Market Analysis: Surge of AI and Digital Health Solutions Redefines the Healthcare Mobility Market

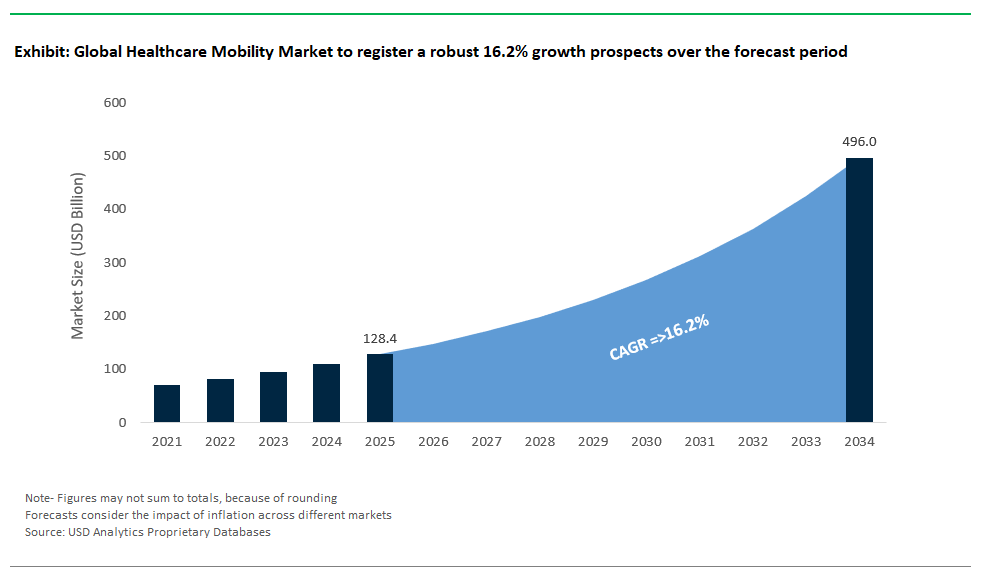

The Global Healthcare Mobility Market Size is estimated at $128.4 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 16.2% to reach $495.9 Billion by 2034.

The Healthcare Mobility Market has entered a new era, powered by rapid advancements in artificial intelligence, strategic acquisitions, and the seamless integration of digital health platforms. October 2025 will see a landmark launch with LOBO EV Technologies Ltd. introducing an AI-powered senior mobility robot. Developed alongside the Jiangsu Research Institute of Dalian University of Technology, this next-generation mobility robot combines advanced safety, mobility, and real-time health-monitoring features such as blood pressure and oxygen tracking into a single, user-friendly solution accessible through mobile apps. This innovation directly addresses the soaring global demand for intelligent elderly care, highlighting how mobile technology is reshaping senior independence and healthcare delivery.

Strategic acquisitions are shaping the competitive landscape in the healthcare mobility market. Sunrise Medical, a global leader in mobility solutions, has notably expanded its reach and expertise through the acquisition of Made for Movement (MfM) in July 2025. This move significantly strengthens Sunrise Medical’s position in neurorehabilitation by adding a suite of therapeutic devices focused on restoring movement for those with complex needs. The company’s commitment to innovation is further underlined by the May 2025 launch of the Empulse M90 Wheel-Add-On, a lightweight, sleek power boost for manual wheelchair users, and the award-winning Empulse R10 Power-Assist Device, which earned “Best Smart Medical Device Technology Product” at the 2025 Future Healthcare Awards in China.

Digital transformation is also accelerating across healthcare delivery. Knipper Health’s acquisition of eBlu Solutions in July 2025 exemplifies this shift, as the integration of eBlu’s extensive specialty provider network and digital platform will streamline therapy initiation and patient support, utilizing advanced mobile and digital services. Meanwhile, WSP Global’s acquisition of Lexica in June 2025 extends its global healthcare advisory capabilities, particularly in digital health infrastructure and mobility strategies for modern healthcare systems.

