Market Overview: Hydrogen Storage Market Size, System Performance Benchmarks, and Technology Insights

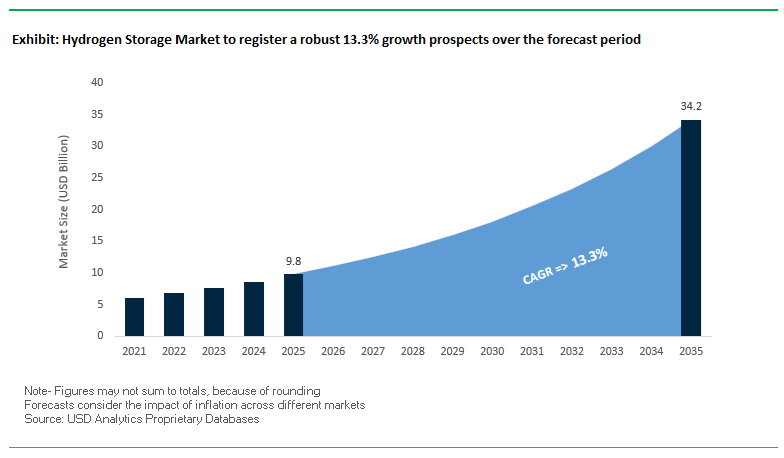

The Hydrogen Storage Market, valued at USD 9.8 billion in 2025, is projected to surge to USD 34.2 billion by 2035, accelerating at a robust CAGR of 13.3% (2025–2035). The market expansion is being driven by rapid decarbonization mandates, large-scale electrolyzer deployments, the commercial rise of fuel cell mobility, and the global shift toward hydrogen-based industrial feedstock. Manufacturers and vendors are increasingly focusing on high-pressure composite vessels, cryogenic storage infrastructure, liquid hydrogen logistics, and solid-state hydrogen materials engineered for enhanced safety, density, and system efficiency. The competitive edge within the hydrogen storage ecosystem now depends on energy efficiency during liquefaction, tank gravimetric density performance, thermal management innovations, and compatibility with emerging hydrogen carriers such as ammonia and LOHCs.

Key Industry Insights

- Type IV 700-bar compressed hydrogen tanks remain essential for achieving competitive FCEV driving ranges above 300 miles.

- The DoE on-board storage target of 1.5 kWh/kg continues to guide material science breakthroughs in advanced solid-state storage.

- Liquid hydrogen systems currently incur a 10–15 kWh/kg liquefaction energy penalty, driving demand for more efficient cryogenic technologies.

- Novel MOF-based adsorbents are proving capable of competitive hydrogen densities at <100 bar, improving safety and cost economics.

- LOHCs like MCH offer ~6.2 wt.% hydrogen capacity, enabling scalable off-board storage using existing fuel infrastructure.

Commercial benchmarks underscore the sector’s advancing technical maturity, with Type IV 700-bar composite tanks now functioning as the standard for light-duty FCEVs, enabling driving ranges exceeding 300 miles. At the same time, research toward the DoE gravimetric target of 1.5 kWh/kg (≈4.5 wt.% H₂) is pushing innovation in solid-state storage, while liquefaction energy penalties of 10–15 kWh/kg remain a cost and efficiency constraint. Emerging materials such as Metal-Organic Frameworks (MOFs) show promise for high-density storage at <100 bar, potentially disrupting both stationary and mobile storage architectures. Meanwhile, Liquid Organic Hydrogen Carriers (LOHCs) like MCH are gaining traction for international hydrogen logistics due to their high volumetric density (~6.2 wt.% H₂) and compatibility with the existing petrochemical supply chain.

