Insulation Coating Market Size, Thermal Efficiency Demand, and CUI Mitigation Technologies Outlook

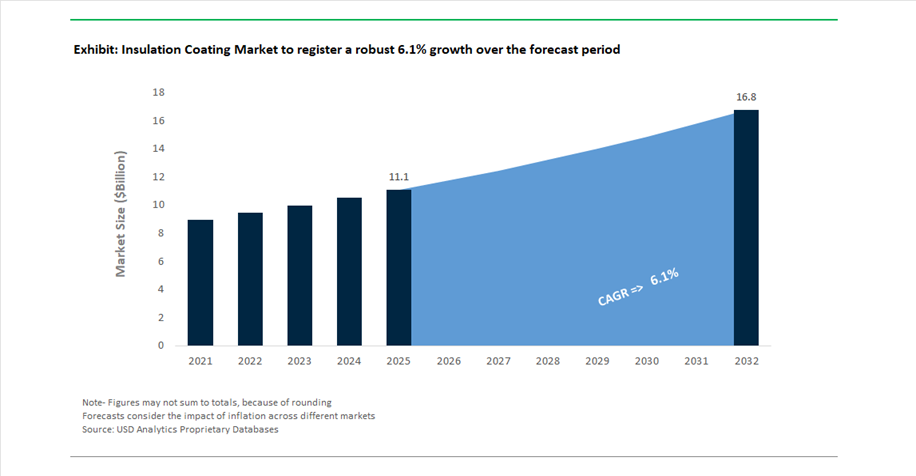

The global insulation coating market was valued at $11.1 billion in 2025 and is projected to reach $16.8 billion by 2032, expanding at a CAGR of 6.1%. This growth is being driven by rising demand for thermal insulation coatings, spray-on insulation (SOI) coatings, energy-efficient coatings, and CUI-resistant coating systems across oil & gas, power generation, construction, marine, and industrial processing sectors. These coatings are increasingly replacing traditional insulation materials due to their ability to deliver thermal resistance, corrosion protection, and space-saving advantages in a single-layer application.

A key market driver is the growing focus on corrosion under insulation (CUI) mitigation, which remains a critical issue in petrochemical and industrial facilities. Conventional insulation systems often create air gaps that trap moisture, accelerating corrosion. In contrast, insulation coatings provide seamless thermal barriers, eliminating moisture ingress and significantly improving asset longevity and maintenance efficiency. Additionally, rising global emphasis on energy efficiency and carbon reduction is boosting adoption of cool roof coatings, radiative cooling coatings, and infrared-reflective insulation technologies, particularly in urban infrastructure and commercial buildings.

The market is also benefiting from the expansion of renewable energy, LNG infrastructure, and high-voltage transmission systems, where advanced insulation coatings are required to manage extreme temperature variations and minimize heat loss. Emerging regions such as Asia-Pacific and the Middle East are witnessing strong growth due to rapid industrialization and infrastructure investments, while North America and Europe continue to lead in innovation, sustainability adoption, and regulatory-driven demand for low-VOC and high-performance insulation coatings.

Spray-On Insulation Innovation, Sustainable Coatings, and Thermal Management Technologies Driving Market Evolution

The insulation coating industry is rapidly evolving, driven by technological innovation, sustainability initiatives, and strategic consolidation among leading players. A notable development occurred in March 2026, when Sherwin-Williams’ Heat-Flex CUI-mitigation system received the Materials Performance Innovation of the Year award, highlighting its dual functionality as both a thermal barrier and corrosion inhibitor. This recognition underscores the growing industry shift toward multi-functional insulation coatings that replace traditional bulky insulation systems.

Market consolidation is also shaping competitive dynamics. In February 2026, AkzoNobel and Axalta announced a proposed merger of equals, expected to combine AkzoNobel’s International® thermal insulation coatings portfolio with Axalta’s industrial energy solutions, creating a strong presence in high-heat and cryogenic insulation coating applications. This move reflects increasing demand for integrated coating systems that address both thermal management and corrosion protection.

