High Performance Ceramic Coatings Market Size, Advanced Materials Demand, and High-Temperature Applications Outlook

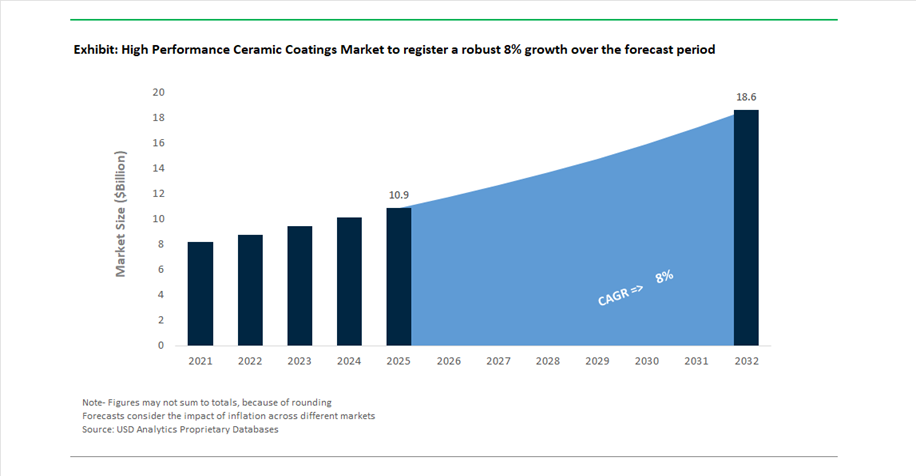

The global high performance ceramic coatings market was valued at $10.9 billion in 2025 and is projected to expand at a robust CAGR of 8% through 2032, reaching $18.7 billion. This accelerated growth trajectory is underpinned by rising demand for thermal barrier coatings (TBCs), environmental barrier coatings (EBCs), and ceramic nanocomposite coatings across aerospace, energy, automotive, and semiconductor industries. These coatings are increasingly critical in enabling high-temperature resistance, corrosion protection, dielectric insulation, and wear resistance in extreme operating environments.

A primary growth driver is the evolution of next-generation gas turbines, hydrogen-ready energy systems, and aerospace propulsion technologies, where ceramic coatings play a pivotal role in improving thermal efficiency and component lifespan. The shift toward higher operating temperatures in jet engines and industrial turbines is directly increasing the adoption of advanced ceramic materials such as ytterbium-disilicate-based coatings and plasma-sprayed ceramic systems. Concurrently, the push for electrification and EV battery safety is expanding the use of ceramic coatings for thermal management, flameproofing, and electromagnetic interference (EMI) shielding.

Additionally, the integration of ceramic-reinforced coatings in architectural and industrial applications is gaining traction, driven by durability enhancement and lifecycle sustainability benefits. Growth in semiconductor manufacturing and microelectronics is also emerging as a high-value opportunity segment, where ceramic coatings serve as dielectric barriers and heat dissipators in precision equipment.

Technology Advancements, Green Coating Shift, and Semiconductor Integration Reshaping Market Dynamics

The high performance ceramic coatings industry is experiencing a significant transformation driven by innovation in deposition technologies, sustainability initiatives, and cross-industry application expansion. In March 2026, Saint-Gobain inaugurated a state-of-the-art production line in Europe for ceramic-based thermal spray powders, specifically targeting environmental barrier coatings (EBCs) for hydrogen-ready gas turbines. This development aligns with the broader energy transition, where high-efficiency turbine systems require advanced ceramic coatings capable of withstanding extreme temperatures and corrosive environments.

Sustainability and performance optimization are also reshaping product development strategies. In January 2026, PPG Industries showcased ceramic-fortified coating formulations at Guangzhou Design Week, emphasizing improved scrub resistance, durability, and reduced lifecycle environmental impact through the use of ceramic nanocomposites. This reflects a growing shift toward low-maintenance, long-life coating solutions in both architectural and industrial segments. Similarly, Bodycote plc, in its April 2025 annual report, formalized its strategic pivot toward “green revenues”, prioritizing HVOF ceramic coatings as REACH-compliant alternatives to hard chrome plating, particularly in aerospace and heavy industrial applications.

