence and 3D printing technology. This deal highlights the accelerating pace of robotics and AI-powered additive manufacturing for bespoke orthopedic solutions, setting a new benchmark in personalized healthcare.

Cutting-edge innovations are also making headlines outside the operating room. In early 2025, Auxilium Biotechnologies successfully leveraged the unique microgravity environment aboard the International Space Station (ISS) to 3D bioprint implantable medical devices with exceptional structural precision. This pioneering experiment not only demonstrates the future potential of space-based bioprinting, but also paves the way for advancements in regenerative medicine and the development of complex tissue constructs that were previously unachievable on Earth. Alongside this, the rapid progress in bioresorbable orthopedic implants notably using magnesium alloys and biocompatible polymers illustrates how 3D printing is delivering next-generation implants that naturally dissolve after fulfilling their therapeutic role, eliminating the need for additional surgeries and enhancing patient recovery.

The healthcare sector is also witnessing new product launches and acquisitions that directly leverage the power of 3D printing for customized care. Sunrise Medical’s acquisition of Made for Movement (MfM) in July 2025 expands its neurorehabilitation device portfolio, where 3D printing is increasingly utilized for the rapid prototyping and manufacturing of tailored orthotic and prosthetic devices. In the same vein, LOBO EV Technologies’ upcoming launch of an AI-powered senior mobility robot demonstrates the industry’s push toward integrating personalized health-monitoring, mobility, and the flexible design capabilities offered by additive manufacturing. These AI-driven, patient-centric solutions not only streamline rehabilitation but also open new pathways for the creation of customized medical devices that enhance quality of life.

Digital health is further transforming with the help of advanced manufacturing. Knipper Health’s acquisition of eBlu Solutions integrates digital platforms with therapy initiation, specialty provider support, and patient engagement. Here, the role of 3D printing extends to the customization of drug delivery systems and medical devices enabling rapid, on-demand manufacturing to suit individual patient needs. The convergence of digital health, AI, and 3D printing underscores a broader trend: healthcare providers are increasingly investing in technologies that enable tailored treatment and real-time health management.

Artificial intelligence continues to shape the future of diagnostics and personalized medicine. At Computex 2025, ASUS presented innovations such as the VivoWatch with “HealthAI Genie” and the Handheld Ultrasound LU800 with AI-assisted imaging. These platforms not only harness big data and AI for precision health monitoring, but also connect seamlessly with 3D printing workflows to create patient-specific anatomical models, diagnostic tools, and procedural guides further advancing the adoption of personalized medical care.

Advancements Shaping the 3D Printing in Healthcare Market

Trend: Surgical Integration of Patient-Specific 3D-Printed Guides & Instruments

The integration of patient-specific 3D-printed surgical guides and instruments is revolutionizing complex medical procedures, especially in orthopedics and craniomaxillofacial surgeries. These tailored tools significantly enhance surgical precision, reducing the necessity for revision procedures due to errors commonly seen in traditional surgical methods. A systematic review of 27 randomized controlled trials across orthopedic procedures highlights the compelling benefits, including a nearly 70% improvement in surgical accuracy, a 42.1% reduction in procedure duration, and over 93% decrease in radiation exposure. These measurable improvements underscore why hospitals increasingly favor personalized 3D-printed guides to optimize patient outcomes and procedural efficiency.

Additionally, patient-specific guides manufactured within hospitals streamline surgical workflows, significantly shortening operation room time and lowering overall costs. A 2025 clinical study involving thoracic scoliosis patients revealed that producing PLA-based surgical guides in-house using fused filament fabrication (FFF) was not only faster but also more cost-effective than outsourcing to external stereolithography (SLA) providers. Further research aggregating 25 clinical studies has shown that the adoption of these 3D-printed instruments typically saves healthcare providers approximately 23 minutes per surgery, equating to cost savings of around $1,488 per case. These advancements position patient-specific surgical instruments as a critical trend driving growth and innovation in the healthcare industry's 3D printing segment.

