High Performance Coatings Market Size, Industrial Demand Expansion, and Advanced Coating Technologies Outlook

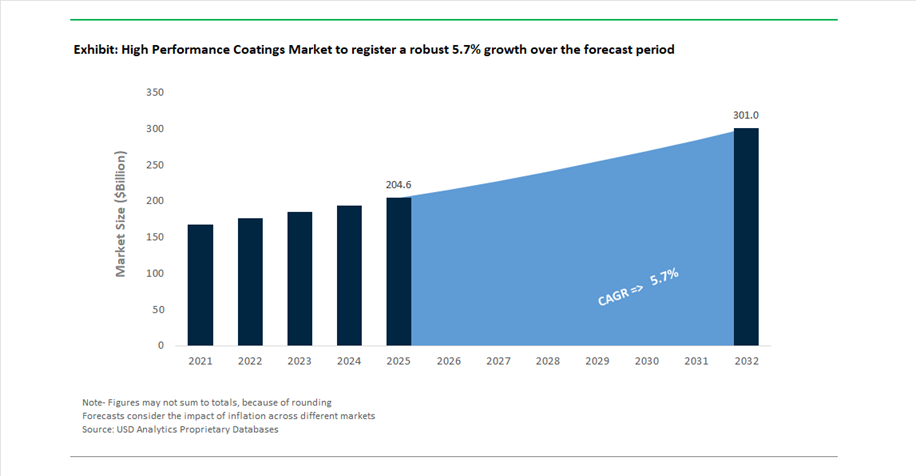

The global high performance coatings market reached a valuation of $204.6 billion in 2025, reflecting its critical role across automotive, aerospace, marine, infrastructure, and industrial protection applications. The market is projected to grow at a CAGR of 5.7% from 2025 to 2032, reaching $301.6 billion by 2032, driven by rising demand for corrosion-resistant coatings, protective coatings, marine coatings, and high-durability architectural coatings.

This expansion is closely tied to the increasing need for long-life asset protection, energy efficiency, and regulatory compliance, particularly in industries operating in harsh environments such as offshore oil platforms, marine vessels, high-rise infrastructure, and aerospace systems. The shift toward low-VOC coatings, waterborne coatings, and bio-based high-performance formulations is accelerating as environmental regulations tighten globally. Additionally, powder coatings and passive fire protection (PFP) coatings are witnessing strong adoption in construction and industrial sectors due to their durability and sustainability advantages.

The market is also benefiting from structural shifts in global infrastructure investment, shipbuilding activity, and electric mobility, where coatings are engineered for thermal resistance, chemical protection, and fuel efficiency optimization. Emerging economies in Asia-Pacific, Latin America, and the Middle East are becoming key demand centers due to rapid industrialization and urban development, while North America and Europe continue to lead in advanced coating technologies, innovation, and regulatory-driven product evolution.

Portfolio Optimization, and Next-Generation Coating Innovations Driving Competitive Dynamics

The high performance coatings industry is undergoing consolidation and strategic repositioning, with major players focusing on high-margin segments, sustainability innovation, and global expansion. A defining development occurred in February 2026, when AkzoNobel and Axalta confirmed an all-stock “merger of equals”, creating a $17 billion coatings powerhouse. This merger is expected to generate $600 million in synergies, particularly strengthening leadership in automotive refinish coatings and industrial high-performance coatings, while reshaping competitive dynamics across global markets.

Leading manufacturers are also optimizing portfolios to focus on core high-performance segments. In January 2026, PPG Industries reported record sales in its Performance Coatings division, driven by double-digit growth in aerospace coatings and protective/marine coatings, and announced $50 million in restructuring savings for 2026, largely through European manufacturing consolidation. Earlier, in December 2024, PPG divested its silica products business to sharpen its focus on liquid and powder high-performance coatings, signaling a broader industry trend toward specialization and margin enhancement.

Strategic realignment is also evident in Hempel A/S’s “Accelerate to Win” strategy, launched in January 2026, which prioritizes marine and infrastructure coatings while reducing exposure to slower-growth oil and gas markets. This shift is reinforced by Hempel’s March 2025 launch of Hempaguard NB, a silicone-hydrogel marine coating that improves vessel efficiency by reducing fuel consumption by up to 6% in the first five years, highlighting the growing importance of performance-driven sustainability in coatings innovation.