Technological innovation in coating application systems is further accelerating market competitiveness. In September 2025, Oerlikon Balzers launched the INVENTA PVD system with Advanced Arc Technology, offering 25% higher loading capacity and enhanced temperature control, which significantly improves coating uniformity and efficiency for automotive components and precision tooling. Meanwhile, Linde’s February 2024 long-term agreement to supply advanced thermal barrier coatings for a major aerospace engine OEM highlights increasing reliance on ceramic coatings to improve fuel efficiency by enabling higher engine operating temperatures.

Emerging applications in electric mobility and microelectronics are also redefining the market landscape. Zircotec’s ElectroHold® ceramic coating range, introduced in September 2024, delivers dielectric insulation, flame resistance up to 1,400°C, and EMI shielding for EV battery enclosures, addressing critical safety challenges in battery design. In parallel, Aremco’s Ceramacast™ enhancements in July 2024 introduced silicate-bonded ceramic coatings with superior thermal shock resistance up to 1,650°C, supporting high-performance sensors and vacuum systems. Furthermore, industry analysis in October 2025 highlighted a strong pivot toward semiconductor applications, where ceramic coatings are increasingly essential for thermal management and electrical insulation in advanced chip manufacturing equipment.

Rare Earth-Doped Zirconate Coatings Advancing Turbine Blade Performance

The high-performance ceramic coatings industry is undergoing a critical material evolution as aerospace manufacturers transition from conventional yttria-stabilized zirconia systems to rare earth-doped zirconates for turbine blade applications. This shift is driven by the need to operate at significantly higher temperatures, particularly beyond 1,200°C where traditional coatings begin to degrade. Rare earth-doped zirconates such as gadolinium zirconate offer substantially lower thermal conductivity, typically in the range of 0.8 to 1.5 W/m·K, enabling improved thermal insulation and allowing turbine inlet temperatures to increase by up to 150°C. This directly contributes to enhanced engine efficiency and reduced fuel consumption. Additionally, these coatings provide improved resistance to calcium-magnesium-alumino-silicate contamination, a major cause of coating failure in high-altitude environments. By forming a protective reaction layer, these coatings prevent structural degradation and extend component lifespan. Another critical advantage is phase stability, as rare earth zirconates maintain structural integrity at temperatures approaching 1,500°C without undergoing the phase transformations that typically lead to cracking in legacy materials. Reduced sintering rates further preserve coating porosity, ensuring long-term strain tolerance under extreme thermal conditions. These performance benefits are positioning advanced ceramic coatings as essential materials in next-generation aerospace propulsion systems.

Yttrium Fluoride Coatings Enhancing Durability in Semiconductor Plasma Etch Systems

The semiconductor manufacturing sector is driving significant demand for advanced ceramic coatings, particularly yttrium fluoride-based systems used in plasma etch chambers. As fabrication processes move toward smaller nodes, including 3 nm and 2 nm technologies, equipment is exposed to increasingly aggressive fluorine-rich plasma environments. Yttrium fluoride coatings are emerging as a superior alternative to traditional yttria and alumina coatings due to their enhanced resistance to plasma-induced erosion. Performance data indicates that yttrium fluoride coatings exhibit erosion rates three to five times lower than alumina under fluorine plasma exposure, significantly extending equipment service intervals. These coatings also contribute to improved process yields by reducing particle contamination, with studies showing approximately 40% reduction in wafer-level defects when yttrium fluoride coatings are used. Surface stability is another key advantage, as these coatings maintain low surface roughness even after prolonged exposure, preventing the flaking of deposited materials that can compromise manufacturing precision. Additionally, yttrium fluoride coatings provide stable dielectric properties, ensuring consistent radio frequency power coupling in plasma systems. These attributes are positioning yttrium fluoride coatings as a critical enabling technology in advanced semiconductor fabrication processes.

