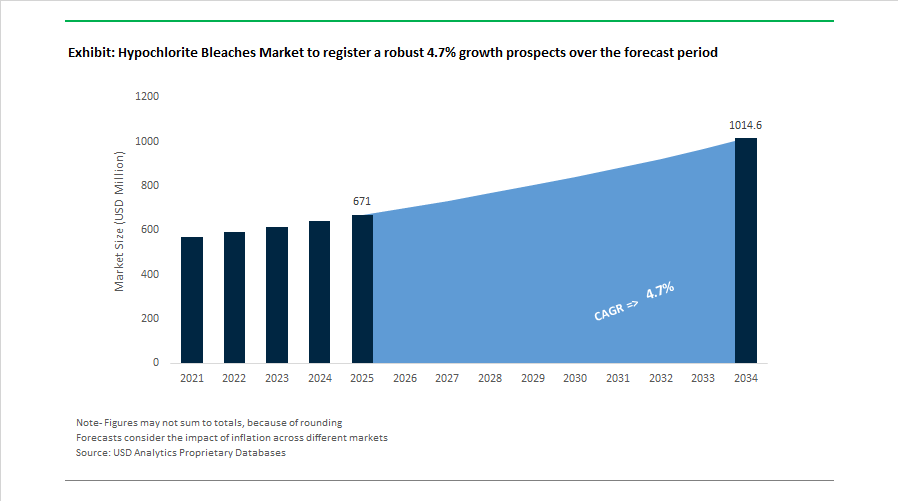

Hypochlorite Bleaches Market to Reach $1,014.5 Million by 2034 at 4.7% CAGR Amid Chlor-Alkali Consolidation, Trade Realignment, and Purity Upgrades

The Hypochlorite Bleaches Market is projected to grow from $671 Million in 2025 to $1,014.5 Million by 2034, expanding at a CAGR of 4.7%. Market growth is being shaped by chlor-alkali industry consolidation, regulatory tightening in healthcare-grade disinfection, municipal water treatment expansion, and shifting global trade flows. Sodium hypochlorite and calcium hypochlorite remain critical for public sanitation, drinking water treatment, textiles, agriculture, and household bleach formulations, while supply-side restructuring is redefining regional competitiveness.

In 2024, India’s domestic sodium hypochlorite production surpassed 500,000 tons, driven by large-scale state supply contracts for rural sanitation and municipal water treatment projects, including initiatives led by Gujarat Alkalies and Chemicals Ltd. The same year, Tianjin Chemical expanded capacity in China by 50,000 tons annually, contributing to Chinese hypochlorite exports exceeding 620,000 metric tons, reinforcing China’s role as a leading supplier to agriculture and textile sectors. In Europe, BASF completed a technical upgrade at its Cologne facility in 2024 to enhance production of high-purity hypochlorite solutions, addressing stringent contaminant thresholds required in healthcare and public sanitation applications. During 2024–2025, Kuehne Company implemented advanced membrane cell technology across its U.S. plants, improving bleach purity standards while reducing energy consumption, setting new operational benchmarks for domestic suppliers.

Trade policy and capacity rationalization intensified in 2025. The United States introduced new tariffs on imported chlorinated compounds, including calcium hypochlorite grades, triggering accelerated domestic capital expenditure to reduce reliance on Asian imports. In July 2025, Vynova ceased PVC production at its Beek site in the Netherlands as part of broader European chlor-vinyl rationalization, while reaffirming sodium hypochlorite and caustic soda as central to its sustainability strategy. In December 2025, Westlake Corporation announced shutdowns of multiple North American chlor-alkali and vinyl units, recording $415 million in restructuring costs with projected annual cash savings of $175 million by 2026, consolidating output into seven optimized facilities. During late 2025, Olin Corporation resolved the long-standing Shintech litigation, clearing financial uncertainty and enabling renewed focus on its value-over-volume commercial model. In parallel, The Clorox Company managed a complex ERP transition throughout 2025, resulting in elevated inventory levels followed by a planned drawdown in early 2026, with an expected temporary 6% to 10% reduction in fiscal 2026 net sales as channel inventories normalize.