Product development continues to advance toward high-efficiency, low-emission, and high-durability coatings. In June 2025, AkzoNobel introduced the Interpon Futura 2025–2028 collection, featuring super-durable powder coatings with bio-based resins and zero VOCs, aligning with global sustainability mandates. Similarly, Jotun’s Hempafire Extreme 100, launched in September 2025, represents a breakthrough in passive fire protection coatings, delivering a 25% reduction in application thickness without compromising fire resistance, which is particularly valuable for high-rise infrastructure projects.

Expansion into emerging markets is another critical growth lever. Sherwin-Williams, in August 2025, leveraged its acquisition of Suvinil to strengthen its industrial coatings footprint in Brazil, while Axalta, in October 2024, established a Refinish Training Centre in South Africa to accelerate adoption of waterborne high-performance coatings in emerging markets. Additionally, Jotun’s May 2024 manufacturing facility in Algeria reflects increasing localization strategies to serve North Africa’s infrastructure boom.

Carbon-Reinforced PEEK Coatings Gaining Adoption in Ultra-Deepwater Oil & Gas Applications

The high-performance coatings industry is undergoing a structural shift as offshore energy operators move into ultra-deepwater environments, requiring materials capable of withstanding extreme pressure, temperature, and chemical exposure. Carbon-reinforced polyether ether ketone coatings are emerging as a preferred solution for subsea connectors and umbilicals, replacing traditional epoxy and metallic systems. These coatings demonstrate exceptional hydrostatic resilience, maintaining structural integrity at depths exceeding 3,000 meters where pressures surpass 300 bar. This results in approximately 40% improvement in fatigue life compared to conventional thermoset coatings. Additionally, PEEK’s inherent resistance to hydrolysis and hydrogen sulfide ensures long-term durability, supporting 25-year operational lifecycles in aggressive offshore environments. The integration of carbon fibers further enhances performance by reducing the coefficient of friction by approximately 25%, improving handling and deployment efficiency in remote-operated subsea operations. Thermal stability is another critical advantage, with PEEK coatings capable of continuous operation at temperatures up to 260°C, meeting the demands of high-pressure, high-temperature reservoirs. These combined properties are positioning carbon-reinforced PEEK coatings as a critical material solution in next-generation deepwater energy infrastructure.

Nano-Boron Nitride Reinforced Polyimide Coatings Advancing EV Motor Efficiency

The rapid evolution of electric vehicle powertrains is driving the adoption of advanced nanocomposite coatings designed to address thermal and electrical performance limitations in high-speed motors. Polyimide coatings infused with hexagonal nano-boron nitride are gaining traction due to their ability to simultaneously enhance thermal conductivity and dielectric strength. The incorporation of nano-boron nitride fillers improves thermal conductivity by 30% to 50%, enabling more effective heat dissipation in high-RPM rotor systems. These coatings also maintain dielectric breakdown strength exceeding 300 kV/mm, ensuring reliability in modern 800V and 900V electric architectures. Thermal stability is another key benefit, with glass transition temperatures reaching up to 400°C, allowing motors to operate at speeds exceeding 20,000 RPM without risk of material degradation. Additionally, the inherent lubricity of boron nitride reduces frictional losses by approximately 15%, directly contributing to improved motor efficiency and energy utilization. These advancements are positioning nanocomposite polyimide coatings as a core technology in high-performance electric propulsion systems.

FAA Mandates Driving Adoption of Polysilazane Ice-Phobic Coatings in Aircraft Systems

The increasing focus on aviation safety and operational efficiency is creating a significant opportunity for advanced hydrophobic coatings, particularly polysilazane-based systems used in aircraft leading edges. These coatings are designed to reduce ice adhesion, a critical factor in preventing performance degradation and safety risks during flight operations. Polysilazane coatings achieve more than 80% reduction in ice adhesion strength compared to untreated composite surfaces, significantly lowering the energy required for de-icing systems. Additionally, these coatings provide self-cleaning properties through high surface energy characteristics, achieving water contact angles above 110 degrees, which helps prevent contamination from debris and insects that can disrupt aerodynamic performance. Durability is another key advantage, with these coatings offering up to five years of resistance to ultraviolet radiation and high-velocity rain erosion at cruise speeds. Environmental compliance is also a critical factor, with modern formulations meeting VOC limits below 250 grams per liter. These attributes are positioning polysilazane coatings as a preferred solution in next-generation aerospace safety systems.

