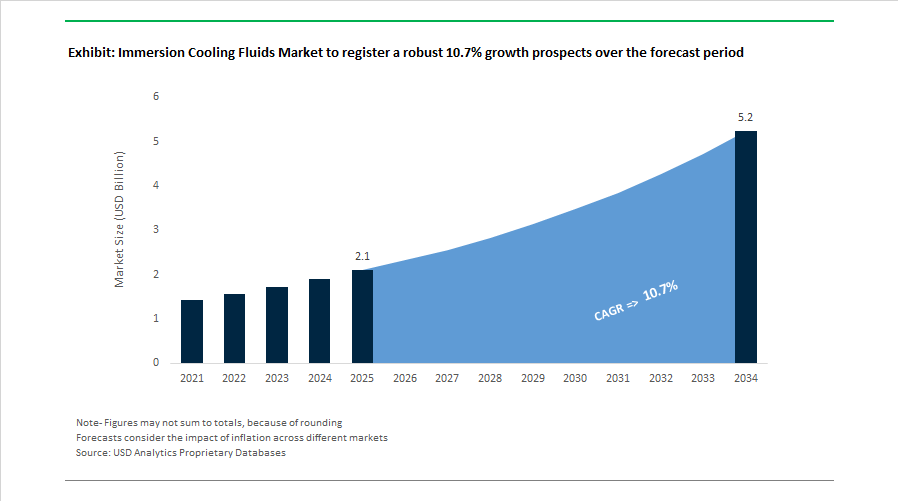

Immersion Cooling Fluids Market to Reach $5.2 Billion by 2034 at 10.7% CAGR Amid AI Data Center Expansion and PFAS Exit

The Immersion Cooling Fluids Market is projected to grow from $2.1 billion in 2025 to $5.2 billion by 2034, registering a robust CAGR of 10.7%. This accelerated expansion is being driven by hyperscale AI infrastructure, high-density GPU clusters, semiconductor manufacturing upgrades, and the structural shift away from air cooling toward liquid-based thermal management. The market has entered a transformative phase following the global phaseout of PFAS-based dielectric fluids, creating significant opportunities for hydrocarbon, synthetic, bio-based, and next-generation two-phase immersion chemistries.

In late 2024 and throughout 2025, Equinix partnered with Green Revolution Cooling to launch “Liquid-Ready” colocation zones, enabling enterprise AI deployments without full-scale facility redesign. In May 2025, Shell became the first lubricant manufacturer to receive official Intel certification for its single-phase immersion cooling fluids under the Immersion Warranty Rider program. This milestone removed hardware warranty barriers for Xeon processors and materially accelerated enterprise adoption of immersion technology. During the same month, Engineered Fluids, Iceotope, and Juniper Networks formed a strategic collaboration to optimize compatibility between dielectric coolants and high-speed networking hardware, addressing performance reliability under full submersion. In June 2025, Shell introduced DLC Fluid S3, a propylene glycol-based direct liquid cooling solution aligned with Open Compute Project PG25 specifications, enabling hybrid cooling architectures that combine direct-to-chip cooling with full-rack immersion systems.

Two-phase cooling gained strong commercial validation in 2025. In August 2025, Chemours announced that its Opteon two-phase immersion fluid was qualified by Samsung Electronics for advanced semiconductor manufacturing and AI training environments. Earlier in May 2025, Chemours signed a production agreement with Navin Fluorine International to secure manufacturing capacity beginning in 2026, ensuring scalable supply for its Liquid Cooling Venture. In October 2025, Castrol invested in Electronic Cooling Solutions to expand from fluid supply into system engineering and lifecycle services, reinforcing its Castrol ON dielectric fluid portfolio. At the 2025 Datacloud Global Congress, Castrol introduced a full lifecycle management service covering installation, monitoring, and disposal, targeting long-term fluid stability and sustainability compliance. Lubrizol reported large-scale deployments of its CompuZol single-phase fluids in June 2025, emphasizing enhanced material compatibility to prevent cable degradation in immersion environments. In November 2025, LiquidStack and Innovo launched modular immersion-cooled data center blocks optimized for high-temperature regions such as the Middle East.

