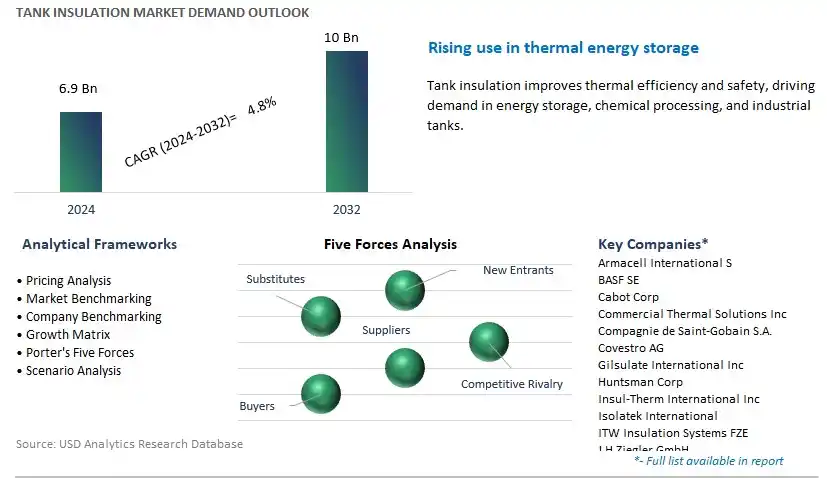

Global Tank Insulation Market Size is valued at $6.9 Billion in 2024 and is forecast to register a growth rate (CAGR) of 4.8% to reach $10 Billion by 2032.

The global Tank Insulation Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Material (PU & PIR, Rockwool, Fiberglass, Elastomeric foam, Cellular Glass, EPS, Others), By Type (Storage Tank Insulation, Transportation Tank Insulation), By Temperature (Cold Insulation, Hot Insulation), By End-User (Oil & Gas, Chemical, Food & Beverage, Energy & Power, Others).

An Introduction to Tank Insulation Market in 2024

Tank insulation plays a critical role in maintaining temperature stability and energy efficiency in industrial storage tanks and vessels in 2024. These insulated tanks are utilized across various industries, including oil and gas, chemical processing, food and beverage, and pharmaceuticals, where the storage of liquids at controlled temperatures is essential. Tank insulation systems typically consist of insulation materials such as foam panels, mineral wool, or aerogels, enclosed within protective jackets or cladding. By minimizing heat transfer and reducing thermal losses, tank insulation helps to preserve product quality, prevent freezing or overheating, and minimize energy consumption associated with heating or cooling processes. With increasing emphasis on energy efficiency, environmental sustainability, and regulatory compliance, the demand for effective tank insulation solutions s to grow, driving innovations in insulation materials, installation techniques, and thermal performance.

Tank Insulation Market Competitive Landscape

The market report analyses the leading companies in the industry including Armacell International S, BASF SE, Cabot Corp, Commercial Thermal Solutions Inc, Compagnie de Saint-Gobain S.A., Covestro AG, Gilsulate International Inc, Huntsman Corp, Insul-Therm International Inc, Isolatek International, ITW Insulation Systems FZE, J H Ziegler GmbH, Johns Manville, Kingspan Group PLC, Knauf Insulation Inc, L'ISOLANTE K-FLEX SpA, MBI Products Company Inc, Microtherm NV, Morgan Advanced Materials, NMC SA., Owens Corning, Pacor Inc, Pittsburgh Corning Corp, Polyguard Products Inc, Rmax Operating LLC, Rockwool A/S, Roxul Inc, Sika AG, The Dow Chemical Company, and others.

Tank Insulation Market Dynamics

Market Trend: Growing Demand for Energy-Efficient Solutions in Industrial Applications

A significant trend in the tank insulation market is the growing demand for energy-efficient solutions in industrial applications. Tank insulation plays a crucial role in maintaining process temperature stability, preventing heat loss or gain, and reducing energy consumption in storage tanks used in various industries such as oil and gas, chemical processing, food and beverage, and pharmaceuticals. With increasing focus on sustainability, energy conservation, and operational efficiency, industries are investing in insulation systems that optimize thermal performance, minimize heat transfer losses, and reduce greenhouse gas emissions. Additionally, regulatory requirements and environmental mandates aimed at reducing carbon footprint and improving energy efficiency drive the adoption of tank insulation solutions that meet stringent performance standards. As industries seek to minimize operational costs, enhance process reliability, and meet sustainability goals, the demand for tank insulation materials and systems that offer superior thermal insulation properties and long-term durability is expected to increase.

