Industrial Cleaning Solvents Market Forecast to Reach $115.1 Billion by 2034 Amid Rising Demand for Green and Low-VOC Cleaning Solutions

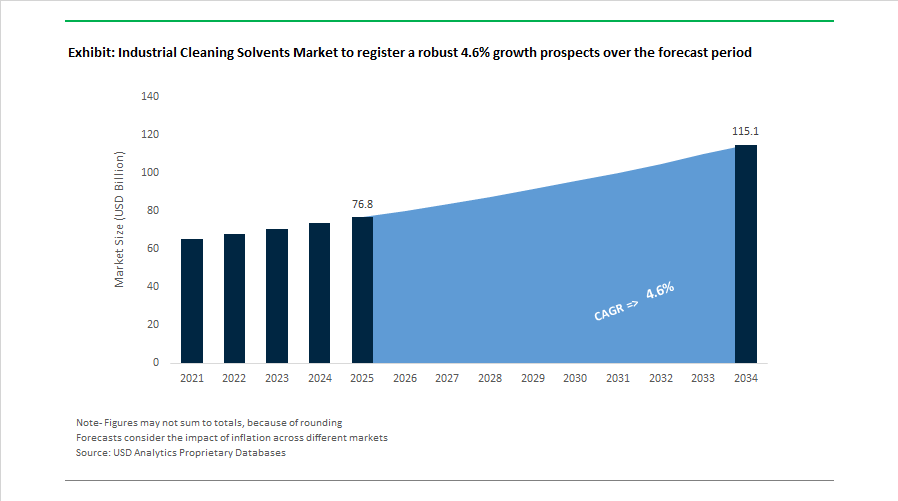

The Global Industrial Cleaning Solvents Market is witnessing steady expansion driven by growing demand across manufacturing, food processing, healthcare, aerospace, and institutional cleaning applications. The market is projected to grow from $76.8 billion in 2025 to $115.1 billion by 2034, registering a CAGR of 4.6% during the forecast period. This growth is largely fueled by increasing regulatory pressure to reduce volatile organic compound (VOC) emissions, the transition toward bio-based and environmentally sustainable solvents, and the rising adoption of advanced cleaning technologies in industrial facilities. Industries are increasingly prioritizing high-performance industrial degreasers, precision cleaning solvents, and eco-friendly industrial cleaning chemicals to maintain equipment efficiency while complying with tightening environmental standards.

The industrial cleaning solvents market is increasingly shaped by sustainability-driven innovation and regulatory pressure, particularly through the adoption of renewable feedstocks and low-emission solvent chemistries. Leading manufacturers such as BASF and Syensqo are introducing bio-based solvent technologies that can reduce net carbon dioxide emissions by over 90% compared to conventional petrochemical solvents, aligning with corporate Scope 3 emissions reduction strategies. Simultaneously, regulatory frameworks including U.S. EPA and EU REACH standards are accelerating the transition toward low-VOC formulations, with some jurisdictions limiting VOC content in multi-purpose industrial degreasers to below 10% by weight for indoor use.

Technological advancements are also improving operational efficiency, as AI-enabled Clean-in-Place systems used in industries such as food and beverage processing can reduce water consumption by 15% to 20% while enhancing uptime through real-time cleaning analytics. In parallel, solvent substitution initiatives led by companies such as Henkel and Diversey have resulted in nearly 80% of global formulators moving away from halogenated solvents toward aqueous and bio-based alternatives including ethyl lactate and D-limonene. Strong demand from healthcare and hospitality sectors is further supporting market expansion, with usage of industrial-grade disinfectants and EPA List N compatible cleaning solvents remaining 60% to 80% above pre-2020 levels due to sustained hygiene and infection-control requirements.