US DOE IEDO Programs Driving Adoption of Carbide-Based Ceramic Coatings in Aluminum Recycling

The United States Department of Energy’s Industrial Efficiency and Decarbonization Office is creating strong demand for high-performance ceramic coatings in metal processing applications, particularly in aluminum recycling. The increasing use of secondary aluminum introduces abrasive contaminants such as silica and iron inclusions, which accelerate wear on extrusion dies and tooling systems. Carbide-based coatings, including tungsten carbide-cobalt systems, are being deployed to address these challenges by providing exceptional hardness levels in the range of 1,200 to 1,450 HV. These coatings significantly outperform conventional tool steels, extending operational lifespan and reducing maintenance frequency. Additionally, advanced cermet coatings reduce friction coefficients from approximately 0.6 to 0.2, enabling lower extrusion pressures and improving energy efficiency by 10% to 15%. These performance gains are aligned with federal decarbonization objectives, which aim to reduce energy intensity in industrial processes by at least 25%. The integration of recycled tungsten carbide powders into coating formulations is also supporting circular economy initiatives, reducing reliance on primary raw materials and enhancing supply chain resilience. These factors are positioning ceramic coatings as a key technology in sustainable metal processing and industrial efficiency improvements.

China MIIT Program Driving Adoption of Ceramic Coatings for High-Speed Dry Machining

China’s industrial policy framework is accelerating the adoption of ceramic coatings in high-speed dry machining applications across automotive and aerospace manufacturing sectors. Titanium nitride and aluminum titanium nitride coatings are being designated as critical technologies for enabling machining processes that eliminate the need for liquid coolants. These coatings provide exceptional thermal stability, maintaining hardness at temperatures up to 900°C, which is essential for high-speed cutting operations. The formation of a protective oxide layer at elevated temperatures enhances wear resistance and prolongs tool life, with coated cutting tools demonstrating up to three times longer lifespan compared to uncoated alternatives. Additionally, the low friction characteristics of these coatings reduce the formation of built-up edges during machining, improving surface finish quality and dimensional accuracy. The transition to dry machining is also delivering environmental benefits by reducing hazardous coolant waste by up to 80%, aligning with broader sustainability goals. Government-driven procurement and industrial modernization programs are further accelerating the adoption of these coatings, positioning ceramic coating technologies as a critical enabler of efficient, high-performance manufacturing processes in China.

High Performance Ceramic Coatings Market Share 2025: Thermal Barrier Coatings and Contract Services Drive Growth

Application Type Insights: Thermal Barrier Coatings (TBCs) Lead with High-Temperature Efficiency Gains

The thermal barrier coatings (TBCs) segment dominates the high performance ceramic coatings market with a 42% market share in 2025, driven by its critical role in enabling extreme high-temperature operation and energy efficiency. Typically composed of yttria-stabilized zirconia (YSZ), TBCs are widely used in jet engines and gas turbines, allowing components such as superalloy blades to withstand temperatures exceeding 1500°C. This thermal insulation capability directly enhances fuel efficiency, reduces emissions, and extends component lifespan, making TBCs indispensable in aerospace and power generation sectors. Beyond traditional applications, the growing adoption of electric vehicles (EVs) and hybrid systems is expanding the use of TBCs in exhaust manifolds, turbocharger housings, and battery enclosures for improved thermal management. As industries push for higher efficiency and durability under extreme conditions, thermal barrier coatings will remain the leading application segment in the high performance ceramic coatings market.

