Hull Coatings Market Size, Fuel-Efficiency Imperatives, and Marine Decarbonization Outlook

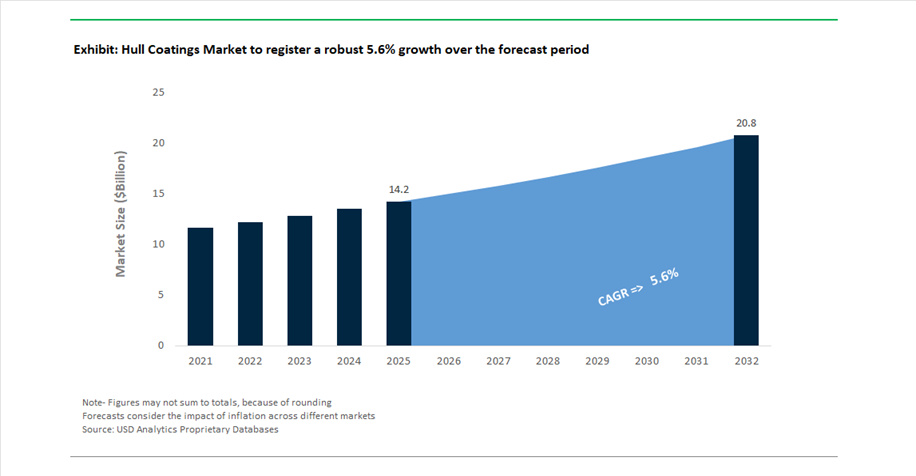

The global hull coatings market was valued at $14.2 billion in 2025 and is projected to reach $20.8 billion by 2032, expanding at a CAGR of 5.6%. This growth is being driven by increasing demand for antifouling coatings, foul-release coatings, marine protective coatings, and high-performance hull coatings that enhance fuel efficiency, vessel durability, and environmental compliance. As shipping operators face tightening decarbonization targets and regulatory mandates such as FuelEU Maritime, hull coatings are transitioning from passive protection solutions to active performance optimization technologies.

A central market driver is the rising focus on biofouling management and drag reduction, which directly impacts fuel consumption and greenhouse gas emissions. Advanced coatings such as silicone-based foul-release coatings, silyl acrylate antifouling coatings, and biocide-free marine coatings are gaining traction due to their ability to maintain smoother hull surfaces and reduce hydrodynamic resistance. Additionally, the integration of long-life coating systems that extend drydocking intervals is becoming critical for shipowners seeking to minimize operational downtime and lifecycle costs.

The market is also benefiting from innovations in sustainable marine coatings, including bio-based epoxy resins and low-VOC formulations, aligning with global environmental regulations. Growth in global shipping, LNG and ammonia carriers, and offshore energy projects is further expanding the demand for specialized hull and ballast tank coatings.

Next-Generation Antifouling Technologies, Strategic Partnerships, and Sustainability-Driven Innovation Reshaping Market Dynamics

The hull coatings industry is undergoing a structural shift toward high-performance, low-friction, and environmentally sustainable coating systems, supported by continuous product innovation and strategic collaborations. In April 2026, Chugoku Marine Paints (CMP) launched BANNOH 1500, a high-solid epoxy universal primer designed to improve shipyard efficiency by enabling faster overcoating across a wide temperature range. This development addresses a key operational challenge in shipbuilding, where reducing coating application time directly enhances throughput and cost efficiency.

Strategic collaborations are expanding the functional scope of hull coatings. In March 2026, AkzoNobel secured a technical endorsement for its Intersleek range for application on advanced hull stabilization fins and interceptors, marking a shift toward specialized hydrodynamic components. Earlier, in December 2025, AkzoNobel entered a large-scale agreement with Winning Shipping to supply Intersleek 1100SR and Intercept 8500 LPP for a multi-vessel drydocking program in China, emphasizing slime-release coating technology to maximize fuel efficiency and emissions reduction.

Sustainability is becoming a defining competitive factor. In July 2025, CMP introduced CMP NOVA 2000 Bio, an ISCC-certified bio-based epoxy resin coating, adopted for a liquefied ammonia tanker—marking a significant step toward low-carbon marine coatings. Similarly, Nippon Paint Marine’s June 2025 partnership with RightShip integrates biocide-free technologies such as AQUATERRAS into global safety and environmental frameworks, reinforcing the shift toward non-toxic antifouling solutions. Supporting this trend, Jotun reported in January 2025 that its hull performance solutions contributed to 11.8 million tonnes of avoided CO₂ emissions, highlighting the role of coatings as carbon reduction enablers.

