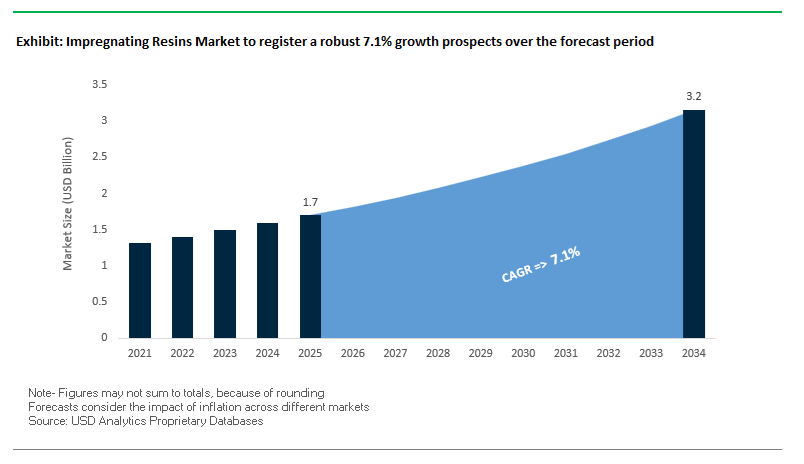

The Global Impregnating Resins Market is projected to expand from USD 1.7 billion in 2025 to USD 3.2 billion by 2034, advancing at a CAGR of 7.1%, as electrification fundamentally reshapes performance requirements for rotating electrical equipment. Growth is structurally anchored in EV traction motors, renewable energy generators, industrial drives, and power transformers, where higher voltages, higher switching frequencies, and compact winding architectures are increasing thermal and dielectric stress. Impregnating resins—often referred to as impregnating varnishes—are no longer passive insulation layers; they are system-defining materials that directly influence motor efficiency, lifetime, noise behavior, and resistance to partial discharge under high-load operation.

From an OEM and Tier-1 perspective, resin selection is increasingly governed by thermal class capability, penetration behavior, and regulatory compliance, rather than legacy cost or chemistry preferences. Leading suppliers such as Elantas (Altana), Von Roll, Axalta, Henkel, and Kyocera Chemical have reoriented portfolios toward Thermal Class 200–220°C polyesterimide and epoxy systems to support EV traction motors and high-duty industrial drives. The rapid adoption of 800V electric powertrains has intensified demand for low-viscosity impregnating resins—typically below 500 mPa·s—optimized for Vacuum Pressure Impregnation (VPI). These formulations enable deep penetration into densely packed stator windings, reducing voids, improving dielectric uniformity, and suppressing partial discharge in high-frequency operating environments.

Regulatory pressure and manufacturing realities are reinforcing this transition. OEMs across Europe and North America are accelerating the shift toward solvent-free and VOC-free impregnating resins to meet REACH, RoHS, and plant-level emission limits while improving operator safety and process stability. At the same time, resin formulators are integrating thermally conductive fillers and oxidation-resistant backbones to enhance heat dissipation from windings, directly enabling higher power density without sacrificing service life. In renewable energy systems—particularly wind turbine generators and large transformers—VPI epoxy and polyester resins remain essential for mechanical reinforcement, vibration damping, and corrosion protection under continuous load and harsh environmental exposure.

The global impregnating resins industry is undergoing significant structural shifts driven by strategic acquisitions, environmental legislation, and technical innovation. The competitive field in 2025 is increasingly defined by players consolidating specialty chemistry portfolios and advancing VOC-free, low-emission technologies aligned with the demands of EV, renewable, and industrial power sectors.

In April 2025, UBE Corporation finalized the acquisition of Lanxess’s Polyurethane Systems business, incorporating five production facilities and laboratories worldwide. This move enhances UBE’s specialty chemicals portfolio, positioning it as a key supplier of polyurethane-based impregnating resins and base feedstocks for electrical insulation coatings used in high-performance EV components. In March 2025, Axalta Coating Systems unveiled its new Voltatex ECO Line, a low-emission, renewable-content impregnating resin series achieving Thermal Class 220°C, specifically targeting e-mobility and energy OEMs. Similarly, ELANTAS Beck India (ALTANA Group) revealed in February 2025 that it is developing fire-retardant and pigmented polyester resins, addressing the growing flame-retardancy standards in power generation and mass transit applications.

