Market Overview: Growing Demand for Sustainable and Protective Industrial Paper Sacks

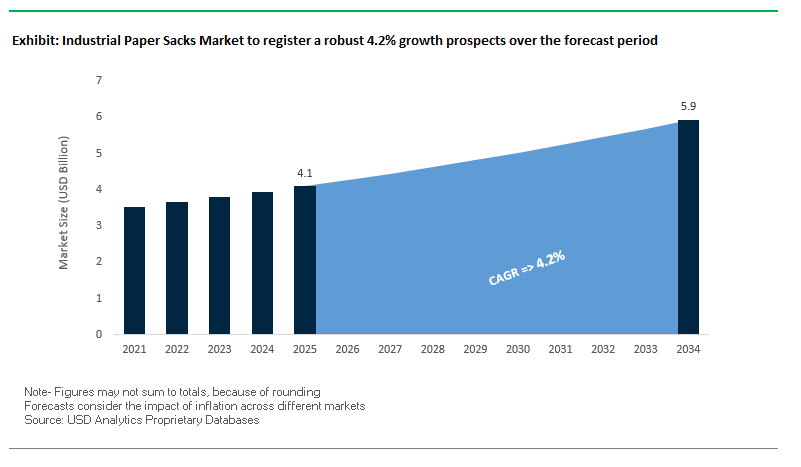

The Industrial Paper Sacks Market is projected to grow from USD 4.1 billion in 2025 to USD 5.9 billion by 2034, advancing at a steady CAGR of 4.2%. Industrial paper sacks are critical packaging solutions across construction, food, chemicals, and agricultural sectors, offering durability, moisture resistance, and product protection in bulk applications. For industry professionals, the key considerations are: how can paper sack manufacturers balance sustainability with performance, deliver moisture-resistant sacks for hygroscopic goods, and scale innovations like Easy Open/Seal features to improve usability in industrial and consumer-facing applications?

Market growth is fueled by the global sustainability push. Industrial paper sacks, made from renewable, recyclable, and biodegradable materials, are increasingly replacing plastic alternatives. Their adoption is also supported by strong performance requirements, particularly for cement, fertilizers, and chemicals, where sack integrity and barrier strength are critical. In parallel, demand from construction and agricultural sectors ensures steady volume growth, while design innovations such as integrated handles and user-friendly seals expand their utility beyond traditional bulk uses.

Key Insights for Industry Professionals:

- Market forecast: USD 4.1B (2025) → USD 5.9B (2034), CAGR 4.2%.

- Eco-friendly alternatives to plastic drive adoption across industries.

- Strong demand from construction, chemicals, food, and agriculture for sack durability and protection.

- Moisture-resistant designs safeguard hygroscopic goods like cement and fertilizers.

- Innovations such as Easy Open/Seal and integrated handles are enhancing usability.

Market Analysis: Recent Developments in Industrial Paper Sacks Industry

The global industrial paper sacks industry is being reshaped by sustainability commitments, material innovations, and high-profile mergers. In August 2025, Smurfit WestRock, formed through the Smurfit Kappa–WestRock merger, partnered with Mindful Chef to deliver fully recyclable packaging with traceability features, underscoring the shift toward paper-based alternatives. In July 2025, the merger of Amcor and Berry Global created another major packaging leader, strengthening the push for flexibles and rigid packaging with lower carbon footprints.

In June 2025, Mondi made two major moves: it launched a water-soluble cement bag in Spain with Cemex, designed to dissolve during mixing and eliminate on-site waste, and also introduced recyclable paper-based packaging for pet nutrition, highlighting versatility in industrial and consumer applications. Meanwhile, in February 2025, Amcor launched its AmFiber Performance Paper stand-up pouch a refill solution for instant coffee that reduces carbon footprint by 73% compared to standard pouches showing crossover innovation in paper packaging.

