Hydrophobic Coatings Market to Reach $4.7 Billion by 2034 at 6.3% CAGR Fueled by PFAS-Free Reformulation, Medical Innovation, and Industrial Surface Protection

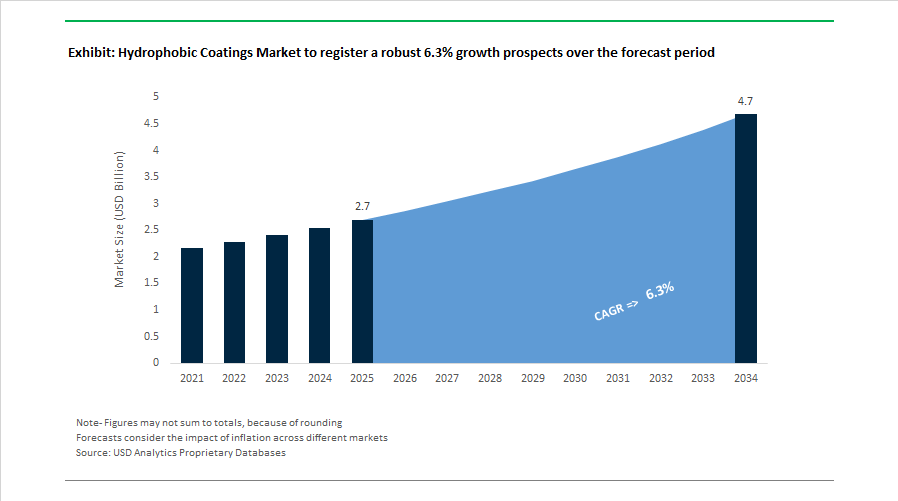

The Hydrophobic Coatings Market is projected to expand from $2.7 billion in 2025 to $4.7 billion by 2034, registering a CAGR of 6.3%. Growth is being driven by rising demand for water-repellent coatings, anti-fouling nanocoatings, moisture-resistant electronics protection, medical device surface modification, and corrosion-resistant industrial coatings. Increasing regulatory pressure on PFAS-based chemistries, combined with rapid adoption across automotive electronics, aerospace, satellite communication, medical devices, and energy infrastructure, is accelerating innovation in fluorine-free hydrophobic technologies and nano-engineered surface treatments.

Market restructuring began in May 2024 when Kansai Helios, a subsidiary of Kansai Paint, acquired Weilburger, strengthening its European footprint in high-performance functional coatings, including non-stick and hydrophobic heat-resistant systems. In June 2024, Hydromer introduced HydroThrombX™, a dual-function hydrophobic and thromboresistant coating for catheters and guidewires, reflecting strong momentum in cardiovascular device surface engineering. In August 2024, Wacker Chemicals completed the acquisition of 3M’s hydrophobic coatings business, securing specialty intellectual property and expanding North American capacity to serve moisture-resistant electronics and medical device manufacturers. In September 2024, Aculon launched AcuFlow® 7 nanocoating technology, engineered to prevent organic and inorganic deposit adhesion in oil and gas pipelines, directly addressing paraffin and scale buildup in upstream operations. During 2024, Continental AG also introduced proprietary transparent hydrophobic coatings for automotive digital dashboards and heads-up displays, improving visibility by 15% under high humidity while delivering smudge resistance for touch-enabled interiors. Surmodics commercialized Preside™ hybrid hydrophilic-hydrophobic coatings for neurovascular catheters, targeting high lubricity and durability for minimally invasive procedures. In late 2024, Cytonix rolled out CytoThane superhydrophobic coatings designed to prevent rain fade in satellite radomes, protecting Ku and Ka-band signal performance during severe weather events.