Product innovation remains a key growth lever. In August 2025, PPG Industries launched PPG PITT-THERM 909, a silicone-based spray-on insulation coating designed to eliminate air gaps and prevent CUI in petrochemical facilities, directly addressing one of the industry’s most costly maintenance challenges. Similarly, Jotun’s January 2026 upgrade of Jotatemp coatings introduced active thermal management capabilities for offshore environments, enhancing performance under extreme saline and high-temperature conditions.

Sustainability-driven developments are expanding the application scope of insulation coatings. In April 2025, PPG expanded its Cool Roof coating portfolio, utilizing infrared-reflective pigments to reduce urban heat buildup and support compliance with energy efficiency regulations in Europe and North America. AkzoNobel’s May 2025 launch of a radiative cooling coating system in China further demonstrates innovation in urban heat mitigation, capable of reducing surface temperatures by up to 10%. Additionally, Sherwin-Williams’ February 2024 introduction of bio-based insulation coatings reflects growing demand for low-carbon, renewable material solutions aligned with corporate sustainability targets.

Earlier product developments also continue to influence market direction. Hempel A/S introduced Hempatherm IC in March 2024, offering a seamless alternative to traditional insulation systems for industrial applications, while Carboline’s Carbotherm 551, launched in January 2024, combines high-build thermal insulation with heavy-duty corrosion protection for storage tanks. In parallel, Dow Inc.’s 525 kV HVDC insulation coating system represents a breakthrough in electrical insulation technology, enabling higher voltage transmission with reduced heat loss, expanding the relevance of insulation coatings into advanced energy infrastructure.

Aerogel-Based Insulation Coatings Enabling High-Performance Thermal Protection in Space-Constrained Systems

The insulation coating industry is experiencing a significant shift toward silica aerogel-based coatings, particularly in industrial environments where space constraints limit the use of traditional insulation materials. These coatings provide exceptional thermal performance, with conductivity values as low as 0.012 to 0.015 W/m·K, enabling equivalent insulation performance at 50% to 70% lower thickness compared to fiberglass or mineral wool systems. This is especially critical in high-density piping networks, where conventional insulation would require structural modifications to maintain clearance. Aerogel coatings can achieve effective insulation with application thicknesses of just 6 to 8 millimeters, replacing traditional lagging systems of approximately 50 millimeters. In addition to thermal efficiency, these coatings address a major industry challenge—corrosion under insulation—by offering hydrophobic and breathable properties that prevent moisture entrapment. This significantly extends asset lifespan, with estimates indicating service life improvements of up to 15 years. From a safety perspective, aerogel coatings reduce surface temperatures of high-temperature steam lines to below 60°C, ensuring compliance with occupational safety standards while maintaining process efficiency. These combined advantages are positioning aerogel-based coatings as a preferred solution for modern industrial insulation challenges.

Perlite-Filled Epoxy Coatings Advancing Cryogenic Insulation in LNG Storage Systems

The LNG storage sector is increasingly adopting perlite-filled epoxy insulation coatings as a secondary barrier solution in full-containment tanks. These coatings are designed to withstand extreme cryogenic conditions while maintaining structural integrity and thermal performance over long operational lifecycles. Advanced epoxy-perlite systems maintain adhesion and crack resistance at temperatures as low as minus 165°C, ensuring reliable performance during repeated thermal cycling. Unlike loose-fill perlite insulation, which can degrade over time due to settling and moisture ingress, epoxy-bound perlite coatings provide a stable, monolithic barrier that preserves thermal resistance throughout a 30-year design life. These coatings also play a critical safety role, acting as a secondary containment layer in the event of primary tank leakage by delaying heat ingress and providing an additional 4 to 6 hours of response time for boil-off gas management. Application advantages further enhance their value, with plural-component spray systems enabling uniform, joint-free insulation layers that eliminate thermal bridging issues associated with panel-based systems. These capabilities are driving adoption in LNG infrastructure projects where safety, durability, and thermal efficiency are paramount.

