Market Overview: High Strength Aluminum Alloys Driving Aerospace Efficiency, Automotive Lightweighting & EV Thermal Safety

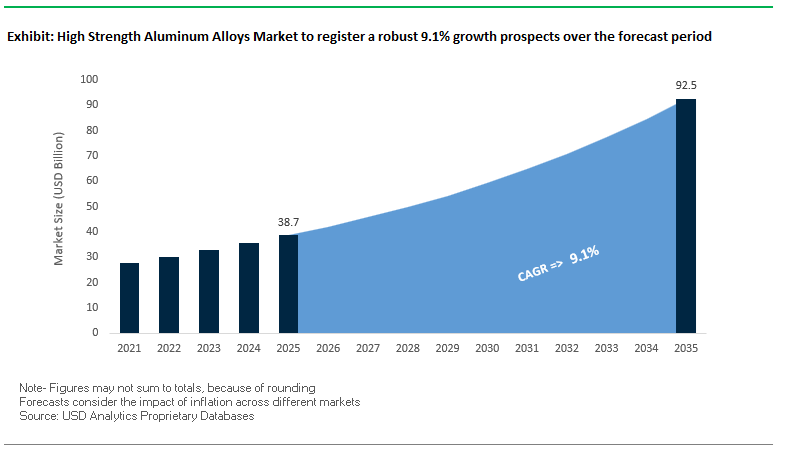

The High Strength Aluminum Alloys Market is projected to grow from USD 38.7 billion in 2025 to USD 92.5 billion by 2035, expanding at a robust CAGR of 9.1%. This growth is driven by their unmatched combination of high tensile strength, lightweighting capability, thermal conductivity, and recyclability, making them crucial materials across aerospace, automotive, EV battery enclosures, construction, and high-performance industrial structures. Manufacturers and alloy developers are increasingly shifting toward high-recycled-content aluminum, lightweight megacasting solutions, and advanced heat-treated alloys to support global decarbonization and vehicle electrification strategies.

Aerospace-grade alloys such as 7075-T6, delivering 540–590 MPa UTS, now rival mild steel in strength while providing dramatically superior strength-to-weight ratios, strengthening their role in fuselage structures, wing components, and landing gear assemblies. Automotive OEMs adopt high-strength aluminum alloys to achieve 30–40% vehicle weight reduction across chassis, closures, crash systems, and engine components—directly improving fuel economy and EV driving range. Meanwhile, EV platforms depend on aluminum battery enclosures offering thermal conductivity nearly 5× greater than steel, enhancing cooling performance and safety under high-load conditions. The transition to circular production models further accelerates demand for alloys containing 90%+ verified recycled content, aligning with OEM sustainability commitments and net-zero material sourcing.

Key Insights for Manufacturers and Alloy Processors

- 7075-T6 aluminum alloys achieve 540–590 MPa UTS, rivaling low-carbon steels while reducing component mass.

- 30–40% lightweighting is achievable in ICE and EV platforms through high-strength aluminum structural components.

- >90% recycled-content alloys are emerging for battery enclosures and crash systems, supporting circular automotive aluminum flows.

- Aluminum battery enclosures offer 5× better thermal conductivity than steel, drastically improving thermal management.

- High-strength alloys remain central to megacasting, EV scaling, aerospace structural redesign, and low-carbon materials adoption.

Market Analysis: Innovation in Megacasting, High-Recycled Content Alloys & Aerospace Growth Driving Market Momentum

The global High Strength Aluminum Alloys market is undergoing a rapid transformation shaped by large-scale automotive casting innovations, rising aerospace demand, decarbonization-focused metal sourcing, and regulatory developments. In October 2025, Alcoa secured its fourth consecutive NADCA Innovation Award for its EZCast™ Alloy, reinforcing the industry shift toward megacasting applications for next-generation automotive bodies. This aligns with its USD 60 million CAD anode baking furnace modernization investment (Oct 2025), ensuring long-term supply of high-quality primary aluminum required for high-strength alloy performance. Additionally, the company announced the permanent closure of the Kwinana alumina refinery (Oct 2025), marking a strategic upstream repositioning toward profitable and low-carbon assets.

