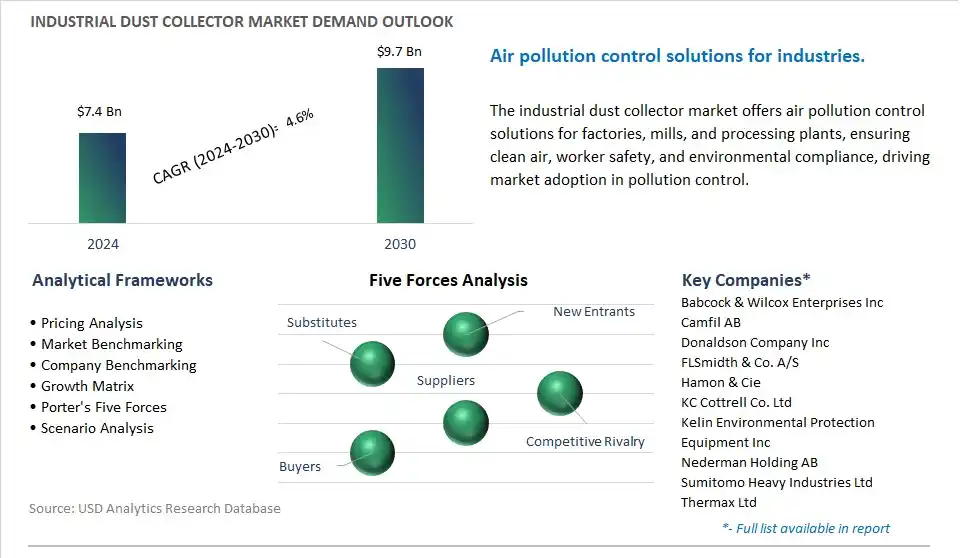

The global Industrial Dust Collector Market is poised to register a 4.6% CAGR from $7.4 Billion in 2024 to $9.7 Billion in 2030.

The global Industrial Dust Collector Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Baghouse Dust Collector, Cartridge Dust Collector, Wet Scrubbers, Inertial Separators, Electrostatic Precipitator, Others), By End-User (Food & Beverage, Pharmaceutical, Energy & Power, Steel, Cement, Mining, Others), By Form (Dry, Wet), By Mobility (Portable, Fixed).

An Introduction to Global Industrial Dust Collector Market in 2024

Industrial dust collectors are equipment used to capture and remove airborne dust, particulates, and contaminants generated by industrial processes such as grinding, cutting, sanding, and material handling, ensuring worker safety, regulatory compliance, and environmental protection. One key trend shaping the future of industrial dust collectors is the adoption of advanced filtration technologies and modular system designs to improve dust collection efficiency, energy savings, and maintenance convenience while reducing operational costs and environmental footprint. Dust collector manufacturers are developing next-generation filter media, such as nanofiber filters, reverse pulse cleaning, and electrostatic precipitators, with enhanced particle capture efficiency and lower pressure drop, enabling higher airflows and longer filter lifespans in demanding industrial environments. Additionally, advancements in dust collector system integration, such as centralized control panels, remote monitoring sensors, and IoT connectivity, are optimizing system performance, adaptability, and scalability to accommodate fluctuating dust load conditions and production requirements. Moreover, the integration of predictive maintenance algorithms, real-time monitoring, and data analytics is enabling condition-based maintenance strategies, proactive filter replacement scheduling, and continuous optimization of dust collection operations, ensuring compliance with air quality standards and minimizing downtime for industrial operations. As industries prioritize worker health and environmental stewardship, the industrial dust collector industry is poised for innovation and growth, with opportunities for collaboration, technology integration, and market expansion to meet the evolving needs of manufacturers, facility managers, and regulatory authorities.

Industrial Dust Collector Market Competitive Landscape

The market report analyses the leading companies in the industry including Babcock & Wilcox Enterprises Inc, Camfil AB, Donaldson Company Inc, FLSmidth & Co. A/S, Hamon & Cie, KC Cottrell Co. Ltd, Kelin Environmental Protection Equipment Inc, Nederman Holding AB, Sumitomo Heavy Industries Ltd, Thermax Ltd.