US DOE IAC Program Driving Adoption of Ceramic Insulation Coatings in Industrial Facilities

The United States Department of Energy’s Industrial Assessment Centers program is creating a strong opportunity for insulation coatings, particularly ceramic-based systems used to improve energy efficiency in small and medium manufacturing facilities. Under expanded funding initiatives, facilities can access implementation grants of up to 300,000 dollars for energy-saving projects, with insulation coatings frequently identified as a high-impact solution. These coatings are particularly effective for insulating complex geometries such as valves, flanges, and heat exchangers, where traditional insulation is difficult to apply. Performance data indicates that ceramic insulation coatings can reduce radiant heat loss by up to 20%, delivering rapid financial returns with payback periods typically under 18 months. The scale of the program is significant, with over 21,000 industrial assessments completed and approximately 15% recommending liquid-applied insulation solutions. Additionally, workforce development initiatives are training hundreds of engineers annually in thermal performance measurement, strengthening technical adoption and market growth. These factors are positioning ceramic insulation coatings as a key technology in industrial energy efficiency improvements.

EU Energy Efficiency Directive Driving Retrofitting Demand for Insulation Coatings

The revised European Energy Efficiency Directive is creating substantial demand for advanced insulation coatings through mandatory energy audits and retrofit requirements for industrial facilities. Under Article 8, large enterprises are required to conduct energy audits every four years, with updated guidelines mandating detailed thermal assessments using infrared thermography to identify heat losses. These audits are increasingly highlighting uninsulated or poorly insulated surfaces as key areas for improvement, driving procurement of rapid-application coating solutions. Non-compliance carries significant financial risk, with penalties reaching up to 4% of annual turnover, incentivizing immediate implementation of recommended upgrades. The directive also sets ambitious targets for reducing final energy consumption by 11.7% by 2030, which is expected to require retrofitting tens of millions of square meters of industrial infrastructure. Additionally, the introduction of digital product passports is encouraging transparency in material performance and environmental impact, favoring manufacturers that provide verifiable data on thermal conductivity and lifecycle emissions. These regulatory drivers are positioning insulation coatings as a critical component in achieving industrial energy efficiency and sustainability goals.

Insulation Coating Market Share 2025: Thermal Insulation Dominance and Project-Based Services Drive Adoption

Function Insights: Thermal Insulation Leads with Energy Efficiency and Space-Saving Benefits

The thermal insulation segment dominates the insulation coating market with a 48% market share in 2025, driven by increasing demand for energy-efficient coating solutions across industrial and commercial sectors. Thermal insulating coatings, typically formulated with ceramic-filled acrylics or epoxy-based systems, are widely applied on process piping, storage tanks, HVAC systems, and building envelopes to significantly reduce heat loss and improve energy conservation. This directly lowers operating costs and carbon emissions, aligning with global sustainability and decarbonization goals. A major advantage over conventional insulation materials such as fiberglass and mineral wool is the thin-film application capability, achieving effective thermal resistance at just 1–5mm thickness compared to 50–100mm in traditional systems. This makes insulation coatings ideal for complex geometries, irregular surfaces, and space-constrained retrofitting projects. As industries prioritize compact, efficient insulation technologies, thermal insulation coatings will continue to lead market growth.

Sales Channel Insights: Project-Based Service Providers Lead with Turnkey Industrial Solutions

The project-based service providers segment holds the largest 44% share in the insulation coating market in 2025, reflecting the high level of technical expertise required for proper application and performance optimization. Insulation coatings demand precise surface preparation standards such as near-white metal blasting (SSPC-SP10), along with controlled multi-layer application and dry film thickness verification to ensure optimal thermal performance and durability. As a result, industries such as refineries, petrochemical plants, and power generation facilities rely on specialized contractors to deliver end-to-end coating solutions. Additionally, these services are often integrated into planned maintenance shutdowns or plant turnarounds, where insulation coatings are bundled with corrosion under insulation (CUI) prevention and fireproofing systems. This integrated approach improves operational efficiency and minimizes downtime. As industrial projects become more complex and performance-driven, project-based service providers will remain the dominant channel in the insulation coating market.

Insulation Coating Market Competitive Landscape: CUI Mitigation, Energy Efficiency, and Advanced Thermal Barrier Technologies Driving Growth

The insulation coating market is highly competitive, driven by corrosion under insulation (CUI) prevention, energy efficiency mandates, and sustainable thermal barrier solutions. Leading players are focusing on aerogel coatings, heat-reflective systems, and insulation replacement technologies to enhance asset longevity, reduce emissions, and improve operational safety.