Technological innovation in antifouling performance is accelerating. CMP’s SEAFLO NEO Z series, launched in May 2025, utilizes advanced silyl acrylate polymers to achieve ultra-low friction surfaces, directly supporting compliance with FuelEU Maritime fuel efficiency mandates. Hempel A/S further advanced the segment with Hempaguard Ultima in March 2025, a silicone-based hull coating system offering up to 120 months of protection, particularly optimized for vessels experiencing extended idle periods. Meanwhile, PPG Industries demonstrated operational innovation through its electrostatic coating application technology, reducing overspray by up to 45%, significantly improving environmental performance during hull maintenance.

Earlier strategic initiatives continue to influence market direction. Nippon Paint Marine’s February 2024 entry into the Global Industry Alliance for Marine Biosafety (GIA) underscores increasing industry focus on biofouling control and invasive species prevention, aligning with global maritime sustainability goals.

Silicone-Based Foul-Release Coatings Replacing Biocidal Antifouling Systems

The hull coatings industry is undergoing a major transition as commercial shipping operators shift away from traditional copper-based antifouling systems toward silicone-based foul-release coatings. This change is driven by tightening environmental regulations and the need to improve vessel efficiency under decarbonization frameworks such as the International Maritime Organization’s Carbon Intensity Indicator. Silicone-based coatings create ultra-smooth, low-surface-energy finishes that significantly reduce hydrodynamic drag, delivering fuel efficiency gains of up to 9% compared to conventional self-polishing copolymer systems. These coatings also maintain surface integrity over extended operational cycles, limiting speed loss to approximately 1.2% over five years, compared to 3% to 5% degradation in traditional coatings due to surface roughening. Adoption is accelerating, with approximately 65% of new commercial vessels incorporating foul-release technologies to meet regulatory performance targets. Additionally, these systems offer extended dry-docking intervals of up to 90 months, reducing maintenance frequency and operational downtime. The combination of environmental compliance, fuel savings, and lifecycle efficiency is positioning silicone-based foul-release coatings as the new standard in commercial marine applications.

Ice-Resistant Hull Coatings Supporting Naval Operations in Polar Environments

The expansion of naval operations in Arctic and sub-Arctic regions is driving the development of specialized ice-resistant hull coatings designed to withstand extreme mechanical and environmental conditions. These coatings utilize reinforced epoxy or vinyl systems incorporating glass platelets or ceramic microspheres to enhance durability under high-pressure ice interactions. Advanced formulations reduce friction against ice surfaces by more than 15%, enabling vessels to maintain operational speed while minimizing structural stress during ice-breaking activities. Mechanical performance is equally critical, with coatings engineered to withstand pressures exceeding 30 megapascals without delamination. Recent innovations also focus on low-temperature curing capabilities, allowing application and repair in environments as cold as minus 5 degrees Celsius, supporting maintenance operations in remote northern shipyards. These coatings are targeting service lifespans of up to 25 years, significantly reducing lifecycle maintenance costs for ice-strengthened vessels. These advancements are positioning ice-resistant coatings as essential materials for naval fleets operating in increasingly strategic polar regions.

US Navy DDG(X) Program Driving Adoption of Biocide-Free Hull Coatings

The United States Navy’s next-generation destroyer program is creating a significant opportunity for advanced hull coatings, particularly biocide-free foul-release systems. Updated naval specifications emphasize the reduction of environmental impact, including a target to reduce copper emissions by at least 50% to meet federal water quality standards. This is driving the adoption of non-toxic coating systems that eliminate the need for biocidal additives while maintaining antifouling performance. In addition to environmental benefits, these coatings offer weight reduction advantages, being up to 70% lighter than traditional multi-layer copper-based systems, which contributes to improved vessel speed and fuel efficiency. Operational performance is also enhanced, with foul-release coatings providing speed gains of 1 to 2 knots at equivalent power output, improving maneuverability and mission readiness. The requirement for extended maintenance cycles, with docking intervals of up to 12 years, further reinforces the need for durable, non-depleting coating technologies. These factors are positioning biocide-free hull coatings as a critical solution in modern naval fleet design and environmental compliance strategies.

China’s Low-Copper Mandate Driving Transition to Sustainable Antifouling Coatings

China’s Green Waterway initiative is creating a large-scale opportunity for environmentally compliant hull coatings by mandating the use of low-copper and copper-free antifouling systems in inland waterways such as the Yangtze River. The regulatory framework restricts the use of high-leach biocidal coatings in sensitive ecological zones, requiring vessel operators to transition to alternative technologies such as silicone-based or advanced polymer antifouling systems. This mandate is impacting a vast fleet of inland vessels, creating a replacement market for tens of thousands of ships. Domestic manufacturers are responding by scaling production of next-generation antifouling coatings, including graphene-enhanced and hydrogel-based systems, with output increasing by approximately 40% in recent years. In addition to environmental objectives, the shift away from copper-based coatings aligns with broader industrial strategies to reduce dependence on imported raw materials. The initiative also targets measurable improvements in water quality, including a 20% reduction in heavy metal accumulation in key port regions. These regulatory and industrial drivers are positioning sustainable hull coatings as a high-growth segment in the global marine coatings market.

Hull Coatings Market Share and Segmentation Insights

Market Share by Product Type: Self-Polishing Copolymer (SPC) Coatings Lead with 45% Share Driven by Fuel Efficiency and Long Service Life

Self-Polishing Copolymer (SPC) coatings dominate the global hull coatings market with a 45% share in 2025, reflecting their superior antifouling performance and lifecycle cost advantages in marine environments. SPC coatings utilize a hydrolyzing polymer matrix that enables controlled and continuous release of biocides such as copper, zinc, and organic boosters, effectively preventing biofouling while maintaining a consistently smooth hull surface. This mechanism significantly reduces hydrodynamic drag, delivering fuel consumption savings of 5 to 15%, a critical economic lever for fleet operators facing volatile fuel costs. Additionally, modern SPC systems are engineered for extended durability, offering protection cycles of 60 to 90 months, thereby reducing dry docking frequency and maximizing vessel uptime. Compared to traditional hard antifouling and epoxy-based systems, SPC coatings provide a self-renewing surface that enhances long-term performance consistency. While silicone-based fouling release coatings and biocide-free technologies are gaining traction under environmental regulations, SPC remains the industry benchmark due to its proven balance of efficiency, durability, and regulatory compliance.

Market Share by Vessel Type: Commercial Vessels Account for 55% Share Fueled by Global Trade and Decarbonization Mandates

Commercial vessels, including cargo ships, tankers, and bulk carriers, represent the largest segment in the hull coatings market with a 55% share in 2025, driven by the scale of global maritime trade and the operational economics of large fleets. These vessels account for over 80% of global shipping tonnage, making hull performance a critical determinant of fuel efficiency and overall operating costs. Even marginal improvements in coating efficiency translate into substantial savings, often reaching millions of dollars per vessel over a five-year operational cycle. Increasing regulatory pressure from the International Maritime Organization (IMO) to reduce CO₂, SOₓ, and NOₓ emissions is further accelerating the adoption of advanced hull coating technologies. High-performance SPC coatings and silicone-based foul release systems are increasingly specified to minimize drag, optimize fuel consumption, and support decarbonization strategies. Additionally, fleet modernization programs and stricter environmental compliance requirements across key shipping regions are driving the replacement of legacy coating systems, reinforcing the dominance of the commercial vessel segment in the global hull coatings market.

Hull Coatings Market Competitive Landscape: Biocide-Free Innovation, Fuel Efficiency, and Decarbonization Driving Maritime Coatings Leadership

The hull coatings market is highly competitive, driven by IMO decarbonization targets, fuel efficiency optimization, and biocide-free antifouling technologies. Leading players are focusing on silicone foul-release coatings, robotic cleaning systems, and low-GWP formulations to reduce drag, emissions, and lifecycle operating costs in global shipping.

AkzoNobel accelerates biocide-free hull coatings and strategic partnerships for fleet decarbonization

AkzoNobel N.V. is a dominant player in the hull coatings market, leveraging its International® brand to lead sustainable marine coatings innovation. The company partnered with Winning Shipping in 2026 to supply coatings for six drydocking projects, targeting a 10% reduction in fleet greenhouse gas emissions. Its Intersleek® 1100SR coating introduces patented slime-release technology, eliminating microfouling resistance without biocides. AkzoNobel has reduced Scope 1 and 2 emissions by 47% since 2018, supported by low-GWP manufacturing processes. Its Intercept® 8500 LPP antifouling system provides high durability for deep-sea vessels through optimized polishing mechanisms. The ongoing $25 billion merger with Axalta is expected to further strengthen its leadership in sustainable performance coatings.

Jotun drives hull performance optimization with robotic cleaning and long-term fuel efficiency guarantees

Jotun A/S is a global leader in hull coatings, delivering advanced solutions focused on operational efficiency and lifecycle performance. The company reported record revenue of NOK 34.33 billion in 2025, supported by strong growth in global maritime trade. Its Hull Skating Solutions (HSS) combines robotic cleaning with SeaQuantum Ultra S coatings, ensuring less than 1.0% speed loss over a 60-month period. Jotun is expanding into emerging markets, including Africa, to capture growing maritime trade routes. Its vertically integrated R&D enables the use of biomass-balanced resins, maintaining strong profitability despite raw material volatility. This combination of innovation and service integration positions Jotun as a leader in performance-driven marine coatings.

Hempel strengthens marine coatings leadership with silicone-based low-friction technologies and emission reduction impact

Hempel A/S is advancing its position in the hull coatings market through high-performance, low-friction coating technologies. The company reported record marine segment sales of EUR 750 million in 2026, driven by strong drydocking and newbuilding activity. Its Hempaguard® coatings have contributed to a reduction of 35.9 million tonnes of CO₂ emissions since 2013 through friction reduction and fuel savings. The introduction of Hempaguard NB enhances performance for newbuild vessels with silicone-based coatings integrated with durable epoxy primers. Hempel’s “Accelerate to Win” strategy aims for a 90% reduction in operational emissions by 2026 through localized production. This focus on sustainability and efficiency strengthens its competitive position in marine coatings.

PPG enhances hull coating efficiency with electrostatic application and carbon-performance partnerships

PPG Industries is strengthening its role in the hull coatings market through advanced application technologies and sustainability partnerships. The company completed its 100th dry docking using electrostatic coating technology, reducing overspray waste by 30% and ensuring consistent film thickness. Its collaboration with RightShip enables shipowners to quantify carbon reduction benefits and improve GHG ratings for regulatory compliance. The PPG SIGMAGLIDE® 2390 coating sets a benchmark in biocide-free foul-release systems, utilizing silicone technology to meet strict EU environmental standards. PPG is also leveraging its MOONWALK® system to optimize color matching and reduce material waste in marine refinish applications. This integration of technology and sustainability enhances its competitiveness in advanced hull coatings.

Nippon Paint Marine advances eco-friendly hull coatings with hydrogel technology and global adoption

Nippon Paint Marine is a key innovator in the hull coatings market, focusing on environmentally safe antifouling technologies. Its AQUATERRAS coating is a biocide-free self-polishing system proven to have zero negative impact on marine ecosystems. The FASTAR solution, incorporating hydrogel water-trapping technology, has been applied to over 1,000 vessels, delivering up to 8% fuel savings per voyage. Under new leadership, the company has achieved a 10% increase in global market share, reflecting strong adoption of its technologies. It also supplied NOA 60 HS coatings for major drydock infrastructure, ensuring uniform application through self-indicating properties. This combination of environmental safety and performance innovation positions Nippon Paint Marine as a leader in sustainable hull coatings.

Chugoku Marine Paints strengthens LNG and ultra-large vessel coatings with ultra-smooth drag-reduction technologies

Chugoku Marine Paints (CMP) is enhancing its position in the hull coatings market through innovation in drag reduction and energy-efficient coatings. The company joined the RightShip Zero Harm Innovation Partners Program in 2026, integrating its coatings into vessel GHG efficiency ratings. Its SEAFLO NEO CF Premium coating delivers an ultra-smooth surface with roughness below 10 microns, significantly reducing drag for ultra-large container ships. CMP is expanding into LNG and LPG carrier segments, providing specialized chemical-resistant coatings. Its expertise in low-temperature curing allows year-round application in challenging climates without additional energy input. This focus on efficiency, sustainability, and niche markets strengthens CMP’s competitive positioning.

South Korea Hull Coatings Market: LNG Leadership and Nano-Type Antifouling Innovation Driving Efficiency

South Korea dominates the global hull coatings market through its leadership in high-value LNG and LPG vessel construction, supported by continuous innovation in nano-type antifouling coatings. The adoption of ultra-smooth nano antifouling paints has significantly enhanced vessel efficiency, enabling measurable reductions in fuel consumption due to minimized hydrodynamic drag. This technological advancement is particularly critical for LNG carriers operating on long-haul routes, where fuel optimization directly impacts operational costs and emissions.

The country’s shipbuilding clusters in Ulsan and Geoje are witnessing strong demand for epoxy-phenolic hull coatings designed for extended immersion cycles, particularly in offshore oil and gas applications. Government-backed initiatives such as the “K-Shipbuilding Strategy” are accelerating the development of low-friction, environmentally compliant coatings to reduce fleet greenhouse gas emissions. Additionally, increased investments in solvent-free marine coatings R&D are enabling manufacturers to meet stringent global VOC regulations. South Korea’s dominance in ballast tank coatings, particularly dual-component epoxy systems, further reinforces its position as a leader in corrosion-resistant marine coatings for harsh operating environments.

Japan Hull Coatings Market: Advanced Foul-Release Systems and Smart Maritime Investments

Japan’s hull coatings market is defined by technological sophistication and strategic government initiatives aimed at capturing high-value segments of the global shipping industry. Innovations such as silicone-based foul-release coatings with dual-protection mechanisms are enabling real-time resistance and release of biofouling organisms, significantly improving vessel efficiency and compliance with environmental standards. These advanced coatings are widely used in merchant fleets to reduce fuel consumption and enhance operational performance.

Government-backed programs such as the JOIN initiative are boosting shipbuilding orders, favoring domestic yards that utilize high-performance Japanese coatings. Technological advancements like hydrogel-based hull coatings are creating water-trapping layers that reduce surface friction and turbulence, optimizing vessel speed and fuel efficiency. Japan’s leadership in eco-modern fleets, combined with expanded coating production capacity in key shipbuilding hubs, is driving demand for specialized coatings such as anti-abrasion systems for ice-class vessels navigating the Northern Sea Route. These innovations position Japan as a global leader in sustainable and high-performance marine coatings.

China Hull Coatings Market: Mega-Yard Dominance and Transition to Biocide-Free Technologies

China continues to lead the global hull coatings market in terms of volume, driven by its unmatched shipbuilding capacity and rapid adoption of environmentally friendly coating technologies. With over half of global ship completions, China has created a massive domestic demand for high-solids epoxy primers and copper-free antifouling coatings. Regulatory updates have restricted the use of certain biocides, accelerating the transition toward organic repellant and biocide-free hull coating systems.

Technological integration is playing a crucial role, with robotic application systems being deployed in major shipyards to enhance efficiency and ensure consistent coating thickness. Strategic partnerships between international coating companies and Chinese shipbuilders are facilitating large-scale deployment of advanced self-polishing coatings on very large crude carriers (VLCCs). Additionally, China’s focus on naval and defense vessel coatings is driving the development of stealth and acoustic-dampening finishes. The expansion of coating services across Belt and Road Initiative ports is further strengthening China’s global footprint in marine coatings and ship maintenance solutions.

Singapore Hull Coatings Market: Global Hub for Autonomous Maintenance and Decarbonization R&D

Singapore has emerged as a global hub for advanced hull coating services, particularly in robotic maintenance, inspection, and decarbonization research. The country is at the forefront of integrating AI-powered autonomous cleaning technologies, enabling large-scale maintenance operations without damaging existing coatings. This innovation is significantly reducing downtime and operational costs for shipowners while maintaining coating performance.

Strong investments in R&D are further enhancing Singapore’s position, with pilot projects demonstrating measurable fuel efficiency gains from graphene-enhanced coatings. The rapid growth of startups focused on robotic inspection and repair technologies is transforming hull maintenance into a highly automated and data-driven process. Singapore’s role as a leading ship-repair hub is also driving increased demand for foul-release coating retrofits, particularly for aging merchant fleets. Regulatory initiatives such as “Green Port” credits are incentivizing the use of low-friction coatings, reinforcing Singapore’s leadership in sustainable maritime solutions.

Norway Hull Coatings Market: Arctic-Grade Protection and Carbon Capture Infrastructure

Norway is a global innovation leader in hull coatings designed for extreme environments, particularly in Arctic and offshore applications. The country’s focus on carbon capture and storage (CCS) infrastructure is driving demand for specialized coatings capable of withstanding extreme temperature gradients during the transport of liquefied CO₂. These coatings are critical for ensuring structural integrity and operational safety in challenging marine conditions.

Advancements in marine coating technology, including silicone-based systems optimized for variable vessel speeds and long idle periods, are enhancing performance across diverse operating conditions. Norway’s offshore wind expansion is also increasing demand for anti-corrosive coatings used in turbine foundations and subsea structures. The development of self-healing coatings that repair surface damage caused by ice or debris is further improving durability and lifecycle performance. Additionally, sustainability initiatives such as the Green Shipping Programme are accelerating the adoption of biocide-free coatings, aligning with environmental regulations in sensitive marine ecosystems like fjords.