Industrial Dust Collector Market Dynamics

Industrial Dust Collector Market Trend: Increasing Focus on Air Quality and Workplace Safety Regulations

A prominent trend in the industrial dust collector market is the increasing focus on air quality and workplace safety regulations. With growing awareness about the health hazards associated with airborne particulate matter, governments worldwide are implementing stringent regulations to limit emissions and ensure safer working environments in industrial facilities. The trend is driving the adoption of industrial dust collectors, which are essential for capturing and removing dust, fumes, and other airborne pollutants generated during manufacturing processes. Companies are investing in advanced dust collection systems that offer higher efficiency, lower maintenance requirements, and compliance with regulatory standards, thereby addressing both environmental concerns and occupational health risks.

Industrial Dust Collector Market Driver: Growth in Industrial Manufacturing Activities

The growth in industrial manufacturing activities serves as a significant driver for the industrial dust collector market. As industrial production expands across various sectors such as automotive, metalworking, pharmaceuticals, and food processing, there is a corresponding increase in the generation of airborne particulates and contaminants. Industrial dust collectors play a crucial role in maintaining clean air quality within manufacturing facilities, protecting machinery from dust-related damage, and ensuring compliance with regulatory emissions standards. The rising demand for efficient and reliable dust collection solutions is driven by the need to improve productivity, prolong equipment lifespan, and create safer working environments for employees in industrial settings.

Industrial Dust Collector Market Opportunity: Integration of IoT and Smart Monitoring Technologies

An emerging opportunity in the industrial dust collector market is the integration of IoT (Internet of Things) and smart monitoring technologies. With the advent of Industry 4.0 and the digitalization of industrial processes, there is a growing demand for dust collection systems equipped with sensors, connectivity, and data analytics capabilities. Smart dust collectors can provide real-time monitoring of air quality parameters, filter performance, equipment status, and energy consumption, allowing for proactive maintenance, remote diagnostics, and optimization of operational efficiency. By harnessing the power of IoT and smart technologies, manufacturers can offer innovative dust collection solutions that deliver enhanced performance, reliability, and cost-effectiveness, thus catering to the evolving needs of industrial customers seeking to improve sustainability and operational excellence.

Industrial Dust Collector Market Ecosystem

The industrial dust collector market involves diverse key stages, with companies specializing in different aspects of the Market Ecosystem. The raw material acquisition includes sourcing steel and other metals from suppliers including ArcelorMittal and Nippon Steel Corporation for fabricating dust collector components, as well as obtaining filter media from companies including 3M and Freudenberg Group. Manufacturing is characterized by the presence of industrial dust collector manufacturers including Donaldson Company Inc. and Nederman Holding AB, which design and engineer various types of dust collectors tailored to customer requirements. Additionally, OEM manufacturers handle production for specific applications.

Distribution channels encompass industrial equipment distributors including Grainger and WESCO International, which supply a range of industrial equipment including dust collectors to diverse industries. Engineering services are provided by companies including Fluor Corporation and Bechtel Corporation for large-scale industrial projects, assisting with dust collector selection, integration, and installation. End-users across manufacturing industries utilize dust collectors for controlling airborne dust particles generated during processes including metalworking, woodworking, pharmaceuticals, and food processing. Dust collectors also find applications in the power generation industry for capturing particulate matter from flue gas emissions, as well as in construction activities and various industrial settings for air pollution control.

Industrial Dust Collector Market Share Analysis: Baghouse Dust Collector held the dominant revenue share in 2024

The baghouse dust collector segment is the largest sector in the Industrial Dust Collector Market, driven by diverse crucial factors contributing to its dominance. Baghouse dust collectors offer high efficiency in capturing and removing particulate matter from industrial air streams, making them widely preferred in various industries such as manufacturing, mining, and power generation. Their robust design, versatility, and ability to handle high volumes of dust make baghouse collectors suitable for a wide range of applications, from fine dust particles to coarse materials. In addition, stringent environmental regulations mandating the reduction of air pollution and the need for clean air in industrial facilities propel the demand for effective dust collection solutions like baghouse collectors. Additionally, advancements in baghouse technology, including the integration of pulse-jet cleaning systems and filter media enhancements, further enhance their performance and efficiency, solidifying their position as the largest segment in the industrial dust collector market. As industries prioritize air quality and compliance with regulatory standards, the baghouse dust collector segment is expected to maintain its dominance and witness continued growth in the coming years.