Opportunity: On-Demand Printing of Bioresorbable Implants in Trauma Care

On-demand 3D printing of bioresorbable implants presents an exceptional growth opportunity in trauma care, particularly for treating complex injuries such as facial fractures and critical bone defects. Made from advanced materials like magnesium alloys and specialty polymers, these implants minimize risks associated with traditional permanent materials, such as infections or immune rejection. Unlike conventional metallic implants, bioresorbable options naturally degrade within the body over time, eliminating the need for additional surgeries to remove hardware and improving overall patient comfort and safety.

Rapid regulatory advancements, notably from agencies such as the FDA, have significantly expedited approval processes for innovative bioresorbable medical devices, encouraging widespread adoption and facilitating faster clinical deployment. For instance, Michigan Medicine's groundbreaking FDA-approved clinical trials in 2025 for 3D-printed bioresorbable tracheal splints highlight this accelerating momentum. Similarly, Hannover Medical School successfully utilized custom 3D-printed bioresorbable bone scaffolds to resolve complex radial shaft injuries after multiple prior surgical failures. In Germany, collaborative research by RWTH Aachen and Fraunhofer ILT has validated automated design systems for patient-specific, load-bearing implants. In-vivo studies confirm these implants’ compatibility and seamless integration into digital surgical planning workflows, enabling personalized, efficient, and effective trauma care. These developments clearly illustrate how on-demand bioresorbable implants represent a transformative opportunity set to reshape the healthcare industry's approach to trauma management.

Competitive Landscape: 3D Printing in Healthcare Market

The 3D printing in healthcare market is witnessing rapid growth fueled by the increasing demand for personalized medicine, complex surgical planning, and cost-efficient medical device manufacturing. This competitive landscape is shaped by innovations in additive manufacturing technologies, biocompatible materials, and advanced software platforms that enable precision, scalability, and customization. Key players are focusing on high-fidelity anatomical modeling, next-generation dental solutions, and groundbreaking developments in bioprinting to address the growing need for patient-specific care and faster prototyping in clinical settings.

Stratasys Ltd. – Multi-Material 3D Printing for Advanced Medical Models

Stratasys is a global leader in polymer-based 3D printing solutions, recognized for its PolyJet and FDM technologies tailored for healthcare. Its flagship products, such as the J5 Digital Anatomy™ and J850™ Digital Anatomy™ Printers, create ultra-realistic anatomical models that mimic human tissue, bone, and vasculature using proprietary materials like BoneMatrix™, TissueMatrix™, and GelMatrix™. These capabilities support pre-surgical planning, simulation, and medical training by delivering models with lifelike haptic feedback and radio-realistic imaging properties. The J5 MediJet™ printer enables multi-material, sterilizable, and biocompatible models for surgical planning and medical device development, while FDM printers provide cost-effective solutions for point-of-care applications. Recent innovations include the launch of the J5 Digital Anatomy Printer in 2024, offering compact, office-friendly design, and a strategic agreement with CollPlant Biotechnologies to advance bioprinting for tissue engineering and regenerative implants. Stratasys’ growing focus on hospital-integrated printing workflows and biocompatible materials cements its leadership in delivering cutting-edge, patient-specific healthcare solutions.

3D Systems Corporation – Comprehensive Additive Manufacturing for Personalized Care

3D Systems is a pioneer in additive manufacturing, known for introducing stereolithography (SLA) and maintaining a strong presence in healthcare through a diverse technology portfolio including SLA, SLS, DMP, and MJP systems. Its solutions cater to customized implants, surgical guides, and detailed anatomical models for complex procedures. The company also offers on-demand manufacturing services, enabling healthcare providers to access high-quality 3D printed components without capital investment in equipment. Dental applications form a significant part of its portfolio, including custom restorations, orthodontic models, and aligner molds. Recent developments highlight investments in regenerative medicine and oncology research, including projects for 3D-printed brain tissue and peripheral nerve repair. Strategic collaborations with medical device companies further enhance its integration into clinical workflows. By combining advanced hardware, materials, and end-to-end services, 3D Systems strengthens its position as a key player in driving personalized healthcare through additive manufacturing.