Meanwhile, Von Roll, a global leader in electrical insulation systems, announced in January 2025 an upgrade to its high-voltage VPI insulation technology. Its Samicabond™ resin system and non-accelerated mica tapes enable faster curing cycles and higher mechanical endurance, optimizing productivity for turbo and hydro generators. Tightening EU environmental directives (December 2024) are further accelerating adoption of water-based impregnating resins, particularly for low-voltage motors and small transformers.

From a materials perspective, Momentive Performance Materials highlighted in November 2024 the role of silicone-based resins for high-temperature traction motors and aerospace-grade insulation, capable of withstanding temperatures exceeding 200°C. In October 2024, Kyocera Corporation expanded its electronic encapsulation material division, leveraging high-dielectric impregnating resins for miniaturized electronics. Axalta’s Voltatex 4224, recognized in September 2024, further underscored the industry’s focus on energy-efficient, low-viscosity formulations that facilitate superior winding impregnation and cooling efficiency in compact electric drives.

The accelerating electrification of the automotive industry is redefining motor insulation processes. Conventional dip-and-bake methods are being replaced by Vacuum Pressure Impregnation (VPI) and low-pressure impregnation (LPI) systems, which are essential for achieving the superior insulation class, dielectric performance, and thermal management required in high-voltage EV traction motors and e-axle assemblies. These systems employ 100% solids, solvent-free epoxy or polyester-imide impregnating resins to achieve a void-free insulation structure, dramatically improving dielectric performance and preventing Partial Discharge (PD) failures, a major reliability issue in high-speed, high-voltage EV components.

A technical case study highlights that VPI-treated electric motor windings demonstrate markedly enhanced heat transfer due to the complete filling of voids between conductors and insulation. The enables a measurable reduction in winding temperature rise, improving overall system efficiency and extending motor life by reducing thermal fatigue. In addition, as the U.S. Department of Energy (DOE) and global energy agencies push R&D for lightweight, high-efficiency EV motors, impregnation technologies that provide thermal stability, reduced dielectric loss, and superior moisture resistance are rapidly becoming a manufacturing standard.

These trends underline the strategic importance of VPI systems not only for OEM-level EV motor manufacturing but also for industrial high-speed drives, alternators, and aerospace rotors, where mechanical and electrical performance are equally critical. The widespread adoption of the advanced impregnation technology marks a turning point toward high-efficiency, thermally resilient electrical machines optimized for next-generation electric mobility and renewable power infrastructure.

The global drive toward miniaturized, high-density electronic components—spanning EV control systems, industrial automation electronics, and aerospace avionics—has intensified the need for impregnating resins that cure rapidly at low temperatures. The latest low-temperature and rapid-cure epoxy and polyester-imide resin systems are engineered to support fast-cycle manufacturing while safeguarding delicate electronic components from thermal stress during curing.

Recent corporate innovations have showcased carbon fiber epoxy systems capable of full cure within three hours at just 60°C, with extended options for curing as low as 45°C under post-cure protocols. The low-heat process represents a major breakthrough in enabling tooling and impregnation for heat-sensitive materials, including advanced composites and miniature circuit components.

Meanwhile, high-reactivity unsaturated polyester-imide resins with cure times as short as 15 minutes at 150°C are revolutionizing production throughput in automotive alternators, micro motors, and high-speed power tools. These systems enhance process efficiency while ensuring deep impregnation and superior mechanical bonding.

For printed circuit boards (PCBs) and power electronics, next-generation resins feature enhanced short-term thermal stability to endure reflow soldering peaks without degradation. The dual benefit—fast curing with thermal durability—is crucial in supporting high-volume production of compact, thermally demanding electronics.