Sherwin-Williams leads insulation coating innovation with CUI-eliminating Heat-Flex® AEB technology

The Sherwin-Williams Company is a dominant player in insulation coatings, driven by its Heat-Flex® Advanced Energy Barrier (AEB) technology designed to eliminate traditional insulation systems. This breakthrough coating mitigates corrosion under insulation (CUI) while operating on assets up to 204°C, reducing reliance on mineral wool and metal cladding. A single coat can lower surface temperatures to safe-touch levels, even on assets operating at 148°C, enabling application without shutdowns. The expansion of its Cleveland R&D center supports innovation in “I-removal” strategies, targeting sustainable asset longevity. Its vertically integrated supply chain enables turnkey insulation solutions that reduce carbon footprints across industrial operations. This focus on performance and sustainability strengthens its leadership in insulation coatings.

AkzoNobel advances energy-efficient insulation coatings with solar-absorbing technologies and global scale

AkzoNobel N.V. is strengthening its position in the insulation coating market through sustainability and advanced functional coatings. The company has achieved a 47% reduction in Scope 1 and 2 emissions, supported by hydrogen-powered spray booths and renewable energy manufacturing. It is the exclusive supplier of solar-absorbing wall technologies that integrate thermal insulation with energy generation for commercial buildings. Its International® portfolio includes low-GWP insulation coatings offering up to 30-year durability, particularly strong in the Asia-Pacific region. The ongoing $25 billion merger with Axalta is expected to further enhance its global coatings portfolio. This integration of sustainability and innovation positions AkzoNobel as a leader in next-generation insulation coatings.

PPG strengthens thermal barrier coatings with AI-driven materials and EV battery insulation leadership

PPG Industries is advancing its role in insulation coatings through innovation in thermal barrier technologies and sustainable product development. The company reported $15.9 billion in 2025 revenue, with 43% derived from sustainably advantaged products. It is leveraging AI-driven coating development to create nanocomposite insulation layers that reduce material waste by 15%. PPG is focusing on aerospace and data center applications, where dielectric and heat-reflective properties are critical. It also dominates the EV battery insulation niche, providing intumescent coatings that delay thermal runaway at temperatures above 1000°C. This combination of advanced materials and targeted applications strengthens PPG’s competitive position.

Hempel drives aerogel-based insulation coatings with energy efficiency and sustainability targets

Hempel A/S is enhancing its presence in the insulation coating market through advanced aerogel technologies and sustainability initiatives. Its Hempatherm IC system combines aerogel with acrylic resins to deliver ultra-low thermal conductivity for industrial applications such as steam lines and valves. The company reported strong financial performance with an 18.2% EBITDA margin, positioning it to capitalize on the growing thermal insulation market. Under its “Accelerate to Win” strategy, Hempel aims to enable customers to reduce 50 million tonnes of CO2 emissions by 2030. Leadership changes and strategic focus on energy infrastructure further support its growth trajectory. This integration of innovation and sustainability reinforces its market position.

Mascoat leads niche insulation coating solutions for complex geometries and high-reflectivity thermal protection

Mascoat is a specialized leader in insulation coatings, focusing on industrial and marine applications where traditional insulation is impractical. Its spray-applied coatings address condensation and personnel safety challenges on complex geometries such as valves and flanges. The enhanced WeatherBloc-H system reflects up to 85% of solar heat, supporting cool roof initiatives in North America and Europe. Mascoat is targeting LNG liquefaction markets, where coatings must withstand extreme thermal cycling and cryogenic conditions. Its solutions enable visual inspection of coated surfaces, improving maintenance efficiency. This niche expertise positions Mascoat as a key innovator in specialized insulation coatings.

Jotun integrates insulation and protective coatings for energy-efficient maritime and pipeline applications

Jotun A/S is strengthening its position in the insulation coating market through integrated protective and thermal solutions. The company reported record revenue of NOK 34.33 billion, supported by growth in the Middle East and Asia-Pacific regions. Its updated Jotapipe™ and Marathon coatings incorporate glass-flake reinforced insulation layers, improving barrier efficiency by 15% in high-temperature pipelines. Jotun is integrating insulation coatings with Hull Performance Solutions to deliver combined energy-saving benefits in maritime applications. The company has achieved a 70% reduction in emissions, with plans to reach 90% through localized production. This focus on efficiency, integration, and sustainability enhances its competitive positioning.