Market Analysis: Industry Developments Accelerating the Transition Toward Green Industrial Cleaning Solutions (2024–2026)

The Industrial Cleaning Solvents industry is currently undergoing a transformation driven by green chemistry innovation, regulatory reforms, and strategic consolidation within the industrial and institutional (I&I) cleaning sector. In March 2026, BASF announced price adjustments for its acrylate-based solvent precursors including butyl acrylate and 2-ethylhexyl acrylate in the Asia-Pacific region, reflecting shifting raw material costs and strong demand from the industrial coatings and cleaning solvent markets. Shortly afterward in February 2026, Syensqo introduced Rhodasurf® B7 UP, a bio-based low-carbon surfactant designed as a drop-in replacement for petrochemical surfactants in industrial laundry and hard-surface cleaning formulations, highlighting the increasing commercialization of bio-based industrial cleaning ingredients.

Corporate sustainability initiatives and partnerships are further strengthening the adoption of environmentally friendly cleaning solutions. In February 2026, BuzzWorks partnered with Born Good to deploy plant-based, toxin-free industrial cleaning solutions across commercial workspace portfolios to support corporate ESG mandates and green facility management strategies. Regulatory changes are also influencing market dynamics. In January 2026, India’s Ministry of Chemicals and Fertilizers revoked six Quality Control Orders (QCOs) for chemicals including toluene and p-xylene, which are widely used as industrial solvent components, in order to reduce regulatory barriers and improve chemical trade flexibility for manufacturers.

Significant developments throughout 2025 also strengthened innovation and consolidation within the sector. In December 2025, Solenis completed the acquisition of Diversey Holdings, a major move that reshaped the industrial cleaning chemicals market by combining advanced sanitation technologies and chemical cleaning solutions under a single platform. In October 2025, Henkel launched Bonderite C-AK DW 805 Aero, a specialized dry wash solvent for aircraft cleaning applications, designed to eliminate water rinsing and significantly reduce aircraft maintenance downtime. Meanwhile, in September 2025, Ecolab introduced CIP IQ™, an AI-powered clean-in-place system for dairy and beverage processing, enabling precise chemical dosing and minimizing chemical waste during industrial cleaning cycles.

Government policy initiatives are also accelerating the shift toward low-VOC and environmentally compliant cleaning solvents. In July 2025, the Government of India proposed draft regulations mandating low-VOC certified materials for new residential and commercial building projects, a move expected to stimulate demand for green industrial solvents and sustainable cleaning formulations across construction and facility management sectors. Earlier, in May 2024, Vantage Specialty Chemicals expanded its production capacity in Leuna, Germany, focusing on bio-based surfactants and high-purity esters to meet increasing demand across the European industrial cleaning and specialty chemical markets. These developments collectively highlight the rapid transformation of the industrial cleaning solvents sector toward low-carbon chemistry, digital cleaning technologies, and environmentally compliant solvent systems.

Industrial Cleaning Solvents Market Trends and Opportunities

Compliance-Driven Substitution Following the Trichloroethylene (TCE) Phase-Out

The industrial cleaning solvents market is undergoing one of its most disruptive regulatory resets in decades, triggered by the U.S. EPA’s 2024 Final Risk Management Rule under the Toxic Substances Control Act. The mandated sunset of trichloroethylene is forcing more than 140,000 industrial and commercial facilities to redesign degreasing operations by September 15, 2025. For most manufacturers, this deadline has accelerated solvent substitution from a long-term ESG aspiration into an immediate operational necessity.

Although limited extensions have been granted for critical infrastructure through 2028, the economics strongly favor full replacement. Facilities retaining TCE under “essential use” exemptions must implement Workplace Chemical Protection Programs that include continuous air monitoring, medical surveillance, and advanced personal protective equipment. Industry cost modeling indicates that these compliance measures can add USD 150,000 to USD 300,000 annually per site, often exceeding the capital cost of converting to alternative cleaning technologies within two to three years. As a result, demand has surged for trans-1,2-dichloroethylene blends, modified alcohol systems, and high-efficiency aqueous cleaning platforms.

Capital expenditure patterns confirm this shift. Equipment suppliers report a sharp increase in orders for multi-stage aqueous ultrasonic cleaners and vacuum degreasers, as manufacturers decommission legacy vapor degreasing units to eliminate long-term regulatory liability. This transition is not only reshaping solvent demand but also redistributing value toward integrated chemical and equipment solutions that deliver compliance assurance alongside cleaning performance.