ESA Clean Space Initiatives Driving Demand for DLC Coatings in Satellite Optics

The European Space Agency’s Clean Space program is creating a specialized opportunity for diamond-like carbon coatings in satellite optical systems, where contamination control is critical for mission success. DLC coatings provide an effective barrier against molecular outgassing, reducing contamination of optical surfaces by up to 95% and preserving sensor performance in vacuum environments. Their exceptional hardness, exceeding 2,000 HV, ensures resistance to mechanical damage during assembly and exposure to micrometeoroid impacts in orbit. Optical performance is also maintained, with advanced deposition techniques enabling transmission rates of approximately 98% in the infrared spectrum, making these coatings suitable for high-precision imaging and sensing applications. Additionally, DLC coatings exhibit low thermal expansion, ensuring dimensional stability across extreme temperature fluctuations ranging from minus 150°C to plus 150°C in low Earth orbit. These characteristics are positioning DLC coatings as a critical material solution in advanced space systems focused on durability, precision, and long-term operational reliability.

High Performance Coatings Market Share 2025: Thermal Spray Technology and Direct Sales Drive Industry Adoption

Deposition Technology Insights: Thermal Spray Leads with Versatility and On-Site Application Capabilities

The thermal spray segment dominates the high performance coatings market with a 45% market share in 2025, driven by its exceptional material versatility and application flexibility across industries. Thermal spray technologies, including flame spray, arc spray, and HVOF (high-velocity oxygen fuel), enable deposition of a wide range of materials such as metals, ceramics, carbides, and cermets (e.g., WC-Co, Cr₂O₃) on large and complex components. This makes them ideal for industrial rolls, hydraulic cylinders, bridge bearings, and heavy machinery parts requiring enhanced wear and corrosion resistance. A key advantage is the availability of field-portable thermal spray systems, allowing on-site repair and coating of assets such as power plant turbines, offshore platform risers, and mining equipment, eliminating the need for costly dismantling. As industries demand durable, repairable, and high-performance surface solutions, thermal spray technology will continue to lead the global high performance coatings market.

Sales Channel Insights: Direct Sales Dominate with OEM Collaboration and Supply Reliability

The direct sales segment holds the largest 48% share in the high performance coatings market in 2025, reflecting the increasing need for customized formulations and technical collaboration between manufacturers and end-users. High performance coatings such as fluoropolymer coatings, ceramic-filled epoxies, and PEEK-based systems require precise validation testing, application parameter optimization, and strict quality control, which are best achieved through direct engagement with producers. Industries including aerospace, semiconductor manufacturing, and medical devices rely on these direct partnerships to meet stringent standards such as AS9100 and ISO 13485, ensuring product traceability and regulatory compliance. Additionally, long-term supply agreements enable stable pricing, consistent formulation quality, and priority access to critical materials. As performance requirements and compliance standards become more demanding, direct sales channels will remain the preferred route in the high performance coatings market.

High Performance Coatings Market Competitive Landscape: Advanced Functional Coatings, Sustainable Chemistry, and Infrastructure Demand Driving Market Leaders

The high performance coatings market is highly competitive, driven by demand from aerospace, data centers, EV batteries, and infrastructure. Leading players are focusing on multifunctional coatings, low-VOC formulations, and digital manufacturing integration to enhance durability, compliance, and lifecycle performance across industrial and protective applications.

PPG drives multifunctional coatings innovation with data center solutions and sustainable chemistry leadership

PPG Industries is reinforcing its leadership in the high performance coatings market through advanced multifunctional coating systems and sustainability initiatives. In April 2026, the company launched an end-to-end protective coatings suite for data centers, integrating EMI shielding, antistatic, and heat-reflective properties to reduce cooling demand. With $15.9 billion in 2025 net sales, PPG is focusing growth on high-margin industrial OEM and aerospace sectors following its architectural business divestiture. 44% of its 2026 revenue is derived from sustainably advantaged products, including coatings compliant with IEEE and UL standards. Its MOONWALK® automated paint mixing system, now deployed in 3,000 locations globally, reduces material waste by 15%. This combination of innovation, compliance, and efficiency positions PPG as a leader in next-generation coatings.