The rapid global expansion of wind energy infrastructure presents one of the most significant growth opportunities for impregnating resin manufacturers. As offshore wind farms scale up, the reliability and longevity of generator insulation systems are paramount. Impregnating resins for wind turbine generators are critical to protecting against moisture ingress, thermal degradation, and salt-fog corrosion, particularly in challenging offshore environments where exposure to humidity and temperature fluctuations is severe.

Industry data indicates that electrical system and generator failures account for up to 4% of annual turbine downtime, with repair or replacement costs ranging from USD 100,000 to USD 225,000 per incident. The high cost of failure drives the vital role of durable, high-build impregnating varnishes and resins that maintain mechanical integrity and dielectric insulation over the turbine’s operational lifespan.

Government-backed renewable energy initiatives—such as Viability Gap Funding (VGF) programs for offshore wind—are further amplifying the demand for moisture- and chemical-resistant impregnating systems capable of withstanding harsh marine exposure. Manufacturers specializing in epoxy-imide and unsaturated polyester systems are seeing heightened demand from both OEM turbine builders and aftermarket service providers. The market’s direction is clear: high-durability impregnating resins are essential to achieving the reliability, energy efficiency, and sustainability objectives of the global wind power revolution.

The next wave of technological advancement in power electronics and high-voltage converters is being driven by Wide-Bandgap (WBG) semiconductors such as Silicon Carbide (SiC) and Gallium Nitride (GaN). These advanced materials enable operation at voltages above 600 V, temperatures exceeding 300°C, and switching frequencies up to 10 times higher than traditional silicon-based systems. To support the evolution, impregnating resins are being engineered with ultra-high dielectric strength, low thermal expansion coefficients (CTE), and crack-free curing performance, making them indispensable for SiC/GaN power module encapsulation and high-voltage insulation.

WBG-enabled devices drastically reduce heat sink requirements by up to 66%, enabling smaller, lighter, and more power-dense designs for EV inverters, industrial drives, and renewable energy converters. However, these benefits come with increased thermal and electrical stress. Specialized impregnating resins—particularly silicone-modified epoxy systems and ceramic-filled imide hybrids—provide both heat dissipation and dielectric isolation, ensuring operational safety and reliability under extreme electrical fields.

In addition, as power electronics miniaturization accelerates, resin suppliers are focusing on precision impregnation technologies that reduce void content and enhance mechanical stability in compact module architectures. The trend is reinforced by the rise of EV fast-charging networks and smart grid applications, both of which depend on high-durability dielectric resin systems to sustain performance under continuous load and variable frequencies.

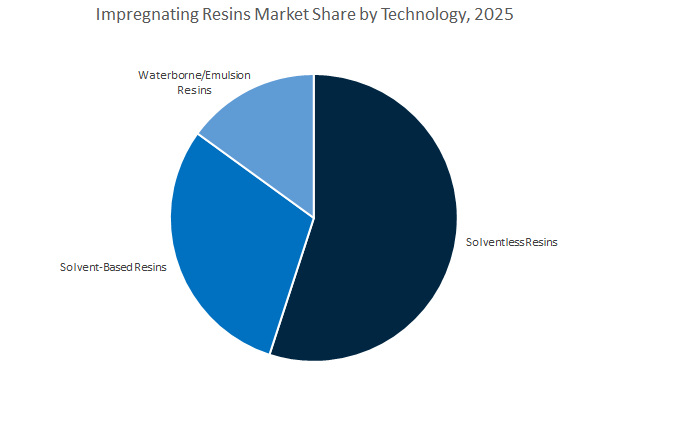

Impregnating Resins Market Share Insights, 2025-2034

Solventless impregnating resins dominate the global impregnating resins market, projected to hold a 53.1% share in 2025, reflecting their superior environmental profile, low VOC emissions, and outstanding dielectric performance in high-reliability electrical systems. These resins are widely preferred for electric motor windings, generator coils, and electronic component encapsulation, where deep impregnation, mechanical reinforcement, and thermal endurance are crucial. Their formulation flexibility—ranging from epoxy and polyester imide systems to unsaturated polyesters—enables tailored performance for diverse electrical insulation requirements. The trend toward solventless and energy-efficient curing systems has intensified due to global sustainability mandates and the electrification of industrial and mobility sectors.