A pivotal structural shift occurred in late 2025 when 3M finalized its exit from Novec and other PFAS-based engineered fluids. This development triggered a global supply chain transition, forcing operators to migrate toward hydrocarbon, synthetic ester, and hydrofluoroolefin-based alternatives. The transition is reshaping procurement strategies and accelerating qualification programs across hyperscalers. The immersion cooling fluids market is now characterized by certification-led adoption, two-phase boiling innovation, hybrid direct liquid cooling integration, lifecycle management services, modular data center deployment, and strategic production alliances designed to support AI-driven computational density.

Immersion Cooling Fluids Market Trends and Opportunities Shaping Next-Generation Data Center Cooling

Data Center Sustainability Regulations Accelerating Adoption of Single-Phase Immersion Cooling Fluids

The immersion cooling fluids market is witnessing accelerated growth as hyperscale data centers transition toward single-phase immersion cooling systems to meet energy efficiency mandates and rising rack power densities. Traditional air-cooling technologies are increasingly inadequate for modern AI and high-performance computing workloads, which generate significantly higher heat loads. As a result, dielectric immersion cooling fluids are emerging as a critical thermal management solution capable of delivering superior heat dissipation while significantly improving Power Usage Effectiveness (PUE) and overall data center energy efficiency.

Regulatory pressure is a major catalyst behind this shift. The EU Energy Efficiency Directive (EU) 2023/1791, implemented with reporting obligations starting May 15, 2025, requires data centers exceeding specified IT power thresholds to disclose detailed energy performance metrics, aligning with the EU’s target of 11.7% energy reduction by 2030. At the hardware level, next-generation AI infrastructure is further accelerating the adoption of immersion cooling. In late 2025, NVIDIA confirmed that its Blackwell GB200 NVL72 architecture, capable of 120 kW per rack, requires liquid cooling, while conventional air systems typically struggle beyond 20–30 kW per rack. Industry validation has also strengthened confidence in immersion cooling technologies. In May 2025, Intel certified Shell’s immersion cooling fluids for its 4th and 5th Gen Xeon processors, signaling enterprise readiness for large-scale deployments. Additionally, LiquidStack’s 2025 technical briefing demonstrated that single-phase immersion cooling systems can reduce data center capital expenditure by approximately 32%, primarily by eliminating large HVAC infrastructure and reducing facility footprint.

Purpose-Built Dielectric Fluid Formulations Emerging for High-Density AI and HPC Workloads

As the AI data center cooling market expands, the industry is shifting away from generic cooling oils toward specialized immersion cooling fluids engineered for specific hardware architectures. These next-generation formulations are designed to address material compatibility, high thermal flux environments, and long-term chemical stability. Purpose-built dielectric fluids allow operators to maintain optimal cooling performance for GPU clusters, AI accelerators, and high-density computing nodes, where rapid thermal fluctuations are common during machine learning training workloads.

Major technology providers are actively investing in specialized fluid development. In June 2025, Shell launched DLC Fluid S3, a propylene glycol-based cooling solution designed for Direct Liquid Cooling (DLC) environments, offering corrosion protection for copper heat sinks for more than six years of operational lifespan. Strategic collaborations are also shaping the market. In October 2025, LG Electronics signed a memorandum of understanding with SK Enmove and Green Revolution Cooling (GRC) to co-develop immersion cooling solutions optimized for AI Data Centers (AIDCs). The partnership focuses on customizing fluid viscosity and thermal conductivity properties to match the thermal profiles of next-generation GPU clusters. Meanwhile, nVent introduced a modular liquid cooling portfolio in November 2025, engineered to manage the rapid thermal ramping associated with AI training workloads, ensuring that cooling fluids respond instantly to spikes in heat generation without chemical degradation.