Materialise NV – Software-Centric Approach to Personalized Healthcare

Materialise stands out in the 3D printing in healthcare market with its software-first strategy, enabling hospitals and manufacturers to optimize additive manufacturing processes. Its flagship Materialise Mimics® Innovation Suite converts medical imaging data into accurate 3D printable models for surgical planning and complex case simulations. In addition to software, Materialise offers prototyping, production services, and innovative digital workflows for personalized orthopedics, implants, and orthotics through solutions like the Phits and Footscan Suites. Recent milestones include the introduction of a bioresorbable implant in clinical trials (2025), showcasing leadership in sustainable medical solutions, and the latest Magics software release, improving additive manufacturing efficiency and scalability. The company’s collaborations with orthopedic firms like restor3d demonstrate its commitment to scaling personalized care solutions globally. Materialise’s blend of software innovation, biocompatible applications, and end-to-end services makes it a dominant force in precision-driven healthcare 3D printing.

EOS GmbH – High-Performance Metal and Polymer Additive Manufacturing

EOS is a leading provider of industrial-grade 3D printing systems, specializing in Direct Metal Laser Sintering (DMLS) and Selective Laser Sintering (SLS) technologies. These systems are widely used in healthcare for manufacturing custom titanium and cobalt-chrome implants, surgical instruments, and high-strength medical device components. The company also provides polymer-based solutions for prosthetics and surgical guides, supported by a comprehensive range of certified biocompatible materials. EOS continues to push innovation with its master file solution for regulatory compliance, simplifying approval for medical applications, and next-generation systems like the EOS M 290-2 and M 290 1kW, which deliver faster, more productive metal additive manufacturing. Technologies such as Smart Fusion and the adoption of Materialise’s CO-AM platform further enhance process monitoring, connectivity, and efficiency. EOS’s focus on series production, regulatory alignment, and material innovation reinforces its role as a top-tier player in industrial-scale medical 3D printing.

Carbon – Digital Light Synthesis™ for Mass Customization in Healthcare

Carbon revolutionizes healthcare 3D printing with its proprietary Digital Light Synthesis™ (DLS™) technology, enabling high-speed, precision production of isotropic parts with exceptional surface quality. This technology powers applications in dental appliances, custom orthotics, prosthetics, and patient-specific medical devices, leveraging Carbon’s range of biocompatible and sterilizable materials such as elastomers and rigid polyurethanes. Advanced design capabilities through Carbon Design Engine™ allow the creation of lattice structures for optimized comfort and functionality, widely used in personalized seating systems and protective healthcare equipment. Recent initiatives include partnerships for custom wheelchair seating solutions and expanding into digital dentures production, addressing the growing demand for same-day dental solutions. Additionally, Carbon is investing in bioprinting research, providing tools for tissue engineering and organ modeling. By combining speed, scalability, and material versatility, Carbon positions itself as a disruptive force in delivering mass customization and next-gen patient-centric solutions.

Market Share and Segmentation Insights: 3D Printing in Healthcare Market

By Technology: Photopolymerization Dominates, Laser Beam Melting Expands Rapidly

In 2025, photopolymerization is expected to hold the largest share of the healthcare 3D printing market at 32.3%, driven by its precision in producing intricate dental aligners, prosthetics, and anatomical models. Its dominance stems from cost efficiency, high detail resolution, and suitability for polymer-based medical applications. However, laser beam melting (LBM) is emerging as the fastest-growing technology, projected to achieve a CAGR of 18.7% between 2025 and 2034. This growth is fueled by rising demand for customized titanium orthopedic implants and spinal reconstruction components, as well as expanding adoption in high-strength surgical instrumentation. LBM’s ability to produce biocompatible, load-bearing implants is transforming orthopedic and maxillofacial surgeries, making it a key enabler for patient-specific treatment solutions.

By Application: Medical Implants Lead, Dental Solutions Surge Ahead

Medical implants and prosthetics dominate the application segment with an estimated 39.8% market share in 2025, supported by the rising trend of personalized hip and knee replacements and growing acceptance of 3D-printed biocompatible materials in orthopedics. These implants reduce surgical time and improve patient outcomes, which continues to drive hospital adoption. On the other hand, the dental segment is positioned for the fastest growth, with a projected CAGR of 19.1% through 2034, thanks to the booming demand for clear aligners, crowns, and bridges. Digital dentistry is revolutionizing the orthodontic landscape as 3D printing accelerates production timelines while delivering unmatched customization. Additionally, innovative uses of 3D printing in biosensors and external wearable devices signal future growth opportunities, particularly in real-time health monitoring and personalized medical devices.