Solvent-based impregnating resins maintain a strong but declining presence, primarily in applications requiring deep penetration into dense windings or complex geometries where capillary action is critical. Despite their reliable performance, this segment faces pressure from environmental and occupational safety regulations targeting VOC content and handling hazards. Waterborne and emulsion-based impregnating resins are emerging as the sustainable alternative, offering low odor, reduced environmental footprint, and easier clean-up, particularly for medium-voltage and industrial equipment applications where extreme dielectric performance is less demanding.

The electrical and electronics (E&E) sector dominates the global impregnating resins market with a projected 42.6% share in 2025, driven by its extensive use in motor insulation, transformer manufacturing, and electronic component protection. Impregnating resins are critical for moisture resistance, dielectric strength, and mechanical reinforcement of electrical assemblies, ensuring operational reliability and heat dissipation in demanding conditions. The growth of electrification, renewable energy, and e-mobility continues to boost resin demand across motors, alternators, and sensors.

The automotive and transportation industry follows closely, fueled by the rise of electric vehicles (EVs) and the integration of high-performance resins in battery modules, motor stators, and electronic sensors. These resins enhance thermal stability, insulation, and vibration damping, directly contributing to vehicle safety and efficiency. The industrial sector sustains consistent demand through machinery, tools, and power equipment manufacturing, where impregnating resins protect components from corrosion, thermal degradation, and mechanical stress. Meanwhile, the energy and power segment represents a strategic growth frontier, with applications in wind turbine generators, high-voltage transformers, and grid infrastructure demanding exceptional heat resistance and electrical insulation.

The global impregnating resins industry is dominated by ELANTAS (ALTANA Group), Axalta Coating Systems, Von Roll, Huntsman Corporation, Momentive Performance Materials, and Wacker Chemie AG—all focusing on high-temperature insulation, sustainability, and advanced resin chemistry for e-mobility and energy systems.

ELANTAS remains the market leader with its Dobeckan, Epoxylite, and Elmotherm resin brands. It offers comprehensive insulation solutions up to Thermal Class 200°C, covering wire enamels, impregnating, and casting resins. The company’s R&D emphasizes monomer-free, low-drainage-loss resins optimized for trickle and dip-roll processes in compact electric motors. Its global application engineering network supports OEMs in achieving reliable, defect-free impregnation for EV traction drives and industrial generators.

Axalta’s Voltatex and Voltabas lines are synonymous with sustainable and high-performance impregnating resins. Its new Voltatex ECO Line, launched in March 2025, integrates renewable feedstocks and epoxy-modified polymers free of SVHC or CMR compounds. With thermal conductivity optimization and styrene-free chemistry, Axalta supports OEMs achieving IE4/IE5 efficiency classes in motors. It also stands out as one of the few companies offering the complete “electrical insulation trio” — enamels, impregnating resins, and electrical steel coatings — ensuring total system compatibility.

Von Roll specializes in high-voltage (HV) insulation solutions for power generation and transmission. Its Micalastic and Dolph’s™ resins serve VPI and resin-rich processes, ensuring outstanding thermal endurance and electrical integrity. Recent investments in Samicabond™ VPI resins (January 2025) focus on faster curing cycles and compatibility with non-accelerated mica tapes, enabling Class H insulation for turbo and hydro generators. Von Roll’s integrated offering combines mica tapes, resins, and flexible materials, positioning it as the industry’s most complete supplier for HV systems.