Constellium strengthened sustainability-driven alloy development in September 2025 with its £10 million CirConAl project, targeting high-recycled-content extrusion alloys optimized for battery enclosures and crash systems. Earlier, at CES 2024, Constellium showcased Laser-Welded Battery Enclosures designed for EV safety, thermal performance, and structural rigidity. Kaiser Aluminum’s Q3 2025 results showed 41.8 million pounds of Aero/HS product shipments, highlighting strong growth in aerospace and heat-sensitive applications, supported by increased airframe production rates globally. Simultaneously, the January 2024 Indian QCO mandate for aluminum alloy standardization ensures higher local material quality, encouraging OEMs to adopt premium alloys in aerospace and defense manufacturing.

The broader high-performance alloys industry witnessed consolidation with Acerinox’s USD 970 million acquisition of Haynes International (Feb 2024), expanding its presence in high-strength, corrosion-resistant specialty alloys, including aluminum used in extreme environments. Meanwhile, supply chain strategy shifts were observed through Alcoa’s asset optimization efforts, balancing megacasting innovation with low-carbon primary aluminum production.

Breakthrough Trends and Commercial Opportunities Shaping High-Strength Aluminum Alloy Innovation

Market Trend 1: Rapid Qualification of 7xxx-Series Aluminum Alloys for High-Voltage EV Battery Enclosures Requiring Extreme Strength-to-Weight Ratios

The shift toward ultra-high-voltage EV architectures is accelerating the adoption of advanced 7xxx-series aluminum alloys designed to combine exceptional strength with lightweight performance. Next-generation 7xxx alloy compositions now routinely achieve yield strengths above 350 MPa, with cutting-edge proprietary variants reaching 450–552 MPa, outperforming standard 6xxx alloys such as 6063, which typically provide only 214 MPa. This dramatic improvement enables battery enclosure frames—one of the heaviest structural elements in an EV—to meet stringent crashworthiness standards without resorting to heavier steel alternatives.

A major differentiator driving OEM adoption is the specific strength advantage. 7xxx aluminum matrix composites achieve a strength-to-weight ratio of 0.272 MPa·cm³/g, approximately 20% higher than titanium alloy Ti6Al4V (0.202 MPa·cm³/g) despite aluminum’s much lower density (2.86 g/cm³ vs. 4.44 g/cm³). This gives EV designers the dual advantage of structural stiffness and aggressive weight reduction, both critical for extending vehicle range.

These alloys further support high-impact crash energy absorption, ensuring battery modules are protected from deformation or puncture under severe g-force conditions. As EV manufacturers advance toward larger battery platforms and multi-node structural integration, the engineering preference is shifting decisively toward 7xxx alloys that provide aerospace-grade performance at automotive economics, positioning them as the new backbone of high-voltage EV structural systems.

Market Trend 2: Scaling Additively Manufactured Crack-Resistant Aluminum Alloys Like Scalmalloy® for Aerospace Lightweight Structures

A second transformative trend shaping the High-Strength Aluminum Alloys Market is the deployment of additive-manufacturable aluminum systems such as Scalmalloy®, engineered specifically to overcome hot-cracking issues in laser-based metal 3D printing. When processed via selective laser melting (SLM) and properly aged, Scalmalloy® reaches ultimate tensile strengths up to 521 MPa, far exceeding typical AM aluminum alloys like AlSi10Mg (≈300 MPa).

The alloy’s innovation lies in the incorporation of Scandium (Sc) and Zirconium (Zr), which form Al₃(Sc,Zr) nanoprecipitates that refine grains, inhibit hot cracking, and push the recrystallization temperature above 600°C, enabling consistently defect-free builds. Importantly, Scalmalloy® exhibits specific strength parity with Ti6Al4V while being ~40% lighter, giving aerospace OEMs a powerful tool for multi-functional weight reduction.

Even with high strength, Scalmalloy® maintains 12–13% elongation, optimizing it for complex geometries requiring ductility and fatigue tolerance. The alloy’s qualification is expanding across UAV frames, satellite brackets, aircraft interior structural components, and space hardware, reinforcing the market shift toward aluminum alloys purpose-built for additive manufacturing.

Opportunities Driving Next-Generation High-Strength Aluminum Development Across Marine, Offshore and Power Infrastructure

Market Opportunity 1: Emergence of Self-Healing High-Strength Aluminum Alloys for Marine and Offshore Corrosion-Critical Structures

One of the most promising innovation frontiers in high-strength aluminum technologies is the development of self-healing alloys and coatings tailored for marine, offshore, and corrosive industrial environments. Self-repairing systems incorporating healing agents such as methyl methacrylate demonstrate a 22% corrosion rate reduction within just two hours of exposure after mechanical damage, significantly extending coating life in saltwater environments.