Biodegradable Ester-Based Dielectric Fluids Unlocking Opportunities in Edge Data Center Deployments

The expansion of edge computing infrastructure is creating new opportunities for environmentally safe immersion cooling fluids designed for deployment in urban and environmentally sensitive locations. Unlike hyperscale facilities located in remote regions, edge data centers are increasingly positioned near population centers, industrial facilities, and telecom networks. This proximity requires cooling solutions that minimize environmental risks in case of leaks or accidental discharge, driving demand for biodegradable and ester-based dielectric fluids.

Industry investments are already addressing this need. In October 2025, Castrol announced a strategic investment in Electronic Cooling Solutions (ECS) to accelerate the development of bio-synthetic ester-based immersion cooling fluids that provide strong dielectric performance while remaining biodegradable. Immersion technology is also expanding into adjacent energy infrastructure applications. In 2025, Shell partnered with QingAn Energy Storage (QAES) to develop an immersion-cooled Battery Energy Storage System (BESS) designed to prevent thermal runaway in high-density lithium-ion battery arrays. Additionally, deployment case studies from 2025 demonstrate that synthetic ester-based dielectric fluids offer superior moisture resistance compared to mineral oil alternatives, making them particularly suitable for edge data centers operating in high-humidity or coastal environments, where moisture intrusion could otherwise compromise system reliability.

Circular Economy Services and Fluid Lifecycle Management Creating New Revenue Streams

As the installed base of immersion cooling systems grows globally, the market is expanding beyond fluid supply toward fluid lifecycle management, monitoring, and recycling services. Dielectric fluids represent a significant portion of the operational costs of immersion cooling infrastructure, prompting data center operators to adopt predictive maintenance, fluid monitoring, and reclamation technologies that extend fluid lifespan and reduce waste.

New service-based business models are emerging in response. At EMO Hannover 2025, Castrol introduced SmartCoolant™, an automated immersion cooling fluid management system that monitors key parameters such as pH, conductivity, and concentration in real time while automating fluid replenishment. This technology helps prevent chemical degradation and minimizes the risk of premature fluid replacement. Complementing this innovation, Castrol launched a four-stage lifecycle service framework in early 2025, covering installation, laboratory-based maintenance testing, break-fix technical support, and certified disposal services. These initiatives reflect the growing Cooling-as-a-Service model, where fluid manufacturers manage the long-term chemical health of cooling systems. At the same time, chemical companies are investing in spent fluid regeneration technologies, enabling the purification and reuse of high-cost synthetic dielectric fluids, which can account for up to 20% of the total immersion cooling system cost over a decade of operation, reinforcing the circular economy within the global immersion cooling fluids market.

Immersion Cooling Fluids Market Share and Segmentation Insights

Single-Phase Immersion Cooling Fluids Lead Adoption Through Operational Simplicity in Data Center Thermal Management

Single-phase fluids accounted for 72.80% of the Immersion Cooling Fluids Market share in 2025, making them the dominant fluid technology for immersion-based data center cooling systems. These fluids, typically formulated from dielectric hydrocarbons, synthetic esters, or engineered dielectric liquids, operate without phase transition during the cooling process, circulating through heat exchangers to remove heat from high-performance electronic components. The technology is widely adopted in data center cooling infrastructure, high-density server racks, and high-performance computing clusters, where thermal management efficiency directly influences operational reliability. Compared with two-phase immersion cooling systems, single-phase designs offer simpler engineering architecture, lower capital costs, and easier integration with existing data center infrastructure, making them attractive to hyperscale operators and enterprise IT facilities. In 2025, manufacturers continue optimizing fluid formulations for long-term chemical stability, dielectric strength, oxidation resistance, and minimal viscosity degradation, enabling reliable cooling performance across thousands of thermal cycles in high-density computing environments.