Market Analysis: Expansion of Liquefaction Plants, Cross-Border Hydrogen Corridors, and Commercial Storage Deployments (2024–2025)

The global Hydrogen Storage Market experienced transformative shifts between November 2024 and December 2025, characterized by large-scale project financing, liquefaction capacity expansions, aviation-related storage innovations, and strengthened international hydrogen trade partnerships. A landmark development occurred in January 2025, when Plug Power secured a $1.66 billion conditional DOE loan guarantee to build up to six U.S.-based green hydrogen facilities. This funding directly accelerates midstream storage infrastructure, tank farms, and logistics capabilities essential for an integrated North American green hydrogen corridor. Earlier, in July 2024, Shell reached Final Investment Decision (FID) for a 100 MW green hydrogen plant in Germany, incorporating onsite storage and distribution infrastructure to supply its refining operations—signaling heightened investment activity in industrial decarbonization pathways.

Cryogenic storage infrastructure advanced significantly as well. In April 2025, Plug Power commissioned a 15 TPD liquid hydrogen liquefaction plant in Louisiana, increasing its total North American liquefaction capacity to 40 TPD and strengthening the availability of high-purity LH₂ for mobility, aerospace, and material handling applications. Parallel developments validate the rising importance of hydrogen carriers in global trade; in June 2024, Scatec and Fertiglobe secured a 20-year, €397 million ammonia offtake contract through H2Global, reinforcing ammonia’s role as a large-scale hydrogen storage and transport medium. Cross-border hydrogen logistics also gained momentum through the September 2024 UK–Chile Green Hydrogen Partnership, with the UK committing £500 million to support Chilean export infrastructure, including storage and loading terminals.

Distributed storage and modular mobility platforms continue to attract investment. E.ON’s September 2024 announcement of a 20 MW electrolyzer in Essen includes compressed hydrogen storage containers designed for regional trucking distribution hubs. In December 2025, Plug Power entered the space industry through its first Liquid Hydrogen storage and supply contract with NASA, highlighting the growing role of high-purity cryogenic hydrogen systems in aerospace missions. The aviation sector also progressed, with ZeroAvia’s September 2024 Series C extension to $150 million, backed by major airlines and Airbus, supporting the development of lightweight onboard hydrogen storage systems for hydrogen-electric aircraft. Further upstream, Topsoe’s 2025 SOEC factory milestones support high-efficiency hydrogen production, directly catalyzing demand for scalable stationary and mobile hydrogen storage infrastructure.

Breakthrough Trends Advancing Geological and Solid-State Storage for Large-Scale Hydrogen Deployment

Market Trend 1: Large-Scale Expansion of Pressurized Salt Cavern Storage as the Backbone of National Hydrogen Systems

A defining trend in the Hydrogen Storage Market is the rapid global acceleration of pressurized salt cavern storage as nations plan hydrogen backbones to support multi-GW renewable integration, industrial decarbonization, and seasonal energy balancing. Geological assessments show that regions such as the UK possess theoretical storage potential of up to 2,150 TWh, equivalent to nearly four times the projected 2050 national electricity demand—highlighting the sheer scalability of subsurface hydrogen storage compared to surface-based alternatives.

Salt caverns also offer decades of real-world validation. Facilities such as those in Teesside, UK, have safely stored pure hydrogen since the 1970s, providing long-term evidence of containment integrity, minimal permeability, and resilience under cyclic loading. These caverns routinely operate at high pressures of 100–200 bar, which minimizes the recompression penalty when feeding hydrogen into high-pressure pipeline networks or industrial processes.

Importantly, salt caverns exhibit extremely low leakage rates, enabling hydrogen to be stored for months to years—a key requirement for balancing intermittent wind and solar generation. The combination of scalability, low loss rates, and operational maturity positions salt caverns as the cornerstone of future national hydrogen storage architectures, especially in Europe, North America, and the Middle East.

