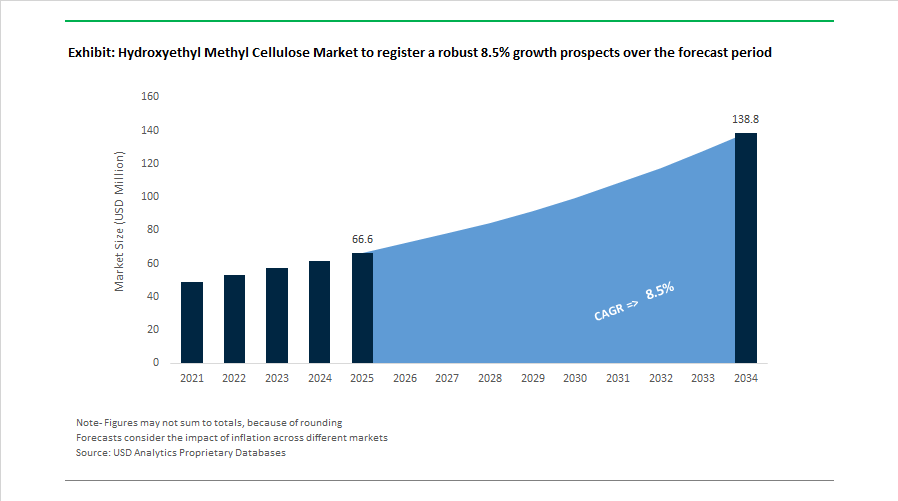

Hydroxyethyl Methyl Cellulose Market to Reach $138.8 Million by 2034 at 8.5% CAGR Fueled by Infrastructure Capex, Pharma-Grade Excipients, and Sustainability-Led Portfolio Shifts

The Hydroxyethyl Methyl Cellulose (HEMC) Market is projected to grow from $66.6 Million in 2025 to $138.8 Million by 2034, registering a robust CAGR of 8.5%. Demand expansion is being driven by rising consumption of cellulose ether-based tile adhesives, dry-mix mortars, self-leveling compounds, exterior insulation systems, and high-purity pharmaceutical excipients. Increasing infrastructure spending, regulatory emphasis on sustainable construction chemicals, and corporate transitions toward high-margin specialty polymers are reshaping the global HEMC competitive landscape.

In August 2024, Lotte Fine Chemical and Japan’s JERA signed a Joint Collaboration Agreement to build a low-carbon fuel value chain, aligning with Lotte’s broader green chemical strategy aimed at reducing the carbon intensity of ammonia and cellulose ether production in Ulsan, South Korea. During 2024, the Indian government increased infrastructure capital expenditure by 11.1% to $133.86 billion, directly stimulating demand for HEMC-enhanced building materials across tile adhesives, plaster systems, and cementitious mortars. In May 2025, Nouryon released its 2024 Sustainability Report, confirming an EcoVadis Gold rating that places it in the top 2% of industry performers. This ESG milestone is strategically important as global construction and personal care brands increasingly require validated low-carbon, biodegradable cellulose ethers within their procurement frameworks.

Strategic restructuring accelerated in 2025. Throughout the year, Ashland finalized the divestiture of its Avoca business and select carboxymethylcellulose and methylcellulose lines, reducing sales by approximately $38 million while sharpening its focus on higher-margin HEMC and rheology modifiers for coatings and pharmaceuticals. In October 2025, Ashland expanded its injectable excipient portfolio, targeting parenteral drug delivery systems where ultra-high-purity HEMC grades serve as stabilizers and viscosity modifiers. In the same month, the company received a $103 million tax refund related to earlier divestitures, reinforcing its balance sheet to support its transformation into a pure-play specialty additives company. In December 2025, Nouryon advanced its South American strategy with a groundbreaking ceremony for a new Home and Personal Care Innovation Center in Brazil, scheduled for full operation by the end of 2026, focused on localized sustainable cellulose ether solutions.

In January 2026, Wacker Chemie AG reported preliminary 2025 sales of €5.49 billion, reflecting a 4% year-on-year decline amid a weak macroeconomic environment, yet emphasized prioritization of specialty polymer systems compatible with HEMC formulations. In February 2026, Ashland Inc. announced first-quarter fiscal 2026 results and narrowed Adjusted EBITDA guidance to $400–$420 million due to temporary startup delays at its Calvert City plant and weather disruptions, while reaffirming resilience in specialty additives including HEMC. In the same month, Lotte Chemical outlined a 2026 strategy to reduce dependence on commodity petrochemicals and accelerate expansion in high-performance and green materials, strengthening upstream support for cellulose ether growth across Asia. Also scheduled for completion in February 2026, Shin-Etsu Chemical’s 2.1 billion yen functional products plant in Zhejiang, China, reinforces regional infrastructure for advanced building chemicals and surface treatments, indirectly supporting high-growth demand for premium HEMC formulations in construction and industrial applications.