.png)

United States Pioneers FDA Approvals and Innovation in Healthcare 3D Printing

The United States continues to lead the global healthcare 3D printing market, driven by significant regulatory milestones and robust institutional adoption. Notably, in April 2024, U.S.-based 3D Systems secured FDA clearance for patient-specific 3D-printed PEEK cranial implants, enhancing precision and personalization in cranial reconstruction surgeries. Supporting this growth, over 47% of U.S. hospitals now operate in-house 3D printing laboratories, notably expanding their use in orthopedic and dental applications. This widespread adoption underscores the increasing importance of tailored, patient-centric medical solutions that improve surgical outcomes and patient care efficiency.

Complementing institutional use, extensive academic research in bioprinting positions the U.S. at the forefront of medical innovation. Prominent universities such as UT Austin are pioneering groundbreaking techniques, including dual-light 3D printing capable of simultaneously printing soft and hard biological segments, enabling revolutionary cartilage regeneration and neural tissue studies. Additionally, industry consolidation further fuels market expansion, exemplified by Stratasys Ltd.'s strategic acquisition of Arevo, Inc. in March 2024, enhancing its expertise in medical imaging and device manufacturing. Meanwhile, federal funding through the National Institutes of Health (NIH) continues to drive critical advances in tissue engineering, drug delivery systems, and customized medical device fabrication, solidifying the nation’s leadership in healthcare 3D printing innovation.

China Accelerates Healthcare 3D Printing with Strategic Investments and Growing Adoption

China's healthcare 3D printing market is rapidly scaling, propelled by significant governmental backing and surging demand for personalized medicine solutions. As a cornerstone of the nation’s 14th Five-Year Plan, major financial investments prioritize localized 3D printing capabilities, enabling China to address its expanding domestic healthcare needs efficiently. Hospitals increasingly leverage advanced 3D printing technologies for personalized prosthetics and surgical instruments, responding to heightened clinical demand for tailored medical solutions that improve patient outcomes.

Simultaneously, Chinese research institutions have advanced significantly in the bioprinting sector, pursuing groundbreaking collaborations between universities and medical centers. These partnerships aim to pioneer innovations in tissue engineering, organ repair, and transplantation techniques. Coupled with robust private sector and governmental investments in medical technology infrastructure, China’s healthcare 3D printing market is poised for substantial growth. The hardware segment, particularly medical-grade 3D printers, remains the highest revenue generator, reinforcing China’s emerging role as a critical global player in healthcare additive manufacturing.

Germany Enhances Clinical Integration and Material Innovation in Healthcare 3D Printing

Germany maintains a strong presence in the healthcare 3D printing market, supported by its well-established healthcare infrastructure and significant investments in cutting-edge medical technologies. With personalized medicine forecasted to grow at an annual rate of 13%, German healthcare providers increasingly adopt 3D printing solutions, specifically targeting customized medical devices. More than 210 hospitals nationwide have strategically integrated 3D printing technologies, using them to create precise surgical models, prosthetics, and implants, demonstrating widespread clinical acceptance.

In addition to clinical integration, German medical manufacturers are actively integrating additive manufacturing processes, especially Laser Beam Melting (LBM), which holds a substantial 42% market share, renowned for its precision and compatibility with biocompatible materials. Academic and research institutions in Germany further advance the industry through continuous material innovations, addressing existing limitations by developing new biocompatible, durable, and polymer-based medical-grade materials. These collective efforts firmly position Germany as a leading European hub for advanced healthcare 3D printing solutions.

Japan’s Aging Population Fuels Bioprinting and Regenerative Medicine Advancements

Japan’s healthcare 3D printing market experiences robust growth driven by demographic pressures from its rapidly aging population and the resulting increased demand for advanced organ transplantation and regenerative solutions. Government-backed entities like the New Energy and Industrial Technology Development Organization (NEDO) have allocated substantial investments, totaling approximately USD 22 million, aimed at advancing 3D bioprinting technologies, particularly in human tissue regeneration. This significant funding accelerates research and development, facilitating breakthroughs in clinical bioprinting applications.