Huntsman Corporation provides ARALDITE™ epoxy and polyurethane systems as critical building blocks for high-performance impregnating and casting formulations. Its focus on low-viscosity and high-toughness base resins enables excellent shock and vibration resistance—vital for automotive electronics and aerospace motors. The company’s integration capability allows custom formulation of epoxy-polyurethane hybrids for VPI processes, offering both dielectric stability and mechanical strength.

Momentive leads the silicone resin segment with formulations capable of maintaining thermal stability beyond 250°C. Its silicone resins and coatings offer excellent resistance to moisture, corona discharge, and chemical degradation, making them indispensable in traction motors, wind turbines, and oilfield electronics. Focused R&D ensures superior partial discharge endurance for high-frequency applications, securing Momentive’s leadership in extreme-condition insulation materials.

Wacker Chemie AG delivers silicone resins, gels, and elastomers engineered for electronic encapsulation and impregnation. Its materials are optimized for electrical insulation, vibration damping, and thermal cycling stability. With a strong footprint across Asia and Europe, Wacker’s R&D focuses on next-generation electrically insulating silicones with enhanced thermal conductivity, crucial for EV batteries and power electronics. The company’s complementary silicone gels offer thermal and mechanical stress relief, ensuring component longevity in e-mobility platforms.

China continues to dominate the global Impregnating Resins and Wire Enamels market, driven by massive investments in New Energy Vehicles (NEVs), ultra-high-voltage (UHV) grid infrastructure, and industrial electrification. The Chinese government’s vehicle trade-in subsidy program, with a budget allocation of RMB 81 billion for 2025, is accelerating the adoption of NEVs by incentivizing consumers to replace older vehicles with newer electric models. The policy directly stimulates demand for high-dielectric, thermal-resistant motor insulation materials, including epoxy and polyester impregnating resins.

Further boosting The demand, draft legislation from the Ministry of Industry and Information Technology (MIIT) sets ambitious sales mandates — 48% of new vehicle sales to be NEVs by 2026, increasing to 58% by 2027. The policy secures sustained, long-term growth for traction motor impregnating resin systems, particularly those based on solventless polyurethane and epoxy chemistries designed for high-speed, high-voltage e-motors.

In parallel, China’s UHV power transmission projects are generating substantial demand for transformer-grade impregnating varnishes with enhanced dielectric strength, moisture resistance, and superior thermal endurance. Domestic players, including Hubei Huitian Glue Co., Ltd., and multinational corporations like Henkel and Elantas, are expanding local production capabilities to meet the needs of the rapidly evolving electrical and automotive supply chain. As China pushes for energy efficiency and thermal reliability, it cements its status as the global epicenter of high-performance impregnating resin manufacturing and innovation.

The United States Impregnating Resins Market is witnessing accelerated growth, fueled by federal initiatives supporting electric mobility, energy storage, and advanced power infrastructure. The Bipartisan Infrastructure Law (BIL) allocates $7.5 billion to expand the national EV charging network, creating large-scale demand for transformer insulating varnishes and grid-grade electrical resins that ensure long-term reliability in high-voltage applications.

The U.S. Department of Energy’s Vehicle Technologies Office (VTO) is channeling R&D funding into next-generation electric drive systems, focusing on thermal management, magnetic material substitution, and advanced impregnating resin formulations that improve motor efficiency. Furthermore, the Inflation Reduction Act (IRA) incentivizes domestic manufacturing of electrical and insulation materials, reinforcing supply chain resilience and promoting onshoring of polyester and epoxy resin production.

Private sector innovation complements The efforts. Companies like 3M, Dow, and H.B. Fuller are investing in thermally conductive resin systems for EV batteries, industrial generators, and electronic encapsulation. Similarly, Ashland and Elantas PDG continue developing solventless impregnating varnishes that meet low-VOC and REACH compliance standards for the automotive, aerospace, and renewable energy sectors. The combination of federal incentives, industrial R&D, and sustainable materials development positions the U.S. as a key growth engine for high-performance impregnating resins in the global market.