AI-powered devices are becoming central to the next phase of healthcare mobility. At Computex 2025, ASUS unveiled a suite of innovations including the ASUS VivoWatch with “HealthAI Genie”, the Handheld Ultrasound LU800 featuring AI-assisted imaging, and the forthcoming EndoAim AI-assisted colonoscopy solution. These devices represent a transformative step toward precision diagnostics and personalized care, enabled by real-time mobile data and artificial intelligence.

Major pharmaceutical companies are now directly embracing digital health, marking a fundamental change in patient engagement. The ongoing trend of industry giants such as Eli Lilly, with its LillyDirect platform launched in 2024, highlights how chronic disease management and medication access are shifting to integrated mobile platforms bridging the gap between patients, providers, and therapeutics.

Global partnerships and secure mobile communication are further enhancing healthcare delivery. In March 2024, NetSfere partnered with KPJ Pasir Gudang Specialist Hospital in Malaysia to deploy secure enterprise messaging, streamlining clinical workflows and patient care coordination via mobile devices. Similarly, Sunrise Medical’s October 2024 acquisition of Nuprodx Inc. has expanded its range of assistive bathroom mobility products, providing a comprehensive portfolio of solutions for accessibility and patient independence.

Market Dynamics of Healthcare Mobility Industry

Trend: Integration of Clinical-Grade Wearables for Remote Patient Diagnostics

The healthcare mobility industry is experiencing significant transformation driven by the integration of clinical-grade wearables in remote patient diagnostics, redefining chronic disease management and home-based care. Leading hospital networks in the U.S. and Europe, such as Mayo Clinic and NHS Trusts, notably expanded their remote monitoring capabilities in 2024 by adopting advanced FDA-approved wearable technologies, including ECG patches and continuous glucose monitors. This strategic adoption enables healthcare providers to conduct comprehensive patient evaluations remotely, significantly reducing the frequency of in-person visits and improving overall healthcare efficiency. Recent clinical trials published in reputable medical journals like JAMA (2023) highlight the tangible benefits, revealing that the use of wearable sensors in managing conditions such as heart failure resulted in nearly a 40% decrease in rehospitalization rates compared to traditional care methods.

Further propelling this trend is strong regulatory backing and growing insurance coverage. The U.S. FDA approved over 30 wearable medical devices in 2023 alone, underscoring a heightened regulatory acceptance of these technologies as primary diagnostic tools. Concurrently, expanded reimbursement policies from U.S. Medicare and numerous EU health systems for remote diagnostics conducted through clinical-grade wearables reinforce this market shift. Collectively, these advancements signal a decisive transition toward mainstream adoption of sophisticated wearables, substantially enhancing patient outcomes and alleviating systemic healthcare burdens.

Opportunity: AI-Driven Mobility Solutions for Underserved Rural Populations

A promising opportunity within the healthcare mobility industry lies in the deployment of AI-driven mobility solutions targeted at underserved rural populations, where more than 60 million Americans currently face considerable barriers in accessing specialized healthcare services. AI-powered diagnostic tools, such as smartphone-enabled retinal scanners and telehealth kiosks, represent an innovative approach to bridging these healthcare gaps. Pilot programs in underserved regions like Appalachia have already demonstrated notable success, achieving faster diagnosis times for chronic illnesses like diabetes while considerably reducing per-patient healthcare costs.

Globally, similar initiatives have yielded encouraging results. For instance, India's "eSanjeevani" telemedicine initiative facilitated over 20 million consultations in rural areas by mid-2024, and comparable programs in Brazil and Sub-Saharan Africa are successfully integrating AI-driven decision-support systems to enhance patient triage and referral processes. Studies by leading health organizations, including The Lancet and WHO, report a 15–25% improvement in early disease detection rates for conditions like hypertension and gestational diabetes in regions like rural India and Kenya. Such outcomes underscore AI's potential to significantly expand healthcare accessibility and affordability, ultimately driving better clinical outcomes in rural communities worldwide.