Structural consolidation accelerated entering 2026. On January 2, 2026, Occidental Petroleum completed the $9.7 billion sale of OxyChem to Berkshire Hathaway, integrating one of North America’s largest sodium hypochlorite producers into a diversified industrial portfolio. This transaction represents one of the most significant ownership shifts in the U.S. chlor-alkali landscape. In December 2025, Aditya Birla Chemicals highlighted its integrated calcium and sodium hypochlorite capabilities at Fi Europe, targeting food-grade disinfection markets across Europe and Asia. These developments underscore a market defined by high-purity manufacturing, regional capacity optimization, and strategic ownership realignment within the global hypochlorite bleaches value chain.

Hypochlorite Bleaches Market Trends and Opportunities Transforming Disinfection and Water Treatment Applications

Regulatory Pressure Reshaping Hypochlorite Bleach Formulations Toward Stabilized and Lower-Concentration Solutions

The hypochlorite bleaches market is undergoing significant reformulation as regulators tighten safety and environmental standards around chlorine-based disinfectants. High-concentration sodium hypochlorite bleach solutions, historically used in industrial sanitation and water treatment, are increasingly being replaced with stabilized, lower-concentration formulations to minimize hazardous off-gassing, chlorine gas formation, and skin irritation risks. This regulatory-driven shift is encouraging manufacturers to focus on improved chemical stabilization technologies rather than simply increasing active chlorine concentrations to maintain efficacy.

Recent policy updates illustrate the direction of the market. In October 2025, the European Commission’s Implementing Decision (EU) 2025/2214 under the Biocidal Products Regulation (BPR) evaluated the “HYPO-CHLOR Product Family,” emphasizing that manufacturers must demonstrate long-term efficacy of aged sodium hypochlorite formulations rather than compensating for degradation through higher concentrations. Similarly, under the U.S. EPA’s revised hazardous materials transport framework (2024–2025), stricter rules for transporting 12.5% high-strength liquid bleach are accelerating the adoption of sub-8% household and commercial bleach formulations with improved safety profiles. At the same time, the European Chemicals Agency (ECHA) extended authorization for calcium hypochlorite-based biocidal products through 2035, encouraging European producers to invest in solid hypochlorite bleach formats, which provide greater chemical stability and easier regulatory compliance under REACH safety standards.

Expanding Water Treatment Infrastructure Sustaining Global Demand for Sodium Hypochlorite Disinfectants

Global investments in municipal water treatment infrastructure and sanitation programs continue to underpin long-term demand for hypochlorite bleach solutions, particularly sodium hypochlorite used in drinking water disinfection. As urban populations expand and governments prioritize safe drinking water access, hypochlorite-based disinfectants remain the most widely used and cost-effective chlorine source for large-scale water treatment systems. Their ability to maintain residual chlorine levels within distribution networks makes them essential for preventing microbial regrowth and ensuring safe potable water delivery.

Government initiatives are significantly expanding this demand base. In India, the Jal Jeevan Mission program aims to deliver piped drinking water to all rural households, driving the water disinfection chemicals market toward approximately $2.8 billion by late 2025. Sodium hypochlorite is widely used in these systems due to its affordability and effectiveness in point-of-entry water treatment facilities. In the United States, municipal infrastructure upgrades are also increasing bleach consumption. For example, procurement records from the City of Peekskill (October 2025) indicate routine purchases of approximately 40,000 gallons of 12.5% sodium hypochlorite annually for a medium-sized water treatment plant. Globally, water infrastructure spending is projected to approach $1 trillion by 2033, with a significant portion dedicated to secondary disinfection processes where sodium hypochlorite maintains residual chlorine levels between 0.2 and 0.4 ppm across distribution networks.

Stabilization Technologies Creating New Value Opportunities in Long-Shelf-Life Hypochlorite Bleach Formulations

The inherent chemical instability of liquid hypochlorite bleach solutions has created a growing opportunity for advanced stabilization technologies that extend shelf life and reduce product degradation. Sodium hypochlorite can lose up to 20% of its active chlorine concentration within one week at high strengths, particularly in warm climates or under poor storage conditions. As a result, manufacturers and research institutions are developing novel stabilizers, controlled-release precursors, and optimized concentration ranges to improve product reliability across industrial, municipal, and household applications.