Market Driver: Expansion of Industrial Infrastructure and Process Automation

The primary driver for the tank insulation market is the expansion of industrial infrastructure and process automation across key end-user industries. With economic growth, urbanization, and industrialization driving investments in infrastructure development, there is a growing need for storage tanks to store and handle liquids, chemicals, and bulk materials efficiently and safely. Tank insulation is essential to ensure the integrity and performance of storage tanks in diverse operating conditions, including extreme temperatures, corrosive environments, and hazardous processes. Furthermore, the adoption of process automation technologies such as IoT (Internet of Things), SCADA (Supervisory Control and Data Acquisition), and advanced control systems drives the demand for insulated tanks that maintain precise temperature control, minimize thermal fluctuations, and ensure product quality and safety. As industries modernize their manufacturing facilities, upgrade storage infrastructure, and implement smart technologies for process optimization and predictive maintenance, the demand for tank insulation solutions that support reliable and efficient operations is expected to grow, supported by the need for high-performance insulation materials and systems that meet industry-specific requirements.

Market Opportunity: Innovation in Insulation Materials and Systems for Challenging Applications

A significant opportunity for the tank insulation market lies in innovation in insulation materials and systems tailored to address the unique challenges of various industrial applications and operating environments. Manufacturers can invest in research and development to develop advanced insulation materials such as aerogels, vacuum insulation panels, and high-performance foams with superior thermal conductivity, compressive strength, and resistance to moisture, chemicals, and UV degradation. Additionally, there is an opportunity to optimize insulation system designs by integrating complementary components such as vapor barriers, jacketing materials, and corrosion protection coatings to enhance durability, weather resistance, and ease of installation. By collaborating with tank designers, engineering firms, and end-users, insulation providers can develop customized solutions that address specific application requirements, regulatory standards, and performance specifications. Furthermore, there is an opportunity to leverage digitalization and data analytics to offer predictive maintenance and condition monitoring services that optimize insulation performance, reduce energy consumption, and extend asset lifespan. By embracing innovation and differentiation, insulation manufacturers can capture market opportunities, expand their product offerings, and position themselves as trusted partners in the global tank insulation market.

Tank Insulation Market Share Analysis: PU & PIR segment generated the highest revenue in 2024

Among the various materials used in tank insulation, the PU & PIR (Polyurethane & Polyisocyanurate) segment is the largest and most dominant player. This leadership position can be attributed to PU & PIR insulation materials offer excellent thermal performance, moisture resistance, and durability, making them ideal for insulating tanks used in various industries such as oil and gas, chemical processing, and food and beverage. Their high insulation efficiency helps maintain consistent temperatures within storage tanks, reducing energy consumption and operational costs for industrial facilities. Moreover, PU & PIR insulation systems are lightweight and easy to install, allowing for faster construction and retrofitting of tank insulation projects. Additionally, the PU & PIR segment benefits from ongoing technological advancements, such as the development of low-temperature formulations and fire-retardant additives, which further enhance their suitability for a wide range of tank insulation applications. With their superior performance, ease of installation, and versatility across industries, the PU & PIR segment is poised to maintain its dominance and drive continued growth in the tank insulation market.

Tank Insulation Market Share Analysis: Transportation Tank is poised to register the fastest CAGR over the forecast period

Among the segments in the tank insulation market, the Transportation Tank Insulation segment is the fastest-growing segment. In particular, with the increasing globalization of trade and the expansion of industries such as chemicals, pharmaceuticals, and food and beverage, the demand for insulated transportation tanks for bulk liquid transport is on the rise. Transportation tank insulation plays a critical role in maintaining the temperature integrity of sensitive liquids during transit, ensuring product quality and safety. Moreover, stringent regulations regarding the transportation of hazardous and temperature-sensitive materials further drive the adoption of insulated tanks to comply with safety standards and mitigate risks during transit. Additionally, advancements in insulation materials and design technologies enable the development of lightweight yet highly efficient insulation solutions for transportation tanks, reducing energy consumption and operational costs for logistics companies. With the growing emphasis on product integrity, safety, and efficiency in liquid transport, the Transportation Tank Insulation segment is poised to sustain its rapid growth trajectory in the tank insulation market.