Innovation accelerated in 2025 with strong emphasis on PFAS-free and advanced nanomaterial systems. In March 2025, NEI Corporation, in collaboration with HydroGraph Clean Power, launched graphene dispersions engineered for integration into hydrophobic coatings, enhancing mechanical strength and corrosion resistance in aerospace and heavy industrial applications. In June 2025, P2i introduced ultra-thin molecular hydrophobic coatings for hearing aids and wearable electronics formulated without PFOA or PFAS, ensuring compliance with updated EU medical device regulations effective mid-2025. Throughout 2025, BYK announced it would cease manufacturing PFAS-containing additives by year end, transitioning its hydrophobic additive portfolio to low- and non-PFAS alternatives in anticipation of global regulatory tightening in 2026. In December 2025, AkzoNobel and Axalta announced a definitive all-stock merger agreement aimed at integrating their R&D capabilities in high-performance hydrophobic and protective coatings, a consolidation entering final regulatory review in early 2026. This merger positions the combined entity as a dominant force in industrial and automotive surface-treatment technologies.

Regulatory dynamics intensified across North America between 2025 and 2026, with 11 U.S. states implementing enforceable PFAS limits. The passage of the PFAS Protection Act in New Mexico, effective 2027, triggered a large-scale reformulation wave across coating manufacturers during 2025 and 2026, accelerating the commercialization of fluorine-free hydrophobic coatings and sustainable water-repellent chemistries. The hydrophobic coatings market is increasingly characterized by nano-engineered surface modification, graphene-enhanced barrier coatings, medical-grade moisture protection, satellite communication resilience coatings, and PFAS-compliant industrial solutions serving automotive, aerospace, electronics, energy, and healthcare end-use sectors.

Hydrophobic Coatings Market Trends and Opportunities Driving Advanced Surface Protection Technologies

Integration of Hydrophobic and Oleophobic Nanocoatings in Consumer Electronics for Durability and Optical Clarity

The hydrophobic coatings market is gaining strong traction in the consumer electronics industry, where manufacturers are embedding hydrophobic and oleophobic properties directly into materials to enhance durability, water resistance, and optical performance. Modern devices such as smartphones, foldable displays, wearables, and camera optics require nanoscale surface treatments that repel water, oils, and contaminants while preserving screen clarity and touch sensitivity. As device designs become thinner and more complex, molecular-level hydrophobic coating technologies are increasingly replacing traditional sealing methods to ensure long-term performance under high humidity and repeated mechanical stress.

Recent product launches highlight this trend. At Mobile World Congress 2026, Corning introduced Gorilla Glass Ceramic 3, designed for foldable devices such as the Motorola Razr Fold and incorporating advanced hydrophobic and oleophobic coating architectures capable of withstanding more than 20 drop tests from one meter onto asphalt while preventing moisture-induced microfractures. In parallel, manufacturers in South Korea and Vietnam have implemented nanoscale hydrophobic barriers capable of achieving IPX8 waterproof ratings, allowing devices to withstand prolonged immersion without bulky mechanical seals. These coatings are also expanding in wearables, where companies like Garmin and Samsung utilize invisible hydrophobic layers to protect biometric sensors from sweat corrosion. Additionally, innovations in optical applications are emerging, such as the water-repellent lens filters launched by Voigtlander at CP+ 2026, enabling rapid cleaning and improved optical performance in professional photography and cinematography environments. Hydrophobic nanocoatings are also being applied to printed circuit boards (PCBs) in high-density 5G and emerging 6G devices, preventing condensation while maintaining the thermal dissipation required for advanced processors.

Renewable Energy Infrastructure Increasing Adoption of Self-Cleaning and Anti-Icing Hydrophobic Coatings

The rapid expansion of renewable energy infrastructure is creating new demand for hydrophobic and self-cleaning coatings that enhance operational efficiency and reduce maintenance costs. In large-scale solar and wind installations, environmental factors such as dust accumulation, ice formation, and salt exposure significantly affect energy output and equipment lifespan. Hydrophobic coatings provide passive protection by enabling water repellency, anti-soiling performance, and reduced surface friction, making them increasingly essential for next-generation renewable energy systems.