Smart packaging integration is also on the rise. A report in April 2025 revealed growing demand for QR codes, NFC, and RFID to improve traceability and consumer engagement. Earlier, in September 2024, a report highlighted advances in manufacturing processes and recycled content, improving efficiency and cost competitiveness. In August 2024, Shiseido replaced plastic bubble wrap in e-commerce with honeycomb kraft paper, a move signaling consumer brand adoption of sustainable paper-based solutions.

Transformative Trends and Growth Opportunities in the Industrial Paper Sacks Market

Strategic Shift to High-Performance Microcrepe Paper Structures

The industrial paper sacks market is witnessing a pivotal transition toward microcrepe paper in multi-wall sack designs, replacing traditional extensible kraft paper. This technology leverages a specialized creping process that imparts exceptional elongation, tear resistance, and flexibility, enabling the production of thinner, lighter sacks without compromising durability. Such advancements reduce material consumption, lower transportation costs, and enhance performance during filling and handling.

High-performance microcrepe paper provides enhanced cushioning and mechanical strength, making it suitable for electrical insulation, heavy-duty industrial materials, and specialty applications. Manufacturers like Weidmann Electrical Technology highlight how the unique trough-and-crest structure contributes to superior tear resistance and puncture protection. Case studies demonstrate that sack producers reducing paper grammage experience material and freight cost savings while improving efficiency on automated filling lines by decreasing bag breakage and product spillage.

Specialized applications, such as VCI (Volatile Corrosion Inhibitor) crepe papers from RUST-X, showcase how this technology can be tailored for corrosion protection in metals, highlighting its versatility across industrial and high-value applications.

Integration of Functional Polymer Coatings and Barriers

Beyond paper structure, the integration of advanced polymer coatings and barrier layers is enabling new applications for industrial paper sacks. These include extrusion-coated polyethylene (PE) layers for moisture resistance, specialized barriers for hygroscopic materials, and bio-based polymer coatings to maintain recyclability and compostability while adding critical functionality.

Innovations in bio-based coatings, such as chitosan and cellulose, enhance moisture and oxygen barrier performance while remaining recyclable. Companies like Mondi have developed FunctionalBarrier Paper Ultimate, an ultra-thin coated product offering protection against oxygen, water vapor, and grease, compatible with existing paper recycling streams.

Regulatory developments, particularly PFAS bans in the EU from August 2026, are accelerating the shift to compliant, non-fluorinated barrier coatings, while H.B. Fuller emphasizes the movement away from plastics, positioning coated paper as a sustainable alternative with plastic-like functionality.

Development of Paper Sacks for the Circular Economy of Bulk Goods

A major growth opportunity lies in designing industrial paper sacks optimized for a circular economy, incorporating recycled fibers, recyclable inks, and coatings, along with take-back programs to convert used sacks back into new paper products.

Industry-wide initiatives like the 4evergreen alliance aim for a 90% recycling rate by 2030, with full participation from suppliers, converters, and recyclers. Research by CEPI Eurokraft confirms that used paper sacks enhance pulp strength and improve mill efficiency, demonstrating energy and cost benefits.

Companies like Origin adopt a holistic supply chain strategy, focusing on onshoring and nearshoring production to minimize transport emissions. Additionally, the EU Packaging and Packaging Waste Regulation (PPWR) supports this shift by mandating recyclable packaging and promoting sustainable material use, enhancing the positioning of paper sacks as environmentally responsible packaging solutions.

Smart Sacks with Integrated Traceability and Condition Monitoring

Smart industrial sacks are emerging as high-value solutions for sensitive or high-value goods, integrating QR codes, RFID tags, and printed sensors to monitor impact, humidity, and other critical conditions.

Real-time monitoring by providers like ParkourSC demonstrates the ability to track temperature-sensitive products throughout the supply chain, reducing spoilage and maintaining quality. Companies like Scantrust highlight unit-level traceability via printed QR codes, supporting product recalls, batch verification, and compliance.

Competitive Landscape: Leading Players in Industrial Paper Sacks Market

The global industrial paper sacks market is competitive, led by integrated paper producers, converters, and regional manufacturers focused on scaling sustainable, high-performance sack solutions. Players are advancing through M&A activity, investments in sack kraft capacity, and design features that boost convenience and product safety.