Competitive Landscape: Healthcare Mobility Market

Oracle Health (Cerner) – Cloud-Driven EHR Mobility Integration

Oracle Health, formerly Cerner, is a global leader in healthcare mobility solutions, driving transformation through advanced mobile-enabled Electronic Health Record (EHR) systems and cloud-based platforms. Following Oracle’s $28.3 billion acquisition of Cerner in 2022, the company has integrated Cerner’s EHR solutions with Oracle Cloud Infrastructure (OCI) to deliver scalable, secure, and mobile-accessible healthcare technology. Its portfolio includes Oracle Health EHR Nursing Mobility, enabling clinicians to access patient data, manage workflows, and communicate securely from mobile devices at the bedside or on the move. Features such as secure text messaging through Oracle Health Messenger, mobile-based medication administration using barcode scanning, and real-time event management reduce alarm fatigue and enhance clinical responsiveness. Oracle’s AI-powered analytics and interoperability initiatives are setting new standards for real-time insights and seamless data exchange across healthcare networks. By leveraging AI, cloud security, and mobile-first solutions, Oracle Health positions itself as a frontrunner in next-generation healthcare mobility and digital transformation.

Epic Systems – Deeply Embedded Mobile Ecosystem

Epic Systems is a dominant force in healthcare mobility, offering a deeply integrated ecosystem that empowers clinicians and patients with on-the-go access to critical health information. The company’s flagship patient-facing platform, MyChart, enables users to view medical records, schedule appointments, and conduct telehealth visits via mobile apps. For clinicians, Epic’s Haiku and Canto apps allow real-time access to patient charts, order management, and care coordination directly from smartphones and tablets. Epic’s commitment to interoperability is evident through its Care Everywhere network, which facilitates secure patient data exchange across healthcare organizations, strengthening mobility and continuity of care. Recent innovations include AI-driven decision support tools and a strategic partnership with Microsoft to integrate generative AI capabilities for ambient clinical documentation and workflow automation. These advancements make Epic a leader in mobile healthcare solutions, ensuring efficiency, scalability, and a patient-centered digital experience.

McKesson Corporation – Mobility Through Supply Chain Digitalization

McKesson Corporation plays a pivotal role in healthcare mobility by enabling digital supply chain management and mobile-enabled inventory control within healthcare facilities. Its innovative solutions, such as McKesson ScanManager℠, utilize barcode scanning and mobile interfaces to streamline inventory workflows, reduce manual processes, and improve procurement efficiency. These capabilities are essential for ensuring timely access to critical medical supplies, a fundamental element of healthcare mobility. McKesson’s strategic focus includes investments in automation, AI-powered distribution centers, and real-time digital platforms that support mobile device compatibility, allowing clinicians and administrators to manage ordering and tracking efficiently. Additionally, portfolio optimization through acquisitions like PRISM Vision Holdings demonstrates McKesson’s commitment to technology-driven growth. By combining logistics leadership with mobile technology integration, McKesson strengthens the operational backbone of healthcare systems, ensuring uninterrupted patient care delivery.

Philips Healthcare – Mobility via Connected Care and Portable Devices

Philips Healthcare stands out as a leading innovator in mobility-driven healthcare, offering an extensive range of portable monitoring devices and connected care platforms. Its solutions, such as the IntelliVue MX40 wearable monitor and IntelliVue X3 transport monitor, provide clinicians with continuous patient data during mobility, from bedside to transport scenarios. Philips also pioneers wireless fetal monitoring systems like Avalon, enhancing maternal mobility during labor without compromising safety. The company’s recent launch of the BlueSeal MR Mobile, the world’s first helium-free mobile MRI scanner, represents a groundbreaking step in diagnostic mobility, bringing advanced imaging to underserved locations. Complementing these hardware innovations are AI-enabled imaging platforms and cloud-based telehealth solutions that integrate seamlessly with hospital networks. By combining portability, remote monitoring, and intelligent analytics, Philips Healthcare empowers providers to deliver high-quality care across diverse environments.