Recent research breakthroughs highlight this opportunity. A 2025 study by Pham et al. demonstrated that powdered high-assay calcium hypochlorite can function as a stable precursor for hypochlorous acid (HOCl), achieving a 99.4% conversion rate within 10 seconds when mixed with water while delivering a shelf life exceeding 24 months, far surpassing traditional liquid bleach. Field research conducted in Ethiopia and Nigeria during 2025 also confirmed that pH-stabilized 1.25% hypochlorite solutions remain effective for up to 12 months in high-temperature climates, supporting their use in household water treatment (HWT) kits distributed by NGOs and public health agencies. Corporate strategies are also aligning with this shift. Following the 2025 merger of NCH and Solenis, the combined entity highlighted that sodium hypochlorite solutions below 7.5% available chlorine offer superior long-term stability, creating a new product category of professional-grade stabilized bleach solutions for healthcare, hospitality, and sanitation markets.

On-Site Electrochemical Generation Systems Transforming Hypochlorite Disinfectant Supply Chains

A major technological opportunity in the hypochlorite bleaches market lies in on-site generation (OSG) systems, which produce sodium hypochlorite directly at the point of use using brine and electricity. This approach eliminates the logistical risks associated with transporting bulk chlorine or high-strength bleach while ensuring a continuous supply of disinfectant for water treatment facilities, industrial plants, and maritime applications. As safety regulations around chemical transport tighten globally, electrochemical hypochlorite generation systems are gaining traction as a safer and more cost-efficient alternative.

Large-scale municipal deployments are already demonstrating the viability of this model. The city of Prague recently implemented an on-site sodium hypochlorite generation system capable of treating 3,000 liters of water per second for approximately 800,000 residents, eliminating the need to transport hazardous chlorine gas through urban environments. Advances in membrane-cell electrolysis technology are also improving system efficiency, reducing electricity consumption by approximately 15% compared to older open-cell systems, while producing a stable 0.8% sodium hypochlorite solution considered non-hazardous for storage and handling. In the maritime sector, International Maritime Organization (IMO) ballast water regulations are driving adoption of electrochlorination systems integrated into new vessel builds, creating a specialized but rapidly expanding market segment where hypochlorite disinfectant is generated directly on board rather than supplied through traditional chemical distribution networks.

Hypochlorite Bleaches Market Share and Segmentation Insights

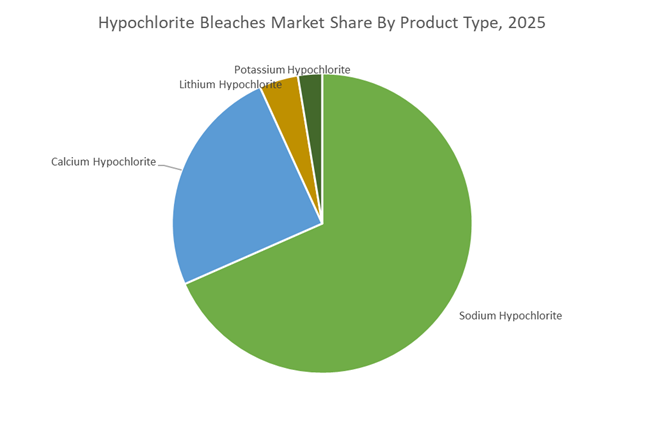

Sodium Hypochlorite Dominates the Market Through Broad Disinfection and Sanitation Applications

Sodium hypochlorite accounted for 68.40% of the Hypochlorite Bleaches Market share in 2025, making it the most widely used hypochlorite bleach product across global sanitation and disinfection applications. Sodium hypochlorite is extensively utilized because it provides high oxidizing strength, strong antimicrobial activity, and cost-efficient large-scale production, making it suitable for household cleaning, municipal water disinfection, industrial sanitation, and textile bleaching processes. The compound is typically produced through the chlorination of sodium hydroxide, allowing integration with existing chlorine production infrastructure and enabling reliable global supply. Its liquid form also simplifies dosing in water treatment systems and industrial cleaning operations. In 2025, a key structural shift in the market is the growing adoption of on-site sodium hypochlorite generation systems, particularly in municipal water utilities and large industrial facilities. These systems generate sodium hypochlorite from salt, water, and electricity using electrochlorination, eliminating the need to transport or store large volumes of concentrated bleach solutions. On-site production improves operational safety, reduces chemical transportation risks, and lowers long-term supply chain costs while maintaining effective disinfection performance.