Moreover, Japanese medical institutions have integrated bioprinting into clinical practices, significantly enhancing reconstructive surgeries, especially for burn injuries and cosmetic reconstruction procedures. Concurrently, top Japanese universities undertake extensive research on next-generation bioinks, refining bioprinting techniques to overcome functional and scalability challenges. Additionally, Japan's pharmaceutical sector increasingly adopts 3D-printed tissues for preclinical drug testing, reducing costs and ethical concerns associated with traditional animal-based methods. Collectively, these initiatives ensure Japan’s continued prominence in healthcare 3D printing innovation.

United Kingdom Expands Clinical 3D Printing Applications and Innovations

The United Kingdom is significantly expanding its adoption of healthcare 3D printing technologies, particularly in patient-specific device manufacturing and surgical planning. The NHS actively scales the use of 3D printing for personalized surgical guides and anatomical models, notably benefiting specialties such as oncology and congenital heart disease. Companies like Axial3D have strengthened partnerships with UK hospitals, providing tailored 3D-printed anatomical models that substantially enhance surgical precision and patient safety.

Parallel to clinical integration, extensive research efforts in the UK aim to develop advanced materials and software that optimize the precision and quality of 3D-printed medical devices. Recent developments include additive manufacturing of artificial muscles and tissues closely resembling natural human tissues, supporting replacement procedures with enhanced biological compatibility. Strong government support through funding and strategic policy initiatives continues to facilitate rapid technology integration into clinical practice, underscoring the UK’s influential role in advancing healthcare additive manufacturing.

South Korea Drives Bioprinting Innovations and Dental 3D Printing Integration

South Korea continues to strengthen its position in healthcare 3D printing through substantial government initiatives and pioneering research efforts. The South Korean Ministry of Health and Welfare actively supports advanced dental 3D printing adoption, with approximately 61% of dental patients expressing preferences for custom-printed solutions due to improved comfort and precision. Policy-driven funding has accelerated the modernization of dental practices, significantly increasing the use of additive manufacturing in dental clinics nationwide.

Notably, South Korea has established itself as a global leader in bioprinting breakthroughs, exemplified by the successful transplantation of a 3D-printed windpipe bioengineered from patient-derived cells in 2023. Research institutions continuously advance the development of functional bioprinted tissues, exploring sophisticated techniques for regenerating cartilage and brain tissue, demonstrating South Korea’s cutting-edge capabilities. The nation’s robust research infrastructure, combined with strong governmental backing, continues to foster groundbreaking healthcare innovations, firmly positioning South Korea as an international leader in 3D bioprinting technologies.

Israel’s High-Tech Ecosystem Drives Healthcare 3D Printing Market Growth

Israel’s dynamic high-tech industry significantly fuels its healthcare 3D printing sector, underscored by rapid market expansion and extensive innovation. Valued at USD 221.4 billion in 2024, Israel’s additive manufacturing market increasingly focuses on customized healthcare solutions, particularly in orthopedics, which emerged as the largest and fastest-growing segment, generating approximately USD 3.29 million in revenue in 2024. Strong clinical adoption, particularly within medical and surgical centers, further underscores Israel’s proactive integration of 3D printing into everyday medical practice.

Active research in bioprinting, Israel’s largest technological segment within healthcare 3D printing, reinforces the nation’s emphasis on material innovation for improved medical device durability, customization, and patient outcomes. Israeli healthcare providers continue to explore advanced 3D printing applications for patient-specific prosthetics and surgical tools, leveraging extensive industry-academic partnerships and government support. Israel's vibrant innovation ecosystem and targeted investments solidify its role as a pivotal global hub for healthcare additive manufacturing.

Canada Advances Global Healthcare Accessibility Through 3D Printing Initiatives

Canada plays an increasingly influential role in global healthcare 3D printing through strategic institutional integration and humanitarian initiatives. A 31% increase in in-house 3D printing labs within Canadian healthcare institutions highlights robust domestic adoption, particularly in rapid prototyping for prosthetics and orthotics. Charitable initiatives such as the Victoria Hand Project exemplify Canada’s global impact, actively providing highly engineered 3D-printed prosthetic arms to amputees worldwide, significantly improving healthcare accessibility in underserved regions.