Zebra Technologies – Enterprise Mobility Hardware Leader

Zebra Technologies dominates the healthcare mobility hardware segment with rugged mobile computing devices, tablets, barcode scanners, and clinical collaboration platforms designed for demanding healthcare environments. Its HC20 and HC50 mobile computers provide secure communication, barcode-enabled medication verification, and telehealth capabilities, while Zebra’s disinfectant-ready designs ensure durability against frequent sanitization. The company’s ET40-HC and ET45-HC tablets enhance patient engagement and clinician workflows with real-time connectivity powered by Wi-Fi 6 and 5G technology. Zebra’s software suite, including Workcloud Communication and Mobility DNA, complements its hardware offerings by enabling task automation, secure messaging, and advanced power management for full-shift reliability. Recognized at the MedTech Breakthrough Awards, Zebra Technologies continues to lead through innovation in mobile hardware and integrated software, ensuring healthcare organizations achieve seamless clinical mobility and operational excellence.

Market Share and Segmentation Insights: Healthcare Mobility Market

By Product & Service: Mobile Devices Lead, Enterprise Platforms and Apps Drive Rapid Growth

In 2025, mobile devices are projected to account for the largest market share at 41.2%, making them the cornerstone of healthcare mobility solutions. Devices such as smartphones, tablets, and smart wearables are widely adopted across hospitals, clinics, and homecare settings to enable point-of-care documentation, teleconsultations, and real-time vitals tracking. Their seamless integration with clinical systems and portability supports optimized workflows and immediate access to patient records, significantly improving care coordination and responsiveness. Alongside devices, enterprise mobility platforms are gaining substantial momentum, anticipated to grow at a CAGR of 17.6% through 2034. These platforms serve as secure, scalable IT infrastructures that support the increasing demand for HIPAA-compliant and GDPR-aligned solutions, particularly as healthcare providers expand remote workforce capabilities and mobile data interoperability. Notably, mobile applications are also experiencing a rapid surge, especially in telehealth, remote monitoring, and mobile access to EHRs, contributing to their remarkable growth trajectory and shaping patient engagement strategies across the care continuum.

.png)

By End User: Providers Dominate, Patient-Focused Mobility Solutions Accelerate

Healthcare providers, including hospitals, ambulatory care centers, and specialty clinics, represent the largest end-user segment with a 44.8% market share in 2025. Their leadership is driven by the increasing digitization of hospital workflows, mobile access to clinical decision support systems, and seamless EHR integration across mobile platforms. The need for operational efficiency, reduced documentation burden, and improved patient engagement tools fuels the sector’s strong investment in mobility. However, the patient segment is growing the fastest, with a projected CAGR of 18.1% during the forecast period. This growth is powered by the rising use of mHealth apps for chronic disease management, self-care tools, and wearable technologies that enable home-based monitoring and virtual care delivery. The increased emphasis on patient autonomy, real-time feedback, and preventative care contributes significantly to this trend. Meanwhile, payers, including insurance companies and health plans, are leveraging mobile platforms for claims processing, fraud detection, and member engagement, highlighting the expanding role of mobility in administrative transformation across the healthcare ecosystem.

United States Dominates Healthcare Mobility with Robust Investment and Technological Innovation

The United States maintains its global leadership in healthcare mobility, underscored by continuous advancements in scientific innovation and robust financial support. As of June 2025, the nation ranks first worldwide for the regulatory approval of new drugs and medical devices, a position reinforced by active venture capital funding directed toward digital health solutions, telehealth platforms, and remote patient monitoring systems. Throughout 2024, substantial investment from venture capital firms such as those highlighted by Forbes and Axios Pro have propelled healthcare startups, creating an ecosystem ripe for digital innovation. The FDA's clearance of 69 AI-enabled medical devices in 2024 a remarkable 40% increase year-over-year has further boosted healthcare mobility by enhancing diagnostic precision and improving patient management workflows, significantly impacting patient care and accessibility.

Leading healthcare corporations in the U.S. have simultaneously intensified their focus on digital health solutions to enhance patient mobility and healthcare accessibility. Eli Lilly’s launch of LillyDirect in January 2024 has been particularly transformative, allowing patients direct digital access to healthcare providers and home-based medication deliveries. Furthermore, Providence’s introduction of Praia Health in April 2024 has enabled seamless integration of third-party digital health services, effectively scaling mobile healthcare operations within the broader U.S. health ecosystem. Complementing these corporate innovations, governmental support through the Centers for Medicare & Medicaid Services (CMS) has expanded reimbursement policies for telehealth services throughout 2025, actively encouraging healthcare providers to adopt virtual care models. This coordinated combination of private-sector innovation and supportive public policy continues to strengthen the United States' dominant position in the global healthcare mobility market.