Self-healing alloy systems such as Al-Ag also exhibit crack closure during thermal treatment via the transformation of Ag₂Al phases when cooled from 550°C, enabling built-in damage repair at the microstructural level. These intrinsic healing mechanisms reduce crack propagation rates and prolong service life—critical for offshore components where repair access is limited and downtime costs are high.

Additionally, advanced passivating self-healing coatings deliver 40% fewer corrosion-related failures over service life, while next-generation vascular healing networks promise multiple healing cycles, supporting life-extension strategies for offshore wind towers, marine hull structures, and coastal infrastructure. As offshore investments scale, self-healing aluminum systems represent a compelling cost-saving opportunity for long-term materials reliability.

Market Opportunity 2: Commercialization of High-Conductivity, High-Strength Aluminum Alloys for Modern Overhead Power Transmission Lines

Grid modernization and electrification are accelerating demand for high-conductivity, high-strength aluminum alloys capable of supporting increased current loads with lower thermal sag. Emerging Al-Zr and Al-Fe-Si alloy systems are engineered to deliver ≥61% IACS conductivity while maintaining tensile strengths of 159–165 MPa—a performance combination that bridges the gap between hard-drawn aluminum (high conductivity, low strength) and conventional aluminum alloys (moderate conductivity).

Thermal performance is a critical driver: Al-Zr conductors can operate continuously at 150°C, compared to 90°C for traditional aluminum conductors, enabling 15–20% higher current throughput with reduced sag. Moreover, these alloys must retain ≥90% of tensile strength after exposure to 230°C for 1 hour, simulating decades of thermal aging at elevated temperatures.

Even small conductivity gains (e.g., 60% → 61% IACS) translate into measurable reductions in transmission losses, thereby reducing energy waste and associated CO₂ emissions. With grid operators intensifying investment in high-capacity, low-loss conductor technologies, these advanced aluminum systems present a major long-term opportunity in the global transmission infrastructure market.

High Strength Aluminum Alloys Market Share Analysis

Market Share by Alloy Series: 6000 Series (Al-Mg-Si) Leads Due to Unmatched Versatility and Extrusion Dominance

The 6000 Series Aluminum Alloys (Al-Mg-Si), including widely used grades such as 6061, 6063, and 6082, account for the largest market share—approximately 40% in 2025—because they offer the optimal balance of strength, formability, corrosion resistance, and cost efficiency required across both structural and aesthetic applications. Their precipitation-hardening capability allows manufacturers to achieve tensile strengths above 400 MPa while maintaining excellent weldability—an advantage not shared by certain higher-strength 7000 and 2000 series alloys that suffer from post-weld cracking. The 6000 series is also the most extrusion-friendly family of aluminum alloys, enabling high-volume production of complex and lightweight geometries such as EV battery trays, bumper beams, crash-management systems, architectural profiles, and structural tubes. This extrudability significantly lowers manufacturing cost per part, making the 6000 series the preferred alloy family for automotive, construction, machinery, and consumer goods applications. Moreover, their natural corrosion resistance enables long-term performance in outdoor environments without the need for heavy protective coatings. Industry studies frequently show that the 6000 series alone can represent over 70% of aluminum alloy usage in automotive sheet and extrusion applications, underscoring their dominant presence in global high-strength aluminum alloy consumption.

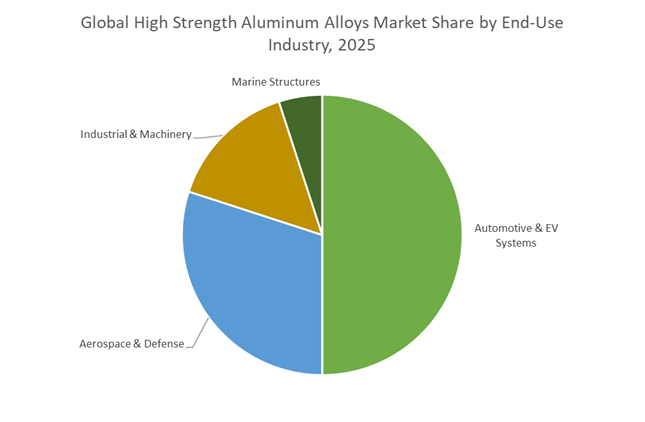

Market Share By End-Use Industry: Automotive & EV Systems Dominate as Lightweighting Becomes a Global Manufacturing Imperative