Distribution Channel Insights: Contract Coating Services Dominate with Specialized Equipment and Expertise

The contract coating services segment holds the largest 48% share in the high performance ceramic coatings market in 2025, reflecting the high capital investment and technical expertise required for advanced ceramic coating processes. Technologies such as atmospheric plasma spray (APS) and high-velocity oxygen fuel (HVOF) systems involve equipment costs ranging from $500,000 to $2 million, making it impractical for most OEMs to maintain in-house capabilities. As a result, manufacturers increasingly rely on specialized contract coaters for on-demand application of thermal barrier, wear-resistant, and corrosion-resistant ceramic coatings. These service providers offer precise control over critical parameters such as particle velocity, temperature, and spray distance, ensuring optimal bond strength, coating thickness uniformity, and controlled porosity. Additionally, certified contract coating services provide quality assurance and repeatability, which are essential in high-performance applications. As demand for advanced surface engineering grows, contract coating services will continue to dominate the market landscape.

High Performance Ceramic Coatings Market Competitive Landscape: Thermal Barrier Innovation, Aerospace Demand, and Advanced Surface Engineering Driving Growth

The high performance ceramic coatings market is driven by aerospace expansion, industrial durability requirements, and advanced thermal barrier technologies. Key players are focusing on plasma spray coatings, oxide ceramics, and sustainable surface engineering solutions to enhance wear resistance, thermal stability, and lifecycle performance across energy, medical, and semiconductor applications.

Saint-Gobain drives sustainable ceramic coatings growth through infrastructure-focused innovation and global scale

Saint-Gobain S.A. is a leading force in the high performance ceramic coatings market, leveraging sustainability and diversified global operations. The company achieved a 35% reduction in Scope 1 and 2 CO₂ emissions while generating 73% of sales from sustainable solutions, including wear-resistant ceramic coatings. Under its “Lead & Grow” strategy, Saint-Gobain is focusing on non-residential infrastructure and construction chemicals to drive growth. Its enhanced oxide ceramic coatings improve durability and wear resistance in demanding chemical processing and pumping applications. With €46.5 billion in 2025 revenue and balanced regional contributions, the company maintains strong global positioning. This combination of sustainability, innovation, and scale reinforces its leadership in advanced ceramic coatings.

Oerlikon Metco accelerates automation and precision coating technologies for aerospace and EV manufacturing

Oerlikon Metco is strengthening its position in the ceramic coatings market through automation and advanced surface technologies. The company is investing in expanding its Michigan facility to meet rising demand from aerospace and electric vehicle manufacturers. Its Surface Two™ platform integrates IIoT-enabled thermal spray systems, enabling high-volume, automated ceramic coating production. The BALINIT® OPTURA PVD coating offers superior performance for precision drilling in automotive and steel applications. Following the divestment of its Barmag unit, Oerlikon is focusing on high-margin advanced surface solutions and additive manufacturing. This strategic focus enhances its competitiveness in high-performance industrial coating applications.

Praxair Surface Technologies leads aerospace ceramic coatings with advanced plasma spray and thermal barrier systems

Praxair Surface Technologies, part of Linde PLC, is a dominant player in the high performance ceramic coatings market, particularly in aerospace applications. The company holds a leading share in the aerospace segment, supplying coatings for jet engine components exposed to extreme temperatures. Its expanded capacity for industrial gas turbine coatings utilizes zirconia-based formulations that improve thermal shock resistance by 15%. Praxair is also advancing semiconductor coatings with high-purity oxide materials for sub-10 nm fabrication processes. With a significant share in plasma spray technology, it maintains leadership in applying dense, high-quality ceramic coatings. This technical expertise positions Praxair as a key supplier in critical high-temperature applications.

Bodycote strengthens ceramic surface engineering through aerospace expansion and low-carbon processing technologies

Bodycote plc is enhancing its role in the ceramic coatings market through strategic acquisitions and advanced processing technologies. In January 2026, the company expanded its aerospace and defense capabilities through a major acquisition, reinforcing its leadership in thermal processing. Its K-Tech ceramic coatings deliver up to 10x longer operational life for complex geometries, utilizing advanced thermochemical bonding. Bodycote reported £727.1 million in 2025 revenue, with high margins driven by its Specialist Technologies division. The company is implementing low-carbon furnace technologies that reduce emissions by up to 90%, aligning with sustainability goals. This integration of performance and environmental efficiency strengthens its competitive positioning.