ESG-Led Strategic Sourcing and the Rise of Bio-Based Industrial Solvents

Beyond regulation, corporate ESG mandates are now exerting structural influence on solvent procurement. Aerospace, automotive, and electronics OEMs are embedding sustainability criteria directly into supplier contracts, prioritizing solvents with high bio-renewable carbon content to meet Scope 3 emissions disclosure requirements. Leading OEMs such as Airbus and Boeing have released updated sustainability standards for 2025 that explicitly favor bio-based glycol ethers, esters, and terpene-derived solvents in maintenance and manufacturing operations.

This shift is being reinforced by upstream investment. Government-backed initiatives, including India’s National Bio-Energy Mission 2025, are accelerating biomass-to-chemicals infrastructure, enabling second-generation bio-solvents derived from agricultural residues. These supply chains are reducing feedstock volatility and supporting regional manufacturing hubs with lower lifecycle emissions profiles. Despite commanding a 15 to 20% price premium over fossil-based alternatives, bio-based solvents are gaining share in high-value applications as procurement teams increasingly rely on Ecovadis and SASB benchmarks to evaluate supplier sustainability performance. In this context, the “green premium” is being reframed as a risk mitigation and brand value investment rather than a discretionary cost.

Ultra-High Purity Solvents for Advanced Semiconductor Manufacturing

One of the most attractive growth avenues in the industrial cleaning solvents market lies in electronic-grade formulations for advanced semiconductor fabrication. The transition toward chiplet architectures and EUV lithography has intensified sensitivity to ionic and organic contamination, driving demand for solvents with sub-parts-per-billion impurity thresholds. In 2025, the global market for semiconductor-grade high-purity solvents is estimated at USD 2.9 billion, supported by accelerating investment in AI, data centers, and 5G infrastructure.

Strategic realignment among suppliers underscores the value at stake. Entegris consolidated its materials purity and materials science operations to streamline yield-critical chemical offerings, while Fujifilm completed a USD 675 million acquisition to strengthen its position in advanced process chemicals. As node sizes approach 2 nanometers, traditional cleaning chemistries struggle to penetrate high-aspect-ratio features without inducing pattern collapse. This is creating sustained demand for specialized hydrofluoroether and ultra-dry isopropanol blends with low surface tension and rapid evaporation profiles, positioning purity and formulation expertise as decisive competitive differentiators.

Hybrid Solvent-Emulsion Systems for Complex Industrial Deposits

A second high-margin opportunity is emerging in hybrid solvent-emulsion technologies designed to address deposits that exceed the capabilities of conventional single-component solvents. Oil and gas pigging residues, turbine varnish in power generation, and polymerized hydrocarbon films increasingly require multifunctional cleaning systems that combine chemical solvency with mechanical emulsification.

Recent industrial studies show that liquid nano-emulsions with optimized oil-to-surfactant ratios remain stable at operating temperatures up to 90°C, enabling the removal of carbonized oils and polymer layers that resist traditional solvents. In upstream energy applications, hybrid systems enhanced with advanced demulsification technologies are reducing hazardous waste volumes by approximately 25% by separating recoverable hydrocarbons from spent cleaning fluids. This performance advantage is reinforcing adoption of “zero-waste” solvent models, where suppliers provide on-site recovery and recycling hardware as part of a service contract. Such programs can recover up to 90% of active solvent content, materially lowering the cost per cleaning cycle while supporting corporate waste minimization targets.

Industrial Cleaning Solvent Market Share and Segmentation Insights

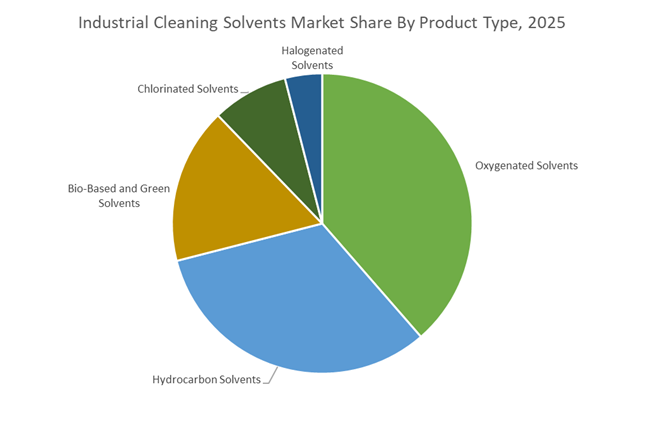

Oxygenated Solvents Lead Industrial Cleaning Solvent Demand Through Regulatory-Compliant Degreasing Performance

Oxygenated solvents accounted for 38.6% of the Industrial Cleaning Solvents Market share in 2025, establishing them as the leading product category in modern industrial degreasing and surface preparation applications. Oxygenated solvents such as alcohols, ketones, esters, and glycol ethers deliver strong solvency for oils, greases, resins, and particulate contaminants while offering improved environmental and occupational safety profiles compared with traditional chlorinated solvents. Their ability to dissolve a wide range of industrial soils has made them widely used in metal parts cleaning, paint stripping, precision component degreasing, and surface preparation prior to coating or bonding processes. In 2025, regulatory pressure has accelerated the substitution of chlorinated solvents such as trichloroethylene (TCE) and perchloroethylene (PERC) as well as high-VOC hydrocarbon solvents. Industrial cleaning product manufacturers increasingly formulate oxygenated solvent blends that replicate the cleaning performance of restricted chemicals while meeting stricter VOC and hazardous air pollutant regulations, enabling compliance with evolving environmental standards in industrial maintenance and manufacturing cleaning operations.

Manufacturing and Industrial Operations Drive the Largest Consumption of Cleaning Solvents

Manufacturing and Industrial applications represented 48.60% of the Industrial Cleaning Solvents Market share in 2025, making this sector the dominant consumer of industrial degreasing and maintenance cleaning chemicals. Manufacturing facilities require large volumes of cleaning solvents to maintain production equipment, metal components, machining tools, conveyor systems, and assembly line machinery, ensuring consistent product quality and preventing contamination during manufacturing processes. Industrial cleaning solvents are widely used in metalworking operations, component preparation before coating or plating, equipment maintenance, and removal of machining oils and cutting fluids. Because manufacturing spans numerous sectors including machinery production, heavy equipment fabrication, electronics assembly, and consumer goods manufacturing, it represents the broadest and most diverse demand base for industrial cleaning chemicals. In 2025, the ongoing shift toward near-shoring and regional manufacturing expansion in North America and Europe has further increased demand for industrial cleaning solvents as production capacity grows closer to end markets. This manufacturing resurgence is accompanied by stricter environmental regulations, prompting solvent manufacturers to develop low-VOC and environmentally compliant cleaning formulations suitable for modern industrial production environments.

Competitive Landscape in Industrial Cleaning Solvents Market

Dow Accelerates Specialty and Silicone-Based Solvent Innovation

Dow Inc. is executing its “Transform to Outperform” initiative, targeting $2 billion in operating EBITDA improvement by 2028, with $500 million in 2026 from AI-driven productivity gains and structural cost resets. Operating in 29 countries with approximately 34,600 employees, Dow generated around $40 billion in 2025 sales. In industrial cleaning, it remains a leader in silicone and oxygenated solvents. DOWSIL™ DS-2025 is specifically engineered for depolymerizing cured silicone residues in manufacturing systems, reducing equipment downtime in electronics and sealant production lines. Dow’s sustainability strategy emphasizes high-flash-point, non-halogenated alternatives aligned with “Safe Materials for a Sustainable Planet,” targeting $1 billion in NPV from nature-positive projects by early 2026.

BASF Shifts Toward Aqueous and Low-VOC Systems

BASF SE is repositioning its solvent portfolio under its “Winning Ways” efficiency strategy, targeting €6.2–€7.0 billion in EBITDA before special items in 2026 and €2.3 billion in annual cost savings by year-end. The Zhanjiang Verbund site, operational since late 2025, enhances supply capacity for Asian industrial markets but slightly increases projected 2026 CO2 emissions to 17.2–18.2 million metric tons. BASF is actively transitioning toward aqueous and low-VOC industrial cleaning systems to comply with EU REACH revisions and European Green Deal directives. Integration advantages from its Verbund model allow backward feedstock optimization for glycol ethers, alcohols, and specialty blends used in heavy-duty degreasing and precision cleaning.

ExxonMobil Maintains Hydrocarbon Solvent Leadership

ExxonMobil Product Solutions remains the dominant force in hydrocarbon-based industrial solvents, a segment estimated to represent roughly 35.5% of global market demand in 2026. Its Actrel™, Exxsol™ D, and Isopar™ brands provide dearomatized, low-odor alternatives engineered for controlled evaporation and high purity. The company’s refining network—larger than other major international oil companies—ensures unmatched consistency and supply reliability. Sustainability efforts include carbon capture and hydrogen fuel-switching at major refining hubs in Texas and the Netherlands to reduce solvent carbon intensity. Hydrocarbon solvents continue to dominate heavy-duty degreasing and metal-cleaning applications due to solvency strength and drying efficiency.

Shell Expands Oxygenated and GMP-Grade Solvent Portfolio

Shell Chemicals is strengthening its position in high-purity oxygenated solvents and Special Boiling Point (SBP) fluids. The PROXITOL brand includes propylene glycol ethers and acetates tailored for waterborne and low-aromatic cleaning systems. Shell remains a key supplier of GMP-grade isopropyl alcohol and ketones for pharmaceutical and electronics cleaning environments. Strategic emphasis is placed on supply security through geographically diversified production assets. In 2026, Shell is integrating bio-based feedstocks into select solvent lines to align with green procurement requirements from multinational manufacturers.

Arkema Prioritizes Specialty Material Margins

Arkema S.A. reported €1.25 billion EBITDA in 2025 with a 13.8% margin and targets modest growth in 2026 despite macro softness in Europe and the U.S. Through portfolio segmentation enhancements, its Specialty Materials division maintained a 15.7% margin. Capacity expansions, including Rilsan® Clear in Asia, are projected to add €50 million in incremental EBITDA in 2026. In industrial solvents, Arkema emphasizes high-performance specialty formulations designed for demanding polymer and coating applications. Organizational streamlining from 2026–2028 anticipates a 3% annual headcount reduction, reflecting its focus on high-value, innovation-driven segments.

Clariant Advances Bio-Based and Localized Production Strategy

Clariant continues strengthening margins, achieving 42% free cash flow conversion in 2025 and targeting approximately 18% EBITDA margin in 2026. A CHF 50 million savings program delivered in 2025 will be supplemented by CHF 30 million in 2026. In March 2026, Clariant partnered with Vertimass to advance bio-based alcohol-to-liquid technologies, supporting sustainable processing pathways. Operating 68 production sites globally, Clariant’s “Local-for-Local” strategy mitigates shipping volatility and tariff exposure. Its solvent portfolio increasingly emphasizes renewable feedstocks and specialty blends designed for compliance-driven industrial cleaning applications.

United States Industrial Cleaning Solvents Market: Semiconductor Security, PFAS Exit, and Aerospace Compliance

The United States industrial cleaning solvents industry is being reshaped by semiconductor supply chain localization, regulatory-driven solvent substitution, and aerospace compliance requirements. In 2025, Eastman Chemical Company finalized the domestic expansion of its electronic-grade solvent production, securing localized access to ultra-high-purity solvents for wafer cleaning and photolithography. This move directly mitigates trans-Pacific logistics risk for U.S. semiconductor foundries and aligns with broader federal objectives to onshore critical chemical inputs for advanced manufacturing. Parallel to this, the Federal Supply Chain Task Force has extended Facility Readiness incentives to chemical producers synthesizing oxygenated solvents such as isopropyl alcohol and ketones, strengthening domestic resilience for essential industrial cleaning solvents.

Regulatory pressure is accelerating formulation change across the solvent value chain. From January 2026, the EPA requires comprehensive PFAS usage reporting for all industrial cleaning formulations, driving rapid adoption of siloxane-based and hydrocarbon-based alternatives. Aerospace maintenance is a key downstream beneficiary. In October 2025, Henkel introduced Bonderite C-AK DW 805 AERO, a dry-wash solvent cleaner that eliminates water rinsing, reduces downtime, and supports airline compliance with stricter 2026 VOC limits for heavy maintenance hangars. These developments are reinforced by a broader bio-based solvent influx, with North America accounting for roughly 40% of global bio-solvent demand by late 2025, driven by corn- and soy-derived cleaning agents adopted across manufacturing and maintenance operations.

China Industrial Cleaning Solvents Market: Mandatory Standards, Tax Enforcement, and Electronics-Led Reformulation

China’s industrial cleaning solvents landscape is dominated by regulatory mandates and policy-led upgrading of traditional solvent chemistries. In May 2025, the Ministry of Industry and Information Technology released the revised mandatory national standard GB 30981.1-2025, which comes into force in June 2026. The regulation sharply restricts solvent content in architectural and industrial accessory materials, forcing a shift toward high-solid and water-based cleaning auxiliaries. Complementing this, the Ministry of Finance intensified enforcement of a 4% consumption tax on cleaning agents exceeding 420 g/l VOCs, incentivizing large producers to reformulate degreasing solvents toward lower-emission profiles.

Industrial policy continues to support solvent upgrading. Under the 2025–2026 MIIT petrochemical growth plan, seven ministries jointly targeted modernization of hydrocarbon and chlorinated solvents toward electronic-grade purity, supporting electronics manufacturing and precision cleaning. In November 2025, BASF commissioned a high-performance dispersant line in Nanjing using Controlled Free Radical Polymerization, enhancing the effectiveness and stability of industrial cleaning solvent systems. At the same time, China is accelerating its HCFC phase-out to meet Montreal Protocol targets for 2026, pushing electronics manufacturing hubs toward hydrofluoroether-based cleaning agents with improved environmental stability.

Germany Industrial Cleaning Solvents Market: Circularity, REACH Substitution, and Energy-Efficient Synthesis

Germany’s industrial cleaning solvents industry is advancing through circular economy initiatives, regulatory substitution, and low-energy production pathways. In December 2025, BASF and industry partners signed a memorandum to advance solvent recovery and high-purity regeneration, positioning circular solvent systems as a core lever for achieving net-zero carbon objectives by 2050. This initiative elevates solvent recycling from waste management to strategic feedstock recovery for industrial cleaning applications.

Regulatory scrutiny is intensifying. In November 2025, the European Chemicals Agency recommended adding new substances, including melamine, to the REACH Authorisation List, prompting German formulators to accelerate substitution programs ahead of potential 2027 restrictions. Supply-side innovation is responding accordingly. European producers, including BioAmber, have expanded bio-based succinic acid capacity, enabling low-toxicity solvent systems for automotive and coatings applications. Concurrently, German chemical clusters are piloting green hydrogen in etherification processes for oxygenated solvents, targeting a 12% reduction in energy intensity by late 2026.

India Industrial Cleaning Solvents Market: Hub Development, Import Substitution, and Waste-to-Solvent Innovation

India’s industrial cleaning solvents sector is transitioning toward domestic capability building and circular feedstock utilization. In 2025, the government designated new Petroleum, Chemical, and Petrochemical Investment Regions in Gujarat, offering fiscal incentives for manufacturers producing high-purity industrial cleaners for pharmaceuticals and textiles. These hubs are designed to integrate upstream raw materials, solvent synthesis, and compliant waste treatment infrastructure.

Domestic producers are scaling purification capabilities. In late 2025, Gujarat Alkalies and Chemicals Ltd. optimized high-purity solvent lines to support localized pharmaceutical-grade cleaning agents, reducing dependence on East Asian imports. India is also emerging as a testbed for circular solvent innovation. Collaborations with European technology providers such as Clariter have enabled pilot plants that convert plastic waste into ultra-pure industrial solvents, aligning solvent production with waste reduction and domestic feedstock security.

Japan Industrial Cleaning Solvents Market: Precision Manufacturing Demand and Wafer-Fab Readiness

Japan’s industrial cleaning solvents market is closely tied to precision manufacturing and semiconductor fabrication. In April 2025, the Ministry of Economy, Trade, and Industry reported a manufacturing production index of 101.0, reflecting expansion in machinery and electronics output. This industrial momentum has translated into rising demand for specialized hydrocarbon solvents used in precision equipment maintenance, where low residue and consistent solvency are critical.

Capacity investments are reinforcing this trajectory. Shin-Etsu Chemical is scheduled to complete a major expansion of high-purity cleaning intermediates by the second quarter of 2026. The expansion targets global 12-inch wafer fabrication requirements, strengthening Japan’s role in supplying ultra-clean solvents for advanced semiconductor manufacturing and reinforcing its position in high-spec industrial cleaning solvent supply chains.

Industrial Cleaning Solvents Industry: Country-Level Strategic Overview

Industrial Cleaning Solvents Market County Level Snapshot

|

Country

|

Primary Policy or Demand Driver

|

Key Industrial Response

|

Structural Direction

|

|

United States

|

Semiconductor onshoring, PFAS reporting, VOC limits

|

Domestic electronic-grade solvents, bio-based adoption

|

Supply security and regulatory-compliant reformulation

|

|

China

|

Mandatory standards and VOC taxation

|

High-solid, water-based, and electronic-grade solvents

|

Policy-driven upgrading at scale

|

|

Germany

|

Circular economy and REACH pressure

|

Solvent regeneration, bio-based intermediates

|

Low-carbon and substitute-ready solvent systems

|

|

India

|

Chemical hubs and import substitution

|

High-purity local production, waste-to-solvent pilots

|

Domestic capability with circular feedstocks

|

|

Japan

|

Precision manufacturing and wafer-fab expansion

|

High-purity solvent capacity build-out

|

Semiconductor-aligned solvent specialization

|

Industrial Cleaning Solvents Market Report Scope

Industrial Cleaning Solvents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$76.8 Billion

|

|

Market Size (2034)

|

$115.1 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Product Type (Hydrocarbon Solvents, Oxygenated Solvents, Chlorinated Solvents, Bio-Based and Green Solvents, Halogenated Solvents), By Function (Degreasing, Precision Cleaning, Solvent-Based Stripping, Surface Preparation, Cold Cleaning and Vapor Degreasing), By End-Use Industry (Aerospace and Defense, Automotive, Electronics and Semiconductors, Manufacturing and Industrial, Healthcare and Pharmaceutical, Pulp and Paper)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Exxon Mobil Corporation, Shell plc, BASF SE, Dow Inc., LyondellBasell Industries N.V., Eastman Chemical Company, Arkema S.A., Celanese Corporation, Solvay S.A., Shin-Etsu Chemical Co., Ltd., Huntsman Corporation, Ashland Inc., Honeywell International Inc., Nouryon B.V., Gujarat Alkalies and Chemicals Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Cleaning Solvents Market Segmentation

By Product Type

- Hydrocarbon Solvents

- Aliphatic

- Aromatic

- Isoparaffins

- Oxygenated Solvents

- Alcohols

- Ketones

- Esters

- Glycols and Glycol Ethers

- Chlorinated Solvents

- Trichloroethylene

- Methylene Chloride

- Perchloroethylene

- Bio-Based and Green Solvents

- Bio-Esters

- Terpenes

- Bio-Ethanol

- Bio-Methanol

- Halogenated Solvents

- Hydrofluoroethers

- Fluorinated Solvents

By Function

- Degreasing

- Precision Cleaning

- Solvent-Based Stripping

- Surface Preparation

- Cold Cleaning and Vapor Degreasing

By End-Use Industry

- Aerospace and Defense

- Automotive

- Electronics and Semiconductors

- Manufacturing and Industrial

- Healthcare and Pharmaceutical

- Pulp and Paper

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Industrial Cleaning Solvents Industry

- Exxon Mobil Corporation

- Shell plc

- BASF SE

- Dow Inc.

- LyondellBasell Industries N.V.

- Eastman Chemical Company

- Arkema S.A.

- Celanese Corporation

- Solvay S.A.

- Shin-Etsu Chemical Co., Ltd.

- Huntsman Corporation

- Ashland Inc.

- Honeywell International Inc.

- Nouryon B.V.

- Gujarat Alkalies and Chemicals Limited

*- List not Exhaustive