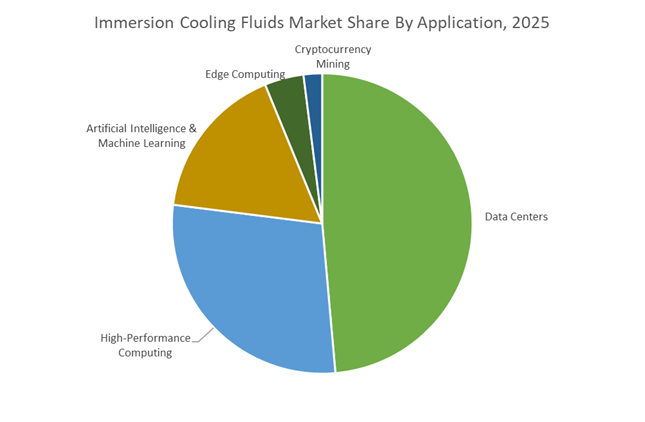

Data Centers Drive the Largest Demand for Immersion Cooling Fluids

Data Centers represented 48.60% of the Immersion Cooling Fluids Market share in 2025, establishing them as the primary application for advanced liquid cooling technologies. Modern data center facilities face rapidly increasing thermal loads as artificial intelligence, cloud computing, big data analytics, and machine learning workloads drive server power densities far beyond traditional cooling limits. Immersion cooling systems submerge servers directly into dielectric cooling fluids, enabling highly efficient heat removal while reducing reliance on power-intensive air conditioning systems. This technology significantly improves data center energy efficiency, power usage effectiveness (PUE), and cooling capacity per rack. In 2025, the rapid growth of AI training clusters and high-performance GPU deployments is pushing rack densities toward 50–100 kilowatts per rack and higher, levels that traditional air cooling systems struggle to manage effectively. As a result, hyperscale cloud providers, colocation operators, and enterprise data center developers are increasingly adopting immersion cooling technologies to support next-generation computing infrastructure while meeting sustainability targets and reducing overall energy consumption.

Competitive Landscape in Immersion Cooling Fluids Market

Shell Expands GTL-Based Immersion Ecosystem

Shell plc has rapidly positioned itself as a leader in data center immersion cooling fluids by leveraging its Gas-to-Liquids platform to produce high-purity synthetic dielectric fluids. In May 2025, Shell became the first fluid manufacturer to receive official Intel certification for use with 4th and 5th Gen Xeon processors, including an Immersion Warranty Rider that removes legal risk barriers for operators. In June 2025, Shell launched DLC Fluid S3, a propylene glycol-based direct-to-chip solution, broadening its portfolio beyond full immersion systems. A partnership with QingAn Energy Storage in October 2025 extended immersion technology into battery energy storage systems. Shell reports potential reductions of up to 48% in data center energy use and up to 80% reductions in cooling floor space.

Castrol Targets Lifecycle Thermal Management Services

Castrol, under BP plc, is repositioning from automotive lubricants to advanced thermal management services. At the Datacloud Global Congress, the company introduced a full lifecycle Fluid Management Service covering commissioning, laboratory analytics, break-fix support, and sustainable disposal. Its Castrol ON DC 15 single-phase dielectric coolant is engineered for low viscosity and rapid heat transfer in high-density GPU environments. Castrol’s Dipping Point research indicates that 74% of data center professionals view immersion cooling as essential for next-generation AI workloads. The company is strategically targeting 2027 as the inflection year when immersion cooling becomes standard in hyperscale facility design.

Chemours Leads Two-Phase Cooling Replacement Cycle

The Chemours Company is advancing two-phase immersion cooling through its Opteon line of fluorinated fluids. In February 2026, Chemours signed a joint development agreement with 2CRSi following successful qualification in high-density server environments. Two-phase systems utilizing Opteon fluids can achieve power usage effectiveness approaching 1.0 and deliver up to 90% cooling energy reduction compared to traditional air systems. With the withdrawal of competing Novec fluids, Chemours is positioned as a primary supplier for high-heat flux AI clusters. The company is implementing circular fluid recovery and reuse programs to address cost and environmental scrutiny surrounding fluorinated chemistries.