The Automotive & EV Systems segment holds the largest market share—approximately 50% in 2025—as high-strength aluminum alloys have become essential for meeting regulatory emissions targets, delivering structural efficiency, and enabling the accelerating transition to electric mobility. Aluminum’s high strength-to-weight ratio directly supports lightweighting strategies, reducing vehicle mass to improve fuel efficiency in internal combustion engines and maximize driving range in electric vehicles (EVs). The 6000 series, in particular, has become the material of choice for battery enclosures, where it provides a critical combination of structural rigidity, crash energy absorption, thermal stability, and corrosion resistance. Advanced 6000-series extrusions used in battery housings have demonstrated 15–20% higher crash energy absorption than steel, a decisive performance factor for EV platforms. Additionally, high-strength aluminum alloys are widely integrated into chassis components, space frames, suspension arms, crash rails, and body-in-white structures as automakers shift toward aluminum-intensive designs to meet safety, performance, and sustainability goals. With global EV adoption surging and average aluminum content per vehicle rising year over year, the automotive sector continues to be the single most influential demand driver in the high-strength aluminum alloys market, reinforcing its position as the dominant and fastest-growing end-use segment.

Country Analysis: Strategic High Strength Aluminum Alloy Advancements Across Global Manufacturing Powerhouses

United States: Scandium-Enhanced and Al-Li Alloy Leadership Driving Next-Gen Aerospace and Defense Manufacturing

The United States continues to dominate the High Strength Aluminum Alloys Market, propelled by strong federal backing for defense-grade alloys, Scandium integration, and high-specification material development. In 2025, the U.S. Department of Defense’s $10 million Defense Production Act Title III funding to NioCorp Developments marked a pivotal move to secure a fully domestic Scandium supply chain—essential for producing Al-Sc alloys used in mission-critical aerospace structures. Programs like the F-35 Lightning II incorporate substantial quantities of aluminum-scandium alloys due to their exceptional strength-to-weight ratios, stress resistance, and fatigue durability, extending deep market visibility well into the 2030s.

U.S. industrial capacity is also expanding through significant public and private investment. In August 2025, the government allocated $1 billion across 16 states to enhance aerospace-grade aluminum manufacturing, including melt technologies, rolling lines, and alloy refinement. Companies like Novelis have responded by expanding the Kentucky facility to support surging demand from both EV platforms and commercial aircraft. Meanwhile, U.S. R&D capabilities are advancing rapidly; Elementum 3D’s A5083-RAM5 alloy, developed with Army support, represents a breakthrough in additive manufacturing aluminum—delivering high strength without post-processing heat treatment and opening new possibilities for complex, lightweight defense components.

China: High-Quality Development Plan Accelerating 7000 Series and NEV-Focused Recycled Aluminum Innovation

China is undergoing a structural transformation in the High Strength Aluminum Alloys Market, guided by the national High-Quality Development Implementation Plan (2025–2027). This framework prioritizes breakthroughs in precision alloy processing and mass adoption of 7000 Series, high-toughness, and corrosion-resistant aluminum alloys, specifically for strategic sectors such as aviation, high-speed rail, and electric vehicles. The April 2025 launch of Chalco’s 6B05 automotive alloy sheet marks a major advancement, offering NEV manufacturers a domestically certified lightweighting solution with exceptional crash performance and recyclability—aligning perfectly with China's NEV penetration goals.

China is also accelerating innovation in Additive Manufacturing with companies like Bright Laser Technologies (BLT) releasing high-strength aluminum powders optimized for Laser Beam Powder Bed Fusion (PBF-LB), expanding the nation’s supply capabilities for 3D-printed aerospace housings, battery components, and thermal structures. Furthermore, sustainability mandates require that clean energy usage in electrolytic aluminum capacity exceed 30% by 2027, sharply increasing demand for low-carbon high-strength aluminum alloys from advanced OEMs. These policies and capabilities collectively position China as a global nucleus for high-volume, high-performance aluminum alloy production.

Germany & the European Union: HFQ-Formed, Giga-Cast HSAA and Multi-Material Architecture Reshaping EV Lightweighting

Germany and the wider EU remain technological frontrunners in the High Strength Aluminum Alloys Market, driven by EV mobility mandates, strict emissions legislation, and a mature materials science ecosystem. European OEMs like BMW and Audi are rapidly deploying Multi-Material Architecture (MMA) strategies, integrating giga-cast structural components and HFQ-formed (Hot Form Quench) high-strength aluminum to achieve substantial mass reduction across EV body structures. For example, heat-treated cast aluminum structures used in the 2025 BMW 5 Series demonstrate the region’s commitment to large, lightweight, energy-efficient vehicle platforms.