Tank Insulation Market Share Analysis: Cold Insulation segment generated the highest revenue in 2024

Among the temperature segments in the tank insulation market, the Cold Insulation segment is the largest and most dominant player. This leadership position can be attributed to cold insulation is extensively used in industries such as oil and gas, chemical processing, and food storage, where the storage and transport of liquids at low temperatures are prevalent. Cold insulation materials such as polyurethane foam, fiberglass, and cellular glass offer excellent thermal resistance and moisture barrier properties, ensuring the integrity of stored liquids and preventing energy loss. Moreover, the demand for cold insulation is driven by the growing need to comply with strict temperature control requirements for sensitive products such as liquefied gases, chemicals, and perishable goods. Additionally, advancements in cold insulation technologies, including the development of high-performance materials and innovative installation techniques, further bolster the dominance of the Cold Insulation segment in the tank insulation market. With the increasing focus on energy efficiency, product quality, and regulatory compliance in cold storage and transport applications, the Cold Insulation segment is poised to maintain its leadership and drive continued growth in the tank insulation market.

Tank Insulation Market Share Analysis: Energy & Power segment is poised to register the fastest CAGR over the forecast period

Among the various end-user industries in the tank insulation market, the Energy & Power segment is the fastest-growing segment. In particular, the energy and power sector encompass a wide range of applications requiring insulated tanks, including thermal energy storage, power generation, and renewable energy installations such as solar thermal and geothermal systems. Insulated tanks play a critical role in maintaining the efficiency and reliability of energy storage and distribution systems by minimizing heat loss or gain during storage and transport of fluids such as hot water, steam, and thermal oils. Moreover, with the increasing focus on renewable energy sources and energy efficiency initiatives, there is a growing demand for insulated tanks in solar power plants, biomass facilities, and district heating systems. Additionally, the expansion of the energy storage market, driven by the integration of intermittent renewable energy sources and grid stabilization efforts, further fuels the demand for insulated tanks in energy storage applications. With the evolving energy landscape and the growing emphasis on sustainability and efficiency in power generation and distribution, the Energy & Power segment is poised to maintain its rapid growth trajectory in the tank insulation market.

Tank Insulation Market

By Material

PU & PIR

Rockwool

Fiberglass

Elastomeric foam

Cellular Glass

EPS

Others

By Type

Storage Tank Insulation

Transportation Tank Insulation

By Temperature

Cold Insulation

Hot Insulation

By End-User

Oil & Gas

Chemical

Food & Beverage

Energy & Power

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Tank Insulation Companies Profiled in the Study

Armacell International S

BASF SE

Cabot Corp

Commercial Thermal Solutions Inc

Compagnie de Saint-Gobain S.A.

Covestro AG

Gilsulate International Inc

Huntsman Corp

Insul-Therm International Inc

Isolatek International

ITW Insulation Systems FZE

J H Ziegler GmbH

Johns Manville

Kingspan Group PLC

Knauf Insulation Inc

L'ISOLANTE K-FLEX SpA

MBI Products Company Inc

Microtherm NV

Morgan Advanced Materials

NMC SA.

Owens Corning

Pacor Inc

Pittsburgh Corning Corp

Polyguard Products Inc

Rmax Operating LLC

Rockwool A/S

Roxul Inc

Sika AG

The Dow Chemical Company

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Tank Insulation Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Tank Insulation Market Size Outlook, $ Million, 2021 to 2032

3.2 Tank Insulation Market Outlook by Type, $ Million, 2021 to 2032

3.3 Tank Insulation Market Outlook by Product, $ Million, 2021 to 2032

3.4 Tank Insulation Market Outlook by Application, $ Million, 2021 to 2032

3.5 Tank Insulation Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Tank Insulation Industry

4.2 Key Market Trends in Tank Insulation Industry

4.3 Potential Opportunities in Tank Insulation Industry

4.4 Key Challenges in Tank Insulation Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Tank Insulation Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Tank Insulation Market Outlook by Segments