Industrial Dust Collector Market Share Analysis: Energy and Power is the fastest growing market segment over the forecast period to 2030

The energy and power segment is the fastest-growing sector in the Industrial Dust Collector Market, driven by diverse critical factors fueling its rapid expansion. With the increasing global focus on sustainability and environmental protection, there's a growing demand for effective dust collection solutions in the energy and power industry. Power plants, including coal-fired, natural gas, and biomass facilities, generate significant amounts of dust and particulate matter during the combustion process, posing environmental and health risks. Industrial dust collectors play a crucial role in capturing and removing these pollutants, ensuring compliance with air quality regulations, and minimizing the impact on surrounding communities. In addition, the shift toward renewable energy sources such as wind and solar necessitates efficient dust collection systems during the construction and maintenance of these facilities. Additionally, technological advancements in dust collection technology, such as the development of high-efficiency particulate air (HEPA) filters and electrostatic precipitators, further drive the adoption of dust collectors in the energy and power sector. As the energy industry continues to transition toward cleaner and more sustainable practices, the demand for industrial dust collectors in this segment is expected to witness significant growth, presenting opportunities for market expansion and innovation.

Industrial Dust Collector Market Share Analysis: Dry is the fastest growing market segment over the forecast period to 2030

The dry segment is the fastest-growing sector in the Industrial Dust Collector Market, driven by diverse pivotal factors propelling its rapid expansion. Dry dust collection systems offer numerous advantages over wet systems, including lower operating costs, reduced water consumption, and easier maintenance. With increasing concerns about water scarcity and environmental sustainability, industries are increasingly favoring dry dust collectors to minimize water usage and discharge. In addition, dry dust collectors are highly efficient in capturing and removing various types of particulate matter, including fine dust particles and toxic pollutants, from industrial air streams. Additionally, advancements in filtration technology, such as the development of high-efficiency filter media and pulse-jet cleaning systems, further enhance the performance and efficiency of dry dust collectors, making them a preferred choice for industries seeking cost-effective and sustainable dust collection solutions. As industries prioritize air quality and regulatory compliance, the dry segment of the industrial dust collector market is poised for significant growth, presenting lucrative opportunities for industry stakeholders.

Industrial Dust Collector Market Report Scope-

By Type

Baghouse Dust Collector

-Woven

-Non-Woven

Cartridge Dust Collector

Wet Scrubbers

Inertial Separators

Electrostatic Precipitator

Others

By End-User

Food & Beverage

Pharmaceutical

Energy & Power

Steel

Cement

Mining

Others

By Form

Dry

Wet

By Mobility

Portable

Fixed

Industrial Dust Collector Market Companies Profiled

Babcock & Wilcox Enterprises Inc

Camfil AB

Donaldson Company Inc

FLSmidth & Co. A/S

Hamon & Cie

KC Cottrell Co. Ltd

Kelin Environmental Protection Equipment Inc

Nederman Holding AB

Sumitomo Heavy Industries Ltd

Thermax Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Industrial Dust Collector Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Industrial Dust Collector Market Size Outlook, $ Million, 2021 to 2030

3.2 Industrial Dust Collector Market Outlook by Type, $ Million, 2021 to 2030

3.3 Industrial Dust Collector Market Outlook by Product, $ Million, 2021 to 2030

3.4 Industrial Dust Collector Market Outlook by Application, $ Million, 2021 to 2030

3.5 Industrial Dust Collector Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Industrial Dust Collector Industry

4.2 Key Market Trends in Industrial Dust Collector Industry

4.3 Potential Opportunities in Industrial Dust Collector Industry

4.4 Key Challenges in Industrial Dust Collector Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Industrial Dust Collector Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Industrial Dust Collector Market Outlook by Segments