Germany’s leadership in automotive electrification and industrial engineering underpins its pivotal role in the European Impregnating Resins industry. The country’s robust E-Mobility ecosystem, supported by major OEMs and Tier 1 suppliers, has created a strong domestic market for thermal class H and C impregnating resins designed for next-generation electric motors and power electronics. The materials deliver enhanced thermal endurance, mechanical strength, and environmental resistance, critical for high-performance EV applications.

German chemical giants such as Henkel AG & Co. KGaA, ALTANA (through ELANTAS), and Axalta Coating Systems continue to pioneer innovations in low-VOC and water-based varnish technologies, aligning with stringent EU environmental and occupational safety standards. Their R&D efforts are concentrated on solvent-free resin systems that meet the dual goals of sustainability and performance, particularly in industrial automation, robotics, and renewable energy equipment.

Moreover, Germany’s advanced manufacturing ecosystem emphasizes digital material validation and simulation-driven development of resin chemistries for automotive, transformer, and generator applications. As the European Union tightens environmental regulations under the European Green Deal, Germany remains the center of excellence for sustainable impregnating resin formulation and production across high-value industrial sectors.

Japan remains a global leader in high-reliability impregnating resin systems, focusing on advanced electronics, semiconductor packaging, and miniaturized automotive components. Japanese chemical producers are developing cutting-edge formulations such as Bismaleimide Triazine (BT) resins and advanced epoxy systems tailored for high-frequency, high-heat electronic environments — including automotive sensors, microcontrollers, and power modules.

In line with Japan’s environmental sustainability targets, companies such as Mitsubishi Chemical are innovating plant-derived, bio-based impregnating resins under ISCC PLUS certification. The sustainable materials are being tested for use in laminate substrates, composite prepregs, and insulation coatings, reflecting Japan’s strategic move toward renewable feedstocks and circular material systems.

Capacity expansions are also accelerating in the semiconductor and electronics materials sector, where major players like Hitachi Chemical and Sumitomo Bakelite are scaling up production of conductive pastes, insulating varnishes, and impregnation resins to meet global demand. Japan’s combination of precision engineering, environmental responsibility, and material science expertise secures its position as a leading hub for high-performance impregnating resin innovation.

South Korea’s technological strength in consumer electronics, displays, and energy storage has created strong downstream demand for high-purity, high-durability impregnating resins. The country’s dominance in semiconductor and OLED display manufacturing necessitates ultra-reliable impregnation materials that offer thermal endurance, dielectric integrity, and chemical stability for microelectronic components.

Simultaneously, the rapid expansion of EV battery production and energy storage systems (ESS) is driving innovation in resin systems for cell insulation, module encapsulation, and pack-level thermal management. Conglomerates like LG Energy Solution and Samsung SDI are investing in epoxy and polyurethane-based impregnating resins that can withstand extreme temperature cycles and prevent thermal runaway events in advanced lithium-ion systems.

Moreover, South Korea’s growing emphasis on green materials and eco-efficient production aligns with global shifts toward sustainable resin chemistry. The convergence of electronics miniaturization and EV electrification establishes South Korea as a critical node in the global supply chain for high-temperature, high-performance impregnating resins.

France plays a strategic role in Europe’s high-performance impregnating resin market, particularly through its strong aerospace, defense, and transportation sectors. The country’s focus on structural and electrical insulation materials for aircraft, rail, and automotive applications is driving innovation in solvent-free, high-temperature impregnating technologies.

French chemical and composite material companies are investing in Dry Powder Impregnation (DPI) techniques that reduce solvent use, lower energy consumption, and align with the European Green Deal’s decarbonization goals. The dry-process technologies also improve worker safety and process efficiency, enabling France to pioneer eco-efficient impregnating methods for both composites and electrical components.

Moreover, the EU’s Ecodesign and Circular Economy regulations are influencing the selection of durable, recyclable impregnating resins that enhance product repairability and end-of-life disassembly — critical for electronic devices, transformers, and electric motors. As sustainability and safety converge as key priorities, France is becoming a key innovation center for green impregnation solutions and advanced resin chemistries tailored to aerospace and industrial markets.