China’s Strategic Investments Accelerate Growth in Healthcare Mobility Solutions

China has rapidly emerged as a pivotal market for healthcare mobility, driven by substantial government investment and strategic policy initiatives. The commitment of USD 1.4 trillion toward digital health under China's 14th Five-Year Plan represents a significant national strategy to bolster domestic capabilities in connected-care technologies and mobile healthcare infrastructure. As part of this transformative plan, the government is proactively providing fiscal subsidies and has expedited clinical trial application reviews, slashing the approval timeline from 60 to just 30 working days in key regions. These decisive actions have greatly accelerated product innovation and the market entry of new healthcare mobility solutions, attracting significant foreign and domestic investment into medical devices and digital health sectors.

Further enhancing China’s healthcare mobility landscape, strategic investments in smart hospital infrastructures have leveraged artificial intelligence to optimize patient care delivery, improve resource allocation, and streamline patient flow management. As of June 2025, these AI-driven innovations have positioned China as an attractive destination for global technology providers aiming to participate in its thriving healthcare market. The rapidly expanding Chinese medical tourism sector further illustrates the nation's rising role in cross-border patient mobility, driven by increased adoption of telemedicine and digitally enabled healthcare services. Overall, China's strategic investment and proactive policy frameworks have set the foundation for sustained growth and considerable opportunities in the healthcare mobility domain.

India’s Digital Health Transformation Fuels Rapid Expansion of Mobile Health Services

India is witnessing a substantial transformation in healthcare mobility, primarily driven by government-backed digital health initiatives such as the Ayushman Bharat Digital Mission. By 2025, the ambitious goal of digitally enrolling 1.4 billion citizens into a unified health-record network is expected to significantly increase the demand for interoperable medical devices and mobile healthcare applications nationwide. Complementing this initiative, the government’s eSanjeevani telemedicine program recorded over 216 million teleconsultations by March 2024, highlighting the rapid adoption and normalization of virtual healthcare delivery in India. These programs have markedly improved healthcare access, particularly for patients in rural and underserved areas, demonstrating the direct impact of digital transformation on enhancing patient mobility and healthcare availability.

Additionally, India's growing prominence in the medical tourism market underscores an expanding patient mobility landscape, with notable corporate entries exemplified by EaseMyTrip.com’s strategic investment in healthcare tourism announced in September 2024. Concurrently, Indian healthcare providers have increasingly embraced transformative technologies such as artificial intelligence, the Internet of Things (IoT), and big data analytics, significantly improving care delivery and patient experiences. The government’s targeted investments in digital public infrastructure have been pivotal in facilitating mobile interactions between patients and healthcare providers, further reinforcing the nation’s rapidly expanding healthcare mobility sector and positioning India as an increasingly influential player on the global stage.

Germany Advances Healthcare Mobility Through Digital Health Innovations and Strategic Investments

Germany is at the forefront of European healthcare mobility, driven by dedicated government initiatives and continuous technological innovation. The country’s High-Tech Strategy 2025 specifically highlights "Health and Care" as a critical challenge area, actively supporting research and development efforts in medical technologies and digital healthcare applications. A prime example is the phased rollout of Germany’s Electronic Patient Record (ePA), which, starting January 15, 2025, significantly improves mobile access to patient information and enhances coordination of care. Additionally, the Digital Act, enacted in March 2024, further integrates Digital Health Applications (DiGA) into healthcare processes, significantly boosting transparency and streamlining patient-provider interactions via mobile platforms.