Mondi plc leads with water-soluble cement sack innovation

Mondi has positioned itself as a sustainability pioneer with its vertically integrated model, from forests to sack conversion. In June 2025, Mondi launched the SolmixBag in Spain with Cemex, a cement bag that dissolves completely during mixing, eliminating waste. Its portfolio includes open-mouth and valve bags with Easy Open/Seal features. Through its Mondi Action Plan 2030 (MAP2030), the company commits to “sustainable by design” packaging, with heavy R&D investment in recyclable and mono-material paper solutions.

Smurfit Kappa strengthens with Smurfit WestRock merger

Smurfit Kappa leverages its global paper network to provide multi-ply sacks for cement, flour, and chemicals with high compression strength. In August 2025, the new Smurfit WestRock entity delivered fully recyclable packaging with traceability for a food delivery brand, reinforcing its commitment to sustainability. Smurfit Kappa also invested in honeycomb cardboard as a plastic alternative for void fill in 2023. Under its Better Planet Packaging initiative, the company continues to focus on sustainable and high-performance sack solutions.

Billerud invests in sack kraft and North American expansion

Billerud specializes in sack kraft paper grades like Ad/Vantage Select and Ad/Vantage Speed, designed for high-speed filling and dust-free operations. Its SEK 1.4 billion Evolution Program in North America, highlighted in Q1 2025, includes new coated linerboard production at the Quinnesec mill, boosting profitability by 19% year-on-year. With a strong forestry-based sustainability model, Billerud positions itself as a global supplier of eco-efficient sack kraft materials that replace fossil-based packaging.

Oji Holdings Corporation develops moisture-resistant paper sacks

Oji Holdings, a major Asian player, leverages its vertically integrated supply chain to deliver multi-wall paper sacks for cement, chemicals, and food applications. Its focus lies in moisture-resistant coatings and adhesives that maintain recyclability while improving performance. The company continues to invest in high-performance sack technology, with a strategy centered on expanding in high-growth Asian markets while promoting sustainable alternatives to plastics.

Hood Packaging Corporation custom-engineers sack solutions

Hood Packaging is a North American leader specializing in multi-wall paper bags for food, chemicals, and construction materials. Its offerings include valve bags, sewn sacks, and open-mouth designs, engineered with barrier layers and closures to meet specific industrial requirements. Hood’s competitive advantage lies in custom-engineering capabilities and a strong focus on sustainable product development, making it a preferred partner for customers seeking tailored, high-performance sack packaging.

Industrial Paper Sacks Market Share Insights

Pasted Valve Sacks Dominate Market Share by Product Type in Industrial Paper Sacks

Pasted valve sacks account for 40% of the industrial paper sacks market in 2025, making them the undisputed leader in this category. Their dominance is closely tied to the needs of industries such as building materials, chemicals, and food ingredients, where dust-free filling, automatic closure, and high-speed filling line compatibility are critical for operational efficiency. The valve design eliminates manual sealing steps, reducing labor costs and improving throughput for bulk powders like cement, flour, or pigments. Pinch bottom and sewn open mouth sacks, while more traditional, continue to serve significant demand for coarse or heavy materials such as animal feed and construction aggregates, valued for their durability and adaptability. Block bottom sacks hold a premium niche, offering stability, stackability, and strong shelf presence, making them increasingly attractive for branded food and agricultural products. Other specialty sacks, often multi-wall or with laminated barriers, address moisture-sensitive and industrial niche applications, highlighting the industry’s push towards performance-oriented and application-specific sack innovations.

Building & Construction Sector Leads Market Share by Application in Industrial Paper Sacks

Building and construction represents 35% of the industrial paper sacks market in 2025, reflecting its role as the backbone application segment. The global reliance on cement, plaster, and related dry materials makes this sector the largest consumer, with sacks required to deliver high-speed filling, dust containment, and consistent performance in challenging handling conditions. The construction sector’s volume-driven demand ensures pasted valve sacks dominate here, directly linking market performance to global infrastructure investment cycles. Chemicals and agriculture also form critical markets, with the former requiring barrier-resistant sacks for fertilizers, pigments, and industrial powders, and the latter relying on sewn open mouth sacks for animal feed and seeds that must endure heavy handling and variable storage conditions. The food sector adds high-value demand for multi-wall sacks with food-contact safety and moisture protection, particularly for flour, sugar, starches, and cocoa. Meanwhile, minerals and other industrial goods emphasize strength and abrasion resistance, reflecting the diverse material requirements across bulk commodity sectors.

United States Industrial Paper Sacks Market Shaped by EPR Regulations and Sustainable Innovation

The U.S. industrial paper sacks market is significantly influenced by a fragmented regulatory environment, with state-level Extended Producer Responsibility (EPR) laws driving the shift toward sustainable, fiber-based packaging solutions. Innovations in barrier coatings are enhancing moisture and grease resistance, enabling paper sacks to meet the durability requirements of agriculture, food, and building materials sectors without compromising recyclability.

Corporate investments demonstrate the commitment to sustainability, as seen with International Paper’s launch of recycled paper sacks for the food industry in March 2024. Demand is particularly strong for packaging cement, flour, and animal feed, where stackable, breathable, and durable containers are critical. Sustainability remains a key focus, with a growing adoption of recyclable and compostable solutions that align with environmental regulations and rising consumer expectations.

Germany Industrial Paper Sacks Market Advances with Regulatory Compliance and Circular Economy Leadership

Germany’s industrial paper sacks industry operates under stringent regulations, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, which mandates fully recyclable or reusable packaging by 2030. This has accelerated the adoption of innovative paper sack solutions, including water-soluble cement bags developed by Mondi, which reduce construction waste and dust.

The country’s well-established Packaging Act (VerpackG) promotes circular economy principles by incentivizing recyclable packaging designs. The market is particularly strong in cement, chemicals, and building materials sectors, supported by Germany’s robust manufacturing base. Additionally, regulatory compliance with the EU Deforestation Regulation (EUDR) by December 2025 is pushing manufacturers to ensure responsible sourcing of wood fiber, further strengthening sustainability credentials in the German market.

China Industrial Paper Sacks Market Expands Through Domestic Production and Technological Innovation

China’s industrial paper sacks market is driven by governmental initiatives such as the “dual carbon” goal and the March 2024 Action Plan for Promoting Large-Scale Equipment Updates, which encourage the use of sustainable materials and recycling. Regulatory reforms, including GB/T 31268, address excessive packaging, directly impacting e-commerce and industrial sack applications.

Technological advancements, including automation, AI integration, and the “5G plus industrial internet” approach, are enhancing production efficiency and flexible manufacturing capacity. Domestic substitution of imported technologies is a key trend, as local companies expand production to meet growing demand for high-quality, circular packaging solutions.

India Industrial Paper Sacks Market Fueled by Circular Economy Initiatives and GST Incentives

India’s industrial paper sacks sector is witnessing significant growth due to government policies supporting a circular economy. In September 2025, paper sacks and biodegradable bags were brought under a reduced GST rate of 5%, down from 18%, stimulating adoption in the packaging sector. Technological advancements, including automated production lines and use of agricultural waste like rice straw and wheat straw, are improving efficiency and sustainability.

Corporate investments are increasing to meet local demand, especially in the food processing and cement sectors. The government’s ban on single-use plastics is further driving the market toward eco-friendly alternatives. High-performance paper sacks are now widely adopted to meet domestic and export requirements for durable, stackable, and safe industrial packaging.

Brazil Industrial Paper Sacks Market Strengthened by Sustainable Practices and Advanced Packaging Solutions

Brazil’s industrial paper sacks market is bolstered by government initiatives under the National Solid Waste Policy, promoting domestic recycling programs. Additional regulations are expected to require companies to recycle a significant portion of their products, further encouraging sustainable packaging.