AkzoNobel strengthens global dominance through Axalta merger and high-margin protective coatings strategy

AkzoNobel N.V. is reshaping the high performance coatings market through strategic consolidation and portfolio optimization. The company’s planned $25 billion merger with Axalta will create a global coatings leader with $17 billion in combined revenue. It has divested non-core assets, including its Pakistan unit, to focus on high-margin markets in Western and Southeast Asia. Its International® brand remains a benchmark in marine and protective coatings, with innovations targeting low global warming potential solutions and 30-year durability. AkzoNobel achieved a 14.2% adjusted EBITDA margin in 2026, driven by its value-over-volume strategy. This strategic alignment enhances its competitiveness in specialized industrial coatings.

Sherwin-Williams expands infrastructure and data center coatings through scale and distribution strength

The Sherwin-Williams Company is strengthening its position in the high performance coatings market through infrastructure-driven growth and operational scale. The company projects 2026 EPS of $11.50 to $11.90, supported by pricing strategies and a 13.4% increase in adjusted EBITDA. It plans to open 80 to 100 new stores across North America, expanding its reach in residential repaint and infrastructure projects. Its Protective & Marine division is scaling Heat-Flex® and Zinc Clad® coatings, capturing demand from data center and energy infrastructure expansions. With over 5,000 company-operated stores, Sherwin-Williams provides just-in-time delivery and technical support for large-scale projects. This distribution advantage strengthens its leadership in high-performance coatings.

Axalta accelerates EV battery coatings and AI-driven manufacturing efficiency

Axalta Coating Systems is enhancing its competitive position in the high performance coatings market through innovation in EV battery safety and digital manufacturing. In April 2026, the company received multiple Edison Awards for technologies including EcoNextJet™, TintMaster AI, and Alesta® e-PRO FG Black coatings designed to resist ignition and thermal runaway in EV batteries. Its Zencore™ system simplifies coating processes and reduces SKU complexity for high-volume manufacturers. Axalta’s integration of AI into production systems has improved Right-First-Time performance by up to 29%, optimizing operational efficiency. The company is prioritizing coatings capable of withstanding temperatures above 1200°C, addressing safety requirements in electric mobility. This focus on innovation and automation positions Axalta as a key player in advanced coatings.

RPM International strengthens building envelope coatings with acquisitions and performance-driven solutions

RPM International Inc. is expanding its presence in the high performance coatings market through strategic acquisitions and innovative construction solutions. The company reported record Q3 2026 sales of $1.61 billion, reflecting an 8.9% year-over-year increase. Its acquisition of Kalzip GmbH enhances its building envelope portfolio, particularly in aluminum roofing and façade systems. Through its Tremco Construction Products Group, RPM is delivering lightweight, weather-resistant coatings used in major global infrastructure projects. The company’s Margin Achievement Plan supports consistent growth despite market volatility, leveraging strong management capabilities and localized distribution networks. This approach reinforces RPM’s competitiveness in construction and infrastructure coatings.

Kansai Paint strengthens automotive and construction coatings leadership through integration and product innovation

Kansai Paint Co., Ltd. is a dominant player in the high performance coatings market, particularly in the automotive segment. The company benefits from strong vehicle production growth and favorable regulatory conditions such as GST 2.0. Its Excel Everlast 20 coating provides 20-year weather resistance and waterproofing, targeting premium residential applications. Kansai Paint is expanding into construction chemicals and industrial coatings through its amalgamation with Nerofix Private Limited. With EBITDA margins of 13–14%, supported by backward integration, the company ensures quality and cost efficiency in high-end coatings. This diversification strengthens its position across automotive, industrial, and construction segments.

United States High Performance Coatings Market: Advanced Defense Manufacturing and Hydrogen Economy Driving Innovation

The United States high performance coatings market is undergoing a significant transformation, fueled by the reshoring of advanced manufacturing and rapid expansion in defense, aerospace, and hydrogen infrastructure. The execution of the CHIPS and Science Act has mobilized over $160 billion in private investment as of early 2026, leading to a substantial increase in demand for ultra-low-outgassing high performance coatings in semiconductor cleanrooms. These coatings are essential for contamination-sensitive environments, reinforcing their importance in next-generation electronics and chip fabrication.