Government initiatives supporting solar deployment are accelerating this trend. In 2025, programs in India and the European Union prioritized waterless cleaning technologies for utility-scale solar parks, encouraging the integration of hydrophobic coatings into photovoltaic glass to minimize dust adhesion and maintain energy output. Research from Advanced NanoTech Lab indicates that these coatings help prevent the “shading effect” caused by environmental pollutants, improving solar panel efficiency over time. The wind energy sector is also adopting advanced hydrophobic surface technologies. Companies such as AkzoNobel have introduced specialized coatings that provide anti-icing protection and resistance to leading-edge erosion caused by rain, sand, and salt spray, which is particularly important for offshore wind farms in the North Sea and Asia-Pacific region. Beyond energy infrastructure, hydrophobic functionality is also being embedded directly into construction materials, demonstrated by Nuvoco Vistas’ launch of Concreto Uno hydrophobic concrete, which incorporates a damp-lock formula to prevent water penetration and carbonation in civil infrastructure.

Regulatory Pressure on PFAS Driving Innovation in Fluorine-Free and Bio-Based Hydrophobic Coatings

The global regulatory crackdown on PFAS (Per- and Polyfluoroalkyl Substances) is creating a significant innovation opportunity in the hydrophobic coatings industry, pushing manufacturers toward fluorine-free and bio-based alternatives. PFAS compounds have historically been used in water-repellent coatings due to their excellent durability and low surface energy. However, increasing environmental concerns and regulatory restrictions are forcing the development of sustainable hydrophobic coatings based on silane, siloxane, and plant-derived chemistries.

Regulatory frameworks across Europe and North America are accelerating this transition. Under EU regulations introduced in 2025, strict limits on PFAS concentrations in consumer products such as food packaging and cosmetics are driving demand for PFAS-free barrier coatings, with the market for these alternatives expected to surpass $1 billion by late 2026. Similarly, the U.S. Environmental Protection Agency’s TSCA reporting requirements, effective in 2026, require manufacturers and importers to disclose PFAS usage volumes, increasing compliance costs and encouraging the adoption of bio-based hydrophobic surface treatments in construction materials, textiles, and consumer goods. Innovation in this segment is already emerging, illustrated by Stahl’s launch of Relca HY-288 in 2025, a PFAS-free hybrid dispersion designed for furniture and interior applications that provides strong stain resistance against substances such as coffee, wine, and mustard while complying with modern VOC and sustainability standards.

Aerospace and Defense Infrastructure Creating Demand for Advanced Anti-Corrosion Hydrophobic Coating Systems

The aerospace and defense sectors represent a high-value growth opportunity for the hydrophobic coatings market, particularly as governments increase investment in military modernization and infrastructure resilience. Aircraft, naval vessels, and coastal defense installations operate in extreme environments where moisture, salt exposure, and chemical contaminants can rapidly accelerate corrosion. Hydrophobic coating technologies provide a protective barrier that repels water, reduces surface degradation, and preserves aerodynamic and structural integrity.

Major industry investments reflect this opportunity. In December 2025, AkzoNobel announced an expansion of its U.S. aerospace coatings facility, focusing on the production of next-generation anti-corrosion hydrophobic coatings for defense aircraft capable of resisting hydraulic fluids, chemical cleaners, and high-stress maintenance conditions. In the marine sector, PPG’s Hydroreset™ technology, following the rollout of SIGMAGLIDE® 2390, offers a biocide-free fouling release coating that prevents marine organism adhesion at the molecular level, improving vessel efficiency and reducing fuel consumption in line with IMO 2026 shipping emission standards. Additionally, the U.S. Department of Defense’s 2025 Climate Adaptation Plan highlights the importance of hydrophobic coatings in protecting coastal radar installations, hangars, and defense infrastructure from salt-air corrosion, creating opportunities for specialized coatings that combine durability with radar-transparent and low-observable material properties required in advanced military systems.