Market Trend 2: Commercial Piloting of Solid-State Hydrogen Storage to Enable Heavy-Duty Mobility Transition

A second transformative trend is the increasing commercialization of solid-state hydrogen storage systems—particularly metal hydrides—for heavy-duty mobility sectors such as freight trucks, rail, and urban transit. Demonstrations led by the U.S. Department of Energy (DOE) and industry partners have achieved rapid refueling of 75.9 kg of hydrogen in 5 minutes 43 seconds, significantly beating the 10-minute heavy-duty vehicle (HDV) refueling target. This achievement proves that high-capacity, fast-fill hydride storage systems are physically and commercially viable.

Solid-state hydrogen storage also provides a major density advantage, achieving volumetric hydrogen densities of 100–130 kg/m³, which is 3× higher than 70 MPa compressed hydrogen (≈40 kg/m³) and nearly 1.8× higher than liquid hydrogen (≈70 kg/m³). This density advantage is crucial for buses, locomotives, and HDVs where onboard space is highly constrained.

These systems further operate at low pressures (0.1–5 MPa) and near-ambient temperatures, eliminating the 70 MPa requirement of gaseous systems and significantly improving safety, system simplicity, and infrastructure compatibility. Ongoing HDV programs are targeting onboard capacities of 60–80 kg, aligning with long-range fleet requirements and accelerating the commercialization of solid-state hydrogen storage as a next-generation mobility enabler.

Strategic Opportunities Enabling Hybrid Refueling Infrastructure and Standardized Storage for Green Steel Manufacturing

Market Opportunity 1: Deployment of Hybrid Storage Architectures for Next-Generation Hydrogen Refueling Stations (HRS)

Hydrogen refueling stations are evolving toward integrated hybrid architectures that combine liquid hydrogen (LH₂), compressed storage, and advanced thermal management technologies. System-level analyses show that LH₂-based stations, which vaporize and compress delivered liquid hydrogen on-site, achieve the lowest equipment footprint, making them ideal for urban or high-throughput HDV hubs.

Simultaneously, optimized on-site production systems—particularly PEM electrolysis using off-peak power and cascade storage banks—have demonstrated the lowest operational cost structure in simulation studies. This combination allows stations to balance capital cost, footprint, and OPEX depending on local grid conditions and hydrogen demand profiles.

The integration of Liquid Organic Hydrogen Carriers (LOHCs) introduces new efficiencies for thermal management. Research prototypes have successfully used molten nitrate salts (NaNO₃–KNO₃) operating at ≈400°C to recover and transfer waste heat from electrolyzers into LOHC dehydrogenation reactors, demonstrating a multi-technology coupling that reduces external heat requirements and improves station efficiency.

Moreover, cascade storage systems, using high-, medium-, and low-pressure banks, ensure sustained filling pressures for rapid fills under 10 minutes—without oversizing compressors. This dynamic response capability is essential for scaling heavy-duty refueling stations designed for fleets, trucks, and long-distance buses.

Market Opportunity 2: Standardization of High-Purity, High-Capacity Hydrogen Storage for Green Steel Production

Hydrogen-based Direct Reduced Iron (H₂-DRI) facilities are emerging as one of the largest future consumers of hydrogen, creating an urgent need for standardized bulk storage, material specifications, and purity management. A typical 1 million tpa DRI plant consumes 50–70 kg of hydrogen per tonne of iron, equating to 50,000–70,000 tonnes of hydrogen per year—a scale unmatched by mobility or power sectors. This industrial demand cannot be met without robust bulk storage systems capable of delivering continuous, stable hydrogen flows.

Purity is another critical requirement. Hydrogen used in DRI must be extremely pure, as contaminants such as moisture and carbon oxides can poison reduction reactions or damage downstream equipment. Therefore, storage systems must minimize contamination risk across compression, pipelines, tanks, and caverns.

Operating compatibility also matters: DRI reactors function at 400–900°C and 1–5 bar, necessitating storage systems that deliver hydrogen at stable, controlled temperatures and pressures to ensure uninterrupted reduction kinetics.

Finally, the shift to high-purity hydrogen infrastructure demands industry-wide standardization of pipeline and storage materials due to hydrogen embrittlement, which reduces fatigue life in conventional carbon steel. This requirement is driving innovation in alloy development, coating technologies, and composite storage materials to support reliable, long-term hydrogen delivery for the global green steel industry.

Hydrogen Storage Market Share Analysis

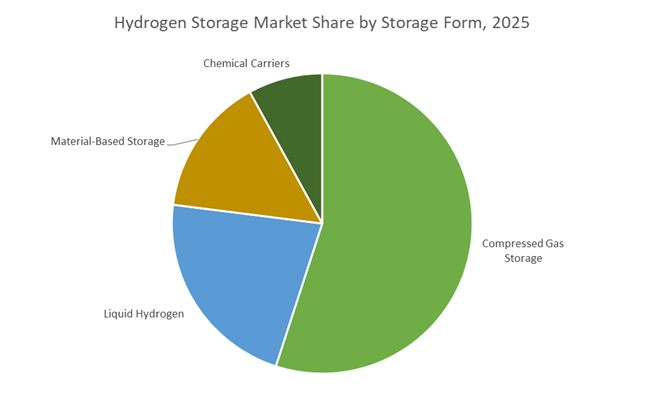

Market Share by Storage Form: Compressed Gas Storage Dominates Commercial and Mobility Deployments

Compressed gas storage accounts for the largest share of the hydrogen storage market—approximately 55% in 2025—reflecting its technological maturity, high reliability, and seamless alignment with current hydrogen mobility and industrial infrastructure. As the most established storage method, compressed gas systems benefit from globally standardized engineering protocols for 350-bar and 700-bar pressure vessels, enabling consistent manufacturing quality, safer operations, and faster adoption across commercial supply chains. Their prominence is further underscored by their central role in Fuel Cell Electric Vehicle (FCEV) platforms, where Type III and Type IV carbon-fiber composite tanks deliver high gravimetric efficiency while maintaining stringent safety thresholds. This storage form supports driving ranges exceeding 300–450 miles, making it indispensable for passenger cars, public transit buses, and long-haul commercial fleets transitioning to zero-emission solutions. Beyond transportation, compressed gas systems are cost-efficient relative to cryogenic technologies and are easier to scale for decentralized hydrogen production sites, industrial users, refueling stations, and pilot hydrogen hubs. As global hydrogen strategies prioritize rapid infrastructure deployment and practical near-term solutions, compressed gas storage continues to lead the market due to its optimal balance of cost, safety, performance, and integration readiness.

Market Share by Application: Transportation Sector Leads High-Pressure Hydrogen Storage Demand

The transportation sector holds the largest application share—around 40% in 2025—driven by accelerating global efforts to decarbonize mobility across commercial and public transportation networks. Hydrogen storage is fundamental to the growth of FCEVs, particularly in heavy-duty trucking, long-haul logistics, buses, and emerging hydrogen-powered rail and maritime applications, where battery-electric systems face limitations in range, payload, and charging time. High-pressure storage at 700 bar has become the industry benchmark for mobility solutions, enabling rapid refueling in 3–10 minutes and supporting operational continuity for fleet operators. This segment’s leadership is reinforced by aggressive policy incentives, national hydrogen roadmaps, and multi-billion-dollar investments in hydrogen refueling corridors across Europe, China, Japan, South Korea, and North America. Automotive OEMs and truck manufacturers are expanding their FCEV portfolios, directly increasing demand for advanced composite pressure tanks and onboard hydrogen storage modules. While industrial hydrogen consumption remains significantly higher in volume, the transportation sector represents the fastest-growing application area for hydrogen storage technologies, driven by high-performance requirements, infrastructure rollout, and the global shift toward zero-emission commercial mobility.

Country Analysis: Global Drivers in Hydrogen Storage Innovation

United States: Large-Scale Salt Cavern Projects, Federal Hydrogen Funding, and Mobility Storage Advancements

The United States is rapidly solidifying its leadership in the global Hydrogen Storage Market through unprecedented federal investment and a coordinated national strategy focused on large-scale infrastructure deployment. Driven by the Bipartisan Infrastructure Law and the Inflation Reduction Act, the U.S. is channeling billions into clean hydrogen production, geological storage, mobility applications, and transmission systems. A landmark development is the Advanced Clean Energy Storage (ACES) project in Utah, which secured a $504.4 million DOE loan guarantee to pair 220 MW of electrolysis capacity with two massive 4.5 million-barrel salt caverns—one of the largest dedicated hydrogen storage initiatives worldwide. These caverns will support the Intermountain Power Project (IPP Renewed), demonstrating the viability of subsurface hydrogen storage at multi-gigawatt scale.

Federal support directly impacts commercialization: the DOE’s March 2024 announcement of up to $6 billion for 33 decarbonization projects includes more than $1 billion for hydrogen, accelerating the build-out of centralized and distributed storage networks for hard-to-abate industries. The HFTO Multi-Year Program Plan (MYPP) released in May 2024 further outlines the roadmap for long-duration storage systems, advanced compression, liquefaction, and conversion technologies. Hydrogen storage for mobility is another area of rapid innovation, backed by a $71 million DOE award to 27 projects in January 2024, including $10.5 million specifically aimed at hydrogen engine and composite tank development. New IRS guidance for the Clean Hydrogen Production Tax Credit (45V) adds long-term financial certainty for green hydrogen production, requiring a proportional rise in storage infrastructure across power, manufacturing, and transport sectors.

European Union & Germany: LOHC Commercialization, Salt Cavern Pilots, and Continental Hydrogen Backbone Storage

Germany and the wider European Union are emerging as global torchbearers for scalable hydrogen logistics, particularly in the fields of Liquid Organic Hydrogen Carriers (LOHC) and geological cavern storage. In October 2025, Hydrogenious LOHC Technologies advanced the commercialization of LOHC systems by awarding the FEED and EPCM contract for the world’s largest hydrogen release plant in Bavaria, demonstrating technical maturity for carrier-based bulk hydrogen transport. This milestone aligns with the EU’s broader hydrogen strategy, which received a structural boost in February 2024 when the European Commission approved the Hy2Infra IPCEI, unlocking major public funding for hydrogen pipelines, compression systems, and long-duration storage infrastructure.

Germany is simultaneously expanding its subsurface hydrogen capabilities. Uniper’s 2024 salt cavern pilot aims to evaluate long-term storage integrity, optimizing operational parameters for geological containment at industrial volumes. The region is also spearheading maritime hydrogen storage: Hydrogenious and partners began developing an integrated LOHC–SOFC maritime power system, showcasing carrier-based storage for ship bunkering and onboard power delivery. The EU’s investment momentum continues through the European Hydrogen Bank, which allocated ~€1 billion in its second auction round in February 2025 to 15 renewable hydrogen projects—each requiring dedicated storage, buffering, and redistribution channels as market volumes scale.

Japan: Cryogenic LH₂ Infrastructure and Solid-State Storage Materials to Support Imported Hydrogen Pathways

Japan’s hydrogen strategy is heavily shaped by its reliance on imported energy and its goal of building stable international hydrogen supply chains. This has accelerated investment in cryogenic liquid hydrogen (LH₂) storage infrastructure, including specialized receiving terminals supported by the Ministry of Economy, Trade and Industry (METI). A pivotal legislative development was the Hydrogen Society Promotion Act, enacted in May 2024 and taking effect in October 2024. The Act commits 3 trillion yen over 15 years to support hydrogen production, logistics, and storage, including price-gap subsidies that reduce financial risk for long-term LH₂ and ammonia import projects.

The country is also advancing solid-state hydrogen storage materials for compact, mobile, and stationary applications. Japanese companies like Resonac and Aichi Steel are developing next-generation metal hydrides and high-capacity solid absorbents, enabling safer and more energy-dense storage solutions. This complements Japan’s broader infrastructure expansion, supported by a ¥5.7 billion hydrogen hub FEED subsidy announced in March 2025, which prioritizes the design of storage tanks, terminal infrastructure, and multi-company hydrogen interchange systems. Collectively, Japan's dual-track strategy—import-led LH₂ systems and domestic advanced material innovation—positions the nation as a global leader in hydrogen storage technology diversification.

China: Green Hydrogen Scale-Up, Standardization Frameworks, and Regional Storage Megaprojects

China is transitioning from the world’s largest producer of fossil-based hydrogen to a global leader in green hydrogen, with rapid progress in storage infrastructure, regulatory frameworks, and renewable-powered hydrogen hubs. A major policy milestone occurred in October 2025 when the NDRC introduced a national subsidy system covering up to 20% of capex for decarbonization projects, including green hydrogen and green ammonia facilities and their associated storage systems. This initiative complements the 14th Five-Year Plan, which prioritizes a national hydrogen supply system integrating by-product hydrogen, renewable hydrogen, and large-scale storage and transportation networks.

China’s investments are increasingly concentrated in resource-rich regions like Inner Mongolia, which accounted for 59% of national green hydrogen investment in 2023. These regional hubs require equally large hydrogen storage capacity—ranging from high-pressure composite tanks to geological storage units—to balance renewable energy intermittency and support industrial off-takers. Standardization is becoming a core pillar of China’s hydrogen strategy: the Hydrogen Energy Industry Standard System Construction Guide (2023) sets unified specifications for hydrogen purity, storage safety, pipeline integrity, and pressure vessel design. With a national target of 200,000 tonnes of green hydrogen production by 2025, China is undergoing a steep scale-up of high-pressure storage and long-distance transport capabilities to support its rapidly expanding hydrogen economy.

Australia: Export-Oriented Hydrogen Hubs and Geological Storage Readiness

Australia is positioning itself as a cornerstone supplier for the future global hydrogen economy, with a strong emphasis on export-scale storage, ammonia-based hydrogen carriers, and geological cavern development. The Australian Government significantly expanded its Hydrogen Headstart Program in 2024, committing an additional AUD 2 billion to support early-stage megaprojects capable of delivering up to 1 GW of clean hydrogen capacity by 2030. This funding bridges the “green premium” gap and improves project bankability—directly catalyzing investment in storage, liquefaction, and large-scale loading terminals.

Australia’s international hydrogen partnerships continue to strengthen its export outlook, underscored by the September 2024 AUD 660 million H2Global agreement with Germany, which provides guaranteed long-term offtake for Australian renewable hydrogen. Geological storage potential is also being mapped aggressively: Geoscience Australia is assessing salt formations in the Adavale and Amadeus Basins as future sites for subsurface hydrogen storage, essential for load balancing in large hydrogen hubs. The government’s USD 283 million commitment in July 2025 to Orica’s Hunter Valley Hydrogen Hub highlights ammonia’s dual role as an export vector and a high-capacity hydrogen storage medium. These initiatives firmly establish Australia as a global hydrogen export powerhouse with equally robust storage capabilities.

Competitive Landscape: Leading Companies Defining Global Hydrogen Storage Technologies and Deployment Scale

The competitive landscape of the global hydrogen storage industry is shaped by industrial gas giants, advanced composite tank manufacturers, cryogenic equipment specialists, and vertically integrated hydrogen ecosystem developers. Companies such as Linde, Plug Power, Chart Industries, Air Liquide, and Hexagon Purus are driving innovation across cryogenic liquid hydrogen storage, compressed gas systems, Type IV composite cylinders, LOHC logistics, and integrated production-to-storage hydrogen networks. Their competitive strength lies in engineering depth, safety expertise, global logistics networks, and strategic investments in large-scale hydrogen corridors and refueling infrastructure.

Linde plc expands global liquid hydrogen storage and distribution leadership

Linde commands the largest global footprint in hydrogen handling, liquefaction, and cryogenic storage systems. Its portfolio spans large-scale LH₂ plants, proprietary liquefiers, and one of the world’s largest fleets of cryogenic hydrogen trailers. With unmatched expertise in safety engineering and hydrogen logistics, Linde provides end-to-end solutions covering production, pipeline transport, localized bulk storage, and tube-trailer delivery. The company’s strategic focus on building European and U.S. hydrogen corridors underscores its role as a foundational infrastructure provider. Linde’s integrated model—combining reformers, electrolyzers, bulk storage vessels, and distribution assets—positions it as a core enabler of industrial, mobility, and power applications requiring high-volume hydrogen supply.

Plug Power strengthens U.S. liquefaction and cryogenic storage ecosystem

Plug Power has evolved into a vertically integrated hydrogen ecosystem operator, manufacturing its own GenFuel storage and dispensing systems while expanding its green hydrogen production footprint. The company’s conditional $1.66 billion DOE loan commitment in January 2025 accelerates construction of multiple production sites, each equipped with extensive midstream storage and distribution systems. Its April 2025 commissioning of a 15 TPD liquefaction plant in Louisiana significantly expanded its LH₂ capacity, supporting mobility, aerospace, and material handling markets. Plug Power remains the leading supplier of storage-integrated fuel cell systems for material handling applications, having deployed 69,000+ fuel cell units globally by 2024.

Chart Industries expands cryogenic hydrogen storage capacity and fueling infrastructure

Chart Industries is a global specialist in cryogenic hydrogen storage equipment, including vacuum-insulated tanks, trailers, cold boxes, and liquefaction technology. Its proprietary systems—such as the C-Flow liquefaction line—support small- and mid-scale hydrogen production sites. From 2024 to 2025, Chart secured multiple contracts for LH₂ storage vessels and refueling stations, reinforcing its role as an indispensable supplier for hydrogen mobility and industrial hydrogen hubs. Its advanced cryogenic insulation technologies minimize boil-off losses and ensure long-term hydrogen retention, making Chart a preferred partner for fueling networks and centralized hydrogen storage terminals.

Air Liquide scales gaseous and liquid hydrogen storage for industrial and mobility networks

Air Liquide maintains a dominant global presence in gaseous and liquid hydrogen storage infrastructure, supported by extensive tube-trailer fleets and large-scale liquefaction facilities. As co-chair of the Hydrogen Council, the company drives strategic infrastructure planning and financing across global hydrogen economies. In August 2024, Air Liquide inaugurated a 20 MW German green hydrogen plant, directly integrating its output into Europe’s hydrogen pipeline network with advanced buffer storage systems. The company invests heavily in digital monitoring and predictive maintenance platforms to enhance the reliability and safety of long-duration hydrogen storage assets for industrial, power, and mobility customers.

Hexagon Purus advances Type IV composite tanks for mobility and transport logistics

Hexagon Purus is a leading manufacturer of Type IV carbon composite cylinders designed for 700-bar onboard hydrogen storage in FCEVs, heavy-duty trucks, and buses. Its lightweight composite technology offers superior gravimetric efficiency, meeting stringent mobility application requirements. The company is expanding its role in hydrogen transport by launching new composite cylinder modules optimized for tube trailers, enabling higher volumes of compressed hydrogen per shipment. Hexagon Purus’ supply contracts with global commercial vehicle OEMs reinforce its position as a key enabler of hydrogen-powered heavy-duty transport and long-range mobility platforms.