Water Treatment Drives the Largest Demand for Hypochlorite Bleach Chemicals

Water Treatment represented 34.80% of the Hypochlorite Bleaches Market share in 2025, establishing it as the largest application segment for hypochlorite-based disinfectants. Hypochlorite compounds, particularly sodium hypochlorite, are widely used for municipal drinking water disinfection, wastewater treatment, and industrial water sanitation, where they effectively destroy bacteria, viruses, and other pathogenic microorganisms. The chemical’s strong oxidizing properties allow it to neutralize organic contaminants and prevent microbial growth in large-scale water distribution systems. As global urbanization increases and regulatory authorities tighten drinking water safety standards, water utilities continue expanding disinfection infrastructure, directly increasing hypochlorite consumption. In 2025, a critical advantage of hypochlorite disinfection lies in its ability to provide residual protection within water distribution networks, maintaining antimicrobial activity as treated water travels from treatment plants to consumer endpoints. Although advanced disinfection technologies such as ultraviolet and ozone treatment are gaining adoption, these systems do not provide residual protection. Consequently, hypochlorite remains an essential secondary disinfectant in water systems worldwide, ensuring continuous microbial control throughout municipal and industrial water supply networks.

Competitive Landscape in Hypochlorite Bleaches Market

Olin Corporation Prioritizes ECU Optimization and Contract Discipline

Olin Corporation remains the structural anchor of global sodium hypochlorite supply through its scale in chlor-alkali production. In its February 2026 10-K, the Chlor Alkali Products and Vinyls segment represented 54% of total company sales, within $11.2 billion in 2025 group revenue. The company’s value-over-volume strategy centers on maximizing electrochemical unit netbacks by favoring high-margin bleach contracts rather than lower-value liquid chlorine spot sales. In late 2025, Olin terminated the Blue Water Alliance joint venture with Mitsui to regain direct control over ECU trading and bleach distribution channels. With nearly 7,849 employees and a hydrogen joint venture with Plug Power, Olin is advancing partial decarbonization of energy-intensive electrolysis operations.

OxyChem Gains Capital Stability Under Berkshire Hathaway

OxyChem entered a new phase on January 2, 2026, when Occidental Petroleum completed the $9.7 billion sale of the business to Berkshire Hathaway. This transition provides long-term capital stability and strategic independence from upstream oil exposure. OxyChem is a leading U.S. supplier of high-strength sodium hypochlorite at concentrations between 12.5 and 15%, widely used in municipal water treatment across the Southern United States. Its integrated Gulf Coast manufacturing footprint reduces logistics costs for bulk bleach shipments. Beyond liquid bleach, OxyChem supports chlorinated isocyanurate and sodium gluconate production, strengthening its role in pool sanitation and industrial treatment markets.

Westlake Optimizes Chlorovinyl Footprint for Margin Recovery

Westlake Corporation is restructuring its Performance and Essential Materials segment to recover profitability after a challenging 2025 marked by lower chlorine pricing and elevated energy costs. The company targets a $600 million EBITDA improvement in 2026 through footprint optimization and cost discipline. In the fourth quarter of 2025, Westlake shut down three chlorovinyl production facilities in North America to address market overcapacity in chlorine and bleach derivatives. The January 2026 acquisition of ACI strengthens its Housing and Infrastructure Products segment, where bleach-treated materials contribute to durability and sanitation compliance. Despite posting a net loss in 2025, Westlake maintains $2.9 billion in liquidity, supporting operational flexibility.

Nouryon Expands Integrated Manufacturing for Sustainable Bleaching

Nouryon is a leading European supplier of hypochlorite solutions integrated into pulp, paper, and detergent value chains. Its Integrated Manufacturing Model places bleach production facilities adjacent to pulp mills, most recently in Brazil, minimizing transport risk and lowering carbon intensity. In February 2026, the company introduced FinnFix PB MAX, a fully bio-based carboxymethylcellulose detergent ingredient often paired with hypochlorite systems. The opening of its expanded Shanghai Innovation Center enhances technical support for Asian textile and cleaning markets. Recognition from Henkel Consumer Brands in 2025 highlights Nouryon’s role in reducing lifecycle emissions across high-volume cleaning chemistries.

ICL Group Drives Growth in Calcium Hypochlorite Solids

ICL Group is a dominant global supplier of calcium hypochlorite, a solid-form bleach containing 65 to 70% available chlorine and favored for stability in remote or decentralized applications. Market growth is supported by global water infrastructure investments projected to exceed $1 trillion by 2033, increasing demand for reliable disinfection solutions. European Union authorization of calcium hypochlorite biocidal families through 2035 secures long-term EMEA access. ICL is expanding on-site hypochlorite generation systems for remote utilities, disrupting traditional bulk-liquid distribution and enhancing water security in developing regions.