Hydrophobic Coatings Market Share and Segmentation Insights

Self-Cleaning Hydrophobic Coatings Lead Adoption Across Infrastructure, Automotive, and Solar Applications

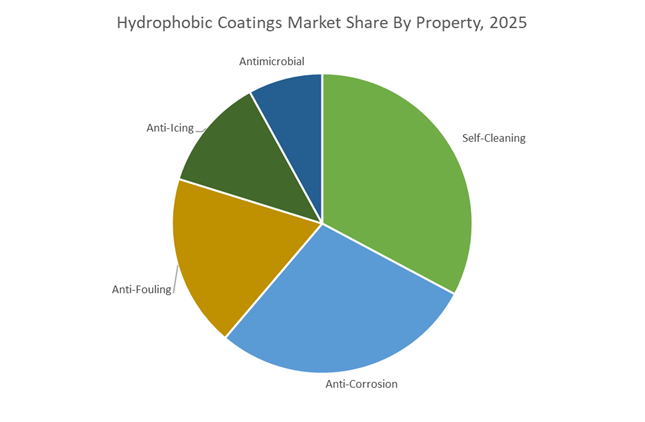

Self-cleaning hydrophobic coatings accounted for 32.80% of the Hydrophobic Coatings Market share in 2025, making them the most widely deployed functional property within the advanced surface protection coatings industry. These coatings create water-repellent surfaces with low surface energy, allowing water droplets to bead and roll off surfaces while carrying dust and contaminants away. The functionality significantly reduces maintenance requirements for building facades, automotive windshields, solar panels, consumer electronics, and industrial equipment, making them attractive across a wide range of sectors. Their adoption is particularly strong in applications where surface cleanliness directly affects operational performance or aesthetic appearance, such as glass structures, photovoltaic panels, and exterior architectural materials. In 2025, innovation in this segment is centered on photocatalytic self-cleaning coatings, which combine hydrophobic properties with titanium dioxide nanoparticle-based photocatalysis. These advanced coatings use ultraviolet light to break down organic contaminants on surfaces, while the hydrophobic layer allows rainwater to remove residual debris. This dual-function technology significantly improves durability and long-term performance in outdoor environments compared with conventional hydrophobic coatings.

Construction Sector Drives the Largest Demand for Hydrophobic Coating Technologies

Construction represented 34.80% of the Hydrophobic Coatings Market share in 2025, establishing the building and infrastructure sector as the primary consumer of hydrophobic surface treatment technologies. Hydrophobic coatings are widely applied to glass panels, concrete structures, stone surfaces, roofing materials, and architectural metals to prevent water infiltration, staining, and biological growth. In modern building design, these coatings support self-cleaning facades, moisture-resistant concrete surfaces, anti-graffiti protection, and improved durability of exterior building envelopes, reducing maintenance requirements and extending structural lifespan. Global urbanization and large-scale infrastructure development continue to expand the addressable market for hydrophobic coating technologies. In 2025, infrastructure protection has become a key growth driver as governments and private asset owners seek to protect bridges, tunnels, highways, and transportation infrastructure from long-term moisture damage. Hydrophobic coatings reduce water penetration into concrete and porous construction materials, preventing freeze–thaw deterioration, corrosion of embedded steel reinforcement, and structural degradation. As climate variability increases rainfall exposure and extreme weather events, demand for advanced hydrophobic coating systems in infrastructure preservation continues to strengthen across both developed and emerging economies.

Competitive Landscape in Hydrophobic Coatings Market

PPG Industries Strengthens EV and Medical Hydrophobic Coating Solutions

PPG Industries continues to lead in multifunctional hydrophobic coating technologies for automotive, aerospace, and medical device applications. In 2025 and 2026, the company scaled thromboresistant and hydrophobic coating systems designed to reduce clot formation risks on surgical tools and implantable devices. PPG is prioritizing EV battery enclosure protection and advanced driver assistance system sensor clarity, ensuring long-term moisture resistance without optical distortion. Its low-VOC nanotechnology coatings deliver anti-corrosion and self-cleaning performance across automotive and infrastructure segments. With a dominant position in North America, PPG leverages a strong R&D pipeline to align with tightening environmental regulations and evolving performance standards.