Technological innovation is evident in premium and digital packaging solutions, improving product protection and shelf life. Key applications include cement, chemicals, and agricultural sectors. Corporate investments, such as Klabin’s BRL 188 million expansion at its Horizonte unit in 2023, are enhancing the production of sustainable corrugated and paper-based packaging, positioning Brazil as a growing market for eco-friendly industrial sacks.

Japan Industrial Paper Sacks Market Driven by Precision Manufacturing and High-Performance Innovations

Japan’s industrial paper sacks market benefits from advanced precision manufacturing and next-generation production technologies. Innovations include heat-resistant and self-sealing paper sacks, tailored for construction and specialty chemicals. Regulatory guidance from the Plastic Resource Circulation Act, effective April 2022, promotes environmentally conscious packaging designs and reduces single-use plastics.

The market focuses on high-performance, value-added products with superior barrier properties and specialized functionalities. Japan’s emphasis on quality, durability, and sustainable materials ensures that industrial paper sacks meet the evolving needs of multiple sectors while supporting circular economy initiatives.

Industrial Paper Sacks Market Report Scope

Industrial Paper Sacks Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.1 Billion

|

|

Market Size (2034)

|

$5.9 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Product Type (Pasted Valve Sacks, Pinch Bottom Sacks, Sewn Open Mouth Sacks, Block Bottom Sacks, Other Sacks), By Material (Kraft Paper, Recycled Paper), By Application (Building & Construction, Chemicals, Food, Agriculture, Minerals, Other Industrial Goods), By Capacity (Up to 10 kg, 10–25 kg, 25–50 kg, Above 50 kg)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mondi Group, Smurfit Kappa Group, Billerud AB, Greif, Inc., WestRock Company, Sonoco Products Company, Novolex Holdings, LLC, KapStone Paper and Packaging Corporation, Sealed Air Corporation, International Paper, Georgia-Pacific LLC, Nordic Paper, DS Smith Plc, UFlex Ltd., Klabin S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Paper Sacks Market Segmentation

By Product Type

- Pasted Valve Sacks

- Pinch Bottom Sacks

- Sewn Open Mouth Sacks

- Block Bottom Sacks

- Other Sacks

By Material

- Kraft Paper

- Recycled Paper

By Application

- Building & Construction

- Chemicals

- Food

- Agriculture

- Minerals

- Other Industrial Goods

By Capacity

- Up to 10 kg

- 10–25 kg

- 25–50 kg

- Above 50 kg

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Industrial Paper Sacks Market

- Mondi Group

- Smurfit Kappa Group

- Billerud AB

- Greif, Inc.

- WestRock Company

- Sonoco Products Company

- Novolex Holdings, LLC

- KapStone Paper and Packaging Corporation

- Sealed Air Corporation

- International Paper

- Georgia-Pacific LLC

- Nordic Paper

- DS Smith Plc

- UFlex Ltd.

- Klabin S.A.

* List Not Exhaustive

Methodology

USDAnalytics conducted a comprehensive analysis of the Industrial Paper Sacks Market using a multi-layered methodology that combines primary insights from industry professionals, including packaging engineers, supply chain managers, and sustainability experts, with secondary research drawn from corporate reports, trade publications, regulatory filings, and verified market databases. Market sizing, CAGR, and growth projections were calculated using a blend of top-down and bottom-up approaches, cross-validated with historical shipment data, material consumption trends, and production capacity information. The study emphasizes sustainability, regulatory compliance (such as EU PPWR and PFAS bans), technological innovations including high-performance microcrepe paper, functional polymer coatings, and smart traceability features, as well as regional market dynamics across North America, Europe, Asia-Pacific, and Latin America. Competitive strategies of key players like Mondi, Smurfit Kappa, Billerud, and Oji Holdings were analyzed to assess innovation, circular economy adoption, and product performance, ensuring a robust, professional-grade market outlook for stakeholders seeking actionable insights into industrial and eco-friendly paper sack solutions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.