Innovation and regulatory dynamics are further accelerating market growth. The EPA’s updated TSCA risk evaluation has pushed manufacturers toward PFAS-free coatings and non-chromate primers, aligning with sustainability and safety standards. Technological advancements, including AI-driven coating discovery platforms, are reducing R&D cycles for aerospace-grade thermal barrier coatings, enabling faster commercialization of high-performance solutions. Product innovations such as cryogenic-stable silicone coatings for liquid hydrogen storage and dielectric fire-retardant coatings for EV battery enclosures are expanding application scope across emerging industries. Strategic investments by major players, including new manufacturing facilities, are strengthening domestic supply chains and enhancing the U.S. position in the global high performance coatings market.

China High Performance Coatings Market: Green Manufacturing Mandates and Offshore Energy Expansion

China continues to lead the global high performance coatings market in volume, supported by its extensive industrial base and strong regulatory push toward environmentally compliant technologies. The country is rapidly transitioning to water-based dispersions, UV-curable coatings, and high-solids systems under the “Green Manufacturing” mandate outlined in the Five-Year Plan. This shift is further reinforced by strict VOC regulations under the “Blue Sky” policy, which requires real-time emissions monitoring across industrial zones.

China’s shipbuilding and offshore energy sectors are key growth drivers, with high-solids epoxy and polyurethane coatings widely used to protect large-scale marine structures. Technological advancements such as graphene-enhanced anti-corrosion coatings are extending the lifespan of offshore wind installations in high-salinity environments. Major infrastructure projects, including water diversion systems, are also increasing demand for durable epoxy coatings for large-diameter pipelines. Additionally, China dominates the photovoltaic coatings segment, where PVDF-based formulations are used to protect solar panels from UV degradation in desert environments. This combination of regulatory enforcement, technological innovation, and infrastructure expansion is solidifying China’s leadership in high performance coatings.

Germany High Performance Coatings Market: Hydrogen Infrastructure and Circular Economy Innovations

Germany serves as the European innovation hub for high performance coatings, driven by stringent environmental regulations and strong investments in sustainable technologies. The country is at the forefront of developing advanced coatings for hydrogen infrastructure, including polymer-ceramic hybrid coatings designed to prevent hydrogen embrittlement in pipeline retrofits. This aligns with broader EU initiatives to build a robust hydrogen economy and achieve decarbonization targets.

Sustainability and circular economy principles are central to Germany’s market evolution. The commercialization of de-coatable coatings allows for complete material recovery during recycling, particularly in the automotive sector. Technological advancements such as UV-LED curing systems are reducing energy consumption in manufacturing processes, while bio-based silicone resin binders are replacing petrochemical inputs. Regulatory frameworks like the EU Net Zero Industry Act are also driving demand for energy-efficient coatings, including vacuum-insulated glass coatings for building renovations. Additionally, antimicrobial ceramic coatings are being standardized in medical device manufacturing, further expanding application areas.

India High Performance Coatings Market: Smart Infrastructure Expansion and Industrial Growth

India is rapidly emerging as a high-growth market for high performance coatings, driven by large-scale infrastructure projects and government-led industrial initiatives. The National Infrastructure Pipeline is prioritizing the development of new airports, which are increasingly adopting high-reflectivity coatings to manage heat gain in tropical climates. Simultaneously, the “Sagar Mala” project is boosting demand for corrosion-resistant coatings in maritime infrastructure, particularly for jetty piling and port structures.

The country’s regulatory environment is also evolving, with the Bureau of Indian Standards implementing strict quality control measures that eliminate sub-standard imports and promote domestic manufacturing. Strategic investments by global coating companies, including the establishment of innovation centers, are enhancing localized production capabilities and customization for key sectors such as electronics and automotive. The rapid expansion of metro rail networks is driving the adoption of fire-retardant intumescent coatings, while the growth of the automotive industry is fueling demand for OEM and refinish coatings. These factors collectively position India as a critical growth engine in the global high performance coatings market.

Japan High Performance Coatings Market: Nano-Coatings and Advanced Display Technology Leadership

Japan continues to lead in high performance coatings through its expertise in nanotechnology and advanced materials engineering. The country is setting global benchmarks in precision coatings for electronics, optics, and automotive applications. Innovations such as anti-fogging nano-coatings with near-perfect optical clarity are enhancing the performance of LiDAR and ADAS systems in next-generation vehicles.