AkzoNobel Advances Biocide-Free Marine Hydrophobic Technologies

AkzoNobel N.V. is expanding its eco-friendly hydrophobic coating portfolio across maritime and industrial sectors. In February 2026, the company reported margin expansion and renewed organic growth following efficiency initiatives. Through its International brand, AkzoNobel is scaling the Intersleek 1100SR coating, a biocide-free slime-release system that reduces hull friction and enhances vessel fuel efficiency. The company is deepening its presence in China via large-scale drydocking partnerships, reinforcing its marine coatings footprint. Strategic discussions regarding a potential merger with Axalta signal further consolidation in the global coatings industry. AkzoNobel’s innovation pipeline emphasizes fouling control, carbon reduction, and solvent-free hydrophobic surface protection.

BASF SE Integrates Hydrophobic Effects into Automotive Surface Innovation

BASF SE is positioning its surface technologies business to deliver high-performance hydrophobic treatments for automotive and industrial markets. The company reported €6.6 billion EBITDA before special items in 2025 and is targeting up to €7.0 billion in 2026 as value is unlocked from standalone segments. Expansion of the Zhanjiang Verbund site strengthens global capacity for advanced surface chemistry. BASF’s Driving the Proxy automotive color collection incorporates liquid metal-like finishes and integrated hydrophobic functionality for enhanced durability and water repellency. Cost-reduction initiatives generating €1.7 billion in annual run-rate savings support reinvestment into next-generation low-emission coatings.

Nippon Paint Expands Hydrophobic Reach Through Asset Assembler Strategy

Nippon Paint Holdings continues to expand its hydrophobic coatings footprint through acquisitions and decentralized growth. The consolidation of AOC in March 2025 enhanced its access to high-performance resin technologies, supporting moisture-resistant industrial coatings. In 2026, the company plans to operate more than 2,000 community stores in China, strengthening penetration in Tier 0-2 repaint markets and expanding into maintenance and industrial operations sectors. Nippon Paint is shifting from developer-focused growth to diversified industrial customers, including millions of MRO enterprises. The company targets medium-term revenue growth of 8 to 9% and EPS growth of 10 to 12%, supported by specialty coatings innovation.

3M Company Leverages Material Science for Multifunctional Repellency

3M Company continues to commercialize hydrophobic and stain-repellent technologies across electronics, textiles, automotive, and construction sectors. Under its 3M eXcellence operating model, the company is accelerating innovation deployment from laboratory research to global supply chains. The Scotchgard portfolio includes advanced water-repellent treatments such as Protector Water Repellent PM-3705 and specialized electronics-safe repellents. 3M’s 2025 Global Impact Report highlights advancements in dichroic films and anti-fouling technologies derived from fluoropolymer and nanoparticle expertise. With more than 87 coating products spanning automotive and design industries, 3M maintains broad penetration in moisture-resistant surface engineering.

Henkel Expands Circular Barrier Coatings Through Strategic Acquisitions

Henkel AG & Co. KGaA is strengthening its position in hydrophobic and barrier coatings through targeted acquisitions and sustainable packaging innovation. In February 2026, Henkel agreed to acquire Stahl Group for €2.1 billion, expanding its high-performance specialty coatings portfolio for automotive, fashion, and packaging sectors. At Interpack 2026, Henkel showcased Loctite Liofol and Technomelt E-COM technologies that provide water and humidity resistance for recyclable fiber-based packaging. The company is prioritizing circular economy solutions that deliver plastic-like barrier performance while maintaining recyclability. Recent acquisition activity is projected to add nearly €1 billion in sales, reinforcing the growth trajectory of its Adhesive Technologies division.

United States: PFAS Transition, Solar Performance Gains, and Functional Surface Innovation

The United States hydrophobic coatings industry is undergoing a structural shift driven by energy efficiency mandates, regulatory pressure on fluorinated chemistries, and accelerated adoption across aerospace, healthcare, and infrastructure. In 2025, the U.S. Department of Energy confirmed measurable efficiency gains in photovoltaic modules using advanced hydrophobic surface layers, reinforcing the role of self-cleaning coatings in utility-scale solar farms. These coatings are now specified to minimize dust adhesion and reduce operational maintenance cycles, particularly in arid regions. Parallel to this, aerospace and defense procurement intensified in late 2025, with hybrid photothermal ice-phobic coatings being adopted to lower dependence on chemical de-icing fluids and improve aircraft operational readiness in cold-weather conditions.

Regulation is reshaping formulation strategies. The Environmental Protection Agency has implemented stricter oversight of long-chain fluorinated compounds effective early 2026, accelerating commercialization of PFAS-free siloxane–acrylic hybrid resins across automotive, industrial, and construction coatings. Medical devices represent another high-value growth vector. In February 2025, Silq Technologies and NuSil Technology advanced zwitterionic surface treatments for silicone implants, materially reducing protein adhesion and biofouling risks. Infrastructure durability remains a consistent demand driver, with American Society of Civil Engineers highlighting silane-based concrete impregnation as a preferred solution for chloride-ion resistance in bridges and coastal tunnels. Startup activity is reinforcing innovation depth, with companies such as Dropel Fabrics and Grox scaling nanotechnology-based hydrophobic treatments for natural textiles and energy systems through 2026.

China: Electronics Miniaturization, Smart Infrastructure, and Grid Protection

China’s hydrophobic coatings market is expanding through electronics manufacturing precision, smart-city infrastructure mandates, and power grid reliability requirements. In mid-2025, smartphone OEMs began using digital printing techniques to apply ultra-thin hydrophobic layers on foldable displays, achieving water resistance without compromising device thickness or flexibility. At the policy level, the Ministry of Industry and Information Technology 2026 work plan elevates specialty surface treatments to a priority category, with explicit targets for G5-grade purity in hydrophobic coatings used in semiconductor wafer cleaning and fabrication environments.

Infrastructure programs are reinforcing volume demand. Smart-city initiatives across the Yangtze River Delta now require water-repellent barriers in public assets to mitigate humidity-driven degradation and climate stress. In parallel, antifouling innovation has accelerated in the power sector. Guangdong Yufeng Industries commercialized one-component RTV silicone coatings in late 2025 that prevent conductive water films on insulators, significantly increasing flash-over voltage in high-voltage grids. Automotive electrification is further embedding hydrophobic functionality, with leading Chinese EV manufacturers integrating nanoparticle-based coatings into battery enclosures and charging interfaces as standard safety features for the 2026 model year.

Germany: Bio-Attributed Inputs, Regulatory Compliance, and Smart Coatings

Germany’s hydrophobic coatings industry is characterized by sustainability-led reformulation, regulatory-driven material substitution, and early adoption of smart coating systems. In December 2025, PPG secured REDCert² certification at key European sites, validating the use of bio-attributed raw materials in hydrophobic automotive topcoats and supporting OEM decarbonization targets. Innovation visibility was high at the European Coatings Show 2025, where Evonik introduced the TEGO Wet Terra biosurfactant line, delivering high hydrophobic performance in single-component furniture coatings while relying on 100% natural feedstocks.

Technology convergence is also shaping demand. German startup AIVAM launched a sensor-embedded smart varnish in 2025 that enables real-time moisture and temperature monitoring within the coating layer, supporting predictive maintenance strategies for chemical storage tanks and industrial assets. Regulatory pressure continues to influence formulation choices. Following 2024–2025 updates from the European Chemicals Agency, German formulators are increasingly replacing legacy anti-corrosion additives with organofunctional silanes to align with REACH restrictions while maintaining long-term hydrophobic performance.

India: Port Infrastructure, Antimicrobial Surfaces, and Climate-Resilient Construction

India’s hydrophobic coatings market is expanding through maritime infrastructure investment, public health-focused surface technologies, and climate-resilient construction materials. Under the SagarMala program, large-scale port and coastal upgrades during 2025–2026 have increased the application of anti-fouling hydrophobic coatings on marine structures and naval vessels to counter tropical salinity and biofouling in the Indian Ocean. Public transport and healthcare settings are emerging as parallel demand centers. In late 2025, Panlys Nanotech commercialized visible-light-activated titanium dioxide nano-coatings that combine hydrophobicity with continuous pathogen neutralization, positioning these systems for use in high-footfall environments.