Sustainability is also a defining advantage for Europe. Companies like Norsk Hydro are achieving significant commercial traction with CIRCAL (75%+ recycled content) and REDUXA (low-carbon aluminum)—two product families that command premium prices due to their verified low CO₂ footprints. Meanwhile, R&D programs such as the FLAMINGo nanocomposite project aim to deliver aluminum systems with up to 45% component weight reduction and improved recyclability. The rapid expansion of HFQ, giga-casting technologies, and low-carbon aluminum brand adoption positions Europe as a global innovation center for designing high-strength alloys suited specifically for EVs and next-generation mobility systems.

Japan: Ultra-Lightweight High Strength Aluminum for Hydrogen Vehicles and Advanced Thermal Management Systems

Japan continues to solidify its leadership in ultra-lightweight high-strength aluminum alloy development, targeting emerging mobility paradigms such as hydrogen vehicles and precision thermal management. A key milestone occurred in July 2025 when Kobe Steel partnered with Toyota to engineer specialized lightweight aluminum alloys capable of withstanding high pressures and hydrogen embrittlement, enabling safer and more efficient storage systems for hydrogen-powered mobility platforms. These alloys support Japan’s national decarbonization strategy and its vision for a hydrogen-based transportation future.

Japanese firms are also advancing high-performance aluminum for thermal management in electric vehicles. In June 2025, UACJ unveiled a new recyclable aluminum alloy optimized for battery enclosure thermal efficiency, significantly enhancing heat dissipation in high-density EV battery packs. Meanwhile, companies such as Nippon Light Metal are strengthening supply chains for critical alloying elements and scaling production of aerospace-grade 7000 Series systems. These developments underscore Japan’s ongoing leadership in precision alloy engineering, particularly for high-temperature, high-pressure, and high-reliability applications.

India: Quality Control Orders Driving Aerospace-Grade Alloy Standardization and Domestic Manufacturing Expansion

India has moved decisively to secure its share of the High Strength Aluminum Alloys Market, implementing strong regulatory mechanisms and industrial investments. The 2025 Quality Control Order (QCO) for aluminum tubes, rods, and bars enforces standardized specifications across domestic production, ensuring consistent quality and alignment with aerospace-grade requirements. This regulatory tightening is foundational for India’s ambition to become a major aerospace materials supply hub.

Simultaneously, India is scaling high-performance aluminum alloy capacity to meet domestic and export demand. Hindalco’s ₹100 crore expansion announced in 2024 reflects rising need for defense, aviation, and EV platforms requiring lightweight structural alloys. India’s Vision 2047, which targets a sixfold increase in aluminum output, emphasizes closed-loop recycling, low-carbon processes, and reduced import dependency—creating long-term momentum for HSAA manufacturing. As India grows into a competitive global supplier of technical alloys, demand for aerospace-grade, heat-treatable, and high-strength aluminum continues to intensify across local and international sectors.

Canada: Green Aluminum Leadership and Scandium-Modified Alloy Development for Advanced Automotive and Aerospace Systems

Canada is increasingly recognized as a global hub for green aluminum production, leveraging abundant hydropower to produce low-carbon, high-strength aluminum alloys that align with OEM sustainability targets in Europe and North America. Canadian low-carbon smelters are essential suppliers for manufacturers seeking verifiable reductions in embedded emissions within automotive body structures, aerospace components, and high-performance industrial products.

The nation is also emerging as a leader in next-generation aluminum alloy innovation. In November 2025, Scandium Canada signed an MoU with Granges Power Metallurgy (GPM) to integrate Scandium-modified aluminum alloys into spray-formed, ultra-light, high-strength metal systems. These alloys enable improved printability, grain refinement, and superior fatigue behavior, making them ideal for additive manufacturing, aerospace panels, EV crash structures, and performance-critical mechanical components. Canada’s dual strengths—clean aluminum production and Scandium-enhanced alloy technology—position it at the forefront of future lightweighting and high-strength metal applications.