APS Materials advances biomedical and aerospace ceramic coatings with plasma spray expertise

APS Materials, Inc. is a specialized leader in high performance ceramic coatings, particularly in biomedical and aerospace applications. The company reported $150 million in annual revenue, driven by strong demand for thermal barrier and medical implant coatings. Its enhanced thermal barrier coatings improve bond strength and reduce thermal conductivity, supporting next-generation turbofan engine efficiency. APS is a key provider of hydroxyapatite coatings for medical implants. Its plasma spray expertise enables precise control of coating density, essential for thermal management in aerospace and space applications. This niche specialization positions APS as a critical supplier in advanced ceramic coating markets.

Aremco expands ultra-high-temperature ceramic coatings for energy and industrial process applications

Aremco Products, Inc. is a niche innovator in the high performance ceramic coatings market, focusing on ultra-high-temperature and chemically resistant coatings. The company expanded its product line in 2026 to include coatings capable of withstanding temperatures above 1,650°C, suitable for industrial furnaces and sensors. Its Ceramacoat™ and Corr-Paint™ series utilize inorganic binders to deliver low-VOC, water-based thermal protection for petrochemical and metal processing industries. With $100 million in 2025 revenue, Aremco maintains a strong position in specialized adhesive and coating solutions. The company is targeting the energy and power sector, which holds a 36% market share, by developing coatings that resist oxidation and carburization. This focus on extreme performance environments reinforces its role as a high-value niche player.

United States High-Performance Ceramic Coatings Market: Aerospace Leadership and PFAS-Free Transition Accelerating Innovation

The United States high-performance ceramic coatings market remains the most advanced and value-driven globally, supported by strong aerospace clusters, semiconductor expansion, and regulatory pressure toward PFAS-free technologies. The execution of the CHIPS and Science Act has catalyzed over $150 billion in private investment as of early 2026, significantly boosting demand for ultra-high-purity ceramic coatings used in semiconductor cleanroom exhaust systems and wafer-handling components. These coatings are critical in maintaining contamination-free environments, positioning ceramic coatings as indispensable in next-generation electronics manufacturing.

Innovation is a defining feature of the U.S. market. The launch of next-generation PFAS-free ceramic-reinforced systems such as Teflon™ EcoElite has set new performance benchmarks for durability and sustainability across industrial and consumer applications. The aerospace sector is also driving demand through the development of ultra-high-temperature ceramics (UHTCs), including hafnium diboride (HfB2) coatings, which are essential for hypersonic vehicles and reusable launch systems. Additionally, federal funding under the Inflation Reduction Act is accelerating the adoption of cool-roof ceramic coatings across the Sun Belt, reducing HVAC energy loads significantly. Regulatory initiatives such as the EPA’s PFAS Strategic Roadmap are further pushing the industry toward sol-gel ceramic coatings, while expansions by major manufacturers are increasing the production of solvent-free nano-ceramic coatings for electric vehicle thermal management applications.

China High-Performance Ceramic Coatings Market: EV Infrastructure Expansion and Semiconductor Localization

China dominates the global high-performance ceramic coatings market in terms of volume, driven by its extensive manufacturing ecosystem and aggressive investments in electric vehicle infrastructure and semiconductor localization. The rapid scale-up of EV production—projected to reach millions of units—has significantly increased the use of ceramic-coated separators and alumina-coated electrode binders, enhancing battery safety and lifecycle performance. This positions ceramic coatings as a critical component in the country’s clean energy transition.

Technological advancements in Chemical Vapor Deposition (CVD) and Physical Vapor Deposition (PVD) are enabling high-precision coatings for automotive and electronics applications. For instance, the development of CVD-coated carbide inserts is improving tool longevity in high-speed machining environments. Government support through the Five-Year Plans is accelerating the adoption of water-based ceramic dispersions and environmentally friendly coating processes. Additionally, the localization of semiconductor manufacturing is driving demand for hybrid ceramic coatings in advanced wafer-processing equipment. The extensive use of ceramic-metallic coatings in power generation infrastructure further highlights China’s leadership in high-temperature industrial applications, while regional manufacturing clusters continue to expand production capacities for silica-based ceramic coatings used in smart city projects.