Cargill Advances Bio-Based Dielectric Alternatives

Cargill is leading the bio-based immersion cooling segment with Naturel dielectric fluids derived from renewable vegetable oils. These fluids feature flash points exceeding 300°C and are biodegradable and non-toxic, appealing to ESG-focused hyperscale operators. Cargill is expanding partnerships with Submer and Green Revolution Cooling to provide turnkey sustainable immersion systems, particularly for edge data centers in urban or environmentally sensitive locations. The company highlights superior heat-carrying capacity compared to air, enabling rack densities exceeding 100 kW. Regulatory stringency in Europe is reinforcing demand for bio-ester-based immersion solutions over synthetic hydrocarbon alternatives.

Engineered Fluids Differentiates Through Material Compatibility

Engineered Fluids maintains a specialized position by focusing on material compatibility and OEM neutrality. Its ElectroCool and AmpCool product lines are formulated to prevent degradation of elastomers, plastics, and seals commonly used in server assemblies. In 2025, the company introduced Synmerse DC, a cost-optimized single-phase fluid designed for industrial and crypto-mining applications. Development of a material compatibility database in collaboration with server manufacturers addresses operational risks such as O-ring failure associated with repurposed mineral oils. Engineered Fluids primarily serves customized high-performance computing deployments requiring tailored dielectric characteristics.

3M Exit Reshapes Two-Phase Supply Landscape

The strategic withdrawal of 3M from the Novec and Fluorinert fluid business at the end of 2025 represents a defining inflection point for the immersion cooling fluids market. Final order deadlines passed in March 2025, prompting widespread fluid replacement programs across global data centers during 2026. The exit created supply gaps in two-phase cooling applications, accelerating adoption of alternative low-global-warming-potential fluids from competitors. 3M has redirected significant PFAS-related research investment toward PFAS-free materials and advanced adhesives. This transition is reshaping procurement strategies, regulatory compliance frameworks, and long-term supply contracts across hyperscale and enterprise cooling ecosystems.

United States Immersion Cooling Fluids Market: Warranty Enablement, Federal Policy Momentum, and Specialty Chemistry Consolidation

The United States immersion cooling fluids industry entered a decisive commercialization phase in 2025, driven by formal processor certification, federal legislative attention, and upstream specialty chemical investments. In May 2025, Shell achieved an industry-first milestone when its immersion cooling fluids received official certification from Intel, enabling deployment under an Immersion Warranty Rider for Xeon processors. This certification materially lowered adoption risk for hyperscale and enterprise data centers by aligning immersion cooling fluids with OEM warranty frameworks, accelerating migration away from air-based thermal management for high-density AI and HPC workloads. The momentum strengthened further in November 2025 when ExxonMobil announced that its single-phase dielectric fluids were granted the “Intel Supported Immersion Fluids” designation following rack-scale validation at Intel’s Advanced Data Center Development Lab in Oregon, specifically targeting 5th Gen Intel Xeon processors.

Policy and ecosystem signals are reinforcing this technical validation. In September 2025, the U.S. House introduced H.R. 5332, the Liquid Cooling for AI Act of 2025, mandating a federal technology assessment of liquid cooling systems and the development of best-practice guidance for AI compute clusters. This legislative move effectively positions immersion cooling fluids within future federal AI infrastructure standards. At the materials layer, Ashland Inc. finalized a $60 million investment to optimize specialty chemical manufacturing in Virginia, focusing on high-purity binders and additives that improve dielectric fluid stability and oxidation resistance. Complementing this, ExxonMobil launched a $100,000 global open innovation challenge via the Wazoku platform to identify non-conductive, low-viscosity, and PFAS-free immersion fluids, highlighting the U.S. market’s pivot toward next-generation, regulation-ready formulations.

China Immersion Cooling Fluids Market: PUE Mandates and Policy-Enforced Adoption at Scale

China represents one of the most policy-driven immersion cooling fluid adoption environments globally, with energy efficiency mandates acting as a direct demand catalyst. Under the Ministry of Industry and Information Technology Green Manufacturing blueprint, newly built national hub data centers are required to achieve an average Power Usage Effectiveness of 1.25 or lower by the end of 2025. This threshold has effectively made immersion cooling fluids a core compliance solution, as operators target near-unity PUE levels that are difficult to achieve with air or hybrid cooling systems. The regulatory push is reinforced by infrastructure planning under the East Data West Computing initiative, which prioritizes liquid-cooled data centers in renewable-rich regions such as Inner Mongolia and Gansu, where waterless cooling provides both energy and resource advantages.

Technology qualification is advancing in parallel. In August 2025, Samsung Electronics successfully qualified Chemours Opteon two-phase immersion cooling fluid for generation four SSDs, marking Samsung’s first approval of a two-phase dielectric fluid. Qualification testing for next-generation DDR memory modules is scheduled for early 2026, signaling deeper integration of immersion cooling fluids into core semiconductor platforms. Additionally, China’s Green Electricity Certificate system, which became the sole official proof of renewable consumption in March 2025, now requires immersion-cooled data centers to align fluid-related energy efficiency metrics with auditable GEC records. This linkage between cooling fluids, energy accounting, and operating licenses further embeds immersion cooling into China’s regulated digital infrastructure.

Singapore Immersion Cooling Fluids Market: Tropical Standards and Incentivized Efficiency Upgrades

Singapore’s immersion cooling fluids market is shaped by climatic constraints and tightly defined efficiency standards rather than scale-driven mandates. In August 2025, the Infocomm Media Development Authority introduced SS 715:2025, a national standard for energy-efficient IT equipment in tropical environments. The standard requires safe and stable operation at ambient temperatures up to 35 degrees Celsius, effectively favoring immersion cooling fluids with high thermal stability, low volatility, and consistent dielectric performance under sustained heat loads. This has positioned immersion cooling as a practical pathway for maintaining reliability in high-density data halls under tropical conditions.

Financial incentives complement regulatory guidance. Singapore’s 2025 industrial budget rolled out the Energy Efficiency Grant, explicitly co-funding upgrades to liquid-cooled IT infrastructure. The grant is designed to help the data center sector achieve a targeted 20% improvement in PUE by late 2025, accelerating retrofit projects that integrate immersion cooling fluids into existing facilities. As a result, Singapore is emerging as a reference market for immersion cooling deployment in hot and humid regions, with strong emphasis on fluid longevity, material compatibility, and operational safety.

European Union Immersion Cooling Fluids Market: Carbon Neutrality, PFAS Transition, and Heat Reuse Integration

The European Union immersion cooling fluids landscape is being redefined by sustainability regulation and material substitution pressures. In the first quarter of 2026, the European Commission announced a comprehensive Data Centre Energy Efficiency Package aimed at achieving carbon-neutral data centers by 2030. Mandatory reporting of water usage and waste heat reuse directly favors immersion cooling fluids, which minimize water dependency and enable efficient heat capture. Under the revised Energy Efficiency Directive, large-scale data centers are increasingly incentivized to channel waste heat from immersion systems into district heating networks in cities such as Amsterdam and Dublin, integrating cooling fluids into broader urban energy systems.

Simultaneously, the mandatory phase-out of all 3M Novec products by December 31, 2025 has triggered an urgent transition toward PFAS-free dielectric fluids. In response, equipment manufacturers and fluid suppliers such as Inventec and Best Technology have introduced drop-in immersion fluids like THERMASOLV, designed to replace legacy Novec chemistries without extensive system redesign. This regulatory-driven substitution is reshaping supplier qualification processes and accelerating innovation in sustainable immersion cooling fluid chemistries across the EU.

India Immersion Cooling Fluids Market: Localization Strategy and Specialty Chemical Export Orientation

India’s immersion cooling fluids industry is at an early but strategically important stage, anchored in manufacturing localization and specialty chemical ecosystem development. In May 2025, Chemours entered into a strategic manufacturing agreement with Navin Fluorine International to produce Opteon two-phase immersion cooling fluids domestically. Commercial-scale capacity is expected to be fully operational by early 2026, positioning India as a supply base for the broader Asia-Pacific region and reducing dependence on imported dielectric fluids.

At the policy level, the Gujarat government has designated Specialty Chemical Hubs in Dahej, offering tax rebates and infrastructure support for producers of biodegradable and ester-based immersion cooling fluids. These hubs are explicitly oriented toward export-grade specialty chemicals, aligning immersion cooling fluids with India’s broader ambition to become a global specialty chemicals manufacturing center. This combination of localized fluorochemical production and incentives for sustainable formulations places India as an emerging node in global immersion cooling fluid supply chains.

Immersion Cooling Fluids Industry: Country-Level Strategic Summary

Immersion Cooling Fluids Market County Level Snapshot

|

Region

|

Primary Adoption Driver

|

Key Industrial Development

|

Regulatory or Policy Lever

|

|

United States

|

OEM warranty certification and AI policy focus

|

Intel-certified fluids, specialty chemical consolidation

|

Liquid Cooling for AI Act, EPA alignment

|

|

China

|

Mandatory energy efficiency thresholds

|

Two-phase fluid qualification, renewable-linked siting

|

MIIT PUE mandates, GEC compliance

|

|

Singapore

|

High ambient temperature resilience

|

Standards-driven immersion adoption

|

SS 715:2025, Energy Efficiency Grant

|

|

European Union

|

Carbon neutrality and PFAS substitution

|

Drop-in PFAS-free fluids, heat reuse systems

|

EED, Data Centre Energy Efficiency Package

|

|

India

|

Localization and export-oriented specialty chemicals

|

Domestic two-phase fluid manufacturing

|

State-level chemical hub incentives

|

Immersion Cooling Fluids Market Report Scope

Immersion Cooling Fluids Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.1 Billion

|

|

Market Size (2034)

|

$5.2 Billion

|

|

Market Growth Rate

|

10.7%

|

|

Segments

|

By Fluid Type (Single-Phase Fluids, Two-Phase Fluids), By Chemistry (Hydrocarbon-Based, Fluorocarbon-Based, Synthetic Esters, Bio-Based Fluids), By Cooling Technique (Macro-Immersion, Micro-Immersion), By Application (High-Performance Computing, Artificial Intelligence & Machine Learning, Cryptocurrency Mining, Data Centers, Edge Computing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shell plc, Exxon Mobil Corporation, The Chemours Company, Castrol, Cargill, Incorporated, Fujifilm Corporation, M&I Materials Ltd., Engineered Fluids, Lotte Fine Chemical Co., Ltd., Lubrizol Corporation, Inventec Performance Chemicals, 3M Company, Navin Fluorine International Limited, Submer, Green Revolution Cooling

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Immersion Cooling Fluids Market Segmentation

By Fluid Type

- Single-Phase Fluids

- Mineral Oils

- Synthetic Fluids

- Silicone-Based Fluids

- Ester-Based Fluids

- Two-Phase Fluids

- Hydrofluoroethers

- Perfluorocarbons

By Chemistry

- Hydrocarbon-Based

- Fluorocarbon-Based

- Synthetic Esters

- Bio-Based Fluids

By Cooling Technique

- Macro-Immersion

- Micro-Immersion

By Application

- High-Performance Computing

- Artificial Intelligence & Machine Learning

- Cryptocurrency Mining

- Data Centers

- Edge Computing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Immersion Cooling Fluids Industry

- Shell plc

- Exxon Mobil Corporation

- The Chemours Company

- Castrol

- Cargill, Incorporated

- Fujifilm Corporation

- M&I Materials Ltd.

- Engineered Fluids

- Lotte Fine Chemical Co., Ltd.

- Lubrizol Corporation

- Inventec Performance Chemicals

- 3M Company

- Navin Fluorine International Limited

- Submer

- Green Revolution Cooling

*- List not Exhaustive