Additionally, Canadian researchers and entrepreneurs actively investigate innovative applications of additive manufacturing in medical simulations, patient-specific medical devices, and essential hospital equipment. Canada’s distinctive healthcare system structure fosters unique collaborations and research endeavors, continuously addressing specific healthcare challenges and driving advancements in personalized medicine. These integrated efforts position Canada prominently in the global healthcare additive manufacturing landscape, fostering technological growth and enhancing patient care outcomes internationally.

3D printing in healthcare Market Report Scope

3D printing in healthcare Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.2 Billion

|

|

Market Size (2034)

|

$48.2 Billion

|

|

Market Growth Rate

|

17.6%

|

|

Segments

|

By Component (Systems (3D Printers), Materials, Software & Services), By Technology (Droplet Deposition, Photopolymerization, Laser Beam Melting, Electron Beam Melting (EBM), Three-Dimensional Printing (3DP)), By Application (Medical, Dental, Biosensors, External Wearable Devices, Clinical Study Devices), By End User (Hospitals & Surgical Centers, Dental & Orthopedic Clinics, Academic Institutions & Research Laboratories, Pharmaceutical & Biotechnology Companies, Medical Device Companies, Clinical Research Organizations)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3D Systems Corporation, Materialise NV, Stratasys, Formlabs Inc., EnvisionTEC (now part of Desktop Metal), General Electric, Renishaw plc, EOS GmbH, Protolabs, Organovo Holdings, Inc., Cellink (focus on bioprinting), Aspect Biosystems Ltd., Cyfuse Biomedical, Allevi, Inc., regenHU Ltd., Desktop Metal Inc., HP Development Company, L.P., SLM Solutions Group AG, Oxford Performance Materials, Inc., LimaCorporate, Konica Minolta

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

3D printing in healthcare Market Segmentation

By Component

- Systems (3D Printers)

- Materials

- Software & Services

By Technology

- Droplet Deposition

- Photopolymerization

- Laser Beam Melting

- Electron Beam Melting (EBM)

- Three-Dimensional Printing (3DP)

By Application

- Medical

- Dental

- Biosensors

- External Wearable Devices

- Clinical Study Devices

By End User

- Hospitals & Surgical Centers

- Dental & Orthopedic Clinics

- Academic Institutions & Research Laboratories

- Pharmaceutical & Biotechnology Companies

- Medical Device Companies

- Clinical Research Organizations

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in 3D printing in healthcare Market

- 3D Systems Corporation

- Materialise NV

- Stratasys

- Formlabs Inc.

- EnvisionTEC (now part of Desktop Metal)

- General Electric

- Renishaw plc

- EOS GmbH

- Protolabs

- Organovo Holdings, Inc.

- Cellink (focus on bioprinting)

- Aspect Biosystems Ltd.

- Cyfuse Biomedical

- Allevi, Inc.

- regenHU Ltd.

- Desktop Metal Inc.

- HP Development Company, L.P.

- SLM Solutions Group AG

- Oxford Performance Materials, Inc.

- LimaCorporate

- Konica Minolta

* List Not Exhaustive

Research Coverage

This USDAnalytics report provides an in-depth, data-driven analysis of the global 3D printing in healthcare market from 2025 to 2034. The research covers market value, annual growth rates (CAGR), and the critical drivers fueling industry expansion, such as strategic acquisitions, advances in robotics and artificial intelligence, and pioneering breakthroughs in medical bioprinting.

Detailed market segmentation includes analysis by component (3D printers, materials, software & services), technology (photopolymerization, laser beam melting, EBM, droplet deposition), application (medical, dental, biosensors, wearable devices), and end user (hospitals, surgical centers, academic institutions, pharmaceutical & biotech companies, and medical device manufacturers).

The study delivers comprehensive regional insights, spanning North America, Europe, Asia Pacific, South America, and the Middle East & Africa, with country-specific analysis for the United States, China, Germany, Japan, United Kingdom, South Korea, Israel, and Canada.

Competitive landscape coverage features the strategies, product launches, partnerships, and bioprinting advancements of top industry players. This USDAnalytics report also explores the latest trends such as patient-specific 3D-printed instruments, on-demand bioresorbable implants, and the integration of AI with digital health and additive manufacturing offering actionable intelligence and forward-looking perspectives for stakeholders, manufacturers, investors, and healthcare leaders navigating the rapidly evolving 3D printing in healthcare sector.

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.