Germany High-Performance Ceramic Coatings Market: Hydrogen Infrastructure and Circular Economy Driving Sustainable Growth

Germany serves as the innovation hub for high-performance ceramic coatings in Europe, with a strong focus on sustainability, hydrogen infrastructure, and regulatory compliance. The country’s investments in green hydrogen electrolyzers are driving demand for oxide and nitride ceramic coatings that offer exceptional chemical inertness under high-pressure and corrosive conditions. This aligns with broader EU decarbonization goals and positions Germany at the forefront of energy transition technologies.

Circular economy initiatives are also shaping the market, with the commercialization of de-coatable ceramic coatings enabling full material recovery during recycling processes. Strategic expansions by key players are increasing the production of PFAS-free ceramic coatings for consumer appliances, particularly induction-compatible systems. The automotive sector is witnessing growing adoption of plasma-sprayed ceramic coatings in high-voltage EV connectors, enhancing durability and preventing electro-corrosion. Additionally, photocatalytic ceramic coatings are being widely applied in urban infrastructure to reduce NOx emissions, while vacuum-insulated ceramic-glass coatings are supporting energy-efficient building renovations under the EU Net Zero Industry Act.

Japan High-Performance Ceramic Coatings Market: Nano-Ceramic Innovation and Optical Coating Excellence

Japan continues to lead in precision-engineered high-performance ceramic coatings, particularly in nanocomposites and optical applications. The commercialization of nano-ceramic anti-fogging coatings capable of maintaining near-perfect clarity in high-humidity environments is driving demand across medical imaging and automotive sensor industries. This reflects Japan’s strength in developing high-functionality coatings with superior optical and environmental performance.

The country is also advancing display technologies through the development of high-transmittance anti-reflective ceramic coatings for next-generation OLED and foldable devices. Government-backed initiatives are supporting the development of recycled ceramic materials, contributing to a closed-loop system for high-value industrial resources. Innovations such as radiative cooling ceramic coatings are enabling passive heat dissipation for industrial storage systems, reducing energy consumption. Japan’s dominance in optical fiber coatings further reinforces its leadership, with zirconia and alumina-based coatings ensuring high thermal stability in extreme industrial conditions. Investments in magnetron sputtering technologies are also expanding production capabilities for low-emissivity ceramic glass used in building-integrated photovoltaics (BIPV).

India High-Performance Ceramic Coatings Market: Smart Cities Expansion and Electronics Manufacturing Boom

India is rapidly emerging as a high-growth market for high-performance ceramic coatings, driven by government-led industrialization programs and infrastructure modernization. The expansion of the domestic electronics sector, projected to reach $300 billion by 2026, is significantly increasing demand for ceramic-based dielectric coatings used in printed circuit board (PCB) manufacturing. This growth is positioning ceramic coatings as a critical enabler of India’s electronics manufacturing ecosystem.

Defense modernization is another key driver, with increased use of plasma-sprayed thermal barrier coatings in fighter aircraft engines and naval turbines. Government initiatives such as the Jal Jeevan Mission are promoting the use of ceramic-epoxy linings in water infrastructure, ensuring long-term durability and safety. Strategic investments, including large-scale manufacturing hubs, are integrating advanced ceramic surface engineering into telecom and industrial equipment production. The Smart Cities initiative is further accelerating demand for solar-reflective ceramic coatings to mitigate urban heat island effects, while regulatory measures from the Bureau of Indian Standards are ensuring quality compliance and eliminating sub-standard imports.