United States Insulation Coating Market: Advanced Thermal Barriers and EV Energy Efficiency Driving Growth

The United States insulation coating market is undergoing a significant transformation, shifting from conventional bulky insulation systems toward high-performance thin-film thermal management coatings. This transition is particularly evident across Gulf Coast refining clusters and the rapidly expanding “Battery Belt,” where advanced coatings are being deployed to optimize energy efficiency and reduce asset footprint. Innovations such as liquid-applied energy barrier coatings are replacing traditional mineral insulation, enabling streamlined industrial processes while improving operational efficiency.

Technological advancements in reflective insulation coatings are further enhancing performance, with next-generation “cool roof” technologies delivering improved thermal resistance and energy savings. Regulatory pressures, including stricter VOC standards, are accelerating the adoption of waterborne and high-solids insulation coatings across industrial applications. Strategic investments in domestic manufacturing are also strengthening supply chains, supporting the growth of semiconductor fabrication facilities and high-performance insulation production. Additionally, insulation coatings are gaining traction in electric vehicle thermal management systems, where advanced materials are improving energy efficiency and reducing heat loss in critical components.

China Insulation Coating Market: Green Building Mandates and LNG Infrastructure Expansion

China continues to dominate the global insulation coating market, driven by aggressive green building regulations and large-scale infrastructure expansion. Government mandates are requiring the use of energy-efficient coatings in public infrastructure, particularly in urban centers, where low-emissivity coatings are reducing HVAC energy consumption. These policies are significantly boosting demand for advanced insulation coatings across commercial and residential construction.

The rapid expansion of LNG infrastructure is another key driver, creating strong demand for cryogenic insulation coatings designed to prevent condensation and thermal loss in complex pipeline systems. Technological innovations such as aerogel-based and ceramic-hybrid coatings are enhancing performance by enabling application on high-temperature substrates without operational downtime. Additionally, the integration of phase-change material coatings in smart city projects is improving thermal stability in buildings. China’s strong manufacturing base and continued investments in coating technologies further reinforce its leadership in the global insulation coating market.

Germany Insulation Coating Market: Passive House Standards and Sustainable Thermal Solutions

Germany serves as the innovation hub for insulation coatings in Europe, driven by stringent energy efficiency regulations and the adoption of Passive House standards. The country is prioritizing sustainable building retrofits, particularly in aging infrastructure, where transparent reflective coatings are being used to improve thermal performance without compromising architectural integrity. These developments are significantly increasing demand for advanced insulation coatings in both residential and commercial sectors.

Technological innovation remains a key growth factor, with the development of hybrid acoustic-thermal systems and advanced nanofiber aerogel coatings offering superior insulation performance. Industrial decarbonization initiatives are also encouraging the use of insulation coatings to improve energy efficiency in manufacturing processes, particularly in steam lines and valves. Investments under the EU Renovation Wave are further driving the adoption of fire-safe, non-combustible insulation materials. Germany’s leadership in district heating systems is also contributing to market growth, with liquid coatings being used to seal complex joints and improve system efficiency.

India Insulation Coating Market: Infrastructure Boom and Smart City Cooling Solutions

India is emerging as one of the fastest-growing markets for insulation coatings, supported by strong economic growth and extensive infrastructure development. Government initiatives such as the National Infrastructure Pipeline and tax incentives for energy-efficient housing are driving the adoption of solar-reflective insulation coatings to combat rising urban temperatures. These coatings are playing a critical role in reducing cooling energy demand across residential and commercial buildings.

The industrial sector is also witnessing increased adoption of advanced insulation coatings, particularly in pharmaceutical and food processing industries where temperature control is critical. Investments in manufacturing capacity and supply chain expansion are supporting the growing demand for insulation solutions in cold chain logistics and industrial applications. Additionally, the expansion of metro rail networks is boosting the use of waterborne insulation coatings in elevated stations, enhancing durability and thermal performance. These factors collectively position India as a key growth market in the global insulation coatings industry.