United States Hull Coatings Market: Naval Modernization and Graphene-Based Coating Innovation

The United States hull coatings market is evolving rapidly, driven by naval modernization programs and advancements in high-performance coating technologies. Strategic collaborations between industry leaders and maritime organizations are accelerating the adoption of silicone-based foul-release coatings that improve vessel efficiency and reduce maintenance requirements. These coatings are particularly valuable for commercial fleets aiming to comply with stringent environmental regulations.

Defense investments are a major growth driver, with the U.S. Navy prioritizing non-ablative, biocide-free coatings to extend maintenance cycles and improve operational readiness. Product innovation is also advancing, with the commercialization of graphene-modified coatings that offer significantly enhanced durability and resistance to saltwater corrosion. Regulatory frameworks, including initiatives to phase out fluorinated additives, are further shaping market dynamics by promoting environmentally sustainable alternatives. Additionally, expansions in marine coating production capacity are supporting offshore oil and gas infrastructure refurbishment, while specialized thermal barrier coatings are being deployed to improve crew comfort and operational efficiency in coastal patrol vessels.

Hull Coatings Market Report Scope

Hull Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.2 Billion

|

|

Market Size (2032)

|

$20.8 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Product Type (Self-Polishing Coatings, Fouling Release Coatings, Anti-Corrosive Coatings, Hard Antifouling Coatings, Hybrid and Biocide-Free Coatings), By Resin Type (Epoxy, Vinyl Ester, Acrylic, Silicone, Polyurethane, Alkyd), By Vessel (Commercial Vessels, Passenger Vessels, Naval, Offshore Structures and Rigs, Leisure Boats and Yachts, Specialized Vessels), By End-User (New Build, Repair and Maintenance), By Technology (Solvent-borne, Water-borne, Solvent-Free), By Substrate (Steel, Aluminum, Fiberglass, Wood), By Functional Performance (High-Efficiency, Abrasion Resistant, Chemical Resistant, Impact Resistant), By Sales Channel (Direct Sales, Specialty Marine Distributors, Shipyard Service Providers)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AkzoNobel N.V., Jotun A/S, Hempel A/S, PPG Industries, Inc., Chugoku Marine Paints, Ltd., Nippon Paint Marine Coatings Co., Ltd., The Sherwin-Williams Company, Kansai Paint Co., Ltd., KCC Corporation, Axalta Coating Systems Ltd., Boero Bartolomeo S.p.A., RPM International Inc., Subsea Industries NV, Chemco International Ltd., Kop-Coat Marine Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hull Coatings Market Segmentation

By Product Type

- Self-Polishing Coatings

- Fouling Release Coatings

- Anti-Corrosive Coatings

- Hard Antifouling Coatings

- Hybrid and Biocide-Free Coatings

By Resin Type

- Epoxy

- Vinyl Ester

- Acrylic

- Silicone

- Polyurethane

- Alkyd

By Vessel

- Commercial Vessels

- Containerships

- Bulk Carriers

- Crude Oil and Product Tankers

- Chemical Tankers

- Liquefied Natural Gas

- Passenger Vessels

- Cruise Ships

- Ferries and Ro-Ro Vessels

- Naval

- Offshore Structures and Rigs

- Leisure Boats and Yachts

- Specialized Vessels

By End-User

- New Build

- Repair and Maintenance

By Technology

- Solvent-borne

- Water-borne

- Solvent-Free

By Substrate

- Steel

- Aluminum

- Fiberglass

- Wood

By Functional Performance

- High-Efficiency

- Abrasion Resistant

- Chemical Resistant

- Impact Resistant

By Sales Channel

- Direct Sales

- Specialty Marine Distributors

- Shipyard Service Providers

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Hull Coatings Market

- AkzoNobel N.V.

- Jotun A/S

- Hempel A/S

- PPG Industries, Inc.

- Chugoku Marine Paints, Ltd.

- Nippon Paint Marine Coatings Co., Ltd.

- The Sherwin-Williams Company

- Kansai Paint Co., Ltd.

- KCC Corporation

- Axalta Coating Systems Ltd.

- Boero Bartolomeo S.p.A.

- RPM International Inc.

- Subsea Industries NV

- Chemco International Ltd.

- Kop-Coat Marine Group

*- List not Exhaustive