Clorox Shapes Consumer and Professional Bleach Standards

The Clorox Company remains the most visible consumer-facing brand in hypochlorite bleach, influencing safety, packaging, and formulation standards. For fiscal year 2026, the company projects net sales between $6.5 billion and $6.8 billion after prior retailer inventory adjustments. Strategic focus has shifted fully to Cleaning and Professional segments following divestiture of its vitamins and supplements business in late 2025. The anticipated acquisition of GOJO is expected to expand Clorox’s professional disinfection portfolio. Its Professional division is accelerating adoption of low-odor, high-efficacy bleach wipes in healthcare environments, signaling a shift from bulk liquid formats toward specialized, application-ready delivery systems.

United States: Capacity Modernization and Regional Supply Chain Rebalancing

The United States hypochlorite bleaches industry is being reshaped by targeted capacity investments and selective rationalization across the chlor-alkali value chain. In mid-2025, Olin Corporation completed a $20 million modernization at its Niagara Falls, New York site, expanding advanced buildings dedicated to the HyPure® high-purity bleach line. This investment strengthens Olin’s competitive position in industrial-grade sodium hypochlorite, where purity stability and controlled decomposition rates are critical for municipal water treatment and industrial sanitation customers. Distribution efficiency has also improved. In June 2025, Olin and K2 Pure Solutions broadened their partnership across California and the Western United States, shortening delivery cycles for large-volume public utilities and reducing logistics-related degradation risks.

At the same time, capacity discipline is tightening. Westlake Corporation approved the shutdown of its diaphragm chlor-alkali unit at Lake Charles, Louisiana in December 2025, removing 825 million pounds of chlorine and 910 million pounds of caustic soda capacity from the market. This move is intended to raise utilization across Westlake’s remaining chlorovinyl assets and reduce exposure to lower-margin commodity bleach output. Regulatory pressure is adding an innovation layer. The Environmental Protection Agency initiated a 2026 review of secondary disinfectant efficacy standards, pushing producers to engineer more stable sodium hypochlorite formulations with lower chlorate formation and longer shelf life under variable storage conditions.

India: Integrated Chlorine Expansion and Rural Sanitation Focus

India’s hypochlorite bleaches industry is benefiting from large-scale upstream integration and policy support for water and sanitation infrastructure. In 2025, Grasim Industries announced the commissioning of major chemical assets at its Vilayat complex, including Epichlorohydrin and CPVC plants scheduled by March 2026. With total caustic soda and chlorine derivative capacity reaching 1,505 KTPA, Grasim has reinforced its position as the country’s largest integrated chlorine producer, ensuring feedstock security for stable bleaching powder and hypochlorite grades used across water treatment and textiles.

Market outreach and product specialization are expanding in parallel. Aditya Birla Chemicals showcased high-strength bleaching powder brands such as Aqua Armor and Rensa at the Riyadh Global Water Expo in September 2025, highlighting formulations designed for high-salinity aquaculture and municipal water systems. On the operational side, Gujarat Alkalies and Chemicals Ltd. introduced automated packaging lines for stable bleaching powder in late 2025, reducing dust exposure and improving shelf life for rural sanitation programs. Government backing remains strong. India’s 2026 industrial budget under the Atmanirbhar Bharat framework earmarked additional incentives for specialized bleaching powder hubs in Gujarat to support domestic textile and pulp and paper value chains.

China: Product Upgrading and Export-Oriented Optimization

China’s hypochlorite bleaches sector is moving from volume-led growth toward higher-value upgrading under coordinated industrial policy. The Ministry of Industry and Information Technology issued a joint petrochemical growth plan for 2025 to 2026 targeting a 5% average annual expansion of the chemical sector, with explicit emphasis on upgrading traditional products such as hypochlorite bleaches. This policy direction is favoring high-concentration calcium hypochlorite and specialty formulations over basic low-grade output.