7.1 Industrial Dust Collector Market Outlook by Segments, $ Million, 2021- 2030

By Type

Baghouse Dust Collector

-Woven

-Non-Woven

Cartridge Dust Collector

Wet Scrubbers

Inertial Separators

Electrostatic Precipitator

Others

By End-User

Food & Beverage

Pharmaceutical

Energy & Power

Steel

Cement

Mining

Others

By Form

Dry

Wet

By Mobility

Portable

Fixed

8 North America Industrial Dust Collector Market Analysis and Outlook To 2030

8.1 Introduction to North America Industrial Dust Collector Markets in 2024

8.2 North America Industrial Dust Collector Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Industrial Dust Collector Market size Outlook by Segments, 2021-2030

By Type

Baghouse Dust Collector

-Woven

-Non-Woven

Cartridge Dust Collector

Wet Scrubbers

Inertial Separators

Electrostatic Precipitator

Others

By End-User

Food & Beverage

Pharmaceutical

Energy & Power

Steel

Cement

Mining

Others

By Form

Dry

Wet

By Mobility

Portable

Fixed

9 Europe Industrial Dust Collector Market Analysis and Outlook To 2030

9.1 Introduction to Europe Industrial Dust Collector Markets in 2024

9.2 Europe Industrial Dust Collector Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Industrial Dust Collector Market Size Outlook by Segments, 2021-2030

By Type

Baghouse Dust Collector

-Woven

-Non-Woven

Cartridge Dust Collector

Wet Scrubbers

Inertial Separators

Electrostatic Precipitator

Others

By End-User

Food & Beverage

Pharmaceutical

Energy & Power

Steel

Cement

Mining

Others

By Form

Dry

Wet

By Mobility

Portable

Fixed

10 Asia Pacific Industrial Dust Collector Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Industrial Dust Collector Markets in 2024

10.2 Asia Pacific Industrial Dust Collector Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Industrial Dust Collector Market size Outlook by Segments, 2021-2030

By Type

Baghouse Dust Collector

-Woven

-Non-Woven

Cartridge Dust Collector

Wet Scrubbers

Inertial Separators

Electrostatic Precipitator

Others

By End-User

Food & Beverage

Pharmaceutical

Energy & Power

Steel

Cement

Mining

Others

By Form

Dry

Wet

By Mobility

Portable

Fixed

11 South America Industrial Dust Collector Market Analysis and Outlook To 2030

11.1 Introduction to South America Industrial Dust Collector Markets in 2024

11.2 South America Industrial Dust Collector Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Industrial Dust Collector Market size Outlook by Segments, 2021-2030

By Type

Baghouse Dust Collector

-Woven

-Non-Woven

Cartridge Dust Collector

Wet Scrubbers

Inertial Separators

Electrostatic Precipitator

Others

By End-User

Food & Beverage

Pharmaceutical

Energy & Power

Steel

Cement

Mining

Others

By Form

Dry

Wet

By Mobility

Portable

Fixed

12 Middle East and Africa Industrial Dust Collector Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Industrial Dust Collector Markets in 2024

12.2 Middle East and Africa Industrial Dust Collector Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Industrial Dust Collector Market size Outlook by Segments, 2021-2030

By Type

Baghouse Dust Collector

-Woven

-Non-Woven

Cartridge Dust Collector

Wet Scrubbers

Inertial Separators

Electrostatic Precipitator

Others

By End-User

Food & Beverage

Pharmaceutical

Energy & Power

Steel

Cement

Mining

Others

By Form

Dry

Wet

By Mobility

Portable

Fixed

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Babcock & Wilcox Enterprises Inc

Camfil AB

Donaldson Company Inc

FLSmidth & Co. A/S

Hamon & Cie

KC Cottrell Co. Ltd

Kelin Environmental Protection Equipment Inc

Nederman Holding AB

Sumitomo Heavy Industries Ltd

Thermax Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Baghouse Dust Collector

-Woven

-Non-Woven

Cartridge Dust Collector

Wet Scrubbers

Inertial Separators

Electrostatic Precipitator

Others

By End-User

Food & Beverage

Pharmaceutical

Energy & Power

Steel

Cement

Mining

Others

By Form

Dry

Wet

By Mobility

Portable

Fixed

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)