Product innovation remains a key strength, with the development of self-healing polyurethane coatings that can repair micro-cracks in consumer electronics, significantly improving durability. Japan is also pioneering radiative cooling coatings, which enable energy-free temperature regulation in buildings, aligning with global sustainability goals. Government support for R&D in recycled fluoropolymer coatings is promoting a circular economy for high-value materials. Investments in magnetron sputtering technology are expanding production of low-emissivity coatings for building-integrated photovoltaics, further strengthening Japan’s leadership in energy-efficient and high-performance coating solutions.

Saudi Arabia High Performance Coatings Market: Oil & Gas Infrastructure and Desalination Driving Demand

Saudi Arabia is emerging as a key market for high performance coatings in the Middle East, driven by large-scale investments in oil & gas, desalination, and infrastructure projects under Vision 2030. The expansion of desalination facilities by the Saline Water Conversion Corporation is significantly increasing demand for high-build epoxy coatings and glass flake linings capable of withstanding harsh saline and high-temperature environments.

Strategic developments in pipeline infrastructure are also boosting demand for advanced coating solutions, including abrasion-resistant overcoats and fusion bonded epoxy systems mandated under updated Saudi Aramco engineering standards. Technological advancements such as predictive maintenance-enabled coatings are enhancing asset reliability by providing real-time corrosion monitoring in desert conditions. Mega-projects like NEOM and “The Line” are driving the adoption of FBE-coated rebar to combat aggressive groundwater conditions. Additionally, investments in green ammonia export terminals are creating new opportunities for specialized coatings designed to protect cryogenic storage systems from chemical degradation.

High Performance Coatings Market Report Scope

High Performance Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$204.6 Billion

|

|

Market Size (2032)

|

$301.6 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Resin Type (Fluoropolymers, Polyurethane, Epoxy, Silicone, Acrylic, Polyester, Specialty Resins), By Coating Technology (Water-borne, Solvent-borne, Powder Coatings, Radiation-Cured, High Solids), By Deposition Technology (Thermal Spray, Physical Vapor Deposition, Chemical Vapor Deposition, Sol-Gel Processing), By Function (Corrosion and Chemical Resistant, Thermal Barrier and Heat Resistant, Wear and Abrasion Resistant, Anti-Fouling and Easy-Clean, Anti-Microbial, Fire Retardant, Electrical Insulation and Conductive), By End-Use Industry (Aerospace and Defense, Automotive and Transportation, Marine and Offshore, Energy and Power Generation, Building and Construction, Industrial Machinery and General Manufacturing, Healthcare and Medical Devices, Electronics and Semiconductors), By Substrate (Metals and Alloys, Concrete and Masonry, Plastics and Composites, Glass and Ceramics), By Sales Channel (Direct Sales, Specialty Chemical Distributors, Industrial Retail)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Axalta Coating Systems Ltd., BASF SE, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Jotun A/S, RPM International Inc., Hempel A/S, Sika AG, Beckers Group, Asian Paints Limited, KCC Corporation, Tnemec Company, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High Performance Coatings Market Segmentation

By Resin Type

- Fluoropolymers

- Polyurethane

- Epoxy

- Silicone

- Acrylic

- Polyester

- Specialty Resins

By Coating Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- Radiation-Cured

- High Solids

By Deposition Technology

- Thermal Spray

- Physical Vapor Deposition

- Chemical Vapor Deposition

- Sol-Gel Processing

By Function

- Corrosion and Chemical Resistant

- Thermal Barrier and Heat Resistant

- Wear and Abrasion Resistant

- Anti-Fouling and Easy-Clean

- Anti-Microbial

- Fire Retardant

- Electrical Insulation and Conductive

By End-Use Industry

- Aerospace and Defense

- Automotive and Transportation

- Marine and Offshore

- Energy and Power Generation

- Building and Construction

- Industrial Machinery and General Manufacturing

- Healthcare and Medical Devices

- Electronics and Semiconductors

By Substrate

- Metals and Alloys

- Concrete and Masonry

- Plastics and Composites

- Glass and Ceramics

By Sales Channel

- Direct Sales

- Specialty Chemical Distributors

- Industrial Retail

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in High Performance Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Axalta Coating Systems Ltd.

- BASF SE

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Jotun A/S

- RPM International Inc.

- Hempel A/S

- Sika AG

- Beckers Group

- Asian Paints Limited

- KCC Corporation

- Tnemec Company, Inc.

*- List not Exhaustive