Impregnating Resins Market Report Scope

Impregnating Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.7 Billion

|

|

Market Size (2034)

|

$3.2 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Resin Type (Epoxy Resins, Polyester Resins, Polyester-Imide Resins, Polyurethane Resins, Silicone Resins, Other Specialty Resins), By Technology (Solventless Resins, Solvent-Based Resins, Waterborne/Emulsion Resins), By Application (Motors and Generators, Transformers, Electrical & Electronic Components, Automotive Components, Home Appliances, Other Industrial Applications), By End-Use Industry (Electrical & Electronics, Automotive & Transportation, Industrial, Energy & Power

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

ALTANA AG, Axalta Coating Systems, LLC, Von Roll Holding AG, Henkel AG & Co. KGaA, Huntsman International LLC, 3M Company, BASF SE, Mitsubishi Chemical Group Corporation, Aditya Birla Group, Wacker Chemie AG, Kyocera Corporation, Bodo Möller Chemie GmbH, Hitachi Chemical Co., Ltd., ADVANCED ELECTRICAL VARNISHES, S.L., Robnor ResinLab Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Epoxy Resins

- Polyester Resins

- Polyester-Imide Resins

- Polyurethane Resins

- Silicone Resins

- Other Specialty Resins

By Technology/Form

- Solventless Resins

- Solvent-Based Resins

- Waterborne/Emulsion Resins

By Application

- Motors and Generators

- Transformers

- Electrical & Electronic Components

- Automotive Components

- Home Appliances

- Other Industrial Applications

By End-Use Industry

- Electrical & Electronics

- Automotive & Transportation

- Industrial

- Energy & Power

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- ALTANA AG

- Axalta Coating Systems, LLC

- Von Roll Holding AG

- Henkel AG & Co. KGaA

- Huntsman International LLC

- 3M Company

- BASF SE

- Mitsubishi Chemical Group Corporation

- Aditya Birla Group

- Wacker Chemie AG

- Kyocera Corporation

- Bodo Möller Chemie GmbH

- Hitachi Chemical Co., Ltd.

- ADVANCED ELECTRICAL VARNISHES, S.L.

- Robnor ResinLab Ltd.

*- List not Exhaustive

Research Coverage

Built for e-mobility, power equipment, and industrial automation decision-makers, the USDAnalytics study on the Impregnating Resins Market aligns materials science with real-world reliability at elevated thermal classes: this report investigates how next-generation epoxy, polyester, polyester-imide, polyurethane, silicone, and specialty systems translate into void-free impregnation, partial-discharge mitigation, and cooling efficiency across motors, generators, transformers, and compact electronics; traces breakthroughs in solventless/VOC-free chemistries, rapid/low-temperature cures, high-TC filler packages, and digital VPI/LPI process control; analysis reviews the impact of electrification, renewable grid build-out, and tightening REACH/RoHS/VOC frameworks on specification and cost-in-use; and highlights the procurement and design levers—viscosity windows, dielectric strength, thermal class up to 220 °C, and cycle-time reduction—that raise uptime and extend asset life. Calibrated for strategy, sourcing, QA, and R&D roadmaps, this report is an essential resource for OEMs, tier suppliers, resin formulators, and investors seeking defensible decisions on insulation performance, compliance, and lifecycle economics, etc……

Scope Highlights

Segmentation

- By Resin Type: Epoxy Resins; Polyester Resins; Polyester-Imide Resins; Polyurethane Resins; Silicone Resins; Other Specialty Resins

- By Technology/Form: Solventless Resins; Solvent-Based Resins; Waterborne/Emulsion Resins

- By Application: Motors & Generators; Transformers; Electrical & Electronic Components; Automotive Components; Home Appliances; Other Industrial Applications

- By End-Use Industry: Electrical & Electronics; Automotive & Transportation; Industrial; Energy & Power

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analytical coverage and profiles of 15+ companies (list not exhaustive).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.