Saudi Arabia Insulation Coating Market: Extreme Climate Solutions and Vision 2030 Megaprojects

Saudi Arabia is a leading market for high-performance insulation coatings in extreme climatic conditions, driven by large-scale infrastructure projects under Vision 2030. Megaprojects such as NEOM and the Red Sea development are utilizing advanced insulation coatings to reduce heat absorption in structural materials, significantly lowering cooling energy requirements. These coatings are critical for maintaining building performance in high-temperature desert environments.

The oil and gas sector is also a major contributor to market growth, with increased adoption of insulation coatings to mitigate corrosion under insulation (CUI) in offshore and onshore assets. Technological innovations such as sand-resistant and UV-stable coatings are addressing the challenges posed by harsh environmental conditions. Investments in desalination and industrial infrastructure are further driving demand for thermal barrier coatings in high-temperature applications. Additionally, sustainability initiatives are promoting the use of bio-based insulation materials, aligning with long-term environmental goals.

Norway Insulation Coating Market: Arctic-Grade Protection and Offshore Thermal Management

Norway leads in specialized insulation coatings designed for extreme cold and offshore environments, particularly in the North Sea energy sector. The country’s focus on retrofitting aging offshore platforms is driving demand for advanced insulation solutions such as sprayable aerogel coatings, which provide high thermal performance without adding significant weight. These coatings are essential for maintaining operational efficiency in harsh marine conditions.

Technological advancements are enabling the development of subsea insulation coatings capable of withstanding high hydrostatic pressure while maintaining low thermal conductivity. Norway’s leadership in hydrogen infrastructure is also driving innovation in insulation materials designed for high-pressure gas transport systems. Regulatory frameworks such as updated NORSOK standards are ensuring high performance and safety in insulation applications. Additionally, the maritime sector is benefiting from anti-icing insulation coatings that reduce energy consumption in cold climates, reinforcing Norway’s position as a leader in advanced insulation coating technologies.

Insulation Coating Market Report Scope

Insulation Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.1 Billion

|

|

Market Size (2032)

|

$16.8 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Type (Acrylic, Polyurethane, Epoxy, Silicone, Yttria-Stabilized Zirconia, Mullite, Specialty Resins), By Technology (Water-borne Coatings, Solvent-borne Coatings, Powder Coatings, Nano-technology Based), By Function (Thermal Insulation, Corrosion Under Insulation, Personnel Protection, Anti-Condensation, Electrical Insulation, Acoustic, Fire Resistance), By End-Use Industry (Industrial, Building and Construction, Automotive and Transportation, Aerospace and Defense, Electronics and Appliances), By Temperature Range (Cryogenic, Low-to-Mid Temperature, High Temperature, Ultra-High Temperature), By Sales Channel (Direct Sales, Specialty Industrial Distributors, Project-based Service Providers, Retail)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Jotun A/S, Mascoat, Carboline, Hempel A/S, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Cabot Corporation, Tnemec Company, Inc., ThermaCote, Inc., Syneffex Inc., Temp-Coat Brand Products, LLC, Superior Products International II, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Insulation Coating Market Segmentation

By Type

- Acrylic

- Polyurethane

- Epoxy

- Silicone

- Yttria-Stabilized Zirconia

- Mullite

- Specialty Resins

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Powder Coatings

- Nano-technology Based

By Function

- Thermal Insulation

- Corrosion Under Insulation

- Personnel Protection

- Anti-Condensation

- Electrical Insulation

- Acoustic

- Fire Resistance

By End-Use Industry

- Industrial

- Building and Construction

- Automotive and Transportation

- Aerospace and Defense

- Electronics and Appliances

By Temperature Range

- Cryogenic

- Low-to-Mid Temperature

- High Temperature

- Ultra-High Temperature

By Sales Channel

- Direct Sales

- Specialty Industrial Distributors

- Project-based Service Providers

- Retail

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Insulation Coating Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Jotun A/S

- Mascoat

- Carboline

- Hempel A/S

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Cabot Corporation

- Tnemec Company, Inc.

- ThermaCote, Inc.

- Syneffex Inc.

- Temp-Coat Brand Products, LLC

- Superior Products International II, Inc.

*- List not Exhaustive