Private-sector innovation complements these governmental initiatives, notably illustrated by Ottobock's June 2024 launch of Juvo B7, an advanced powered wheelchair that exemplifies continued innovation in personal mobility solutions. Germany’s thriving medical technology market, reaching EUR 43 billion in 2023 with steady growth projected through 2025, has solidified the nation’s reputation as a hub of cutting-edge healthcare technology. Additionally, pioneering projects such as "GenAI-Med," backed by the Federal Ministry of Education and Research, are exploring the application of generative AI to medical product approval, further demonstrating Germany’s commitment to accelerating innovation within healthcare mobility.

United Kingdom Scales Healthcare Mobility Through Digital and Virtual Care Expansion

The United Kingdom is significantly enhancing healthcare mobility through dedicated regulatory frameworks and substantial investments in digital health initiatives. The Medicines and Healthcare products Regulatory Agency (MHRA), funded by the Wellcome Trust, launched a three-year project in February 2025 to streamline the regulation and evaluation of digital mental health technologies. These forward-thinking regulatory measures ensure that digital health applications, particularly in mental health, can efficiently reach patients, significantly enhancing mobile healthcare services. Additionally, the NHS has actively scaled up virtual wards and remote monitoring kits, allowing patients to receive clinician-guided care from home, greatly increasing patient convenience and mobility.

Further strengthening the UK's healthcare mobility, substantial investment in digital transformation initiatives has targeted enhanced efficiency and productivity within the healthcare sector, as highlighted in Deloitte's January 2025 healthcare outlook. Government policy support and funding have consistently driven telehealth expansion, acknowledging its crucial role in enhancing patient access to healthcare services while reducing the need for physical travel. Collectively, these initiatives underscore the UK's progressive approach toward healthcare mobility, positioning it as a leader in digitally driven patient care.

Japan’s Aging Population Drives Innovation in Healthcare Mobility Solutions

Japan continues to innovate in healthcare mobility, driven by demographic pressures resulting from its rapidly aging population. High life expectancy and an increasing elderly demographic have prompted significant investment in mobility-oriented healthcare technologies. Yamaha Motor’s January 2025 launch of the JWG-1 wheelchair for domestic and international markets underscores Japan’s proactive approach in developing advanced personal mobility solutions to address aging-related mobility challenges.

Government reforms further encourage innovation, aiming to control healthcare spending through home-based and mobile care solutions, increasing out-of-pocket payments for affluent elderly patients, and shifting care away from hospitals. These measures are complemented by national initiatives aimed at improving Japan’s innovation framework and fostering startup growth within the healthcare sector. By addressing aging pressures with technology-driven solutions, Japan remains a critical market for innovations that support healthcare mobility.

Sweden Leads the Nordics in Advanced Mobility and Assistive Technologies

Sweden maintains a leading position within the Nordic region through continuous innovation and investment in healthcare mobility and assistive technologies. The country's advanced welfare model places a strong emphasis on independent living for elderly and disabled populations, creating substantial domestic demand for specialized mobility solutions. In line with this focus, Etac AB launched the R82 Chilla pediatric buggy in September 2024, specifically designed to cater to complex patient mobility needs. This launch underscores Sweden's ongoing commitment to pioneering highly specialized assistive products, thereby reinforcing the nation's reputation for innovative healthcare mobility solutions tailored to diverse user groups.

Complementing Etac AB’s advancements, Permobil Holding AB remains a prominent global leader specializing in powered mobility devices, consistently investing in next-generation products through 2024 and 2025. Their advanced solutions, aimed at addressing complex mobility needs, have solidified Sweden’s position in the global assistive technology market. Moreover, Swedish manufacturers continue to significantly influence the international assistive devices sector, benefiting from strong governmental support and favorable regulatory frameworks. Sweden’s strategic focus on technological excellence, supported by academic and government initiatives, ensures sustained growth and international competitiveness within healthcare mobility markets, further establishing the nation as a key innovation hub in Europe.

South Korea’s Aging Population and Government Initiatives Boost Healthcare Mobility Growth

South Korea has rapidly become a leading nation in healthcare mobility, significantly driven by its rapidly aging population, which ranks among the fastest-growing elderly demographics globally. The pressing demand for continuous monitoring, remote diagnostics, and mobile healthcare solutions has encouraged significant government investments in telehealth infrastructure and electronic health record (EHR) systems. The Ministry of Science and ICT reported over a 15% year-on-year increase in healthcare technology investments by late 2024, underscoring a booming environment ripe for tech-driven healthcare solutions aimed at mobility enhancement.