Competitive Landscape: Global Leaders Advancing Low-Carbon Aluminum, Aerospace Alloys & Automotive Lightweighting

The High Strength Aluminum Alloys market is shaped by global producers focused on low-carbon metal production, innovative structural casting, high-recycled-content alloy solutions, and aerospace-grade metallurgical precision. Companies differentiate through control over upstream production, recycling dominance, alloy innovation, and integration with EV and aerospace demand cycles.

Alcoa Corporation Prioritizes Low-Carbon Aluminum and Megacasting Innovation

Alcoa maintains strong leadership in high-strength aluminum alloys through its EZCast™ and EcoLum® lines, targeting both automotive megacasting and low-carbon material sourcing. The company is advancing its portfolio with alloys engineered for integrated chassis structures, high-load body components, and automotive thermal systems. Its EcoLum® low-carbon billet positions Alcoa as a preferred supplier for OEMs adopting sustainable metals in North America and Europe. The USD 60 million CAD modernization at the Massena smelter strengthens upstream anode quality, ensuring alloy consistency for aerospace and transportation markets. Additionally, the strategic closure of the Kwinana refinery reflects Alcoa's shift toward profitable, sustainability-aligned assets. Alcoa continues to pioneer structural aluminum technologies that support lightweight vehicle designs and improved EV safety.

Constellium SE Expands High-Recycled Content Alloys for Automotive Lightweighting

Constellium has built a specialized position in automotive lightweighting, supplying high-strength alloys such as HSA6® and Surfalex® to global OEMs. The company’s CirConAl project, a £10 million sustainability initiative, is accelerating the development of low-carbon, high-recycled-content extrusion alloys for EV battery enclosures, crash management systems and structural frames. Constellium's advanced scrap sorting capabilities—including LIBS (Laser-Induced Breakdown Spectroscopy)—enable precise alloy separation and closed-loop recycling for automotive plants. At CES 2024, the company demonstrated cutting-edge lightweight battery enclosures designed for crash resistance and improved thermal performance. Constellium continues to expand its presence in the EV ecosystem through alloy innovation and circular material supply.

Kaiser Aluminum Focuses on Aerospace-Grade Precision and High-Strength Flat-Rolled Products

Kaiser Aluminum remains a leading supplier of aerospace alloys, specializing in Aero/HS products including 2000- and 7000-series sheet, plate and extrusions. Its Q3 2025 shipment volume of 41.8 million pounds highlights robust demand from commercial aerospace, military aircraft and defense applications. The company is investing heavily in modernization at its Trentwood and Warrick facilities, enhancing production efficiency and enabling tight-tolerance alloys for structural components exposed to extreme stress and fatigue loads. Kaiser continues to target high-margin sectors where mechanical performance, fatigue resistance and metallurgical precision are critical. Its strategic alignment with rising global aircraft build rates reinforces strong long-term growth potential.

Novelis Inc. Strengthens Global Leadership in Rolled Products and Recycling Ecosystems

Novelis—part of Hindalco Industries—operates as the world’s largest producer of aluminum rolled products, leveraging proprietary Fusion™ and Advanz™ alloys for automotive body sheets, closures and structural components. The company processes more than 2.2 million metric tons of recycled aluminum annually, giving it a clear advantage in supplying OEMs seeking high-recycled-content aluminum, especially for EV platforms. Its deep integration with global automotive manufacturing makes Novelis the preferred supplier for next-generation vehicles featuring lightweight closures, battery trays and crash structures. Beyond automotive, Novelis supplies sustainable alloys for beverage packaging and consumer electronics, reinforcing its dominance in high-volume recycled aluminum systems.

Norsk Hydro Accelerates Low-Carbon Aluminum and Sustainable Construction Alloys

Norsk Hydro differentiates itself through low-carbon aluminum production, utilizing hydropower to deliver alloy families such as Hydro REDUXA (≤4.0 kg CO₂/kg Al) and Hydro CIRCAL, which contains certified high recycled content. These products support strict ESG standards across the automotive, building and industrial sectors. Hydro’s technologies enable high-strength extrusions for architectural systems, high-rise infrastructure, and EV structural modules. The company's sustainability commitments and premier low-carbon credentials make it a strategic supplier for customers aiming to reduce Scope 3 emissions through material selection.