Hydrogen Storage Market Report Scope

Hydrogen Storage Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.8 Billion

|

|

Market Size (2035)

|

$34.2 Billion

|

|

Market Growth Rate

|

13.3%

|

|

Segments

|

By Storage Form (Compressed Gas Storage, Liquid Hydrogen, Material-Based Storage, Chemical Carriers), By Physical Storage Technology (Compressed Hydrogen Tanks, Cryogenic Storage Tanks, Underground Storage), By Material-Based Technology (Metal Hydrides, Chemical Hydrides, Adsorption Materials), By Application (Transportation, Stationary Power Systems, Grid Storage, Industrial Feedstock Storage, Hydrogen Logistics & Distribution), By End-User Industry (Automotive, Chemicals & Petrochemicals, Energy & Utilities, Metals & Mining, Marine & Logistics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hexagon Purus, Plug Power, Linde plc, Air Liquide, Worthington Enterprises, QuantumScape, Toyota Motor Corporation, Hydrogenious LOHC Technologies, Cummins Inc., BayoTech, Pragma Industries, Uniper SE, Chart Industries, Kawasaki Heavy Industries, Hymatech

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hydrogen Storage Market Segmentation

By Storage Form

- Compressed Gas Storage

- Liquid Hydrogen

- Material-Based Storage

- Chemical Carriers

By Physical Storage Technology

- Compressed Hydrogen Tanks

- Cryogenic Storage Tanks

- Underground Storage

By Material-Based Technology

- Metal Hydrides

- Chemical Hydrides

- Adsorption Materials

By Application

- Transportation

- Stationary Power Systems

- Grid Storage

- Industrial Feedstock Storage

- Hydrogen Logistics & Distribution

By End-User Industry

- Automotive

- Chemicals & Petrochemicals

- Energy & Utilities

- Metals & Mining

- Marine & Logistics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Hydrogen Storage Market

- Hexagon Purus

- Plug Power

- Linde plc

- Air Liquide

- Worthington Enterprises

- QuantumScape

- Toyota Motor Corporation

- Hydrogenious LOHC Technologies

- Cummins Inc.

- BayoTech

- Pragma Industries

- Uniper SE

- Chart Industries

- Kawasaki Heavy Industries

- Hymatech

*- List not Exhaustive

Research Coverage: Hydrogen Storage Market

This USDAnalytics study on the global Hydrogen Storage Market provides a rigorous, end-to-end assessment of how policy-driven decarbonization, fuel cell mobility, large-scale electrolysis, and green industrial feedstock are reshaping storage technologies and business models; this report investigates the performance, cost, and safety trajectories of compressed gas, liquid hydrogen, underground caverns, and material-based storage solutions, tracks technology breakthroughs in Type IV composite tanks, cryogenic systems, solid-state materials, LOHCs, and MOF-based adsorbents, and delivers analysis reviews on how these advances translate into real-world deployment across transportation, grid-scale storage, industrial feedstock, and logistics value chains. It highlights the impact of salt cavern megaprojects, heavy-duty mobility pilots, and green steel initiatives on storage system sizing, purity requirements, and infrastructure standardization, while also benchmarking leading vendors on project pipelines, partnership strategies, and innovation roadmaps. By combining quantitative market modeling with qualitative insights on regulations, safety codes, and hydrogen backbone planning, this report is an essential resource for OEMs, storage technology suppliers, gas utilities, EPC contractors, investors, and policymakers seeking to position themselves competitively in the fast-evolving hydrogen storage ecosystem.

Scope Highlights

- Segmentation:

By Storage Form – Compressed Gas Storage, Liquid Hydrogen, Material-Based Storage, Chemical Carriers

By Physical Storage Technology – Compressed Hydrogen Tanks, Cryogenic Storage Tanks, Underground Storage

By Material-Based Technology – Metal Hydrides, Chemical Hydrides, Adsorption Materials

By Application – Transportation, Stationary Power Systems, Grid Storage, Industrial Feedstock Storage, Hydrogen Logistics & Distribution

By End-User Industry – Automotive, Chemicals & Petrochemicals, Energy & Utilities, Metals & Mining, Marine & Logistics

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies: Analysis / profiles of 15+ leading hydrogen storage companies across cylinders, cryogenic systems, LOHC platforms, and integrated hydrogen infrastructure solutions.