The telemedicine segment remains particularly robust in South Korea, reflecting extensive adoption and flexible regulatory measures established during the pandemic, further solidifying the nation’s commitment to mobile health services. Additionally, smart wearable devices including fitness trackers, smartwatches, and continuous glucose monitors are widely integrated into both clinical and wellness applications, underscoring the prominence of mobile health adoption in daily patient care. These developments demonstrate South Korea’s strategic alignment of demographic necessities and technological advancements, positioning the nation as an attractive market for companies aiming to capitalize on opportunities in smart healthcare mobility solutions.

Healthcare Mobility Market Report Scope

Healthcare Mobility Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$128.4 Billion

|

|

Market Size (2034)

|

$495.9 Billion

|

|

Market Growth Rate

|

16.2%

|

|

Segments

|

By Products and Services (Mobile Devices, Mobile Applications, Enterprise Mobility Platforms), By Application (Enterprise Solutions, mHealth Applications), By End User (Payers, Providers, Patients), By Care Setting (Hospitals & Clinics, Home-Care, Ambulatory Services), By Deployment Model (Cloud-based platforms, On-premise solutions)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

McKesson Corporation, Cisco Systems Inc., Zebra Technologies Corporation, Oracle Cerner, Omron Corporation, Koninklijke Philips N.V., AT&T Inc., Stanley Healthcare Solutions, AirStrip Technologies, Microsoft Corporation, Qualcomm Life, Inc., Infosys Limited, IBM Corporation, Wipro Limited, Verizon Communications Inc., Athenahealth, Inc., Cognizant Technology Solutions, Alphabet Inc. (Google), Samsung Electronics Co., Ltd., Medtronic, Abbott Laboratories, Johnson & Johnson, Stryker, GE HealthCare

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Healthcare Mobility Market Segmentation

By Products and Services

- Mobile Devices

- Mobile Applications

- Enterprise Mobility Platforms

By Application

- Enterprise Solutions

- mHealth Applications

By End User

- Payers

- Providers

- Patients

By Care Setting

- Hospitals & Clinics

- Home-Care

- Ambulatory Services

By Deployment Model

- Cloud-based platforms

- On-premise solutions

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Healthcare Mobility Market

- McKesson Corporation

- Cisco Systems Inc.

- Zebra Technologies Corporation

- Oracle Cerner

- Omron Corporation

- Koninklijke Philips N.V.

- AT&T Inc.

- Stanley Healthcare Solutions

- AirStrip Technologies

- Microsoft Corporation

- Qualcomm Life, Inc.

- Infosys Limited

- IBM Corporation

- Wipro Limited

- Verizon Communications Inc.

- Athenahealth, Inc.

- Cognizant Technology Solutions

- Alphabet Inc. (Google)

- Samsung Electronics Co., Ltd.

- Medtronic

- Abbott Laboratories

- Johnson & Johnson

- Stryker

- GE HealthCare

* List Not Exhaustive

Research Coverage

This report delivers a comprehensive analysis of the global healthcare mobility market, with a base year of 2025 and forecasts through 2034. It covers market size, growth rates, and drivers such as AI integration, digital health transformation, and wearable adoption. The scope includes detailed segmentation by products and services (devices, apps, platforms), application (enterprise solutions, mHealth), end user (providers, payers, patients), care setting (hospitals, home-care, ambulatory), and deployment model (cloud-based, on-premise).

Geographic coverage spans North America, Europe, Asia Pacific, South America, and the Middle East & Africa, with dedicated country-level insights for the United States, China, India, Germany, the UK, Japan, Sweden, and South Korea. The report analyzes competitive strategies, recent product launches, acquisitions, and regulatory developments, profiling leading global companies and outlining the latest market trends, opportunities, and challenges shaping the future of healthcare mobility.

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.