7.1 Tank Insulation Market Outlook by Segments, $ Million, 2021- 2032

By Material

PU & PIR

Rockwool

Fiberglass

Elastomeric foam

Cellular Glass

EPS

Others

By Type

Storage Tank Insulation

Transportation Tank Insulation

By Temperature

Cold Insulation

Hot Insulation

By End-User

Oil & Gas

Chemical

Food & Beverage

Energy & Power

Others

8 North America Tank Insulation Market Analysis and Outlook To 2032

8.1 Introduction to North America Tank Insulation Markets in 2024

8.2 North America Tank Insulation Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Tank Insulation Market size Outlook by Segments, 2021-2032

By Material

PU & PIR

Rockwool

Fiberglass

Elastomeric foam

Cellular Glass

EPS

Others

By Type

Storage Tank Insulation

Transportation Tank Insulation

By Temperature

Cold Insulation

Hot Insulation

By End-User

Oil & Gas

Chemical

Food & Beverage

Energy & Power

Others

9 Europe Tank Insulation Market Analysis and Outlook To 2032

9.1 Introduction to Europe Tank Insulation Markets in 2024

9.2 Europe Tank Insulation Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Tank Insulation Market Size Outlook by Segments, 2021-2032

By Material

PU & PIR

Rockwool

Fiberglass

Elastomeric foam

Cellular Glass

EPS

Others

By Type

Storage Tank Insulation

Transportation Tank Insulation

By Temperature

Cold Insulation

Hot Insulation

By End-User

Oil & Gas

Chemical

Food & Beverage

Energy & Power

Others

10 Asia Pacific Tank Insulation Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Tank Insulation Markets in 2024

10.2 Asia Pacific Tank Insulation Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Tank Insulation Market size Outlook by Segments, 2021-2032

By Material

PU & PIR

Rockwool

Fiberglass

Elastomeric foam

Cellular Glass

EPS

Others

By Type

Storage Tank Insulation

Transportation Tank Insulation

By Temperature

Cold Insulation

Hot Insulation

By End-User

Oil & Gas

Chemical

Food & Beverage

Energy & Power

Others

11 South America Tank Insulation Market Analysis and Outlook To 2032

11.1 Introduction to South America Tank Insulation Markets in 2024

11.2 South America Tank Insulation Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Tank Insulation Market size Outlook by Segments, 2021-2032

By Material

PU & PIR

Rockwool

Fiberglass

Elastomeric foam

Cellular Glass

EPS

Others

By Type

Storage Tank Insulation

Transportation Tank Insulation

By Temperature

Cold Insulation

Hot Insulation

By End-User

Oil & Gas

Chemical

Food & Beverage

Energy & Power

Others

12 Middle East and Africa Tank Insulation Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Tank Insulation Markets in 2024

12.2 Middle East and Africa Tank Insulation Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Tank Insulation Market size Outlook by Segments, 2021-2032

By Material

PU & PIR

Rockwool

Fiberglass

Elastomeric foam

Cellular Glass

EPS

Others

By Type

Storage Tank Insulation

Transportation Tank Insulation

By Temperature

Cold Insulation

Hot Insulation

By End-User

Oil & Gas

Chemical

Food & Beverage

Energy & Power

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Armacell International S

BASF SE

Cabot Corp

Commercial Thermal Solutions Inc

Compagnie de Saint-Gobain S.A.

Covestro AG

Gilsulate International Inc

Huntsman Corp

Insul-Therm International Inc

Isolatek International

ITW Insulation Systems FZE

J H Ziegler GmbH

Johns Manville

Kingspan Group PLC

Knauf Insulation Inc

L'ISOLANTE K-FLEX SpA

MBI Products Company Inc

Microtherm NV

Morgan Advanced Materials

NMC SA.

Owens Corning

Pacor Inc

Pittsburgh Corning Corp

Polyguard Products Inc

Rmax Operating LLC

Rockwool A/S

Roxul Inc

Sika AG

The Dow Chemical Company

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise