Industrial Maintenance Coatings Market Size, Corrosion Protection Demand, and Asset Lifecycle Optimization Outlook

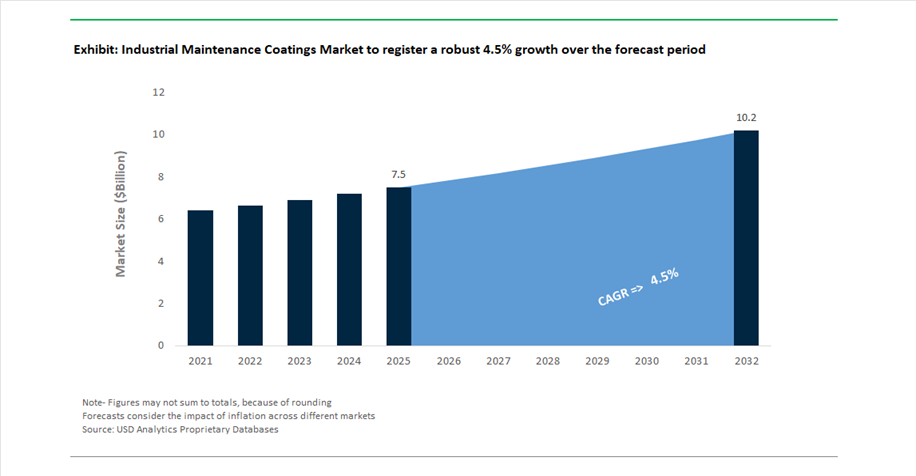

The global industrial maintenance coatings market was valued at $7.5 billion in 2025 and is projected to reach $10.2 billion by 2032, growing at a CAGR of 4.5%. This steady expansion reflects the critical role of industrial protective coatings, corrosion-resistant coatings, high-temperature maintenance coatings, and CUI-resistant coating systems in extending the operational lifespan of assets across oil & gas, power generation, marine, infrastructure, and heavy industrial sectors.

A primary growth driver is the escalating global cost of corrosion, estimated in trillions, which is pushing asset owners to adopt advanced maintenance coatings that reduce downtime, prevent structural degradation, and improve lifecycle cost efficiency. Technologies such as zinc-rich primers, epoxy-based coatings, polyurethane coatings, and silicone-based insulation coatings are increasingly deployed to protect assets exposed to extreme environments, thermal cycling, and chemical exposure. The shift toward corrosion under insulation (CUI) mitigation coatings is particularly significant in aging industrial infrastructure, where traditional insulation systems often accelerate corrosion risks.

The market is also evolving in response to stricter environmental regulations and sustainability targets, driving the adoption of low-VOC coatings, bio-based resins, and long-life maintenance solutions. Growth in renewable energy infrastructure, LNG terminals, and industrial retrofitting projects is creating new demand for coatings that can be applied efficiently without disrupting operations.

Bio-Based Coatings, and Advanced CUI Mitigation Technologies Reshaping Market Dynamics

The industrial maintenance coatings industry is undergoing strategic consolidation and innovation, with companies focusing on high-value protective solutions, sustainability, and operational efficiency. A major development occurred in February 2026, when AkzoNobel and Axalta confirmed a proposed $17 billion merger of equals, aiming to integrate AkzoNobel’s International® protective coatings brand with Axalta’s industrial maintenance portfolio. The combined entity targets $600 million in synergies by 2029, strengthening its position in global maintenance and repair coatings markets.

Strategic repositioning toward high-growth segments is also evident across leading players. Jotun reported record 2025 earnings of NOK 34.3 billion, driven by strong growth in its protective coatings segment, and is entering 2026 with a focus on expanding in the Middle East and Southeast Asia. Similarly, Hempel A/S launched its “Accelerate to Win” strategy in January 2026, prioritizing the maintenance and repair segment while shifting away from lower-margin commodity markets. This aligns with Hempel’s continued investment in Avantguard technology, an activated zinc primer that delivers self-healing corrosion protection, addressing micro-cracks before they propagate.

Innovation in coating technologies is increasingly centered on corrosion mitigation, operational efficiency, and sustainability. In April 2025, PPG Industries introduced PPG PITT-THERM 909, a silicone-based spray-on insulation coating designed to replace traditional cladding systems that trap moisture, directly addressing corrosion risks in industrial maintenance. Sherwin-Williams advanced this trend with its June 2025 upgrade of the FIRETEX M90/02 system, optimized for shop application, enabling coatings to be applied in controlled environments before installation, thereby improving coating consistency and long-term durability.

Sustainability-driven innovation is gaining traction, as demonstrated by Chugoku Marine Paints’ CMP NOVA 2000 Bio, launched in July 2025, which utilizes ISCC-certified bio-based epoxy resins to reduce the carbon footprint of maintenance cycles in chemical storage and tanker applications. At the same time, Carboline’s January 2024 launch of Carbothane DTM Mastic provides a one-coat solution for emergency maintenance, capable of application on surfaces up to 121°C, enabling “live maintenance” without operational shutdowns, a critical requirement for continuous industrial processes.

Competitive intensity in the market is also increasing, highlighted by the September 2025 legal dispute between Carboline and Sherwin-Williams over performance claims related to fire-resistant and high-heat maintenance coatings, reflecting heightened scrutiny over certification standards and product performance validation.

Regional expansion strategies continue to support market growth. Jotun’s May 2024 manufacturing facility in Algeria strengthens local production capabilities for North Africa’s energy sector, addressing rising local content requirements and reducing supply chain constraints.

Industrial Maintenance Coatings Market Share 2025: Preventive Strategies and Service Providers Drive Growth

Maintenance Type Insights: Preventive Maintenance Dominates with Asset Longevity and Cost Control

The preventive maintenance segment leads the industrial maintenance coatings market with a commanding 58% market share in 2025, driven by the growing emphasis on asset life extension and operational reliability. Industrial asset owners—including chemical plants, refineries, bridges, storage tanks, pipelines, and offshore platforms—are increasingly adopting scheduled recoating programs every 5–10 years based on condition monitoring metrics such as dry film thickness, coating adhesion, and corrosion progression (rust creep). This proactive approach minimizes the risk of unexpected failures, downtime, and costly emergency repairs, ensuring uninterrupted operations. Additionally, preventive maintenance enables better budget predictability, as these programs are integrated into annual capital expenditure plans, unlike corrective or emergency maintenance which require contingency funding. As industries prioritize long-term infrastructure durability and cost optimization, preventive maintenance coatings will continue to dominate the industrial maintenance coatings market.

Sales Channel Insights: Professional Service Providers Lead with Turnkey Coating Solutions

The professional service providers segment holds the largest 52% share in the industrial maintenance coatings market in 2025, reflecting strong demand for end-to-end coating application services. Industrial operators increasingly rely on specialized contractors who deliver turnkey solutions, including surface preparation (abrasive blasting to NACE No. 2 / SSPC-SP10 standards), coating application, inspection, and quality assurance. This approach eliminates the need for in-house expertise and ensures consistent coating performance in critical environments. Moreover, service providers take on significant safety and regulatory responsibilities, managing complex requirements such as confined space entry, fall protection, hazardous material handling, and environmental compliance permits. This transfer of liability is particularly valuable for asset owners in high-risk industries like oil & gas, marine, and heavy manufacturing. As maintenance operations become more complex and compliance-driven, professional service providers will remain the dominant channel in the industrial maintenance coatings market.

Industrial Maintenance Coatings Market Competitive Landscape: Asset Protection, Low-VOC Systems, and Infrastructure Lifecycle Optimization Driving Competition

The industrial maintenance coatings market is driven by infrastructure rehabilitation, energy transition projects, and demand for long-life corrosion protection systems. Leading players are focusing on low-VOC formulations, rapid-curing technologies, and integrated coating services to enhance asset durability, reduce downtime, and meet stringent environmental standards.

PPG drives integrated maintenance coating solutions with data center focus and sustainable product leadership

PPG Industries is a leading player in industrial maintenance coatings, leveraging integrated coating systems and strong financial performance. In April 2026, the company launched an end-to-end protective coatings suite for data centers, combining insulative, dielectric, and heat-reflective properties to reduce cooling demand. With $15.9 billion in 2025 revenue, PPG is focusing on high-margin industrial OEM and aerospace sectors following its architectural business divestiture. The company stands out as the only global provider combining coatings with in-house application expertise, enabling up to 25% faster project execution. 44% of its 2026 sales are derived from sustainably advantaged products, including low-VOC systems compliant with IEEE and UL standards. This integration of performance, sustainability, and service strengthens its leadership in maintenance coatings.

AkzoNobel strengthens global MRO dominance through strategic consolidation and low-GWP coating innovation

AkzoNobel N.V. is reinforcing its position in industrial maintenance coatings through strategic consolidation and sustainability-driven innovation. The company is progressing toward a $25 billion merger with Axalta, aimed at creating a global leader in performance coatings. It has divested non-core regional businesses, including Pakistan and India, to focus on high-growth industrial corridors in Western and Southeast Asia. AkzoNobel achieved a 14.2% adjusted EBITDA margin in 2026, supported by investments in advanced manufacturing facilities such as its Waukegan site. Its International® brand remains the benchmark in Maintenance & Repair (MRO) coatings, offering low-GWP solutions with up to 30-year durability. This strategic focus enhances its competitiveness in long-life industrial coatings.

Sherwin-Williams accelerates maintenance coatings adoption with rapid-curing systems and global distribution strength

The Sherwin-Williams Company is expanding its leadership in industrial maintenance coatings through innovation and operational scale. The company projects 2026 EPS of $11.50 to $11.90, supported by pricing strategies and strong EBITDA growth. Its Envirolastic® 2500 system enables single-coat application, reducing labor costs by 35% while maintaining premium finish performance. Sherwin-Williams is establishing a new global R&D center focused on low-VOC and waterborne maintenance coatings designed for high-corrosive environments. With over 5,000 stores globally, the company delivers just-in-time supply and on-site technical auditing for large infrastructure projects. This combination of efficiency, innovation, and distribution strengthens its market leadership.

Jotun drives offshore and energy maintenance coatings with robotic cleaning and high-performance PFP systems

Jotun A/S is a major player in industrial maintenance coatings, driven by strong performance in energy and offshore segments. The company reported record revenue of NOK 34.33 billion in 2026, supported by growth in offshore wind and oil & gas projects. Its Hull Performance Solutions and robotic Hull Skating systems represent a shift toward proactive maintenance, ensuring optimal asset performance. The Jotachar passive fire protection range offers mesh-free application, reducing installation time by up to 60% in critical infrastructure projects. Jotun has expanded production capacity in Asia-Pacific, a region holding 43.4% market share, to support growing demand. This focus on innovation and lifecycle optimization strengthens its competitive position.

Hempel advances sustainable maintenance coatings with strong financial growth and energy infrastructure focus

Hempel A/S is strengthening its presence in industrial maintenance coatings through sustainability and strategic focus on energy infrastructure. The company achieved a record 18.2% EBITDA margin in 2026, supported by strong growth in its marine and infrastructure segments. Its “Accelerate to Win” strategy prioritizes Energy & Infrastructure, generating €775 million in annual revenue. Hempel has reduced emissions by 70% since 2019 and is targeting a 90% reduction by the end of 2026 through localized production and green chemistry. Its Hempafire and Hempaguard technologies have contributed to significant CO2 reductions for customers. This integration of sustainability and performance enhances its competitive positioning.

RPM strengthens maintenance coatings portfolio with acquisitions and high-performance building envelope solutions

RPM International Inc. is expanding its role in the industrial maintenance coatings market through acquisitions and performance-driven solutions. The company reported record Q3 2026 sales of $1.61 billion, reflecting an 8.9% increase driven by demand for protective coatings and passive fire protection. Its acquisition of Kalzip GmbH enhances its building envelope capabilities, integrating roofing and façade systems into its maintenance portfolio. RPM reported strong regional growth, particularly in Europe and the Middle East, supported by infrastructure rehabilitation projects. Through its MAP strategy, the company is optimizing margins and driving EBIT growth despite market volatility. This strategic expansion strengthens RPM’s position in global maintenance coatings.

United States Industrial Maintenance Coatings Market: Infrastructure Rehabilitation and PFAS-Free Transition Driving Demand

The United States industrial maintenance coatings market is undergoing a structural transformation, fueled by large-scale infrastructure rehabilitation and the reshoring of advanced manufacturing. Federal initiatives such as the Infrastructure Investment and Jobs Act are accelerating the restoration of aging steel and concrete assets, significantly increasing demand for high-performance maintenance coatings such as zinc-rich primers and polyaspartic topcoats. These coatings are critical for extending asset lifespan across pipeline networks, bridges, and industrial facilities.

The reshoring of semiconductor manufacturing is also contributing to market expansion, with ultra-low-outgassing epoxy coatings being widely adopted in cleanroom exhaust systems. Regulatory developments, particularly the EPA’s PFAS Strategic Roadmap, are driving a shift toward nano-ceramic hybrid coatings that offer improved durability while meeting environmental compliance standards. Technological advancements such as AI-powered inspection drones are enhancing maintenance efficiency by identifying micro-fissures in protective coatings before failure occurs. Additionally, the development of hydrogen-ready coatings is supporting the transition toward hydrogen infrastructure by preventing embrittlement in repurposed pipelines. These factors collectively position the U.S. as a key innovation hub in the global industrial maintenance coatings market.

China Industrial Maintenance Coatings Market: Zero-VOC Mandates and Mega Infrastructure Driving Adoption

China continues to dominate the global industrial maintenance coatings market in terms of volume, supported by its vast industrial base and stringent environmental policies. The implementation of Zero-VOC mandates across major industrial zones has accelerated the transition toward water-based and solvent-free coating technologies, effectively eliminating traditional high-solvent maintenance systems. This regulatory shift is driving significant demand for environmentally friendly coatings that meet strict emission standards.

Large-scale infrastructure projects are further boosting market growth. The expansion of major water diversion systems has utilized high volumes of ceramic-epoxy coatings to prevent corrosion and ensure long-term operational efficiency. Technological advancements, including graphene-modified coatings, are extending maintenance cycles by providing enhanced durability and resistance to harsh environments. Additionally, increased domestic production of glass flake pigments is strengthening supply chains and reducing dependency on imports. The adoption of intumescent coatings in industrial parks, mandated by safety regulations, is further expanding application areas, reinforcing China’s leadership in industrial maintenance coatings.

Saudi Arabia Industrial Maintenance Coatings Market: Oil & Gas Expansion and Vision 2030 Infrastructure

Saudi Arabia is emerging as a key growth market for industrial maintenance coatings, driven by extensive oil and gas investments and infrastructure development under Vision 2030. The expansion of hydrocarbon production capacity is significantly increasing demand for heavy-duty protective coatings, particularly thick-film epoxy and passive fire protection (PFP) coatings used in subsea production equipment and cross-country pipelines.

Regulatory frameworks are playing a crucial role in shaping the market. Updated engineering standards mandate the use of advanced coatings such as fusion bonded epoxy systems to ensure long-term durability and corrosion resistance in extreme environments. Mega-projects like NEOM and the Red Sea development are further driving demand for UV-stable, low-VOC coatings capable of withstanding high desert temperatures. Strategic expansions by global coating manufacturers are enhancing local service capabilities, particularly through just-in-time maintenance hubs supporting offshore operations. Additionally, investments in green ammonia export terminals are creating new opportunities for specialized coatings designed to protect cryogenic storage systems.

Norway Industrial Maintenance Coatings Market: Offshore Life Extension and CCS Infrastructure Growth

Norway remains a global leader in industrial maintenance coatings, particularly for offshore applications and carbon capture and storage (CCS) infrastructure. The country’s focus on extending the lifespan of North Sea assets is driving demand for advanced maintenance coatings that can withstand extreme environmental conditions, including high salinity, temperature fluctuations, and mechanical stress.

The deployment of specialized coatings for CO₂ transport pipelines is a key development, ensuring durability under rapid pressure changes and preventing coating failure. Technological innovations such as self-healing coatings are improving asset reliability by repairing minor damage caused by ice or debris. Regulatory requirements aimed at reducing carbon footprints are also encouraging the adoption of bio-based resin coatings. Additionally, the growth of offshore wind energy is increasing demand for anti-corrosive coatings used in turbine foundations, particularly in splash zones exposed to harsh marine conditions. These advancements position Norway as a leader in high-performance maintenance coatings for offshore and energy applications.

Germany Industrial Maintenance Coatings Market: REACH Compliance and Sustainable Coating Innovation

Germany serves as the European hub for sustainable industrial maintenance coatings, driven by stringent REACH regulations and a strong focus on decarbonization. The country is leading the development of zero-VOC mineral-based coatings that provide long-term durability while meeting strict environmental standards. These coatings are gaining widespread adoption across industrial and infrastructure applications.

Circular economy initiatives are also shaping the market, with the commercialization of de-coatable coatings enabling full material recovery during maintenance cycles. Technological advancements such as UV-LED curing systems are improving manufacturing efficiency by reducing energy consumption. The growing hydrogen economy is driving demand for specialized ceramic-hybrid coatings that can withstand high-pressure hydrogen environments. Additionally, regulatory mandates requiring migration-tested coatings for food-processing equipment are expanding application areas. Germany’s leadership in radiative cooling coatings further highlights its commitment to energy-efficient industrial solutions.

India Industrial Maintenance Coatings Market: Maritime Expansion and PLI-Driven Industrial Growth

India is rapidly emerging as a high-growth market for industrial maintenance coatings, driven by maritime modernization and government-led industrial initiatives. Under the Maritime India Vision 2030, major ports are increasingly adopting glass flake epoxy coatings for structural steel maintenance, enhancing durability in harsh marine environments. This growth is supported by large-scale investments under the Production Linked Incentive (PLI) schemes, which are creating a strong domestic market for high-performance coatings.

Infrastructure development is another key driver, with the establishment of new industrial corridors increasing demand for maintenance-ready coatings across manufacturing facilities. Regulatory measures implemented by the Bureau of Indian Standards are ensuring quality compliance and eliminating sub-standard imports, further strengthening domestic production. The expansion of metro rail networks is also driving the adoption of waterborne anti-graffiti coatings for stations and rolling stock. Additionally, investments in localized blending facilities are improving supply chain efficiency, enabling faster delivery of customized coating solutions. These factors collectively position India as a critical growth market in the global industrial maintenance coatings industry.

Japan Industrial Maintenance Coatings Market: Smart Urban Renewal and Advanced Nano-Coating Technologies

Japan continues to lead the industrial maintenance coatings market through its focus on precision engineering and advanced material innovation. The country’s large-scale infrastructure renewal programs are driving demand for high-performance coatings that enhance durability and sustainability in urban environments. This includes the widespread adoption of nano-ceramic coatings designed for high-performance applications in industrial and automotive sectors.

Technological advancements are a key differentiator, with innovations such as anti-fogging nano-coatings providing superior clarity and reliability for industrial sensors and automotive systems. The development of radiative cooling coatings is enabling energy-efficient temperature management for industrial structures, reducing reliance on traditional cooling systems. Government support for recycled material technologies is promoting circular economy practices in the coatings industry. Additionally, Japan’s leadership in optical fiber maintenance coatings, utilizing zirconia-infused resins, is ensuring high thermal stability in extreme industrial conditions. These innovations reinforce Japan’s position as a global leader in advanced industrial maintenance coatings.

Industrial Maintenance Coatings Market Report Scope

Industrial Maintenance Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.5 Billion

|

|

Market Size (2032)

|

$10.2 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Resin Type (Epoxy, Polyurethane, Acrylic, Alkyd, Fluoropolymers, Polyester, Specialty Resins), By Technology (Solvent-borne Coatings, Water-borne Coatings, Powder Coatings, 100% Solids, Radiation-Cured), By End-Use Industry (Oil and Gas and Petrochemical, Energy and Power Generation, Infrastructure and Construction, Chemical Processing and Industrial Plants, Transportation and Marine, Metal Processing and Manufacturing, Water and Wastewater Treatment, Other Industrial), By Substrate (Steel and Ferrous Metals, Concrete and Masonry, Non-Ferrous Metals, Plastics and Composites), By Functional Property (Anti-Corrosive, Chemical and Acid Resistance, Abrasion and Impact Resistance, Thermal and Fire Resistance, Weather and UV Resistance), By Maintenance Type (Preventive Maintenance, Corrective, Emergency Maintenance), By Sales Channel (Direct Sales, Specialty Industrial Distributors, Professional Service Providers)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., RPM International Inc., Jotun A/S, Hempel A/S, Axalta Coating Systems Ltd., Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Sika AG, Tnemec Company, Inc., Asian Paints Limited, KCC Corporation, Belzona International Ltd., Teknos Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Maintenance Coatings Market Segmentation

By Resin Type

- Epoxy

- Polyurethane

- Acrylic

- Alkyd

- Fluoropolymers

- Polyester

- Specialty Resins

By Technology

- Solvent-borne Coatings

- Water-borne Coatings

- Powder Coatings

- 100% Solids

- Radiation-Cured

By End-Use Industry

- Oil and Gas and Petrochemical

- Energy and Power Generation

- Infrastructure and Construction

- Chemical Processing and Industrial Plants

- Transportation and Marine

- Metal Processing and Manufacturing

- Water and Wastewater Treatment

- Other Industrial

By Substrate

- Steel and Ferrous Metals

- Concrete and Masonry

- Non-Ferrous Metals

- Plastics and Composites

By Functional Property

- Anti-Corrosive

- Chemical and Acid Resistance

- Abrasion and Impact Resistance

- Thermal and Fire Resistance

- Weather and UV Resistance

By Maintenance Type

- Preventive Maintenance

- Corrective

- Emergency Maintenance

By Sales Channel

- Direct Sales

- Specialty Industrial Distributors

- Professional Service Providers

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Industrial Maintenance Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- RPM International Inc.

- Jotun A/S

- Hempel A/S

- Axalta Coating Systems Ltd.

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Sika AG

- Tnemec Company, Inc.

- Asian Paints Limited

- KCC Corporation

- Belzona International Ltd.

- Teknos Group

*- List not Exhaustive