Hydroxyethyl Methyl Cellulose (HEMC) Market Trends and Opportunities

Regulatory-Driven Performance Upgrades in European Construction Mortars

The European construction chemicals market is entering a compliance-led reformulation cycle, with Hydroxyethyl Methyl Cellulose becoming a critical performance enabler rather than a discretionary additive. The Revised Construction Products Regulation (EU) 2024/3110, effective January 2025 and fully applicable from January 2026, is reshaping formulation priorities across masonry mortars, tile adhesives, and screeds governed under EN 998-1 and EN 13813. These frameworks place direct accountability on chemical additives to support documented performance, sustainability reporting, and digital traceability.

A central catalyst is the phased introduction of Digital Product Passports, which require construction materials to carry verified, auditable data across the value chain. For HEMC suppliers, this is accelerating demand for premium, high-consistency grades that reliably deliver long open time, stable water retention, and predictable rheology under varied site conditions. Contractors and specifiers are increasingly selecting mortar systems where HEMC performance variability is minimized, as deviations can now trigger non-compliance at the building or project certification level.

Environmental reporting obligations are reinforcing this shift. From January 2026, manufacturers must disclose Global Warming Potential for major construction product families. Advanced HEMC grades allow for thinner application layers while maintaining workability and adhesion, directly reducing material intensity per square meter. Field audits from high-specification commercial projects in Germany and France show that optimized HEMC formulations have reduced on-site rework by up to 18%, a material productivity gain as labor shortages continue to challenge European construction timelines. This positions HEMC as a compliance-critical additive aligned with both regulatory risk mitigation and operational efficiency.

Supply Concentration and Feedstock Inelasticity Tightening the HEMC Market

On the supply side, the HEMC market is increasingly characterized by strategic allocation rather than open availability. Global production remains concentrated among a small group of tier-one manufacturers, including Dow, Ashland, and Shin-Etsu, while feedstock availability for dissolving wood pulp continues to tighten. In 2025, global DWP consumption reached roughly 10 million tons, with more than 83% absorbed by the viscose textile sector, leaving cellulose ethers exposed to competition for high-purity pulp.

Recent growth in North American and Asian pulp consumption exceeding 20% has amplified supply-side pressure for non-contracted buyers. Market data from late 2025 shows quarter-over-quarter spot price volatility of 3 to 5% for cellulose ethers, driven by rising energy costs, refined cotton pricing, and environmental compliance expenses. As a result, producers are prioritizing long-term, high-volume contracts linked to the USD 43.6 billion global dry-mix mortar market, where demand visibility and margin stability are strongest.

This strategic prioritization has downstream implications. Smaller-volume applications in personal care and pharmaceuticals are experiencing lead-time extensions of four to six weeks, pushing formulators to either absorb higher costs or evaluate alternative rheology modifiers. For construction-focused HEMC suppliers, however, this environment reinforces pricing discipline and strengthens the strategic value of backward integration and feedstock security.

Engineered HEMC for Automated and 3D Construction Systems

The industrialization of construction through automation and 3D printing is creating a high-margin niche for engineered HEMC grades with tightly controlled dispersion and dust profiles. Automated dry-mix blending plants and closed-loop silo systems demand low-dusting, rapid-dispersing cellulose ethers to maintain process integrity and protect worker health. Updated occupational safety rules, including the UK’s S.I. 2025 No. 1172, are intensifying scrutiny on airborne particulates, making surface-treated HEMC formulations that cut dust emissions by up to 65% increasingly attractive.

In parallel, rapid-setting tile adhesive and self-leveling compound lines require additives that hydrate instantly without lump formation. Construction chemical leaders such as Sika are specifying advanced HEMC grades compatible with RFID-linked dosing and just-in-time logistics, as demonstrated by new automated facilities commissioned in Asia during 2025. These systems reduce formulation variability while improving throughput and waste control.

The opportunity extends into 3D concrete printing, a segment now exceeding USD 300 million in annual value. In these applications, HEMC provides the yield stress and shape retention required to support extruded layers without collapse. Patent activity surged in 2025 around printable mortar systems, with HEMC and related cellulose ethers forming the backbone of many proprietary binder technologies. This positions engineered HEMC as a strategic material for the next phase of digitally enabled construction.

Biodegradable Seed Coatings and Bio-Based Film Formers

Beyond construction, regulatory pressure in agriculture is opening a structurally new demand channel for HEMC as a biodegradable film former. European Commission Regulation (EU) 2023/2055 mandates the removal of microplastics from seed coatings, with a firm compliance deadline of October 2028. This has elevated HEMC as a preferred alternative to synthetic polymers due to its water solubility, film-forming capability, and biodegradability.

To meet regulatory thresholds, seed treatment manufacturers are investing in HEMC-based coatings capable of passing OECD 301F biodegradability requirements, which mandate 60% degradation within 28 days. The shift toward biological seed treatments further strengthens HEMC’s positioning. Its neutral pH and high water-retention capacity support the viability of nitrogen-fixing microbes and biostimulants, which are increasingly integrated into modern seed systems.

Demand signals from major agricultural markets underscore the scale of this opportunity. During the 2024 to 2025 season, Brazil’s record 169-million-ton soybean harvest drove increased adoption of friction-reducing, bio-compatible seed coatings to improve planting efficiency and seed flowability. As microplastic restrictions expand globally, HEMC is emerging as a frontier material that bridges regulatory compliance, agronomic performance, and sustainability objectives across the agricultural value chain.

Hydroxyethyl Methyl Cellulose Market Share and Segmentation Insights

Industrial Grade Hydroxyethyl Methyl Cellulose Leads the Market Through Large-Scale Construction and Coatings Applications

Industrial grade hydroxyethyl methyl cellulose (HEMC) accounted for 52.80% of the Hydroxyethyl Methyl Cellulose Market share in 2025, establishing it as the dominant grade across global cellulose ether demand. Industrial grade HEMC is widely used as a thickener, water-retention agent, and rheology modifier in high-volume applications including construction chemicals, paints and coatings, adhesives, and industrial formulations, where standard purity specifications meet operational requirements. Its ability to enhance viscosity control, water retention, and workability in cementitious systems makes it an essential additive for modern building materials. In 2025, the growth of industrial grade HEMC is closely tied to expanding construction and infrastructure investment worldwide, particularly in emerging markets experiencing rapid urban development and residential construction. HEMC is commonly incorporated into cement-based tile adhesives, plasters, renders, self-leveling compounds, and gypsum-based dry-mix mortars, where it improves consistency, prevents premature water loss, and enhances bonding strength. These functional advantages support the rising demand for high-performance dry-mix construction materials, reinforcing industrial grade HEMC as a core additive in construction chemical formulations.

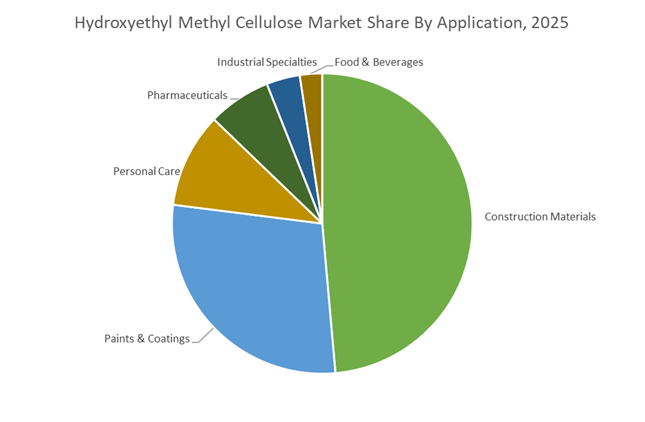

Construction Materials Segment Drives the Largest Hydroxyethyl Methyl Cellulose Consumption

Construction Materials represented 48.60% of the Hydroxyethyl Methyl Cellulose Market share in 2025, making it the largest application segment for HEMC-based additives. Hydroxyethyl methyl cellulose plays a crucial role in cement-based mortars, gypsum plasters, tile adhesives, and self-leveling compounds, where it provides water retention, improved workability, enhanced adhesion, and controlled setting behavior during application. Even small additions of HEMC significantly improve the performance of dry-mix formulations, ensuring consistent curing and reducing cracking in finished surfaces. The demand for HEMC in this segment is further strengthened by the rapid growth of pre-mixed and dry-mix construction materials, which offer improved consistency and efficiency compared with traditional on-site mixing methods. In 2025, a major technological shift in the construction sector is the growing adoption of mechanized mortar and plaster application systems, driven by labor shortages and the need to improve construction productivity. These automated spraying and pumping systems require HEMC formulations with precisely engineered viscosity profiles and open time control, enabling optimized pumpability, sprayability, and application stability in high-throughput construction environments.

Competitive Landscape in Hydroxyethyl Methyl Cellulose Market

Shin-Etsu Leads with Thermal Stability and Financial Strength

Shin-Etsu Chemical remains the global benchmark in cellulose ethers through its SE Tylose network. In May 2025, the company initiated a ¥500 billion share buyback representing approximately 6.4% of market capitalization and increased its dividend payout target to 40%, reflecting strong cash generation from specialty materials. Its Tylose HEMC grades are positioned for extreme climate construction in the Middle East and Africa, where higher gelation temperatures deliver performance stability under elevated ambient conditions. Deployment of a biomass cogeneration system in Rayong, Thailand is projected to reduce CO2 emissions by 48,000 tons annually. With an equity ratio exceeding 82% as of March 2026, Shin-Etsu retains significant capacity for strategic expansion in Germany and Japan.

Dow Optimizes Portfolio Around High-Value Construction Additives

Dow Inc. is restructuring its operating model to prioritize high-margin downstream specialty additives. The Transform to Outperform initiative launched in January 2026 targets $2 billion in incremental EBITDA by 2028 through simplification and operational streamlining. WALOCEL HEMC products are engineered for efficient dissolution and high performance in cement-based plasters and tile adhesives, supporting modern dry-mix mortar systems. Dow’s European Asset Review is evaluating upstream rationalization to reinforce its specialty materials focus. The company now sources more than 1,000 megawatts of renewable electricity, accounting for over half of its purchased power, strengthening its sustainability positioning in cellulose derivatives.

Lotte Fine Chemical Expands Green Materials and IT Applications

Lotte Fine Chemical is repositioning its cellulose ether portfolio toward green and high-purity materials. The Fine Chemical division reported KRW 439.1 billion in 2025 revenue, with margin recovery expected as inventory normalization concludes. MECELLOSE HEMC grades dominate infrastructure projects across South Korea and Southeast Asia due to optimized water retention and improved mortar workability. Group leadership has designated 2026 as a turning point for expansion into food, pharmaceutical, and semiconductor-related materials. Production scaling at Yeochun and Ulsan supports rising demand from AI hardware and advanced construction sectors, reinforcing Lotte’s move away from commodity petrochemicals.

Nouryon Strengthens Localized Innovation and Bio-Based Ingredients

Nouryon operates a decentralized development model centered on regional customer collaboration. In November 2025, the company opened a new Innovation Center in Shanghai, significantly expanding its technical capabilities for construction and pharmaceutical clients. Plans for an additional polymer innovation center in Tianjin in 2026 will accelerate product co-development for Asian markets. Nouryon recently launched fully bio-based cellulose-derived detergent ingredients and received sustainability recognition from Henkel. Expansion into Brazil through a new customer experience center strengthens its footprint in home and personal care applications, supporting diversified hydroxyethyl methyl cellulose demand.

Ashland Prioritizes Pharmaceutical-Grade Cellulose Ethers

Ashland has shifted its strategy toward higher-margin life sciences applications, exiting lower-return construction segments. In early 2026, the company narrowed its revenue outlook following divestitures but improved margin quality through portfolio optimization. Under the Benecel brand, Ashland is promoting parenteral and tablet-coating cellulose excipients aligned with pharmaceutical sector growth. The company appointed Tilley Distribution as its exclusive U.S. partner for food and beverage ingredients to strengthen hydrocolloid distribution. By concentrating on regulated pharmaceutical and personal care markets, Ashland is reinforcing its leadership in premium hydroxyethyl methyl cellulose applications.

Wacker Chemie Transitions Toward Specialty and Energy Efficiency

Wacker Chemie is executing the PACE restructuring program, targeting €300 million in annual savings by 2027 and reducing workforce levels to stabilize profitability. Although reporting a preliminary €800 million net loss in 2025 due largely to asset impairments, the company maintained balanced net cash flow through inventory optimization. Its VINNAPAS and HYDROMAR systems pair HEMC with dispersible polymer powders to deliver integrated green building solutions. Wacker is narrowing its focus to specialty chemicals and semiconductor-grade materials to counter high European energy costs. This transition positions the company to compete in performance-driven hydroxyethyl methyl cellulose systems rather than volume-based commodity segments.

South Korea: Premium Construction Focus and Digitally Optimized Production

South Korea has positioned itself as a high-value producer in the hydroxyethyl methyl cellulose industry, led by strategic capacity expansion and ESG-aligned manufacturing. In its August 2025 update, Lotte Fine Chemical reaffirmed its 2030 Roadmap ambition to rank among the global top ten specialty chemical companies. This strategy prioritizes the expansion of cellulose derivatives facilities with a clear emphasis on high-performance HEMC grades engineered for premium construction applications, where workability, water retention, and viscosity control directly influence contractor productivity and finished surface quality.

Operational excellence has become a differentiator. Lotte Fine Chemical integrated its MECELLOSE® HEMC and HPMC portfolio into its Green Materials division by mid-2025, aligning product development with LEED and BREEAM certification requirements demanded by global developers. The rollout of AI-based predictive maintenance across the Ulsan plant during 2024–2025 improved batch consistency for pharmaceutical-grade HEMC by more than 12%, reinforcing trust among regulated-market buyers. Looking ahead, the company is evaluating the use of green ammonia in nitrogen-enrichment steps for specialty cellulose ethers to reduce lifecycle emissions in its 2026 product lines, while recognition from the Korea Corporate Governance Service has strengthened its credibility with European pharmaceutical customers.

China: Localization Mandates and Industrial Digitalization

China remains the largest growth engine for HEMC, driven by policy-led localization and application diversification. In November 2025, Nouryon inaugurated an expanded innovation center in Shanghai, more than doubling previous capacity and establishing a dedicated Bermocoll® HEMC laboratory. This facility is tailored to optimize water-based paints and coatings for Asia-Pacific climatic conditions, addressing humidity, temperature variation, and rapid urban construction cycles.

Policy momentum has accelerated domestic substitution. Under the Ministry of Industry and Information Technology culmination of the Made in China 2025 program, authorities are targeting 70% domestic content in core materials. This has catalyzed aggressive expansion by local HEMC producers in Shandong and Jiangsu to replace high-end European imports. Regulatory pressure is also intensifying. The MIIT’s December 2025 proposal to expand the China RoHS catalogue is forcing HEMC suppliers to certify hazardous-substance-free additive systems for electronics and appliance assembly. Parallel investments in industrial digitalization hubs have positioned HEMC as a functional component in emerging applications such as construction-grade 3D printing inks and cellulose-based stabilizers for advanced nylon recycling projects linked to Sinopec loopamid® operations.

Germany: Regulatory Transparency and Performance-Led Innovation

Germany’s HEMC market is shaped by regulatory rigor and innovation in coatings and excipient applications. At the European Coatings Show in April 2025, Nouryon launched Bermocoll® EHM MAX, a next-generation HEMC rheology modifier that demonstrated up to 10% higher efficiency in architectural paints during field trials. This performance gain is particularly relevant as German formulators seek to reduce dosage while maintaining sag resistance and open time under tightening environmental standards.

Regulatory transparency is becoming a strategic factor. The European Chemicals Agency announced that from July 2026 it will publish company names in the C&L Inventory, prompting German exporters to audit and strengthen their compliance documentation. At the policy level, the EU Chemicals Industry Action Plan launched in July 2025 includes simplification measures for CLP and Cosmetics Regulations, offering cost relief for manufacturers of high-purity HEMC excipients. Looking forward, the proposed Advanced Materials Act expected in late 2026 is likely to stimulate demand for bio-based HEMC in aerospace and automotive composites, extending the material’s relevance beyond traditional construction and coatings.

United States: Nearshoring, Low-VOC Enforcement, and Infrastructure Innovation

The United States HEMC industry is being reshaped by supply chain resilience strategies and regulatory enforcement in coatings. In 2025, Ashland Inc. introduced Culminal™ Plus 3540PF, a modified HEMC grade optimized for premium cementitious tile adhesives. Designed for extended open time and visual workability in extreme heat, the product addresses performance challenges in large-format tiling across the Sun Belt construction markets.

Trade and regulatory forces are reinforcing domestic investment. Tariff adjustments implemented in 2025 prompted U.S. producers to accelerate nearshoring and expand local cellulose ether capacity to stabilize pricing amid volatile wood pulp costs. Concurrently, upcoming 2026 low-VOC standards enforced by the Environmental Protection Agency have driven a 15% increase in R&D spending on HEMC stabilizers that enable zero-VOC waterborne paint systems. Beyond coatings, the U.S. Department of Energy highlighted HEMC-modified concrete inks in 2025 as a key enabler for large-scale 3D-printed housing, positioning HEMC as a functional additive in next-generation infrastructure.

Japan: Pharmaceutical Compliance and Advanced Materials Synergies

Japan’s HEMC industry is anchored in pharmaceutical precision and advanced materials integration. In October 2025, Shin-Etsu Chemical released expanded technical documentation for METOLOSE® cellulose ethers, focusing on enteric coating systems and advanced tabletting guidance for regulated drug formulations. This technical depth supports formulators navigating increasingly complex dissolution and bioavailability requirements.

Regulatory alignment has enhanced export potential. During 2024–2025, Shin-Etsu AQOAT® was newly listed in the European Pharmacopoeia 11.4, enabling Japanese-made HEMC derivatives to be used in medicines marketed across Europe without additional qualification hurdles. Beyond pharmaceuticals, Shin-Etsu’s 2025 announcement of recyclable thermoplastic silicone materials highlighted the use of cellulose-based binders to maintain structural stability during injection molding. This cross-material synergy underscores Japan’s focus on integrating HEMC into advanced, circular material systems rather than competing on construction volume alone.

Comparative Snapshot: Hydroxyethyl Methyl Cellulose Industry by Country

Hydroxyethyl Methyl Cellulose Market County Level Snapshot

|

Country

|

Strategic Priority

|

Key Driver

|

Industry Implication

|

|

South Korea

|

Premium construction and ESG

|

AI-driven efficiency and green materials

|

Higher margins and export credibility

|

|

China

|

Localization and scale

|

MIIT content targets and digital hubs

|

Volume leadership with rising compliance

|

|

Germany

|

Regulatory transparency and performance

|

CLP enforcement and coatings innovation

|

High-efficiency, high-cost positioning

|

|

United States

|

Supply chain resilience and low-VOC

|

Nearshoring and infrastructure innovation

|

Domestic capacity growth and R&D intensity

|

|

Japan

|

Pharmaceutical precision

|

EP listing and technical specialization

|

Strong role in regulated drug markets

|

Hydroxyethyl Methyl Cellulose Market Report Scope

Hydroxyethyl Methyl Cellulose Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$66.6 Million

|

|

Market Size (2034)

|

$138.8 Million

|

|

Market Growth Rate

|

8.5%

|

|

Segments

|

By Grade (Industrial Grade, Pharmaceutical Grade, Food Grade, Cosmetic Grade), By Application (Construction Materials, Paints & Coatings, Pharmaceuticals, Personal Care, Food & Beverages, Industrial Specialties), By Physical Form (Powder, Granules, Liquid / Dispersion)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shin-Etsu Chemical Co., Ltd., Lotte Fine Chemical Co., Ltd., Ashland Inc., Dow Inc., Nouryon B.V., Associated British Foods plc, Zhejiang Haishen New Materials Co., Ltd., Shandong Head Pharmaceutical Co., Ltd., Celotech Chemical Co., Ltd., Lamberti S.p.A., Yil-Long Chemical Group, Wuxi Sanyou New Material Technology Co., Ltd., Zhejiang Kehong Chemical Co., Ltd., Reliance Cellulose Products Ltd., SE-Tylose GmbH & Co. KG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hydroxyethyl Methyl Cellulose Market Segmentation

By Grade

- Industrial Grade

- Pharmaceutical Grade

- Food Grade

- Cosmetic Grade

By Application

- Construction Materials

- Paints & Coatings

- Pharmaceuticals

- Personal Care

- Food & Beverages

- Industrial Specialties

By Physical Form

- Powder

- Granules

- Liquid / Dispersion

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Hydroxyethyl Methyl Cellulose Industry

- Shin-Etsu Chemical Co., Ltd.

- Lotte Fine Chemical Co., Ltd.

- Ashland Inc.

- Dow Inc.

- Nouryon B.V.

- Associated British Foods plc

- Zhejiang Haishen New Materials Co., Ltd.

- Shandong Head Pharmaceutical Co., Ltd.

- Celotech Chemical Co., Ltd.

- Lamberti S.p.A.

- Yil-Long Chemical Group

- Wuxi Sanyou New Material Technology Co., Ltd.

- Zhejiang Kehong Chemical Co., Ltd.

- Reliance Cellulose Products Ltd.

- SE-Tylose GmbH & Co. KG

*- List not Exhaustive