South Korea High-Performance Ceramic Coatings Market: Solid-State Battery Innovation and Marine Engineering Applications

South Korea is positioning itself as a leader in next-generation energy storage and advanced industrial applications for high-performance ceramic coatings. Significant investments in solid-state battery research are driving the development of ceramic-based electrolyte coatings, which act as critical barriers against dendrite formation and enhance battery safety and efficiency. This innovation is central to the future of high-capacity energy storage systems.

The marine sector is also a key application area, with ceramic-infused anti-fouling coatings being deployed in LNG carriers to protect underwater sensors and structures from biofouling and corrosion. Advances in nanocomposite coatings are enabling superior hardness and durability for foldable OLED devices, supporting the country’s leadership in consumer electronics. Smart factory integration is further expanding the use of conductive ceramic coatings in semiconductor cleanrooms to prevent electrostatic discharge during wafer processing. Additionally, major battery manufacturers are increasingly adopting ceramic thermal management coatings to meet stringent fire safety standards, reinforcing South Korea’s role in high-performance, safety-critical coating technologies.

High Performance Ceramic Coatings Market Report Scope

High Performance Ceramic Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.9 Billion

|

|

Market Size (2032)

|

$18.7 Billion

|

|

Market Growth Rate

|

8%

|

|

Segments

|

By Product (Oxide Coatings, Carbide Coatings, Nitride Coatings, Others), By Technology (Thermal Spray, Physical Vapor Deposition, Chemical Vapor Deposition, Others), By Application Type (Thermal Barrier Coatings, Wear-Resistant Coatings, Corrosion-Resistant Coatings, Electrical Insulation Coatings, Anti-Friction), By End-Use Industry (Aerospace and Defense, Automotive and Transportation, Energy and Power, Industrial Goods and Machinery, Healthcare, Chemical Processing, Electronics and Semiconductors), By Substrate Material (Metals and Alloys, Ceramics and Glass, Polymers and Composites), By Form (Powder-based Coatings, Liquid-based, Gas-phase), By Distribution Channel (Direct Sales, Contract Coating Services, Specialty Chemical)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Oerlikon Metco AG, Saint-Gobain S.A., Linde plc, 3M Company, Bodycote plc, Morgan Advanced Materials plc, APS Materials, Inc., Kyocera Corporation, PPG Industries, Inc., A&A Coatings, Oerlikon Balzers, Aremco Products, Inc., Zircotec Ltd., Keronite Group Limited, Swain Tech Coatings, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High Performance Ceramic Coatings Market Segmentation

By Product

- Oxide Coatings

- Alumina

- Zirconia

- Titania

- Chromia

- Carbide Coatings

- Tungsten Carbide

- Silicon Carbide

- Titanium Carbide

- Nitride Coatings

- Titanium Nitride

- Silicon Nitride

- Aluminum Nitride

- Others

By Technology

- Thermal Spray

- Physical Vapor Deposition

- Chemical Vapor Deposition

- Others

By Application Type

- Thermal Barrier Coatings

- Wear-Resistant Coatings

- Corrosion-Resistant Coatings

- Electrical Insulation Coatings

- Anti-Friction

By End-Use Industry

- Aerospace and Defense

- Automotive and Transportation

- Energy and Power

- Industrial Goods and Machinery

- Healthcare

- Chemical Processing

- Electronics and Semiconductors

By Substrate Material

- Metals and Alloys

- Ceramics and Glass

- Polymers and Composites

By Form

- Powder-based Coatings

- Liquid-based

- Gas-phase

By Distribution Channel

- Direct Sales

- Contract Coating Services

- Specialty Chemical

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in High Performance Ceramic Coatings Market

- Oerlikon Metco AG

- Saint-Gobain S.A.

- Linde plc

- 3M Company

- Bodycote plc

- Morgan Advanced Materials plc

- APS Materials, Inc.

- Kyocera Corporation

- PPG Industries, Inc.

- A&A Coatings

- Oerlikon Balzers

- Aremco Products, Inc.

- Zircotec Ltd.

- Keronite Group Limited

- Swain Tech Coatings, Inc.

*- List not Exhaustive