Innovation infrastructure is supporting this shift. In November 2025, Nouryon opened a significantly expanded innovation center in Shanghai, featuring a dedicated laboratory for household and industrial cleaning solutions. The center focuses on co-developing bleach formulations optimized for Asia-Pacific climate conditions and regulatory requirements. Capacity discipline is also being enforced. Under 2026 MIIT guidelines, approvals for new chlor-alkali refining capacity are being tightly controlled, while producers are encouraged to optimize existing assets and channel output toward export-grade calcium hypochlorite for North American and Southeast Asian markets. Environmental efficiency gains are visible at Sinopec Jianghan Salt Chemical, which reduced energy consumption per ton of hypochlorite output by 12% in early 2025 through recycling workflow optimization aligned with national green manufacturing mandates.

European Union: Regulatory Compression and Low-Carbon Transition

The European Union hypochlorite bleaches market is increasingly shaped by regulatory compression and decarbonization objectives. Updates to the Biocidal Products Regulation in 2025 shortened renewal timelines and limited market availability to a maximum of 180 days following permit expiry. This has forced distributors and formulators of bleach-based biocides to streamline approval management and inventory planning to avoid product disruptions. Distribution structures are adapting accordingly. In December 2025, Nouryon partnered with IMCD to expand access to bleaching and sizing solutions across EMEA, improving reach to textile and leather processors seeking ISCC Plus-certified auxiliaries.

Labeling and hazard communication will become more complex. From November 2026, new CLP hazard classes including endocrine disruption will require reclassification and relabeling of existing hypochlorite products, triggering widespread packaging and compliance updates. Alongside regulatory pressure, sustainability is emerging as a competitive lever. Arkema reported progress in late 2025 on decarbonizing its European chlor-alkali operations, targeting a 15% reduction in CO2 intensity for sodium hypochlorite production by end-2026 through renewable energy procurement and process efficiency gains.

Comparative Snapshot: Hypochlorite Bleaches Industry by Country

Hypochlorite Bleaches Market County Level Snapshot

|

Region

|

Strategic Priority

|

Key Development

|

Competitive Implication

|

|

United States

|

Capacity discipline and stability

|

Olin modernization and Westlake shutdown

|

Higher utilization and formulation innovation

|

|

India

|

Integrated expansion

|

Grasim Vilayat complex and sanitation hubs

|

Feedstock security and domestic self-reliance

|

|

China

|

Product upgrading

|

MIIT capacity control and export focus

|

Shift toward high-value calcium hypochlorite

|

|

European Union

|

Regulatory tightening

|

BPR and CLP updates

|

Compliance-driven consolidation and relabeling

|

Hypochlorite Bleaches Market Report Scope

Hypochlorite Bleaches Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$671 Million

|

|

Market Size (2034)

|

$1014.5 Million

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Product Type (Sodium Hypochlorite, Calcium Hypochlorite, Potassium Hypochlorite, Lithium Hypochlorite), By Form (Liquid, Solid), By Concentration (Low Concentration, Medium Concentration, High Concentration), By Application (Household Cleaning & Laundry, Industrial Disinfection & Sanitation, Water Treatment, Textile Bleaching & Finishing, Pulp & Paper Processing, Agrochemicals), By End-Use Industry (Residential, Commercial, Institutional, Industrial)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Olin Corporation, The Clorox Company, Westlake Corporation, Grasim Industries Limited, Nouryon B.V., Arkema S.A., Solvay S.A., Nippon Soda Co., Ltd., Tosoh Corporation, Sinopec, Gujarat Alkalies and Chemicals Limited, INEOS Group, BASF SE, Occidental Petroleum Corporation, Kuehne Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hypochlorite Bleaches Market Segmentation

By Product Type

- Sodium Hypochlorite

- Calcium Hypochlorite

- Potassium Hypochlorite

- Lithium Hypochlorite

By Form

By Concentration

- Low Concentration

- Medium Concentration

- High Concentration

By Application

- Household Cleaning & Laundry

- Industrial Disinfection & Sanitation

- Water Treatment

- Textile Bleaching & Finishing

- Pulp & Paper Processing

- Agrochemicals

By End-Use Industry

- Residential

- Commercial

- Institutional

- Industrial

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Hypochlorite Bleaches Industry

- Olin Corporation

- The Clorox Company

- Westlake Corporation

- Grasim Industries Limited

- Nouryon B.V.

- Arkema S.A.

- Solvay S.A.

- Nippon Soda Co., Ltd.

- Tosoh Corporation

- Sinopec

- Gujarat Alkalies and Chemicals Limited

- INEOS Group

- BASF SE

- Occidental Petroleum Corporation

- Kuehne Company

*- List not Exhaustive