Kobe Steel (KOBELCO) Advances High-Precision Extrusions and Forgings for Mobility Applications

Kobe Steel leverages deep expertise across steel, copper, and aluminum to supply high-strength extrusions, forgings and rolled products used in Japanese automotive, high-speed rail, and industrial equipment. Its 2000- and 7000-series alloy competence enables production of lightweight structures with high tensile and fatigue strength. Through advanced forming technologies and metallurgical integration, KOBELCO supports the development of multi-material joints, hybrid structures and precision components increasingly required in electric mobility platforms. Its vertically integrated approach provides predictable quality and supply stability for demanding engineering applications.

High Strength Aluminum Alloys Market Report Scope

High Strength Aluminum Alloys Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$38.7 Billion

|

|

Market Size (2035)

|

$92.5 Billion

|

|

Market Growth Rate

|

9.1%

|

|

Segments

|

By Alloy Series (2000 Series, 5000 Series, 6000 Series, 7000 Series, 8000 Series), By Product Form (Plates & Sheets, Extrusions, Forgings, Bars & Rods, Powders), By Temper (Annealed, Strain Hardened, Solution Heat-Treated & Naturally Aged, Solution Heat-Treated & Artificially Aged), By End-Use Application (Aerospace & Defense, Automotive & EV Systems, Industrial & Machinery, Marine Structures)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Constellium, Novelis, Alcoa, Kobe Steel, UACJ, Kaiser Aluminum, CHALCO, Vimetco/ElvalHalcor, Norsk Hydro, Aleris (Novelis), Arconic, Aichach-Hofstetter, Rusal, Precision Castparts, Hulamin

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High Strength Aluminum Alloys Market Segmentation

By Alloy Series

- 2000 Series (Al-Cu)

- 5000 Series (Al-Mg)

- 6000 Series (Al-Mg-Si)

- 7000 Series (Al-Zn-Mg-Cu)

- 8000 Series (Al-Li, Al-Sc, specialty high-strength alloys)

By Product Form

- Plates & Sheets

- Extrusions

- Forgings

- Bars & Rods

- Powders

By Temper

- Annealed (O)

- Strain Hardened (H)

- Solution Heat-Treated & Naturally Aged (T3/T4)

- Solution Heat-Treated & Artificially Aged (T6/T7)

By End-Use Industry

- Aerospace & Defense

- Automotive & EV Systems

- Industrial & Machinery

- Marine Structures

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in High Strength Aluminum Alloys Market

- Constellium

- Novelis

- Alcoa

- Kobe Steel

- UACJ

- Kaiser Aluminum

- CHALCO

- Vimetco/ElvalHalcor

- Norsk Hydro

- Aleris (Novelis)

- Arconic

- Aichach-Hofstetter

- Rusal

- Precision Castparts

- Hulamin.

*- List not Exhaustive

Research Coverage

The High Strength Aluminum Alloys Market research report by USDAnalytics provides an in-depth strategic intelligence framework that this report investigates across value chains, alloy innovations, and end-use transitions in aerospace, automotive, EV, marine, and power infrastructure. It tracks breakthroughs in megacasting, additive-manufacturable alloys, self-healing systems, and high-conductivity conductor grades while offering analysis reviews on capacity shifts, policy-led quality standards, and low-carbon metal sourcing. The study highlights how 6000, 7000, and emerging 8000 series systems are reshaping lightweight structures, thermal management, and circular aluminum flows. With rigorous coverage of technology roadmaps, application-level performance demands, and competitive positioning of global manufacturers, this report is an essential resource for industry professionals, OEM sourcing teams, alloy developers, and investors seeking actionable insights into the future trajectory of high strength aluminum alloys.

Scope Highlights

- Segmentation By Alloy Series – 2000 Series (Al-Cu); 5000 Series (Al-Mg); 6000 Series (Al-Mg-Si); 7000 Series (Al-Zn-Mg-Cu); 8000 Series (Al-Li, Al-Sc, specialty high-strength alloys)

- Segmentation By Product Form – Plates & Sheets; Extrusions; Forgings; Bars & Rods; Powders.

- Segmentation By Temper – Annealed (O); Strain Hardened (H); Solution Heat-Treated & Naturally Aged (T3/T4); Solution Heat-Treated & Artificially Aged (T6/T7).

- Segmentation By End-Use Industry – Aerospace & Defense; Automotive & EV Systems; Industrial & Machinery; Marine Structures.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.ime Frame: Historic data from 2021 to 2025 and detailed forecasts from 2026 to 2034.

- Company Coverage: Analysis and profiles of 15+ leading players, including primary aluminum producers, rolled product leaders, extrusion specialists, and high-performance alloy innovators.