Construction materials are also evolving. Nuvoco Vistas introduced Concreto Uno in 2025, a hydrophobic concrete incorporating a proprietary damp-lock formulation. This innovation is gaining traction in high-rainfall regions such as the Western Ghats, where moisture ingress and durability constraints have historically limited asset lifespans. Collectively, these developments indicate a shift toward performance-driven, multifunctional hydrophobic coatings tailored to India’s climatic and infrastructure conditions.

Japan: Optical Precision and Automotive Display Performance

Japan’s hydrophobic coatings industry is closely aligned with optical electronics and automotive human–machine interfaces. In 2025, AGC announced a new generation of fluorinated hydrophobic coatings engineered for AR and VR lenses, combining smudge resistance with high light transmittance to support next-generation wearable displays. Automotive applications are reinforcing demand. Through collaborations with regional OEMs, Japanese formulators have deployed transparent hydrophobic coatings on head-up displays, improving driver visibility by approximately 15% under high-humidity conditions. These advances underscore Japan’s focus on precision surface engineering where hydrophobicity directly enhances user experience and safety.

Summary Table: Country-Level Signals in the Hydrophobic Coatings Industry

Hydrophobic Coatings Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Key Technology Focus

|

Strategic Implication

|

|

United States

|

Solar efficiency, PFAS regulation

|

PFAS-free hybrids, ice-phobic layers

|

Regulatory-led reformulation and multi-sector adoption

|

|

China

|

Electronics, smart infrastructure

|

Ultra-thin coatings, RTV silicones

|

Volume scale with high-purity requirements

|

|

Germany

|

Sustainability and compliance

|

Bio-attributed binders, smart varnishes

|

Premium, regulation-aligned innovation

|

|

India

|

Maritime assets, public health

|

Antifouling and antimicrobial nano-coatings

|

Climate-resilient infrastructure solutions

|

|

Japan

|

Optics and automotive displays

|

High-durability transparent coatings

|

Precision-driven performance leadership

|

Hydrophobic Coatings Market Report Scope

Hydrophobic Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.7 Billion

|

|

Market Size (2034)

|

$4.7 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Property (Antimicrobial, Anti-Icing, Anti-Fouling, Anti-Corrosion, Self-Cleaning), By Substrate Type (Metals, Glass and Ceramics, Concrete and Masonry, Polymers and Composites, Textiles and Leather), By Technology (Water-Based, Solvent-Based, Nanotechnology-Based, UV-Cured Coatings), By End-Use Industry (Automotive, Aerospace and Defense, Construction, Electronics, Renewable Energy, Medical Devices)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., The Sherwin-Williams Company, Akzo Nobel N.V., BASF SE, 3M Company, Nippon Paint Holdings Co., Ltd., Axalta Coating Systems Ltd., Kansai Paint Co., Ltd., Evonik Industries AG, Hempel A/S, RPM International Inc., AGC Inc., Aculon, Inc., P2i Ltd., NeverWet, LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hydrophobic Coatings Market Segmentation

By Property

- Antimicrobial

- Anti-Icing

- Anti-Fouling

- Anti-Corrosion

- Self-Cleaning

By Substrate Type

- Metals

- Glass and Ceramics

- Concrete and Masonry

- Polymers and Composites

- Textiles and Leather

By Technology

- Water-Based

- Solvent-Based

- Nanotechnology-Based

- UV-Cured Coatings

By End-Use Industry

- Automotive

- Aerospace and Defense

- Construction

- Electronics

- Renewable Energy

- Medical Devices

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Hydrophobic Coatings Industry

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Akzo Nobel N.V.

- BASF SE

- 3M Company

- Nippon Paint Holdings Co., Ltd.

- Axalta Coating Systems Ltd.

- Kansai Paint Co., Ltd.

- Evonik Industries AG

- Hempel A/S

- RPM International Inc.

- AGC Inc.

- Aculon, Inc.

- P2i Ltd.

- NeverWet, LLC

*- List not Exhaustive